I Ran 16,000 Simulations on Australian Property. The Result Shocked Me | APS161

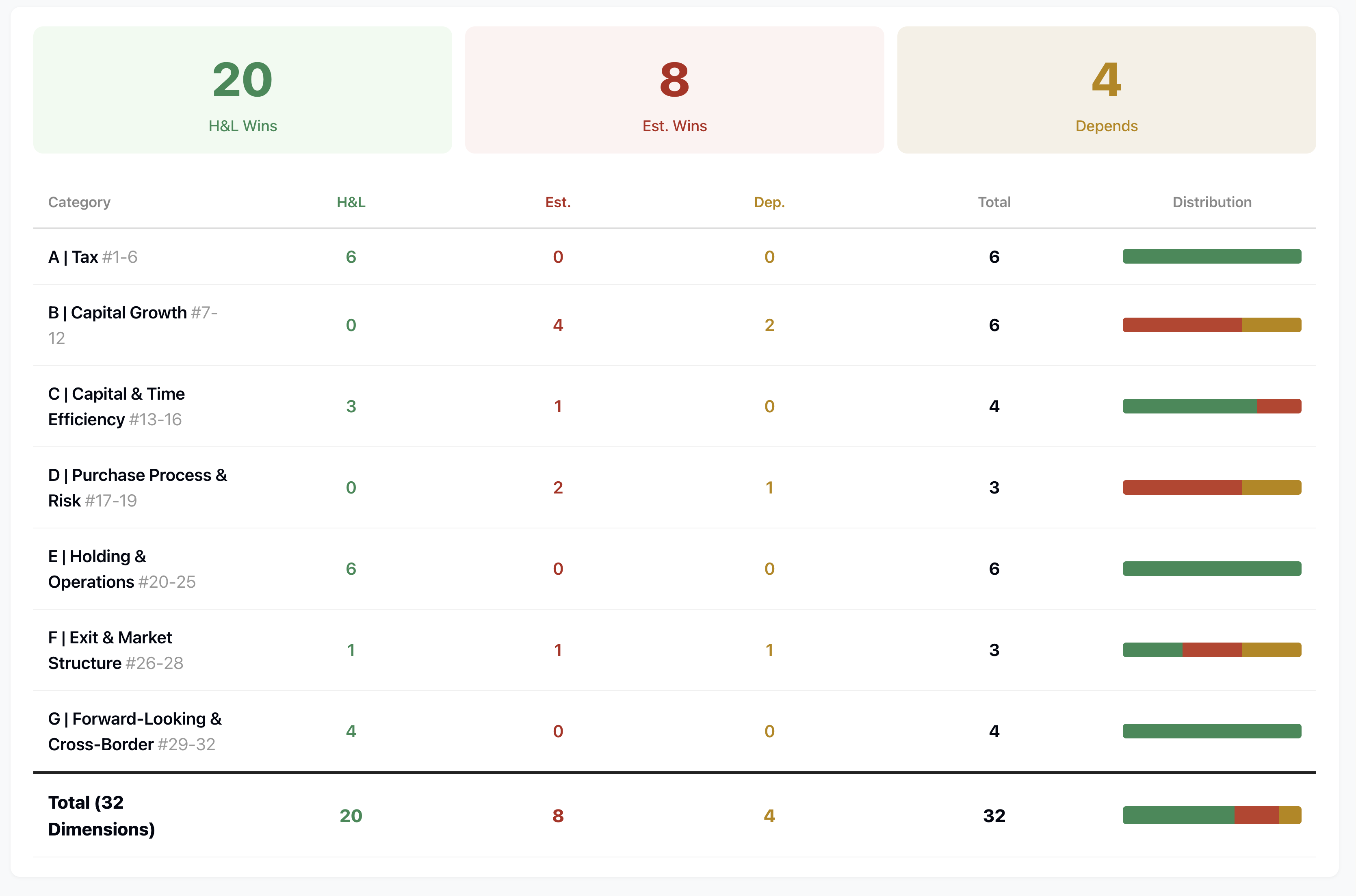

Under the new tax rules, dollar for dollar, house and land packages will, in most cases, deliver a clear after-tax advantage over their entire holding period. That’s not an opinion. It’s a conclusion I got from quantitative modelling across 32 dimensions, four price tiers, and a full lifecycle framework. Of those 32 dimensions, house and land won 20. Established houses won 8. Four were a draw. On the 6 tax dimensions, house and land won all 6 to nil. Over 10 years, the tax gap alone runs into tens of thousands, sometimes over $100,000. This is the complete opposite of what you’ll hear from most buyer’s agents, self-proclaimed experts, and former finance executives who’ve switched into property. Can they really not do the maths? Or do they know the answer and are telling you the opposite on purpose?

Today I’m laying out all the data, logic, calculations, and results for you to see. We’ll walk through every part of this comparison and work out whether house and land or established houses are the better investment. This one’s longer than usual. It’s our analysis framework under the new tax laws, and if you have any interest in Australian property investment, I’d strongly suggest watching it right through to the end. When anyone can put out a short video and say whatever they want with zero accountability, this kind of deep analysis is hard to come by.

Why This Video

The 2026-27 Federal Budget’s CGT reform and negative gearing quarantine passed both houses on June 25th and received Royal Assent on the 26th. It’s law. It takes effect July 1st 2027. You’ve got 12 months.

During those 12 months, every established investment property you buy in your personal name will have its negative gearing permanently quarantined. It can’t offset your other personal income. For CGT, you’re locked into the indexation method plus a 30% minimum tax rate. This isn’t a one-year thing. It affects the entire time you hold that property. These 12 months are your decision-making window.

After the Budget, plenty of buyer’s agents told you “don’t worry, the impact is small, tax is just one variable.” Really? CBA senior economists Saunders and Clarke worked out that losing the immediate offset from negative gearing hits cash flow by the equivalent of a 0.9% to 1.55% interest rate increase. Right now the mortgage rate is around 6.5%. Stack that on top and your holding cost feels like 7.5% to 8%. Over 10 years, that gap adds up to $80,000 to $135,000. And you’re going to tell me that’s “just one variable”?

It gets worse. Some buyer’s agents got a basic fact wrong. They thought companies weren’t affected. They are. After July 1st 2027, residential property losses that aren’t grandfathered cannot offset a company’s other business income. So these buyer’s agents are making investment recommendations worth hundreds of thousands of dollars based on incorrect information. I’m not talking about the top-tier buyer’s agencies with proper research depth and professional ethics. I respect those operators.

Now let me give you a sense of the research behind this. Our team went through both pieces of legislation in full, the Treasury Laws Amendment (Tax Reform No. 1) Act 2026 and the Income Tax Rates Amendment (Tax Reform No. 1) Act 2026. Not news summaries. The actual law. We built a knowledge base of over 7,000 lines and cross-referenced analysis from economists at all four major banks. We studied professional reports from over a dozen law firms and accounting practices including PwC, Baker McKenzie, Holding Redlich, and Pitcher Partners, and ran tens of thousands of simulations.

Holding Redlich classified this as the most significant structural tax change in 25 years. So why hasn’t anyone done a full lifecycle comparison of house and land versus established? Because it takes expertise in three things at once: tax law, the property market, and financial modelling. Buyer’s agents understand property but not tax law. Accountants understand tax law but not property. Most people can’t build models. Our team has all three, so we had to be the ones to do it.

Before I ran the model, I didn’t have a definitive answer either. I knew the new rules were bad for established houses, but not by how much. After finishing the full comparison, the result was more one-sided than I expected.

Take the time value of negative gearing for example. If your property loses $8,000 a year, the $8,000 refund you get this year is worth far more than $8,000 you can only use in a decade. Time steals that money from you. Then there’s maintenance. The model showed new-house maintenance over 10 years totalled about $8,000. Established house? $36,000. That’s a $28,000 gap most people never think about when they’re making an investment decision.

What concerns me even more is cognitive bias. Content creators latch onto one negative point about house and land in their short videos, and their audience ends up with the Horn Effect, where one bad feature colours your view of everything.

Or the Need for Cognitive Closure, where you grab the first negative signal and lock in a verdict. Or Black-and-White Thinking, where it’s all good or all bad. Once people lock into that thinking, they won't budge. It’s a textbook sales technique. That’s one reason I did this analysis. If you haven’t seen a detailed comparison, you could end up making a decision that costs you real money.

This video is the highlights version. The full breakdown will be put together for VISION Gold Members and AusPropertyStrategy Masterclass students. But the highlights are free. Why? If you don’t have a basic analytical framework, membership won’t help you. I want you to see the big picture. I’d rather you watch this and not become a member than get misled and spend hundreds of thousands on the wrong property.

Save this video and come back to it. I’m not making this to prove I’m always right. I’m human and there will be things I’ve missed. If you spot a data error, a gap in the logic, or a dimension I haven’t thought of, leave a comment. I’ll put out a correction video. The people who can be corrected are the ones worth trusting.

Right. Background covered. Now let’s get into it.

We’re looking at one scenario: buying a residential investment property in your personal name after July 1st 2027. Not trusts, companies, or SMSFs. Not properties bought during the transition period. July 1st 2027 is when the new rules fully kick in. It’s the cleanest scenario to explore.

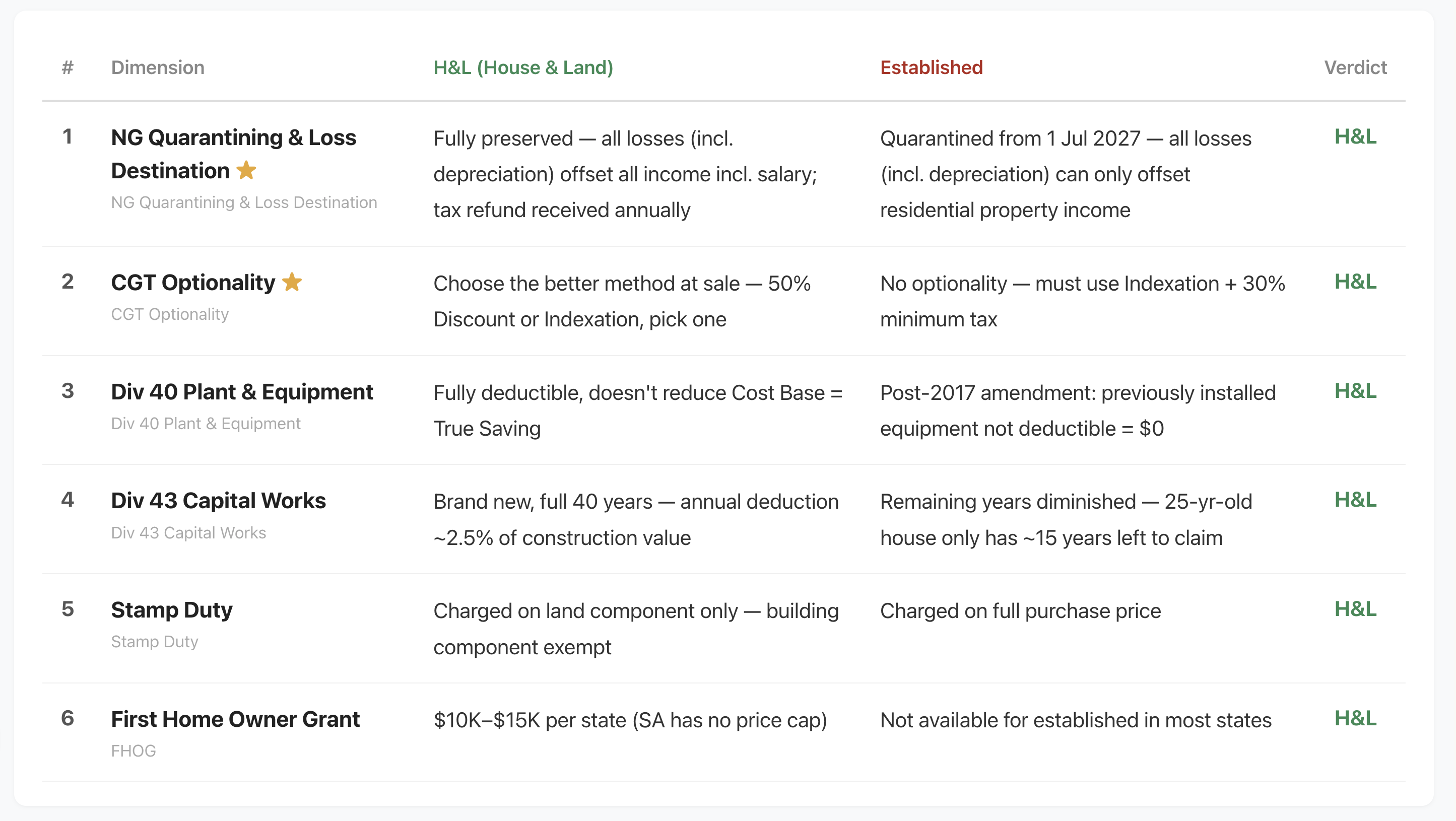

A. Tax Dimensions

After July 1st 2027, if you buy an established residential investment property in your personal name, negative gearing is gone. CGT switches to the indexation method plus a 30% minimum rate, which in many scenarios hurts established properties. Depreciation is still available for established houses, but only against residential rental income or capital gains when you sell, and the Division 40 and Division 43 entitlements are far less than for new builds. Stamp duty on established houses is charged on the full contract price. House and land is charged only on the land component. First-home owner grants almost always favour new builds. Across all 6 tax dimensions, house and land win outright. This is the overview, though. In practice, location, lending, inflation, and interest rates all need individual consideration. We’ll get to those.

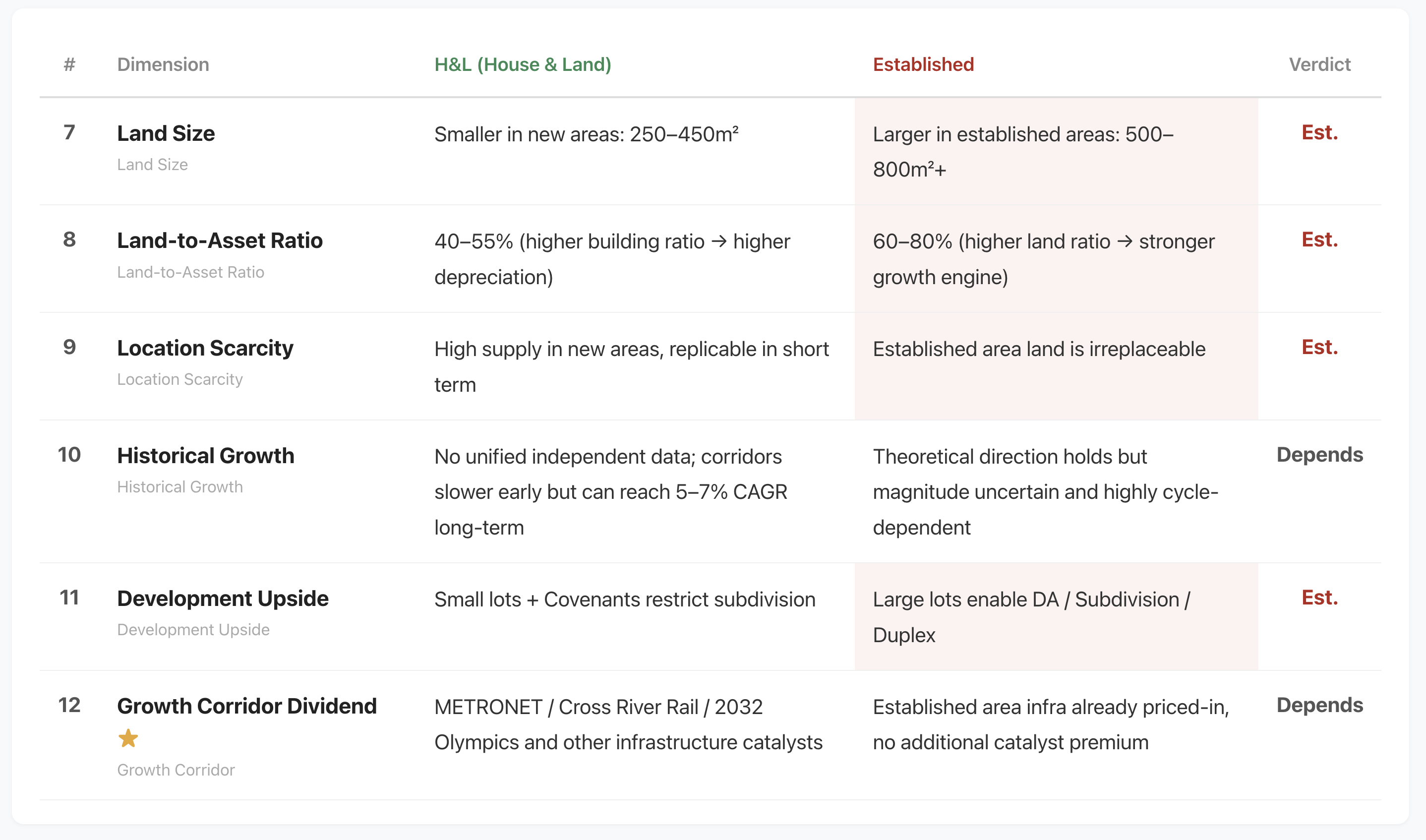

B. Capital Growth Dimensions

Before doing the maths, most people assume established houses grow faster. When you break it down, the answer is, it depends.

Buyer’s agents argue that houses in established areas have larger blocks, higher land-to-value ratios, and therefore better growth. That principle holds up, but only when you’re comparing within the same suburb. Land-to-value ratio is one factor in growth, and growth is one-sixth of the return equation. Capital appreciation, CGT, tax refunds, rent, holding costs, stamp duty, and leverage efficiency all matter. Drawing a conclusion from one factor alone means the homework wasn’t done. New areas do have more supply, and established areas do have land scarcity. But many new areas also have stronger demand, and over time what was once the urban fringe turns into a mid-ring suburb. Look at Kellyville in Sydney.

A few large buyer’s agencies claim their research shows new suburbs grow slower historically. But you have to ask how that data was pulled together, whether it was cherry-picked, and whether there are conflicts of interest. The data we use in the research comes from banks, universities, and federal government agencies. The independent conclusion is “it depends.”

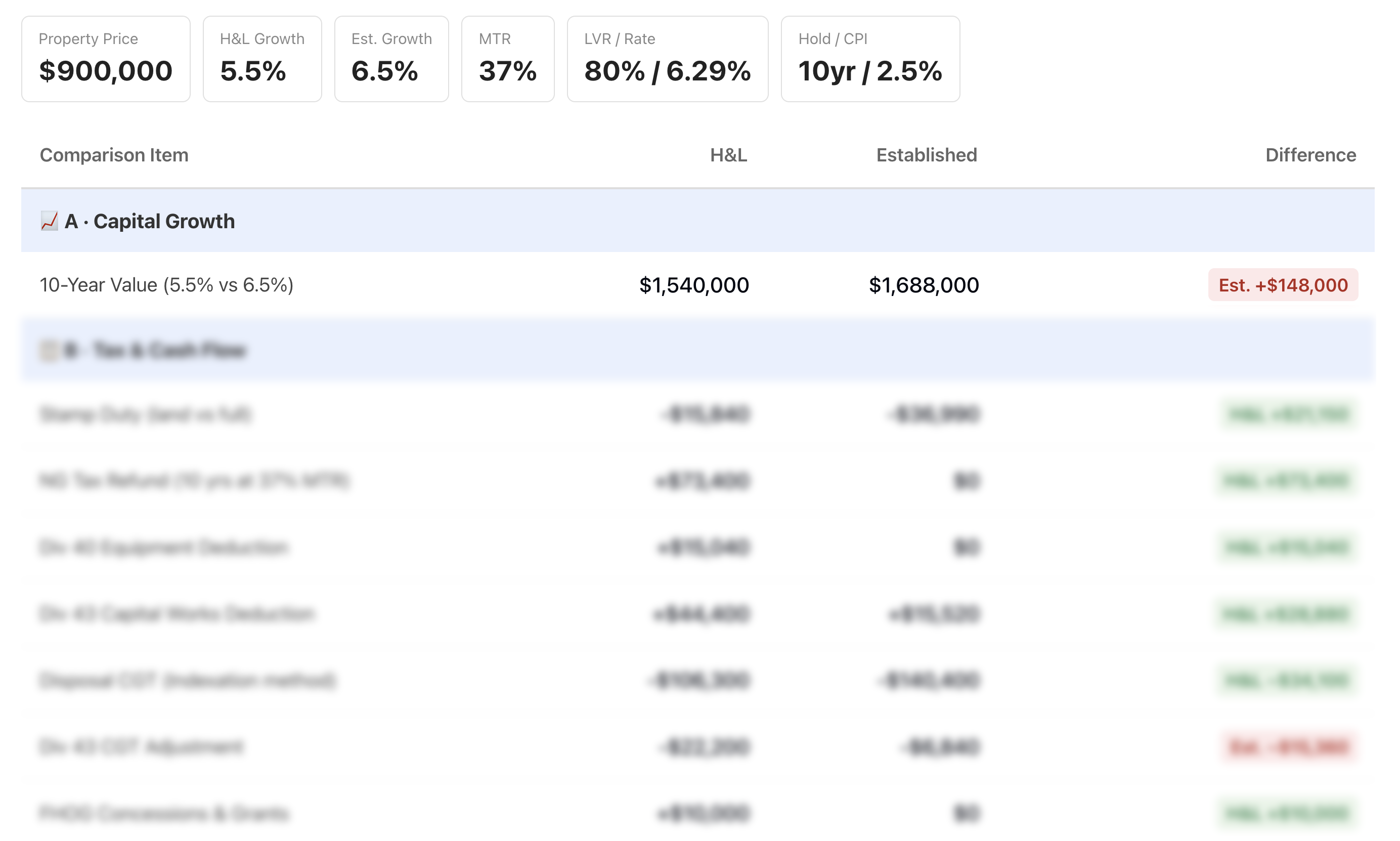

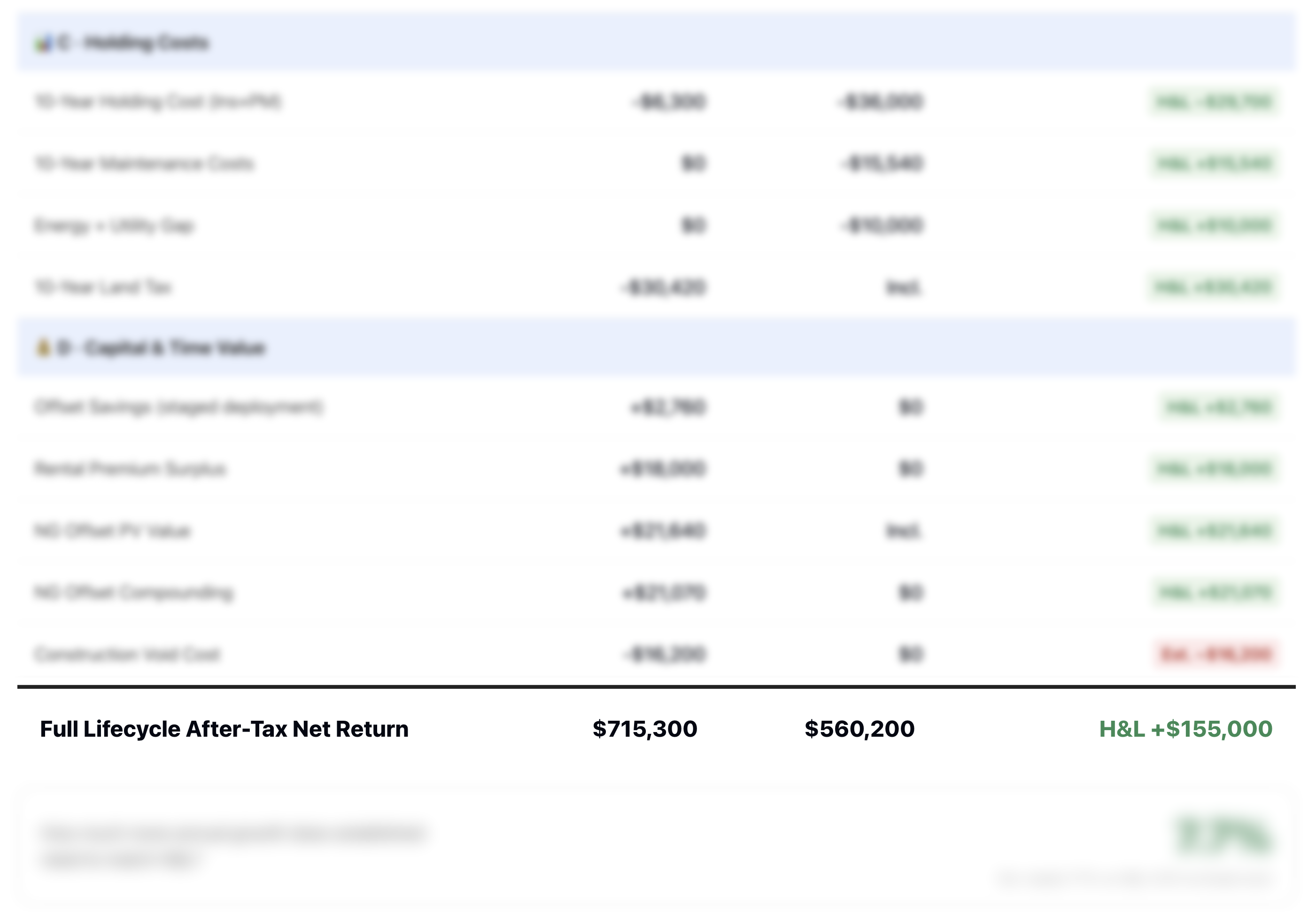

I modelled a 10-year lifecycle for a $900,000 property, and I gave an established house an advantage, 6.5% annual growth versus 5.5% for house and land. Established came out $148,000 ahead on raw growth. Sounds like established won, right? But once you factor in tax refunds, depreciation, stamp duty savings, CGT method choice, maintenance, energy efficiency, and the rental premium, house and land came out $155,000 ahead on after-tax net return.

And here’s what most people miss. All existing growth data was generated under the old tax system. After July 2027, both CBA and Westpac predict capital will rotate from established toward new builds. The old growth patterns may not hold up.

So on growth, established houses may have an edge. But once you work out the net after-tax return, house and land in the $800,000 to $1,200,000 range still comes out ahead by over $100,000.

Now I want to be clear about something. I’m not saying established houses are a bad investment across the board. There are scenarios where they win, and I’ll show you exactly where those are in the price tier analysis coming up. But the claim that “established is always better”? The numbers don’t back it up. Not anymore.

I know some people will push back and say house and land packages carry a premium over established houses, so why haven't I factored that in? First, take a similar location, a similar land size, and a similar floor area. Between a house and land package where construction hasn't started and a near-new home completed within the last five years, a price gap does exist in some locations, with some builders, in some price brackets, and in some states and territories. Compared to a 30-year-old established house and there may be a gap as well. That part is true. But most of the time, what we do for our members is find house and land packages with no premium, or only a small one, and in practice they can be found. The people pushing back simply don't know how to find them, or they've got a conflict of interest.

Second, I'm planning a video that runs a full life-cycle analysis across 5, 10, and 20 years, comparing house and land packages and established houses under similar conditions, to work out how much more you could pay for a house and land package and still walk away with the same after-tax return at sale. I'm running that analysis right now, and the early results point the same way: the premium can be very large and the house and land package still comes out level with the established house. I'll decide later whether that video goes out, but most likely it'll only be shared with our VISION Gold Members and Masterclass students.

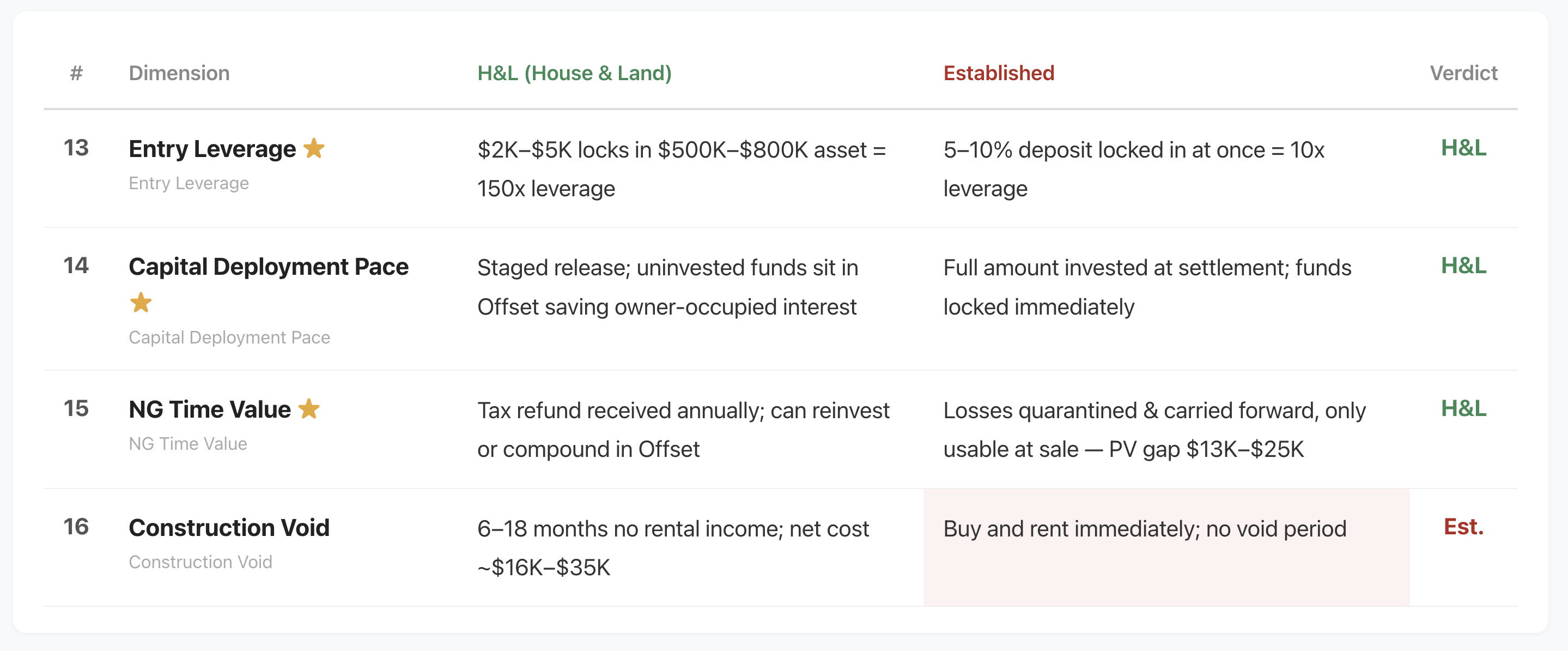

C. Capital and Time Efficiency Dimensions

Four dimensions here. House and land wins three, established wins one.

Established wins on the construction vacancy period. House and land takes 12 to 18 months from contract to tenant, and that’s real money. But buyer’s agents stop right there. What they don’t bring up is that to earn rental income during that period, established house buyers need to service their full mortgage and cover holding costs from day one. House and land buyers pay far less during construction. The tax refund difference over two years can make up for the lost rent, and the stamp duty savings close the gap further. In practice, house and land more often ends up with a net surplus.

Now the three where house and land wins. Entry leverage: $5,000 locks in a $900,000 asset, that’s 180 times leverage. Established needs $90,000, which is 10 times, dropping to 5 times once you settle. Same starting capital, house and land lets you lock in multiple properties. Capital deployment: staged payments mean unused cash can sit in your offset account saving interest. And the time value of tax refunds: house and land refunds land in your pocket every year and keep compounding. Established losses are quarantined until you sell. A dollar today is worth more than a dollar in 10 years.

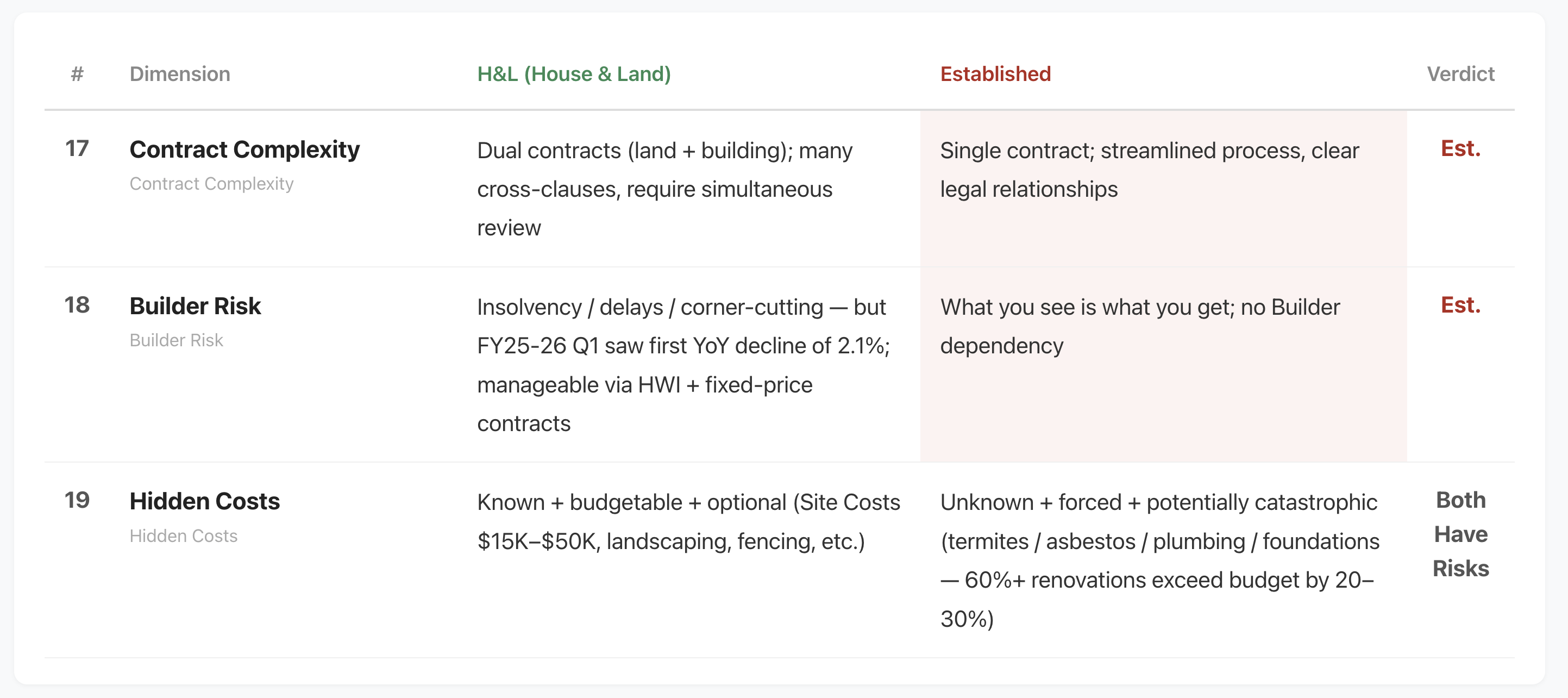

D. Purchase Process and Risk Dimensions

Three dimensions. Established wins two, the third is a draw.

Contract complexity: house and land has two contracts, land and construction. Sunset clauses, extension clauses, and site costs all need cross-checking. Established has one contract. But the dual-contract structure is exactly what saves you stamp duty. Complex isn’t bad. That’s what lawyers are for, and it’s one reason to join as a VISION Gold Member. We look after that for you.

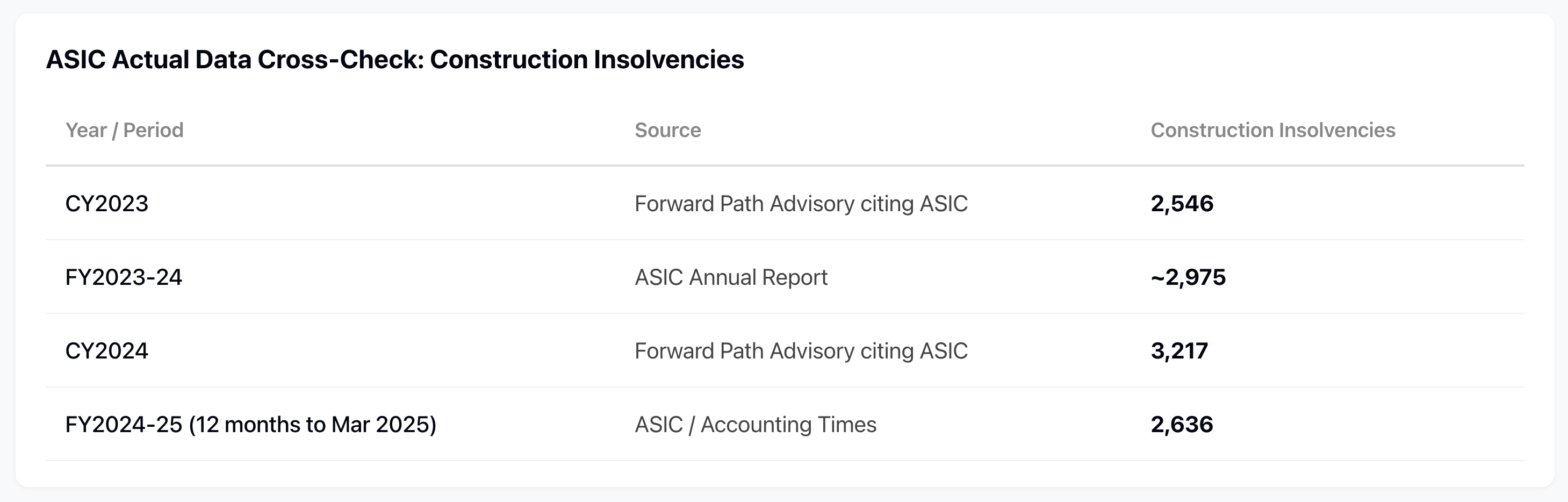

Builder risk: insolvencies run into the thousands every year, and the industry has low barriers to entry. But 2025 numbers are already coming down year on year, which tells you the industry is stabilising. The root cause was that fixed-price contracts signed during the pandemic ran into cost blowouts of 30% to 50%. Those toxic contracts have largely been flushed out of the system. Pick the right builder, sign a fixed-price contract, do your background checks, and the risk is manageable. In over five years of running VISION Gold Membership, not a single builder we’ve worked with has had an issue.

Hidden costs: a draw, but the nature is completely different. House and land extras are known and budgetable, things like site costs, landscaping, and fencing. You know what you’re up for before you sign. Established? Asbestos, termites, foundation issues, and rewiring. No matter how carefully you inspect, things slip through. Known risks aren’t really risks. The unknown ones are.

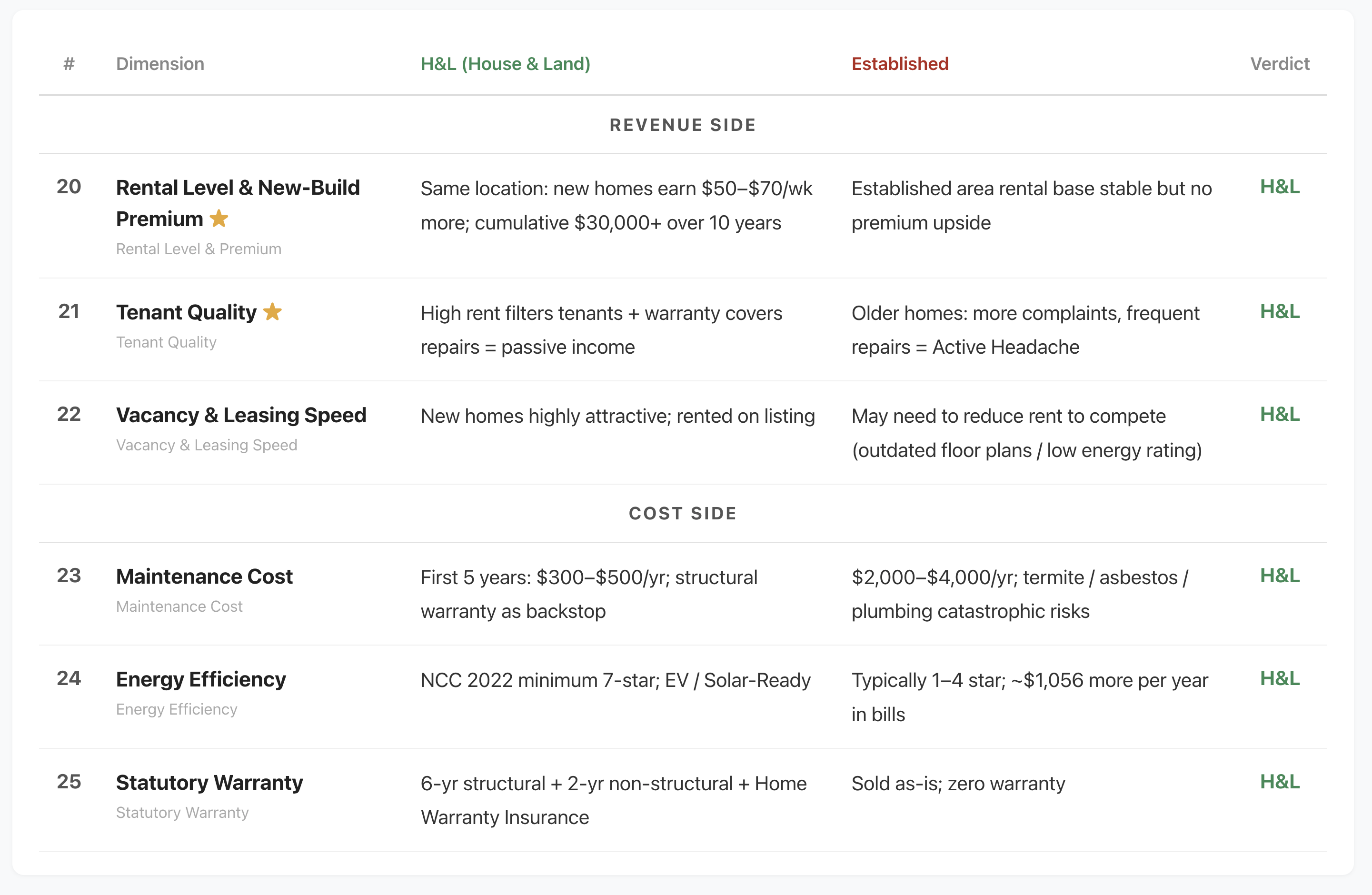

E. Holding and Operations Dimensions

This is where the gap is the biggest. Six dimensions, house and land wins all six.

Income side.

Rental premium: within the same economic corridor, a new house pulls in around $50 more per week than a 10-year-old house. A 7-star energy rating, modern layouts, new appliances, no asbestos or lead paint concerns. Tenants are willing to pay more for that.

Tenant quality: higher rent is a filter in itself. New houses get about one-third the maintenance requests of older ones in the first five years.

Vacancy: new houses get leased within a week or two, established typically takes a bit longer.

Here’s something property managers keep telling me: “Managing a new house is like being on autopilot. Collect the rent, pay the bills, send the year-end report, make two phone calls. Managing an old house is like firefighting. Hot water breaks, toilet leaks, tenant calls about wall cracks. Same management fee, five times the work.” You’re buying an investment property for passive income, not a second job.

Expense side.

Maintenance: new houses cost almost nothing for 10 years. Established? Ageing pipes, overloaded wiring, failed waterproofing, any one of these runs into thousands.

Energy efficiency: houses built after 2024 must meet NCC 7-star (note that Tasmania and the Northern Territory haven’t adopted this yet). Older houses sit at one to four stars, and that power bill gap shows up every single year.

Statutory warranties: new houses generally get six years structural and two years non-structural cover. Established houses are almost always sold “as is.”

F. Exit and Market Structure Dimensions

Three dimensions. House and land wins one, established wins one, and the third depends on circumstances.

So where does most of the negative noise about house and land come from? I’d bet 9 out of 10 times, it’s buyer’s agents. Their income comes from helping you buy established. If you buy house and land from the developer directly, they earn zero commission. Are they going to recommend a product that makes them no money? The government’s tax reform clearly favours new builds, and that’s pushing the buyer’s agent business model to the margins.

But house and land has one structural weakness: the exit. Before completion, many developers restrict resales, so you can’t get out. After completion, your house and land becomes “established.” The next buyer loses the new-build tax advantages, which narrows the buyer pool. Established houses can list on the open market any time. So under the new tax law, house and land suits buy-and-hold investors, not short-term traders.

Bank valuations are the third dimension. In a rising market, post-completion valuations often come in above the contract price, which means easier lending. In a falling market, you may need to cover a cash shortfall, but there are ways around it, multiple lender valuations, bridging finance, and so on. After July 2027 though, there’s a new factor: the negative gearing quarantine on established properties will affect how banks assess your borrowing capacity. The market hasn’t fully priced this in yet.

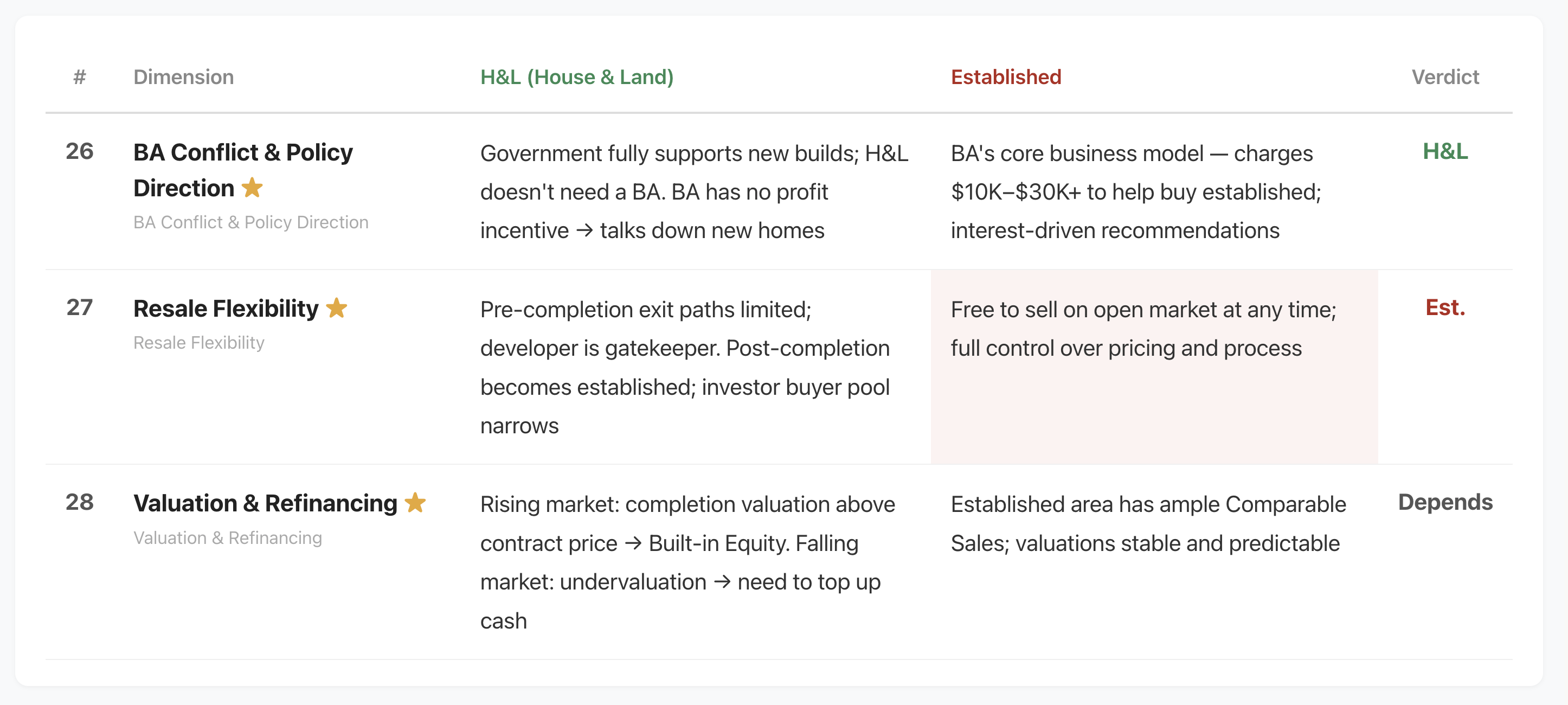

G. Forward-Looking Dimensions

Four dimensions. House and land wins all four.

External factors. Interest rates: during construction, the full loan hasn’t been drawn down, so the higher rates are, the more you save. ESG compliance: new houses come standard with NCC 7-star, EV-ready, and solar-ready features. If established houses are eventually required to meet minimum energy standards before they can be rented out, forced upgrades could cost tens of thousands. Victoria is already heading in that direction.

Personal factors. Portfolio expansion: house and land’s low deposits plus annual tax refunds help you build up the next deposit faster. Each established purchase locks up over $100,000 with no tax refund flowing back. And the most important one for migrants, residency status:

If one day you move overseas for the long term and become a non-resident, the first thing to remember is the "one-day rule". It doesn't matter whether you bought a house and land package or an established house. If you're a non-resident for tax purposes for even a single day during the ownership period, you lose indexation permanently. The rule treats both property types exactly the same, and moving back to Australia later won't bring it back.

The real difference is in the 50% discount. With a house and land package, the discount doesn't drop to zero. It gets apportioned by days instead. The formula is your resident days divided by twice the total days. Spend six years as a resident out of ten, and your discount is 30%, applied to the entire gain. There are two things to note here. First, this is a forced outcome, not something you choose. Picking between the 50% discount and indexation is a privilege reserved for people who stay residents the whole way through. Second, the formula only counts days. It doesn't look at when the growth happened. Even if the entire price rise came during the years you were a resident, the formula still only recognises the days.

So what happens with established houses? They get no 50% discount at any point. For an established house bought after July 2027, even someone who stays a resident the whole time gets no discount. That has nothing to do with your residency status. Its only relief is indexation, and indexation sits under the one-day rule. So if you've ever been a non-resident, selling an established house means paying tax on the full nominal gain.

So for anyone who might become a non-resident in the future, a house and land package can save you a significant amount of CGT. Take the same property bought at $1 million and sold at $1.6 million, held for six years as a resident and four as a non-resident, then sold as a non-resident. The house and land package gets the 30% discount and pays $164,000 in tax. The established house gets zero relief and pays $245,000. That one factor alone opens up a gap of $81,000.

But the most brutal scenario is this one. You did everything by the book and stayed a resident for nine and a half years, and the only break was a six-month posting overseas that broke your tax residency. The legal threshold is actually just one day. Then you came back to Australia and sold as a resident. With the established house, indexation is still permanently gone, you pay tax on the full gain, and you hand over about $132,000 more than if you'd never left. With the house and land package, the discount only slips from 50% to 47.5%, and you pay about $7,000 more. The same six-month break in residency status costs $132,000 on one property and $7,000 on the other. That's a difference of nearly 19 times. So the answer to this question is clear. If you're ever going to leave Australia, buy a house and land package.

The resident versus non-resident question is very complex, because it depends on whether you're a resident when you buy, while you hold, and when you sell. Then you stack new builds versus established houses on top, and owner-occupied homes versus investment properties on top of that. I'll make a dedicated video on this later on and share it with our VISION Gold Members and Masterclass students.

32-Dimension Summary

So across 7 categories and 32 dimensions, house and land won 20, established won 8, and 4 depend on circumstances. House and land dominates on tax, holding, and forward-looking categories. But one critical assumption I have to spell out: all of this is built on similar locations and equivalent prices. For the same $900,000, house and land might be in Perth or Brisbane, while established might be in Sydney’s south-west or Melbourne’s south-east. Different markets, different cities. You need to look at each one on its own merits.

Without breaking it down by price, these conclusions only give you direction. So now I’m going to do something nobody else in the market has done. House and land versus established, across Australia, by four price tiers.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

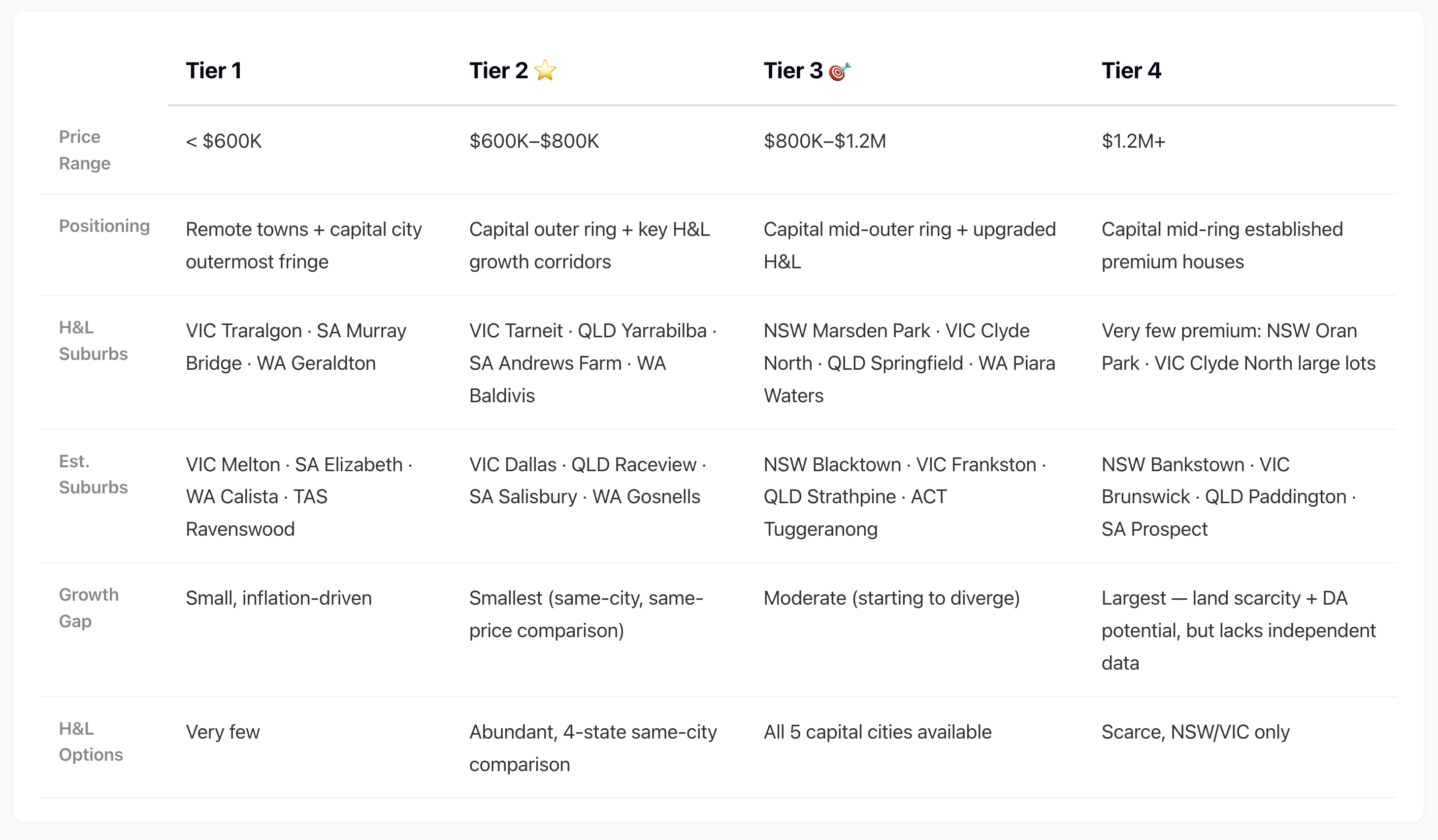

Four Price Tiers

Your budget determines which playing field you’re on, and each field has completely different rules.

Tier 1, under $600,000. Concentrated in remote towns and the outermost fringes of capital cities. More likely 20 to 30-year-old houses on larger blocks. Yields can hit 5%. Sounds good on the surface, but Treasury’s Budget Paper says that for regional houses held five years, 53% of capital growth is just inflation. If the price went up $100,000, over $50,000 of that is just the cost of everything else going up too. Tier 1 logic is cash flow, not wealth building. And if the property is already positively geared, the negative gearing quarantine barely touches it.

Tier 2, $600,000 to $800,000. This is where house and land’s tax advantage is at its largest. At this price, you can find both options in the outer suburbs of capital cities. A new house and land in Tarneit versus established in neighbouring Werribee at a similar price. House and land keeps full negative gearing plus CGT method choice. Established loses both. Even if established grows 1% more per year, the 10-year tax gap sits at around $100,000. That growth edge doesn’t necessarily close the gap.

Tier 3, $800,000 to $1,200,000. The entry price for far outer Sydney, and another tier where house and land has a strong advantage. Investors here typically earn $120,000 to $200,000, putting them in the 37% tax bracket. Loan sizes are large, interest is high, and these properties are almost certainly negatively geared. CBA estimates the quarantine is equivalent to adding 0.9% to 1.55% to the interest rate. But established has a real advantage too: land scarcity in mature suburbs is a fact. So Tier 3 comes down to one number: how much more does established need to grow each year to close the tax gap?

Tier 4, over $1,200,000. Here the logic flips. You can find house and land at this price in Sydney and Brisbane, but nationally the supply is thin. This is established property's home ground. Mid-ring houses have strong growth potential, but at a 45% marginal rate, the annual tax refund gap is over $10,000. So the question is whether that growth can outrun the extra tax cost. And then there's the cash flow pressure of holding without negative gearing, which is a real issue at this price point.

Four tiers, four different investment logics. Making a blanket call that 'house and land is better' or 'established is better' without specifying the tier is just irresponsible.

Full Lifecycle Modelling

We picked matched pairs in each tier and modelled them across 5, 10, and 20-year holding periods, calculating every number through to the year of sale. From methodology to data collection to getting the calculator working, our team put in four full days, with heavy AI assistance.

We accounted for state-specific tax rules, growth rates, insurance, maintenance, and labour costs. We built in the present value of negative gearing, the add-back when you sell, land tax, marginal tax rates by tier, and buyer’s agent fees for established properties.

We deliberately gave established houses a growth rate premium. Without it, established loses in almost every tier.

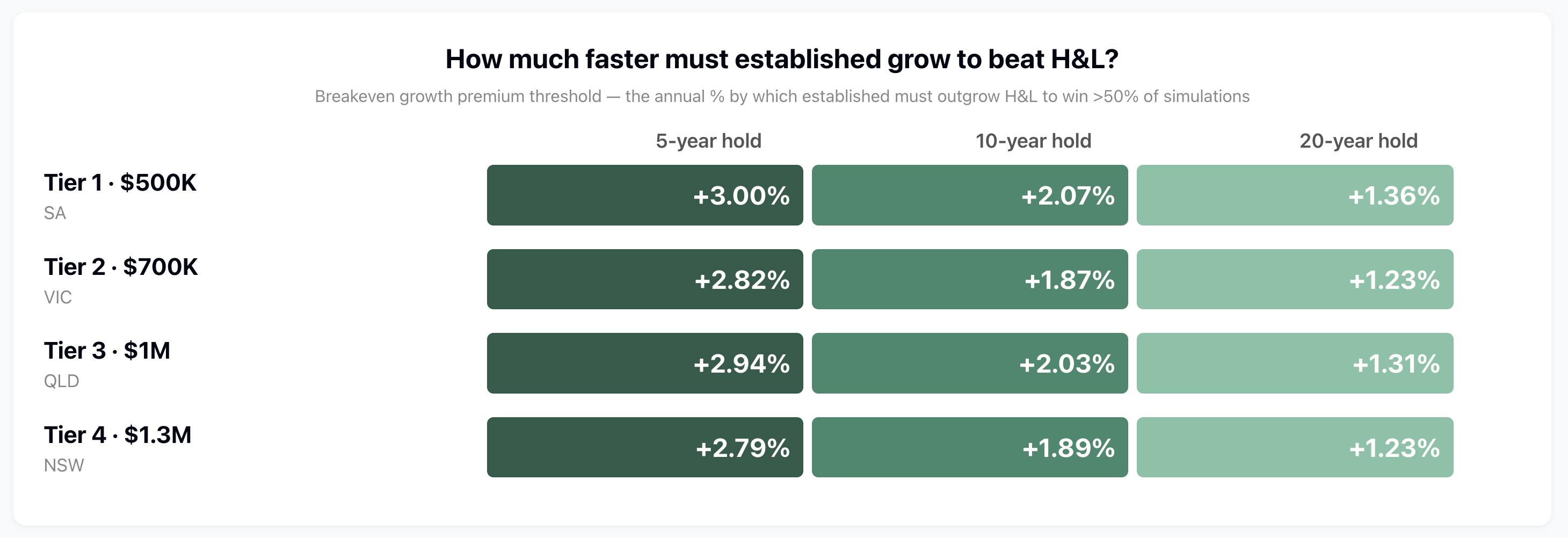

Here’s one set of examples with a 10-year holding period. South Australia at $500,000, assuming established grows 0.5% more per year, house and land still comes out nearly $100,000 ahead. The breakeven threshold? Established would need to grow 1.86% more, every year, for 10 straight years. Victoria at $700,000, house and land is $74,000 ahead, threshold 1.69%. Queensland at $1,000,000, assuming established grows 1.5% more, house and land is still $53,000 ahead, threshold 1.94%. So your reason for buying established in Queensland at that price is basically a bet that it’ll outgrow house and land by 2% every single year for a decade. New South Wales at $1,300,000, assuming established grows 2% more, house and land returns are $25,000 lower, threshold 1.84%. But honestly, I don’t believe the real-world gap would exceed 1% a year.

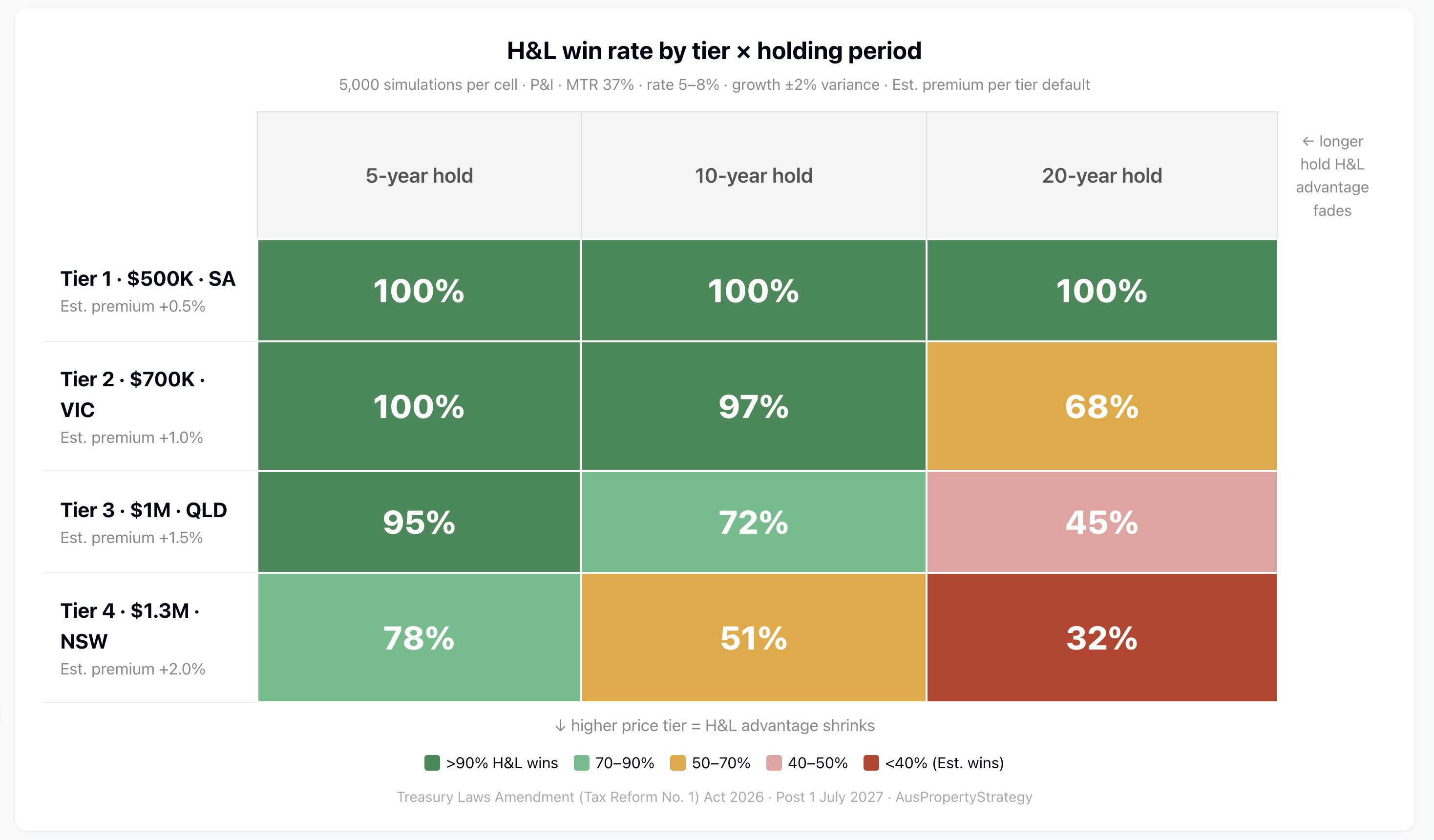

To get the big picture, I ran Monte Carlo simulations, three rounds, 16,000 tests total. Our methodology and parameters were verified by industry leaders, including several Australian PhDs in statistics.

The results. Tier 1: house and land wins 100% of the time. As you move up the tiers, house and land’s win rate drops, and longer holding periods bring it down further. At Tier 3 with 20 years and Tier 4 with 10 years, the win rate falls to about 50%. At Tier 4 with 20 years, established wins outright.

The lower the price and the shorter the hold, the worse established performs. This directly challenges buyer’s agents who push low-priced established houses with a 3 to 5-year flip strategy. The costs are too high. What they want is for you to buy and sell every few years so they collect fees each time. You’d actually end up with more by holding for 20 years.

Action Recommendations

So here’s where we’re at. Your budget and holding period determine the answer. Tier 1 and Tier 2, any holding period, house and land comes out ahead. Tier 3, house and land has the edge for 5 to 10 years, and roughly ties with established around 20 years. Tier 4, beyond 10 years you need to work out whether growth can outrun the tax cost. Ask yourself: which tier is my budget in? How long can I hold? And can I actually hold on that long without the cash flow support of negative gearing?

Now, a note on buyer’s agents. Not directed at any individual. This is about a structural problem with a business model.

Tactic one, geographic shift. They start in one city, trash every other state, and funnel all their clients into the one market where they earn commissions. When that market dries up and the deals stop flowing, suddenly they go national. And just like that, their videos stop trashing those other states. Because now they need those commissions too.

Tactic two, only recommending established. If you buy house and land, you go direct to the developer. The buyer's agent gets nothing. So of course they have to argue that established is better. You've heard the lines. "Higher land-to-value ratio means better growth." "Growth corridors are a trap for beginners." "New build quality is terrible." Every one of those claims has a grain of truth wrapped in a lot of exaggeration, and every one of them happens to steer you toward the product that pays their commission.

Tactic three, dodging the numbers. They never do a full lifecycle quantitative analysis. Why not? Because the numbers would blow their argument apart. Instead they talk about feel. "It's a good suburb." "Strong school zone." "Land is scarce." All true, but none of it answers the questions that actually matter. How much tax did you save? What's the negative gearing gap worth over 10 years? How much more depreciation does a new build give you? What's the CGT method choice worth in actual dollars? They wouldn't dare sit down and work it out with you.

AusPropertyStrategy’s model is completely different. We cover every state, every property type, and every price point in Australia. Accounting, lending, legal, wealth planning, cross-border tax planning, all under one roof. Once you’re a member, I’ll recommend whatever’s best for you. I don’t have to talk up any particular state, push any particular property type, or defend any price range. I just look at the facts and find the best property for my members.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs