Recession! Canada’s Property Crash Hit 20%. 3 Conditions That Would Break Australia | APS159

Canada has officially entered a recession. Home prices have dropped roughly 20% from their peak. The apartment market in Toronto is frozen. Unemployment hit 7.1%. And the population has been shrinking for three straight quarters, something that hasn’t happened since 1951. Now here’s what makes this relevant to you: Canada and Australia look almost identical on paper. Commonwealth nations, immigration-heavy economies, resource exporters, and both saw property prices take off after the pandemic. So the question a lot of people have been wanting to ask but don’t want to face is this: is Australia next? I spent two weeks digging through the data from both countries. What I found was far more complicated than I expected.

How Canada Fell Apart

Let’s start with the economy. Statistics Canada confirmed on May 29 that GDP shrank for two consecutive quarters, the textbook definition of a recession and the first one since 2020. Three of the last four quarters showed contraction. Trump’s tariffs hit hard: 50% on steel and aluminium, 50% on copper, and more on lumber. Business investment dropped for five straight quarters, and export expectations were cut in half. For the full year 2025, Canada’s GDP growth came in at just 1.7%, the slowest since the pandemic. The patient says they’re fine, but the test results tell a completely different story.

What about Australia? Q1 GDP came in at positive 0.3%, marking 18 straight quarters of growth. That sounds decent until you look inside. Strip out the big data centre projects, and growth was close to zero. HSBC economists flagged that Q2 could actually turn negative. Total GDP is going up, but per capita GDP is going down because the population is growing faster than the economy. Australia isn’t in recession yet, but the edge is getting closer.

Now look at unemployment. Canada’s rate peaked at 7.1% before pulling back to 6.6% in May. Don’t be fooled by one good month. In the first two months of the year, Canada lost close to 110,000 jobs. Youth unemployment is sitting at 13.4%, with long-term unemployment well above the long-run average. This generation of young buyers simply isn’t there.

Australia’s unemployment is at 4.5%, a four-year high, and the RBA expects it to keep climbing. That still looks manageable next to Canada, but here’s what most people don’t realise: Canada was also sitting in the low 4s before it climbed all the way to 7.1%.

So what about property prices? Canada’s national benchmark dropped about 20% from the 2022 peak, from C$840,000 down to C$667,000. But May sent a signal: the average crossed C$700,000 for the first time in 23 months, up 1.5% year on year. The market is finding a floor. The worst damage is in Toronto, where apartment prices dropped more than 9%.

Australia? Prices went up 8.6% in 2025, but growth has clearly slowed down. May’s national index came in flat month on month, the weakest reading in a year. Perth led the country with 26% annual growth. Sydney sits 2.1% below its peak, Melbourne is down 2.9%, and the gap between Perth and Melbourne hit 24%, a new record. It’s the same lesson as Canada: the national average tells you very little. What matters is which city your property is in.

So the economy, unemployment, and prices look somewhat similar on the surface. But the apartment market crash is where Canada’s story turns ugly, and it has echoes of something we've seen here before.

The Apartment Crash and the Supply Divide

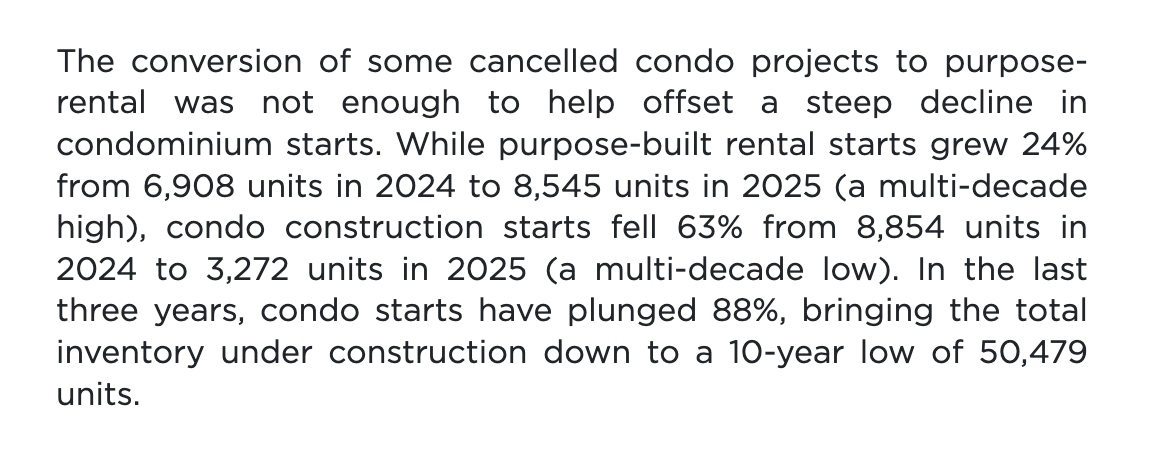

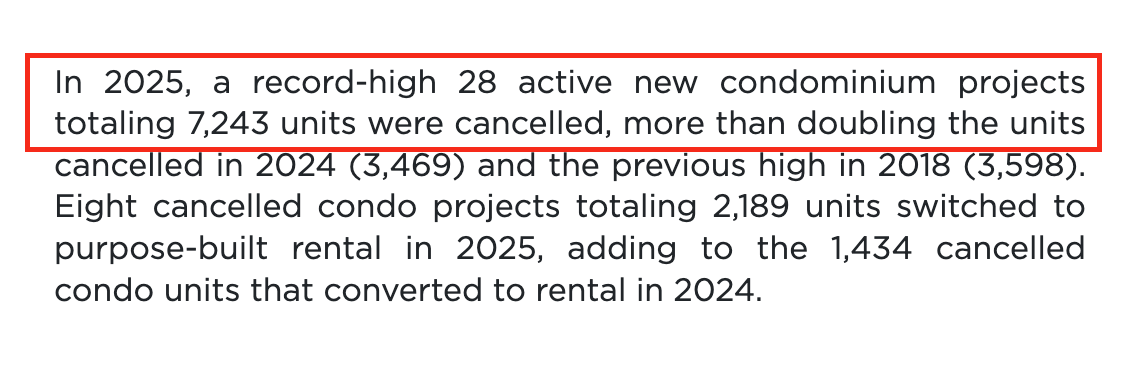

Toronto sold just 1,599 new apartments in 2025, the lowest since 1991, and more than 90% below the 10-year average. Construction starts collapsed 88% over three years. Twenty-eight projects were cancelled, wiping out over 7,000 units. Investors who bought pre-sales near the peak at C$1 million are now looking at a market value of around C$700,000. That’s C$300,000 gone on a single unit.

And here’s the part most people miss: that 88% drop in construction starts means there will be almost no new apartments coming through after 2029. Today’s crash is creating tomorrow’s shortage. This story looks a lot like the off-the-plan wave in Sydney and Melbourne between 2014 and 2016.

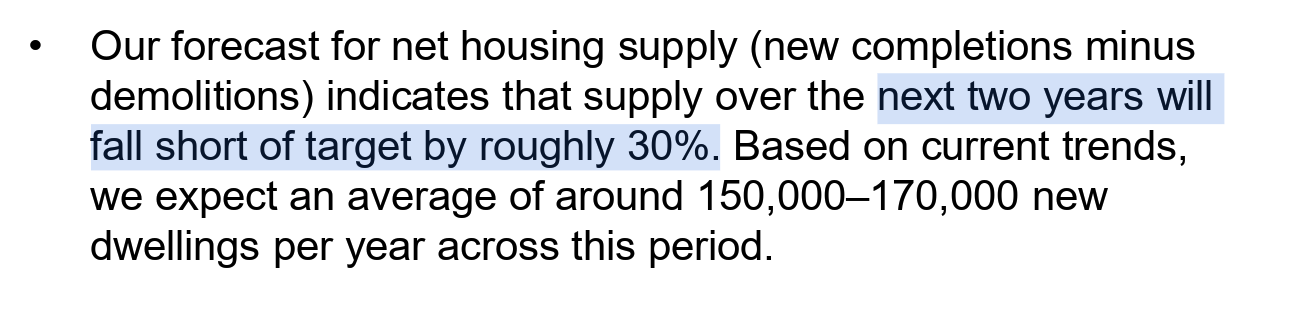

Now flip to Australia. It’s the complete opposite. There’s no oversupply. There’s a structural shortage of more than 200,000 homes. The 1.2 million home target under the National Housing Accord is expected to fall short by about 260,000 homes, and KPMG forecasts new supply will come in 30% below target. Vacancy rates are around 1%. In Perth, it’s just 0.7%. Canadian rents have been falling for 20 straight months. Australian rents are still going up, 5.7% and climbing. One country built too many apartments it can’t sell. The other can’t build enough houses to keep up. That’s not a small difference.

Mortgages and Immigration

Now let’s dig into what’s really driving both markets.

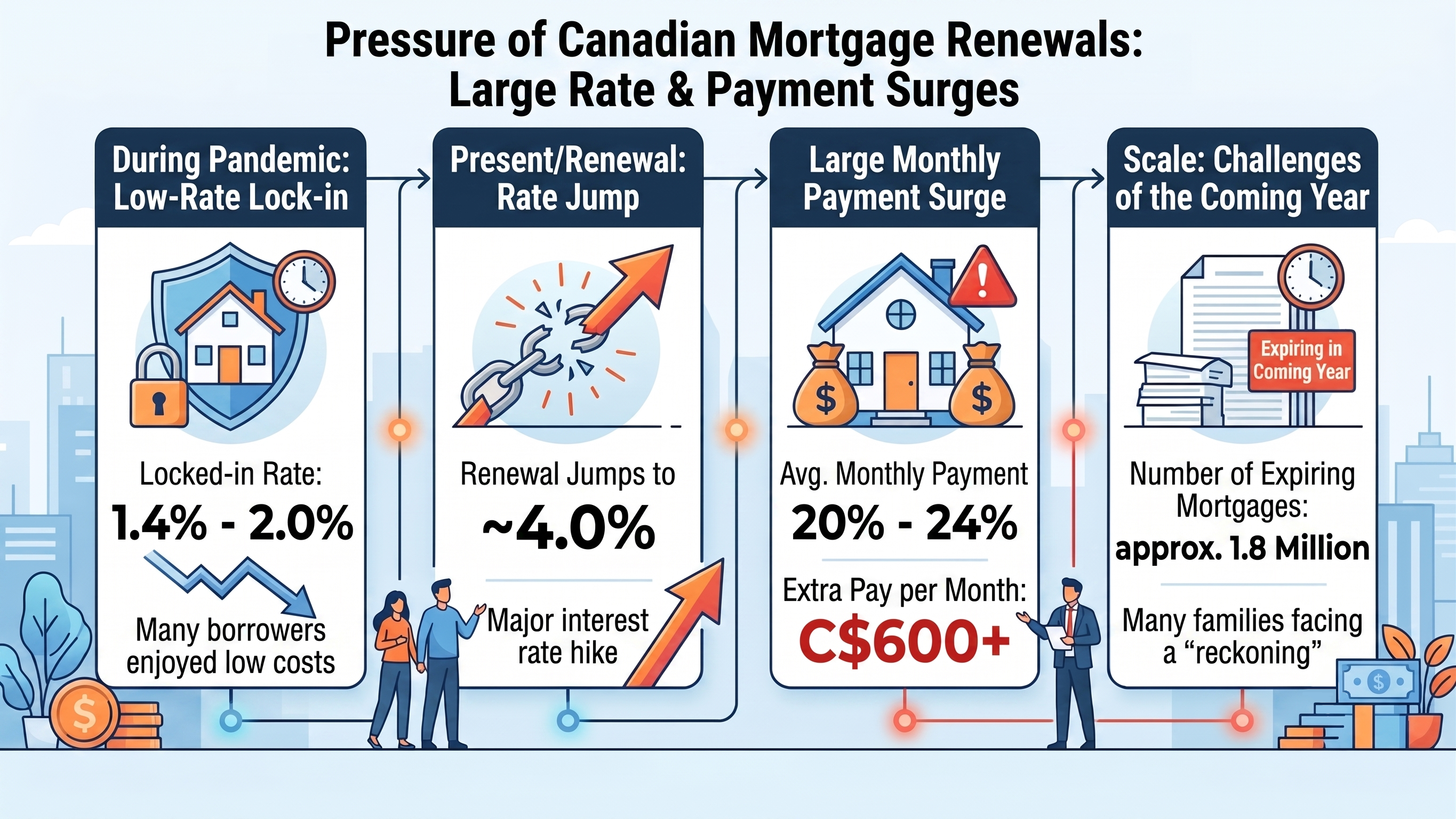

In Canada, 60% of all mortgages come up for renewal between 2025 and 2026. During the pandemic, borrowers locked in rates between 1.4% and 2%. On renewal, those rates jump to around 4%, and monthly repayments go up by 20% to 24%, roughly C$600 extra every month. About 1.8 million mortgages will roll over in the next year. To put that in perspective, that’s roughly the same as the total number of homes in all of Melbourne.

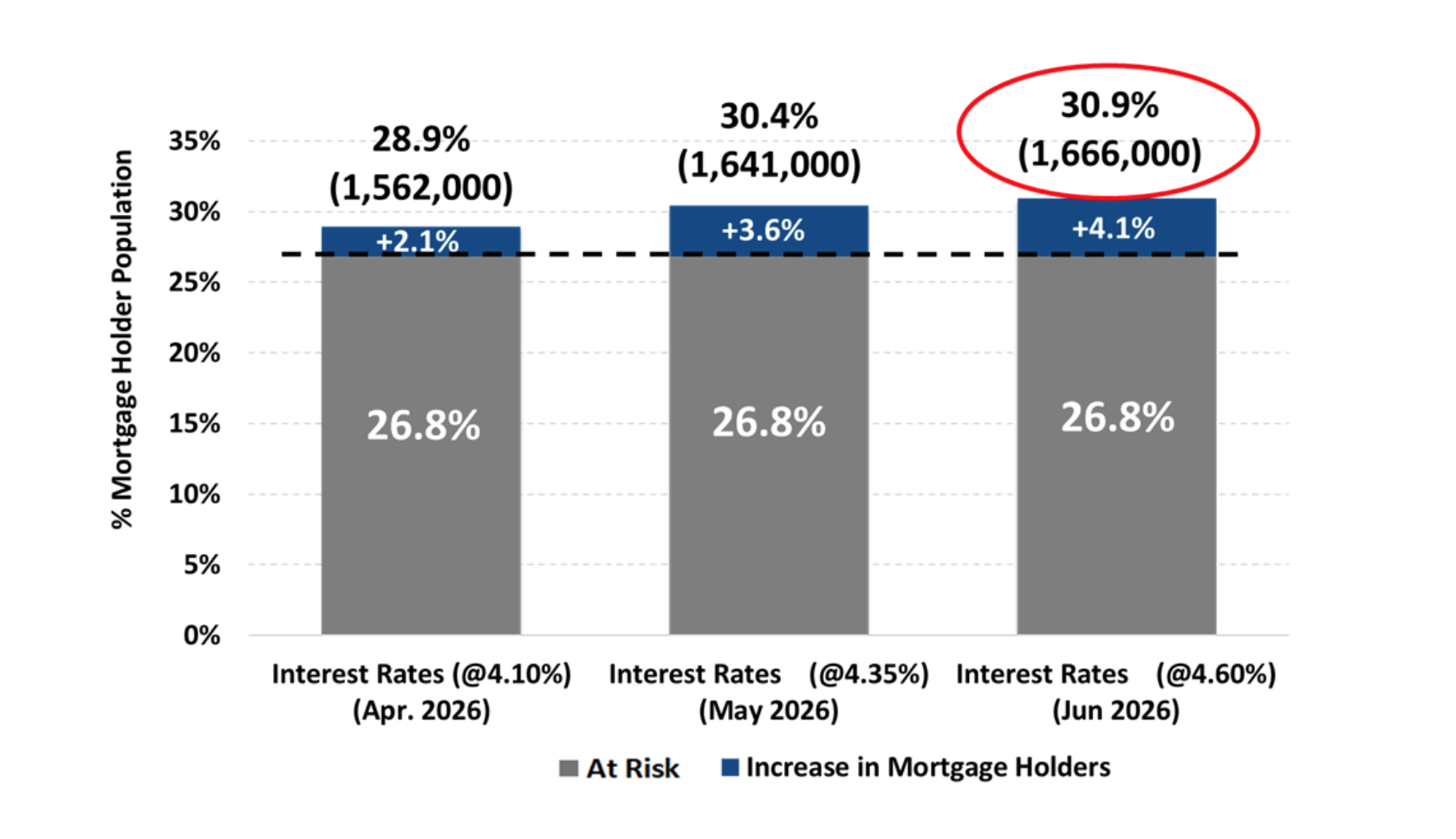

Australia’s mortgage stress is building up too, with 26.8% of borrowers sitting in a high-risk zone. But the mechanics work differently. Australia runs on variable rates, so when rates move, you feel it straight away. The pain arrives gradually, and you have time to adjust. Canada runs on five-year fixed terms, so on renewal day the entire increase hits at once. Neither system is great. But at least in Australia, you won’t see 1.8 million people all getting hit with the same shock on the same day.

Then there’s immigration, the engine behind both economies. Canada’s population fell for three straight quarters. Student visas were cut by 49%. Prime Minister Carney himself admitted that weak GDP growth is directly linked to cutting migration. When you open the doors, infrastructure can’t keep up. When you close them, the economy can’t keep up. That’s what depending on immigration looks like.

Australia? It’s a completely different story. Annual population growth is over 410,000, and net overseas migration sits at about 300,000. The government actually revised the forecast upward, not down. Canada said it would cut immigration and followed through. Australia said it would cut and then quietly bumped the target up by 35,000. Australia watched what happened to Canada and decided not to make the same mistake.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

Australia’s Variables

That covers six comparisons, but Australia has a few variables that Canada simply doesn’t have.

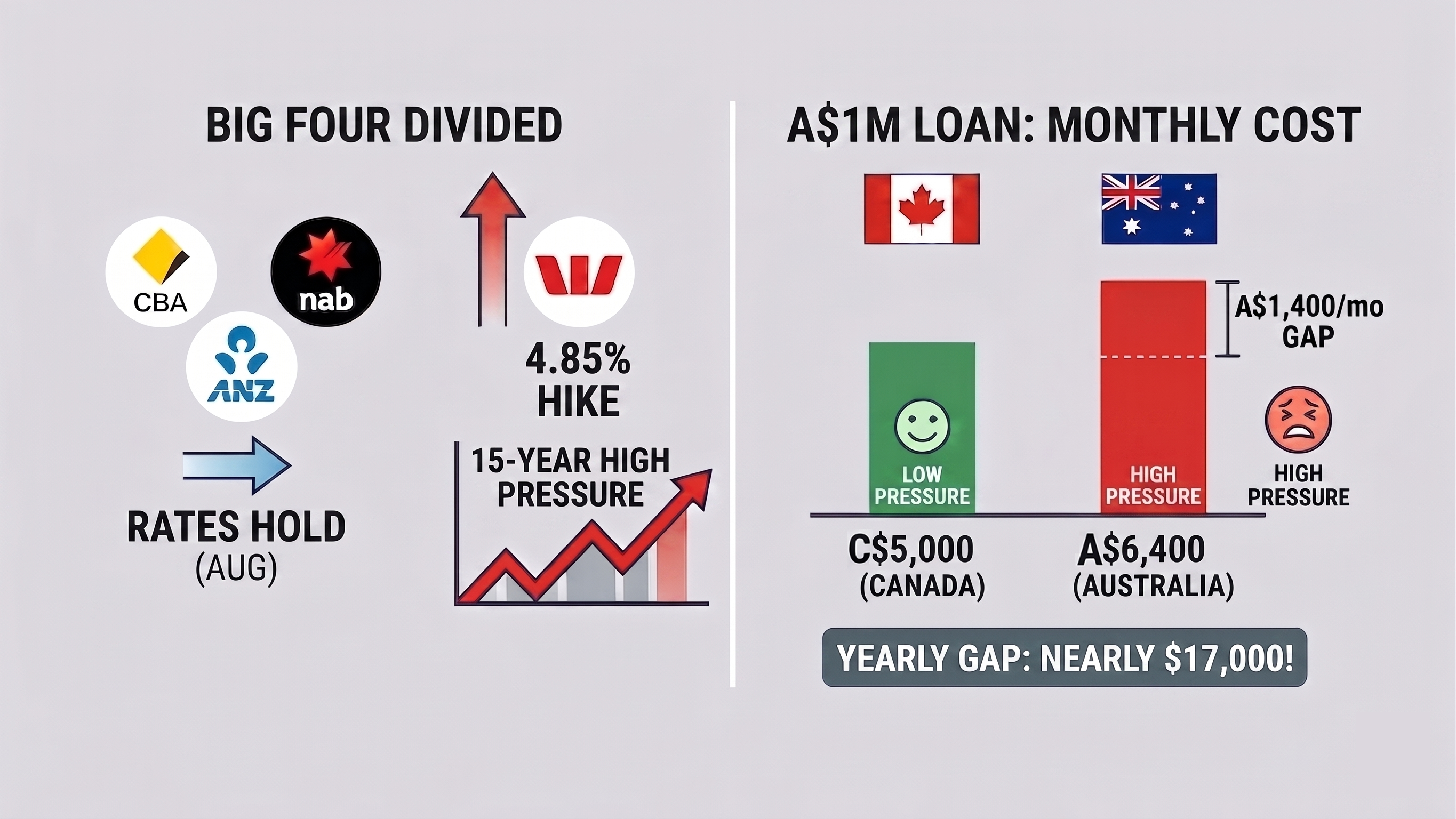

Interest rates are heading in completely opposite directions, and this is the key to the whole story. The Bank of Canada is at 2.25%, leaning towards cuts. The RBA raised rates three times in 2026, pushing the cash rate from 3.85% up to 4.35%, completely undoing the 2025 cuts. Inflation hasn’t come down, with April CPI still at 4.2%. The conflict in the Middle East pushed Brent crude to US$126 a barrel, and those costs have flowed straight through to your power bills and your fuel. Governor Bullock put it this way on June 16: “If we need to raise again, we will.”

The big four banks are split. CBA, NAB, and ANZ expect a hold in August. Westpac forecasts two more hikes to 4.85%. On the same A$1 million loan, monthly repayments in Australia come to about A$6,400 compared to around C$5,000 in Canada, a gap of nearly A$17,000 a year. Australian borrowers are paying more every single month.

But here’s the real story. If you take away one number from this episode, make it this: Canada has an apartment oversupply of 20,000 plus units. Australia has a housing shortage of more than 200,000. Approvals are up 10.2% year on year, but it takes 12 to 18 months to get from approval to completion, and building high-density simply doesn’t pay at current costs. A vacancy rate of 1% means just one in every 100 rental homes is sitting empty. When demand keeps outstripping supply like that, prices have a floor. That is Australia’s moat.

Will Australia Crash?

Now let’s put all of this together. Affordability in both countries is almost identical. Sydney ranks second in the world behind Hong Kong in the Demographia survey, with a median multiple of 14 times income. Mortgage repayments eat up about 46% of household income. Young people in both countries can’t afford to buy, and that pressure feels the same.

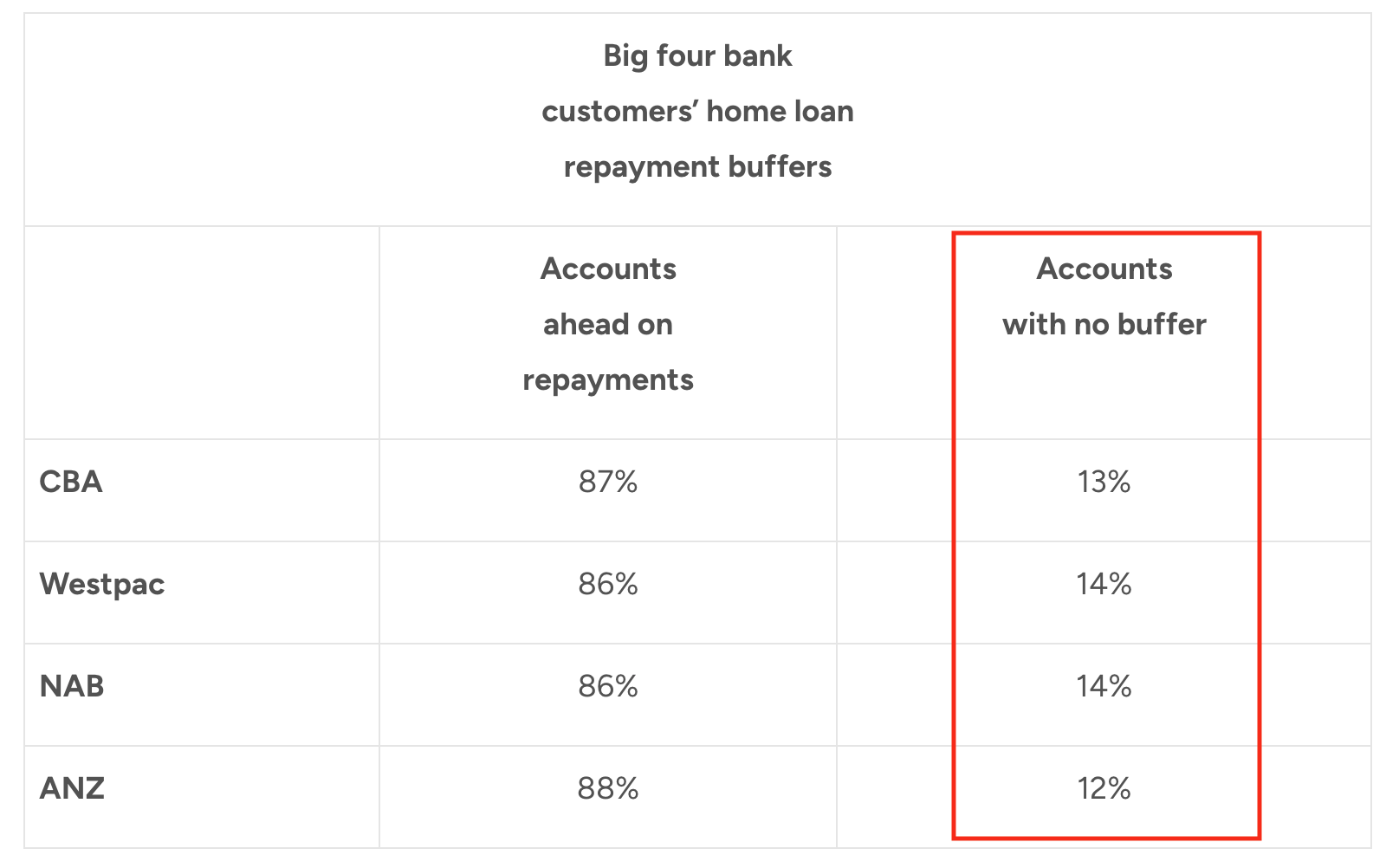

But affordability is a pressure gauge, not a trigger. The real triggers are different, and here are the ones to watch. Canstar data shows about 13% of big-four bank mortgage customers have no buffer left at all. The market will be a lot different after 1 or 2 more interest rate hikes. Sydney is 2.1% below its peak and Melbourne is down 2.9%. Now Canada’s national crash also started from its two biggest cities with drops exactly this size before it picked up speed. If those falls spread to Brisbane or Adelaide, the whole “supply holds up prices” story could start to crack.

I’m not saying Australia’s property market is bulletproof, but I am saying the three conditions that broke Canada don’t exist here right now. Unemployment would need to spike above 7%, and it’s at 4.5%. The RBA would need to push rates to 4.85% or higher, we are at 4.35% now. And 200,000 homes would need to show up out of thin air overnight. The chance of all three lining up at once is very low. The data tells us the risk is real but not imminent.

The more likely outcome is a split market. Sydney and Melbourne drift sideways or keep falling slowly. Brisbane and Perth slow from rapid growth to moderate growth. CBA is forecasting a flat national market for 2026. KPMG forecasts houses up 7.7%. Both are major institutions with rooms full of analysts, and they’re 8% apart. If the experts can’t agree, you and I shouldn’t pretend we’ve got it figured out from the couch.

What Should Investors Do?

Canada’s crash came from multiple failures hitting at once: immigration cut too fast, the economy shrank, apartments were overbuilt, and mortgages all came up for renewal in the same window. Australia doesn’t have any of those at Canada’s level right now. But that doesn’t mean you sit back and ignore the signals.

Here’s what to watch: unemployment breaking through 5% and still climbing, the RBA hiking again, auction clearance rates staying below 50%, vacancy rates going above 2%, and price falls in Sydney and Melbourne spreading to Brisbane or Perth. If those two cities start falling as well, that’s the real warning sign. Also keep an eye on how the market reacts once negative gearing and CGT reforms land.

On strategy, stay away from apartments and high-density products, and look for scarcity. Perth has a 0.7% vacancy rate, Brisbane 0.9%, and both have genuine supply pressure behind them. Put cash flow and capital safety first, because rates could go higher or stay high for longer, and your portfolio needs to hold up even in a worst-case scenario. And every time someone tells you Australia will end up just like Canada, ask them one question: are the supply and demand fundamentals the same?

Canada’s market is already finding a floor, and that shows markets have a way of self-correcting. Australia hasn’t reached that point. As long as immigration continues and supply stays short, there is a floor under this market. But property investment is 50% about location. Which city, what type of home, and what structure you hold it in are what drive your result.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs