How Foreign-Born Buyers Are Quietly Outplaying Local Investors | APS153

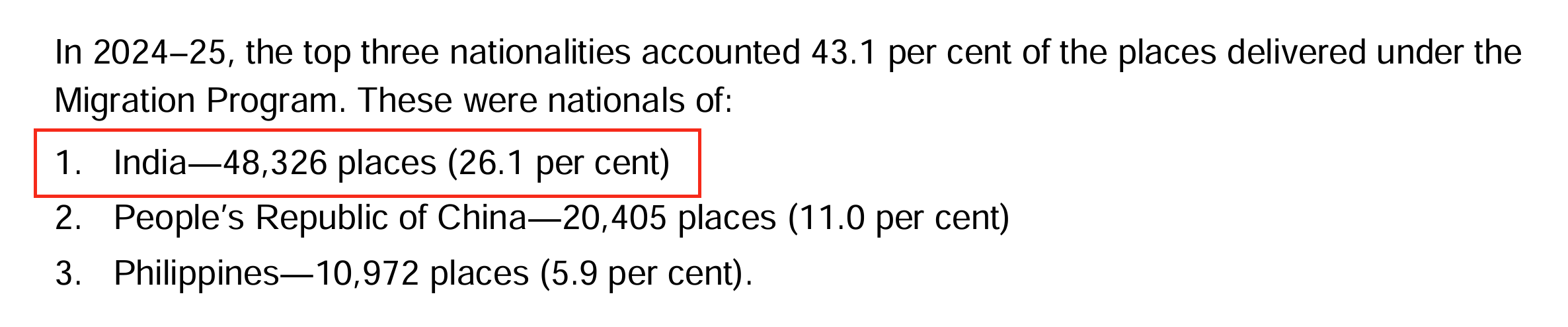

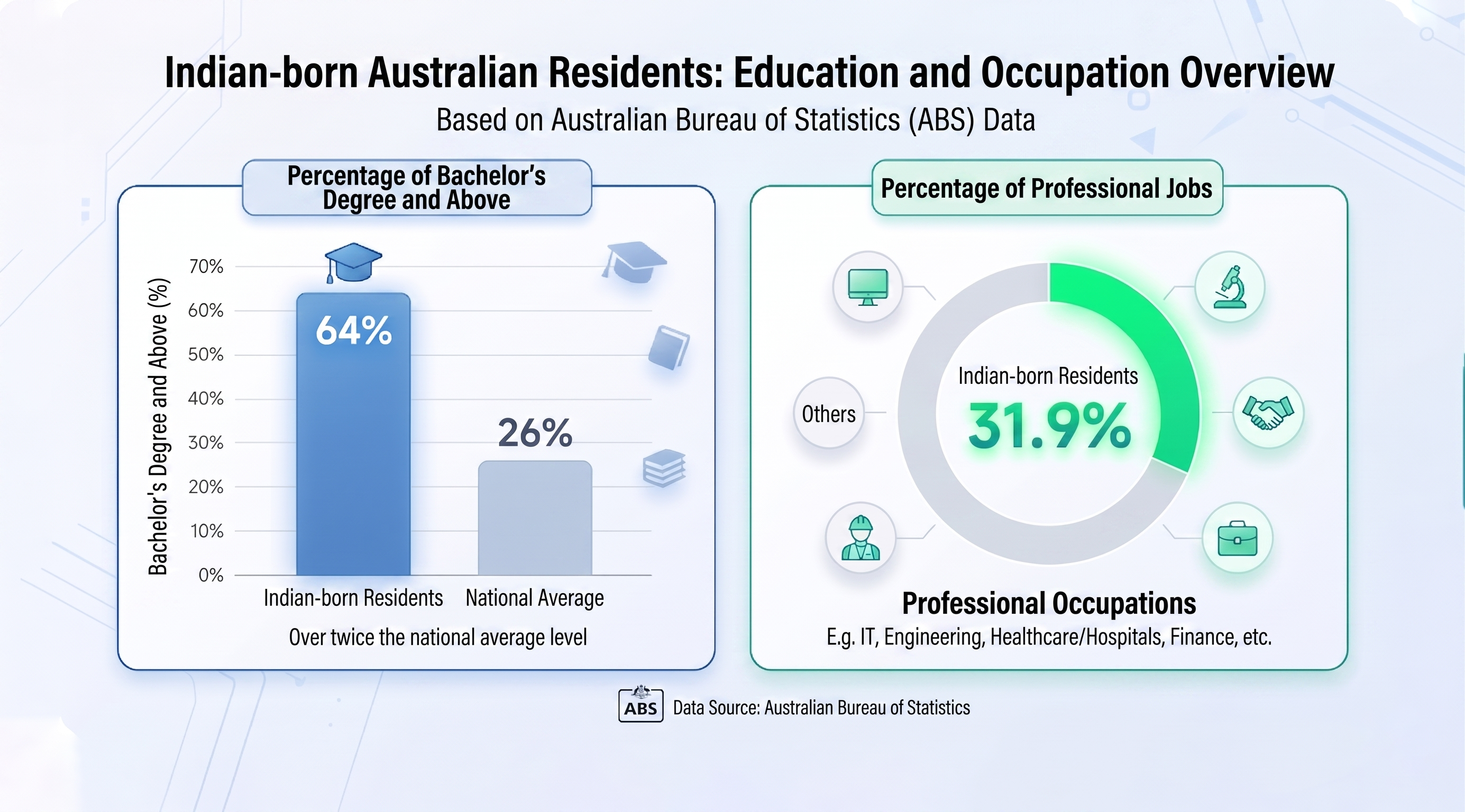

48,000. That’s how many Indian-born migrants picked up Australian permanent residency in the last financial year, topping every other country in the world. These aren’t people coming here to fill entry-level jobs. 64% hold a bachelor’s degree or higher, and their household incomes come in 41% above the national average. They walk into a bank and get approved for bigger loans than most of us. They spot a property and move on it faster. Quietly, one house at a time, they’ve been snapping up properties across the country, piling pressure onto a market that’s already stretched thin. But here’s what most property buyers have never heard of: Indian investors have figured out a combination of tax savings, low deposits, and annual ATO refunds that gives them a serious edge. And just 2 weeks ago, the federal Budget made a change that turned this combination from a smart strategy into pretty much the only strategy left standing.

The Indian Migration Wave

In the 2024–25 financial year, Indian-born migrants landed 48,000 permanent residency places, making up 36.6% of Australia’s skilled migration intake. But the numbers alone don’t tell the full story. The quality of this wave is what stands out. ABS data shows 64% of Indian-born Australian residents hold a bachelor’s degree or above, while the national average is just 26%. Nearly 32% work in professional roles, and in IT, India is the single biggest source country for software development positions.

This trend shows up globally, too. Microsoft CEO, Google CEO, IBM CEO, plus more than a dozen Fortune 500 chief executives are of Indian heritage. In Australia, the 2025 AFR Rich List put Motherson Group’s CEO at number 19 with $8.05 billion, and Australia’s largest gold miner, Newcrest Mining CEO, on the list too.

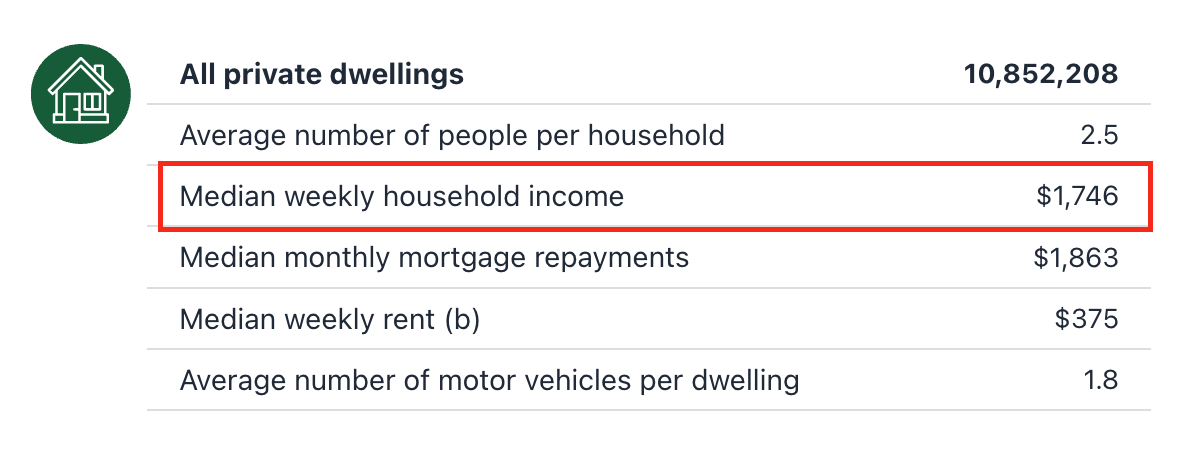

So what does this mean on the ground? The median weekly household income for Indian-born residents is $2,461, compared to $1,746 nationally. That’s 41% higher. While most buyers are still trying to scrape together a deposit, these buyers are already walking into the bank with a strong payslip. But here’s the thing. Their real advantage isn’t how much they pull in. It’s that they think about spending money in a completely different way, and the story I’m about to tell you might make you rethink your own approach.

If You Wait Until You’re Ready, You’re Already Late

There was a media report about an Indian migrant who showed up in Melbourne nine years ago with his wife and child, no job, and debts back in India. He squeezed every expense down to the bare minimum and put away 60% to 70% of his pay.

In 2018 he landed a job at Commonwealth Bank, and his first move wasn’t to upgrade his lifestyle. He cleared his debts in India. Then he had one goal: get into the property market as fast as possible. He didn’t wait for prices to drop and he didn’t wait for rates to come down. In early 2019 he pulled money from his Indian provident fund, put together a deposit, and bought in Werribee, in Melbourne’s west. It wasn’t a glamorous suburb, it wasn’t a top school zone, and it wasn’t the kind of address you’d show off to anyone. He wasn’t thinking about the image today. He was thinking about the value tomorrow.

Over the following years, that suburb’s prices nearly doubled, with most of the growth in the earlier years. What came next was textbook. He refinanced, pulled out the equity, and used it as the deposit for the next one. From Sydney to Brisbane to Perth, he kept going, and he ended up with 12 properties worth $13 million in total.

Now here's the thing. Most property buyers in this country get caught up in perfectionism. We want something close to the city, in a well-known school catchment, somewhere familiar. The median price for a detached house in Sydney sits at around $1.6 million right now, and in a decent suburb, you're looking at $3 million to get started. Deposit and stamp duty alone will set you back about $600,000. So most people keep waiting, and three to five years go by while they're still sitting on the sidelines.

Indian buyers turn that on its head. If they can't afford the inner suburbs, they go further out. They don't hold out for the perfect deal, they get into the market and adjust from there. They understand one of the most basic truths about Australian property: land goes up in value and buildings go down. You pick a block in the right spot, and time does the heavy lifting. In our 5-4-1 framework, 50% of the weighting goes to location, and that's exactly why.

So that covers the mindset. Now let's get into the mechanics, because what they're buying and how they're getting in with the least cash is where this gets interesting.

The Secret Behind Buying Land

They’re buying House and Land packages. The core structure is two separate contracts: one for the land, one for the build, and stamp duty only gets calculated on the land part. Say you’re looking at an $800,000 H&L where the land is $350,000 and the build is $450,000. Stamp duty is worked out on $350,000, roughly $18,000. If you went and bought an $800,000 established house instead, stamp duty hits the full price, around $44,000. In one transaction, you save over $20,000.

I do need to flag something, though. This only works with genuinely separate contracts. Some developers put together a single-contract package, and when they do, the revenue office will hit you with stamp duty on the full price. Before you sign, make sure your conveyancer goes through the contract structure carefully.

On the deposit side, land typically needs just 5% to 10%, and the build cost gets paid in stages over 12 months. For buyers tight on cash, that construction period becomes your buffer to keep saving and sort out your finances.

But the most powerful part of this strategy is the snowball effect. You lock in land at today’s price, and a year or two later, when the house is done, land values in the area have usually moved up. You refinance, pull out the equity, and that becomes the deposit for the next property. One rolls into the next.

So the product makes sense, and you know how to get in. But there's one thing that trips most people up. A lot of buyers hear “negative cash flow” and immediately back away, because paying when holding a property sounds like a losing game. Indian investors don’t see it that way, because they’ve run a calculation most people have probably never even looked at.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

Your Tax Refund Is Your Second Income

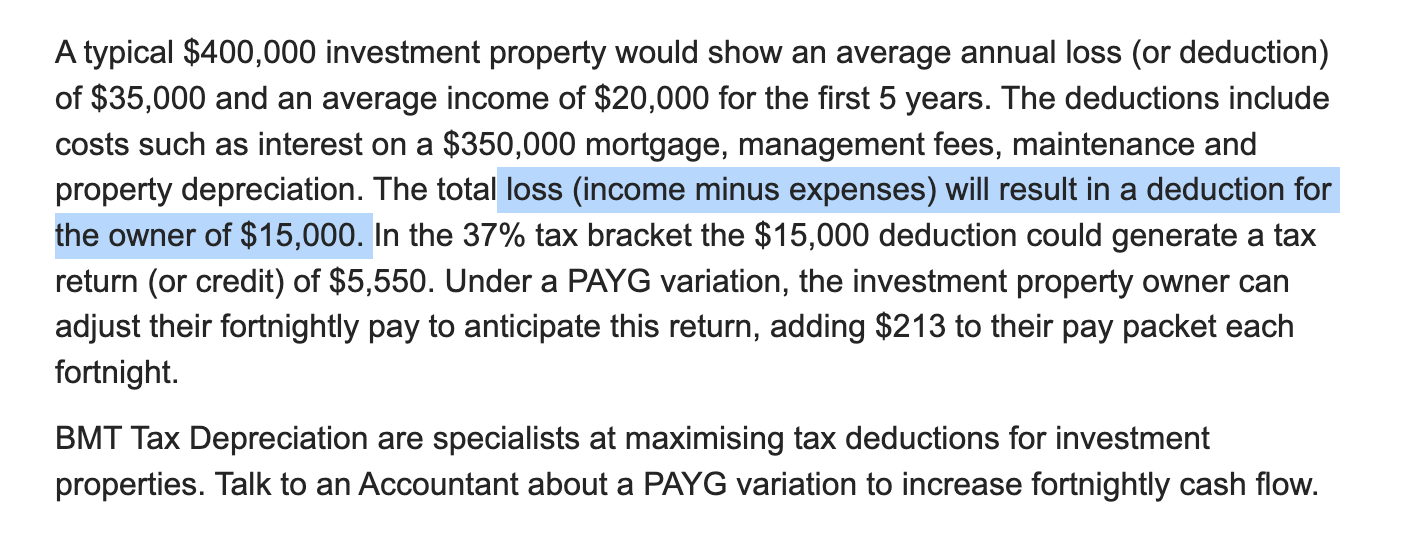

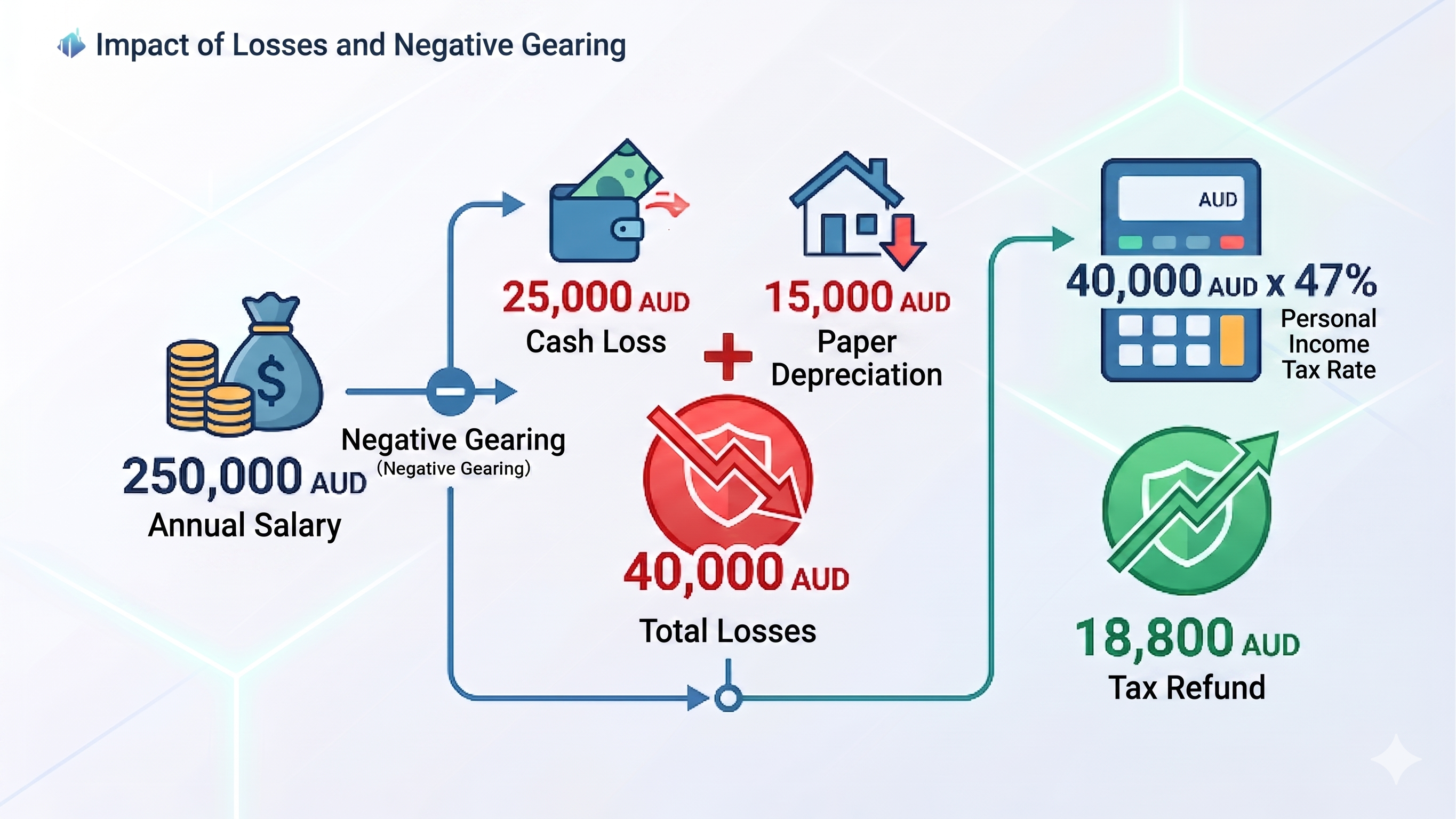

Let's say you're an IT manager earning $250,000 a year. You buy a brand-new $1 million House and Land in Brisbane, with an 80% loan at 6.8%. Rental yield comes in at around 3.8%, so that's about $38,000 a year, roughly $730 a week. On the expense side, annual interest comes to about $54,000, plus around $9,000 for council rates, insurance, land tax, water, and property management. Total expenses come to about $63,000, leaving a cash gap of $25,000 a year. That's money you'd normally have to find out of your own pocket. Most people look at that and walk away, because who wants to lose $25,000 a year?

But this is where it gets interesting. In year one of a brand-new House and Land, you can claim around $15,000 in depreciation through Division 43 for the building structure and Division 40 for fixtures and fittings. \ And here's the key part: this is a pure paper deduction. You don't spend a dollar of cash to get it.

Now, after the 2017 tax changes, individual investors who buy established properties can't claim existing Division 40 depreciation anymore. Only brand-new properties qualify for both types. That matters.

So let's work through the tax return. You've got a $25,000 cash loss plus $15,000 in paper depreciation, giving you a total deductible loss of $40,000. Through negative gearing, that gets taken off your $250,000 salary before the ATO works out your tax. At the top marginal rate of 47%, that saves you $18,800, money that would have gone to the ATO but now stays in your pocket. Your out-of-pocket cost drops to just $6,200 a year, about $120 a week. Think about that. For $120 a week, you're holding onto a million-dollar brand-new house where the land keeps going up, and the building is helping you claim tax back. Now, this assumes you're holding the property in your own name without other income, and if you hold through a trust or company, the maths works differently. But the core logic is simple: use the lowest holding cost, combined with the longest time horizon, to capture long-term capital growth. The higher your marginal tax rate, the harder this works in your favour.

Now, I'll be straight with you. I'm not saying the tax benefit is free money forever. Some depreciation does get added back when you sell, and you need to work that out properly when you factor in the time value of money. I'll do a full technical breakdown in a future episode. But here's what it boils down to. A dollar in your hand today is worth more than a dollar later, and that cash flow benefit helps you hold on longer and capture more growth. You don't even have to sell, because you can refinance and pull out equity to fund the next purchase. Without negative gearing, smoothing out your cash flow, the cost of holding goes up dramatically, and you might have to sell before you want to. Anyone who says "depreciation gets clawed back, so just buy established" is missing the bigger picture.

Right, the numbers are clear. But there's one more thing you need to know, because 2 weeks ago, the government made a decision that turned "buying new" into the best choice by almost every measure.

The Government Is Pushing You Toward New Builds

The May 2026 Budget included two proposals. From 1 July 2027, negative gearing on established residential property will be abolished for new purchases. Any rental losses on established investment properties can only be offset against other property income, with the rest carried forward. But new builds are completely untouched. Negative gearing stays. The 50% CGT discount stays. Depreciation stays. Everything carries on as before. Established properties will use the index and a 30% minimum tax to calculate CGT, making them unattractive for tax purposes.

I'm not saying established property will crash. I'm saying the risk profile has shifted. Think about what we've just gone through. Indian investors have been buying brand-new House and Land packages, using new-build depreciation and negative gearing from the start. This strategy was on the right track from day one, because Australia is so short on housing that the government was never going to go after new construction, and this Budget has stamped it with an official seal.

From July 2027, new builds will be the only residential investment in the country that can access negative gearing, the CGT discount, and full depreciation all at once. The approach Indian investors took five years ago has become the only direction the government is encouraging. The legislation is still going through Parliament, and the details could shift, but the direction is locked in, and support for new housing isn't going anywhere.

So the strategy stacks up, the numbers work, and the policy backs it. But before you get carried away, there are things I need to lay out.

You Need Vision, But You Also Need to Accept Risk

Not every city's House and Land market is worth buying into right now. Australia's property market is going through a serious split between cities. Perth and Brisbane are still the two I'm most confident about, with strong population inflows and tight supply. Sydney and Melbourne have drifted lower recently, but we could see a turning point in the second half of this year. If you're looking at H&L in either of those cities, you need to be precise about which area you pick, because buying randomly won't cut it.

Now, there are five risks you need to know about. The first is builder risk. If your builder goes under, you're looking at an unfinished house and extra costs. You won't figure out a builder's financial health from their ads, and we've got our own criteria for screening them. In five years of running AusPropertyStrategy's VISION Gold Membership, not a single builder we've picked has gone bust. The second is interest rate risk. Investment home loan rates are already pushing close to 7%, and if they climb higher your holding costs go up, although the tax advantages on new builds do help cushion that. The third is vacancy risk. When lots of new stock lands on the rental market at once, vacancies can spike in the short term, but strong population growth cancels that out, which is why picking the right area matters. The fourth is taking on too much debt. By the time you're rolling into your third or fourth property, the bank might say no, and if rates go up or rents come down, high leverage turns into high risk very fast. And the fifth is joint ownership risk. Buying property with someone who isn't your spouse comes with complicated legal relationships, and if a dispute kicks off, sorting it out gets expensive.

This is exactly why I keep coming back to the all-weather investment approach. You don't stick to one city or one product type, you spread across Australia, across property types, and across market cycles, so your portfolio can ride out whatever comes. We cover both new and established properties, so we recommend whatever works best for our members.

What Indian investors have shown us comes down to one simple principle: get on the train first and adjust as you go. Buy land. Act before the perfect moment arrives. They picked the right product, used the right tools, and moved in the right direction, and the Federal Budget has confirmed it. Don't let perfectionism become your excuse for standing still. The opportunities have always been there. You don't need more money or better spreadsheets. You need the willingness to see the potential, the courage to take the step, and the commitment to follow through.

New Builds vs Established: Setting the Record Straight

After my last few videos went up, I saw a lot of comments pushing back on new builds, and I want to talk about the main arguments.

This one goes: "When you buy new and sell later, it becomes a second-hand property, so you'll never get a good price for it. New builds always carry a premium over established homes, so you pay more going in and get less coming out. You get cut on both sides."

Let me go through this point by point.

First, why would you buy a new build that carries a big premium over comparable established homes in the same area? You look for one where the premium is small or where there's no premium at all, and those properties are out there if you know where to look. I find them for our members all the time.

Second, think about what happens once the Budget changes kick in. Any established property bought before the cut-off keeps its negative gearing rules, but when you sell it a few years later, the next buyer won't have access to negative gearing either, so on that front, it's no different from selling a former new build. And any established property bought after the cut-off has no negative gearing at all, which means new builds win on that point outright. So when you sell after the changes take effect, the buyer faces the same negative gearing restrictions, regardless of whether the property was new or established for the previous owner. If there's any "discount" from the loss of negative gearing, it applies to both types equally, so neither trades at a discount relative to the other. And honestly, I don't think that discount will happen at all, because when both types face the same rules, there's nothing to discount against.

Third, since selling works the same either way, you just need to buy a new build with little or no premium and you pick up all the benefits during ownership that established properties can't touch. Negative gearing strengthens your cash flow, lets you hold for longer, and helps you capture the gains that come with time. Established properties can't do that to the same degree, and I've already covered this earlier in the video.

Fourth, let's talk about location. Some people say House and Land packages are always out in the suburbs while established properties let you buy closer to the city. This is a serious misunderstanding. I've already explained in this video why development areas and growth corridors are where the real potential is, and that's exactly why Indian investors are buying there while others aren't. I think the people making this argument are mostly thinking about a few outer suburbs in Melbourne that underperformed over the past five years, but the country is a lot bigger than one city. When you compare new and established at the same price point, that budget will typically land you an established home in an older, low-growth suburb with limited upside, and in industry terms, there's no alpha there. At the same price, a House and Land in a well-chosen development area, even with a small premium, will generally give you more room for profit.

And fifth, we haven't even talked about CGT yet. Under the new rules, anyone buying any established property at any point will only have access to the indexation method for working out capital gains. But the first owner of a new build can choose between the 50% CGT discount and the indexation method, whichever works out better. That alone makes new builds the stronger option.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs