10 Properties to Financial Freedom, Dead Under Tax Reform? | APS152

The CGT and negative gearing reforms dropped, and people lost their minds. Some said property investment is done. Others said sell everything. A few said Australia is going down the same road as New Zealand. So I spent two weeks digging into the data, tracking clearance rates, watching how the market actually responded. And here’s what I found: the only people freaking out are the ones who were leaning on tax subsidies the whole time. The investors who bought the right properties haven’t moved, not one of them. That tells you everything. This Budget didn’t kill property investment. What it killed was the safety net that said “doesn’t matter if you bought wrong.” Negative gearing used to bail you out. You overpaid, picked a dud suburb, and at tax time you’d still claw some of it back. That backup plan is almost gone. In this episode I’ll walk you through what these rules would do to all eight capital city markets, and whether buying 10 properties to hit financial freedom can still work.

How Much Higher Is the Bar

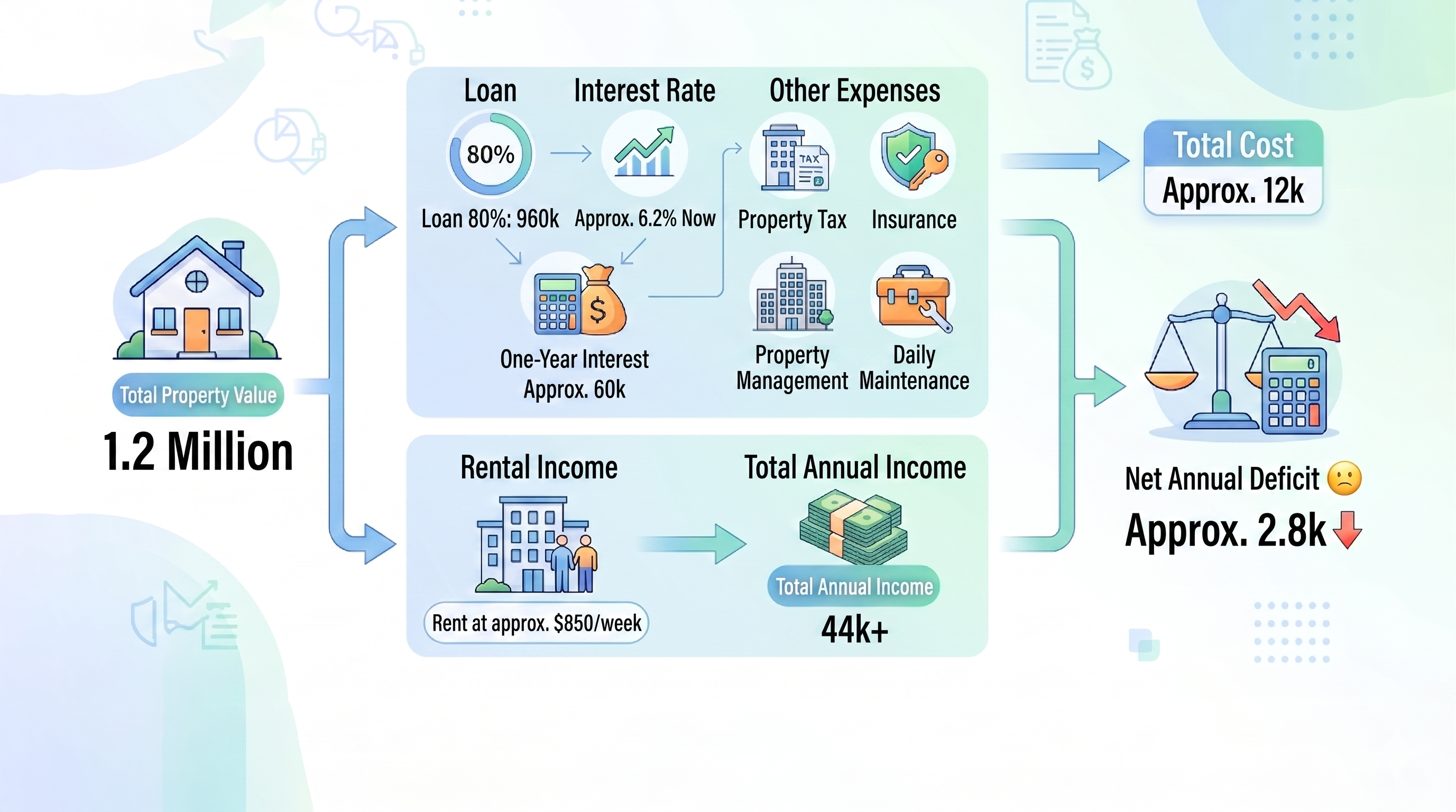

Let me break this down with a quick example. Take a $1.2 million investment property with an 80% loan at 6.2%, and interest alone chews through close to $60,000 a year. Throw in land tax, insurance, management, and upkeep, and that adds another $12,000. Rent at $850 a week brings in just over $44,000. So you’re running at a net loss of roughly $28,000. This won’t fit every property, and I’m not saying every investment ends up negatively geared, but the odds of running negative right now are definitely higher. Residential property is a high-growth, leveraged, low-cash-flow asset. If cash flow is what you’re chasing, property probably isn’t where your money should go.

Before the reforms, at a 47% marginal rate, that $28,000 loss would get you back about $13,000 in tax savings, and that’s before depreciation. So you’d be out of pocket about $15,000 a year. Under the new rules, second-hand property losses can’t offset your personal income anymore. The $28,000 goes out and nothing comes back. For one property, that’s a $13,000 gap. Now picture ten of them, and you’re looking at $130,000 a year in extra cash flow pressure, assuming they’re all held in personal names.

I’m not saying property investment is dead. I’m saying the risk profile has shifted. Before, negative gearing picked up the slack when you bought wrong. Going forward, that cushion shrinks, holding costs go up, and people who can’t carry the weight will drop out. When they drop out, there’s less competition for those who stay. But here’s the thing: not every city gets hit the same way. Higher-yield cities feel less pain, and lower-yield cities feel a lot more. It’s the same policy across the board, but it produces eight very different outcomes. Let’s break them down, but first, a quick recap.

Three Cuts

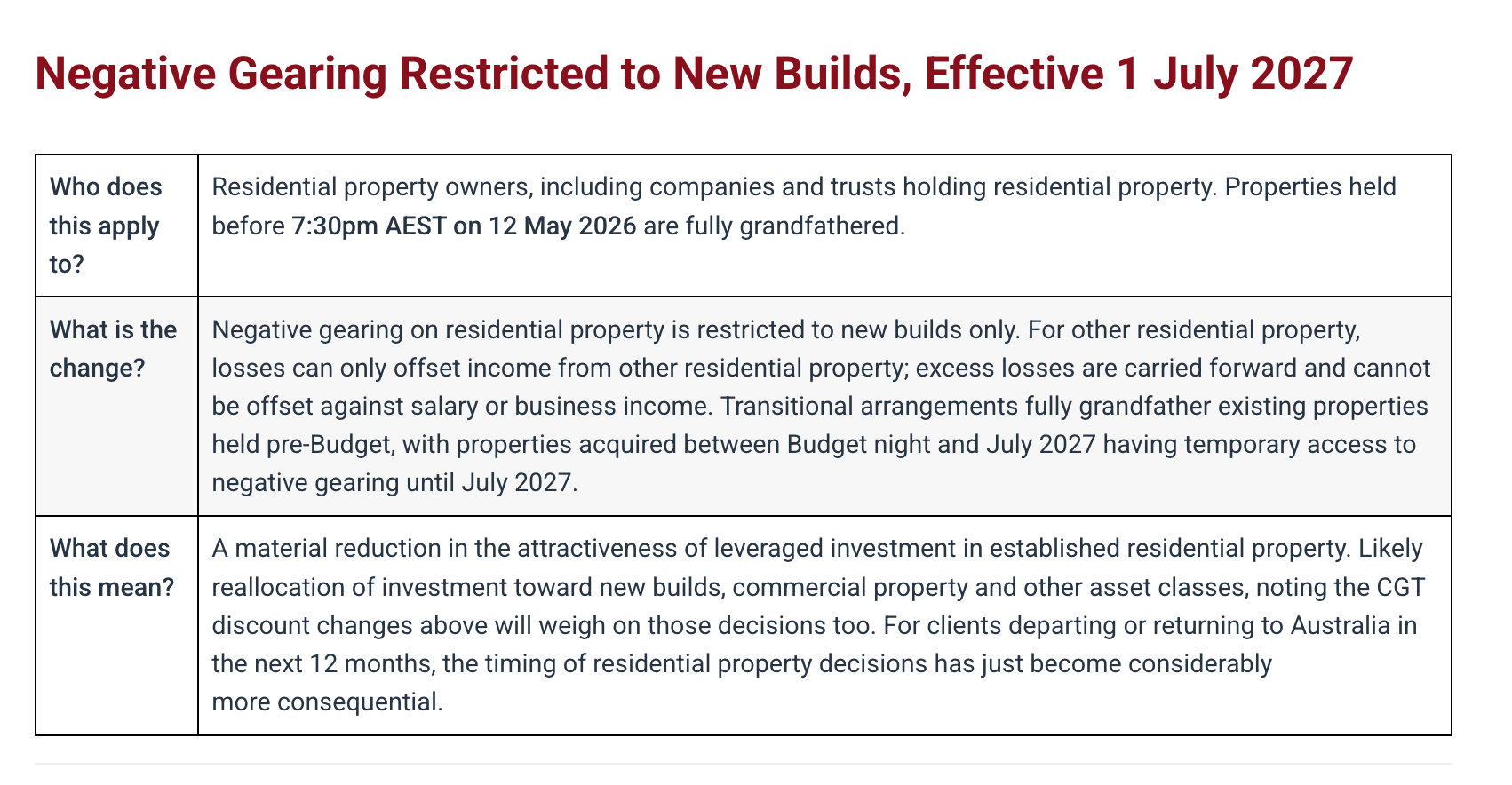

The first cut is to negative gearing. Up until now, any investment property running at a loss could offset that loss against your salary. Going forward, only brand-new properties qualify. Contracts exchanged before Budget night get a permanent grandfather clause. The cut-off day is 12 May 2026. After that date, second-hand property losses get trapped inside your investment portfolio.

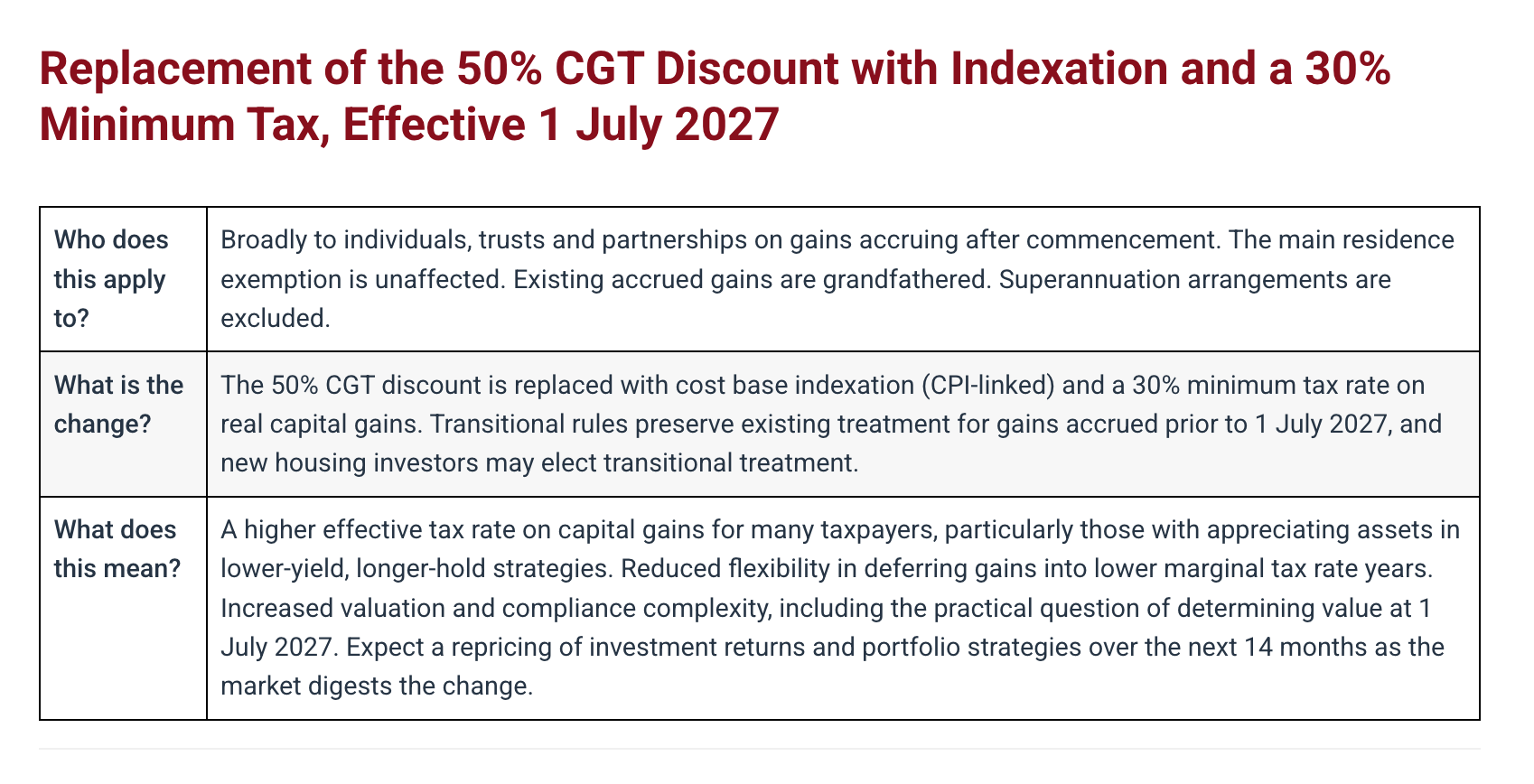

The second cut is to CGT. Under the old rules, a million-dollar gain meant you paid tax on half of it. Under the new rules, you strip out inflation first, then pay at least 30% on whatever real profit is left. But buyers of brand-new residential properties get to pick whichever method works out better for them when they sell.

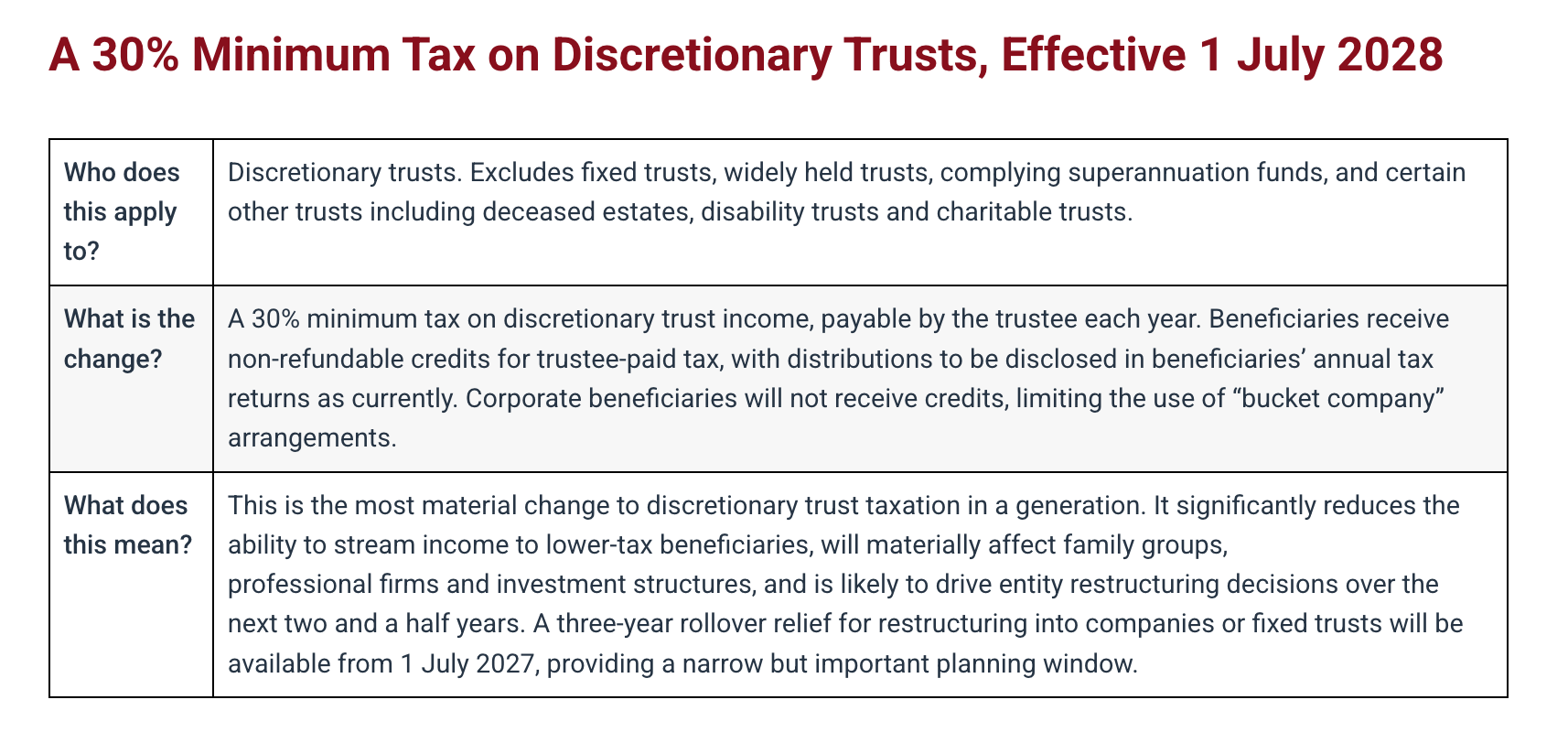

The third cut is a minimum 30% trust tax, kicking in from July 2028. If you’ve been using a bucket company to catch profits, the effective rate could climb past 51% or even above 60%. That strategy is basically dead. But there’s a three-year restructuring window from July 2027 to June 2030 where you can convert to a company or fixed trust without setting off a CGT event.

Three cuts at once, and brand-new residential is the only investment type that holds onto all three benefits. So that covers the rules. But the truth is, rules don’t decide whether you make money. Where you buy is what decides that. Let’s go city by city.

Eight Cities, Eight Windows

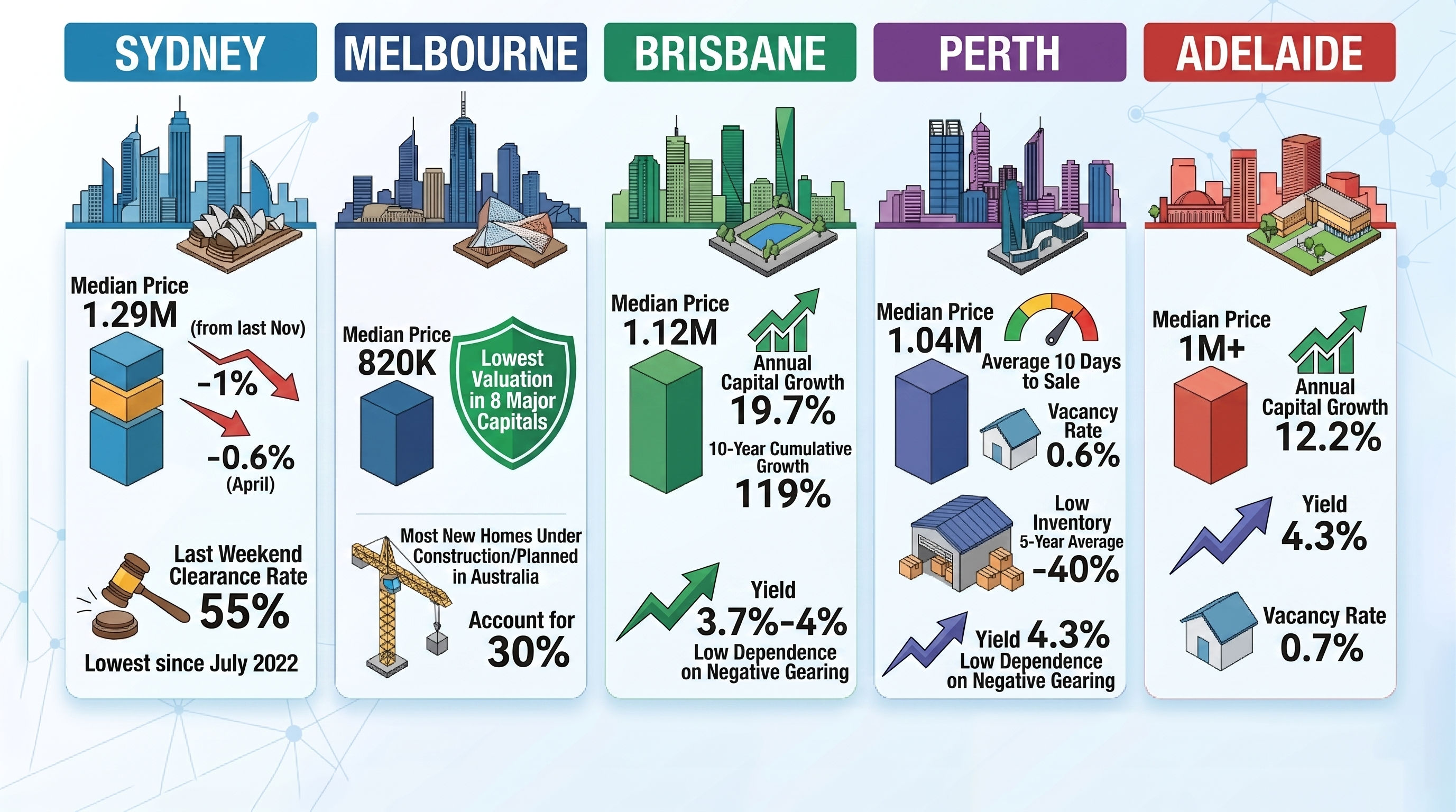

Let’s start with Sydney, where the median sits at $1.29 million, down 1% from the November peak, with another 0.6% drop in April. Last weekend’s clearance rate came in at 55%, the lowest since July 2022. Some people look at those numbers and panic. My view is the exact opposite. When has Sydney ever handed you a cheap way in? The last proper correction ran from 2018 to 2019, and that window stayed open for under two years. Everyone who sat it out has been kicking themselves since.

The reform does hit Sydney harder than anywhere else, because high prices sitting next to a 3.1% gross yield give you the biggest holding loss in the country. But flip it around: investors who can’t hold on will sell up, listings will climb, and negotiating room will open up. I’m keeping my eye on land-and-house packages in the growth corridors, where prices haven’t changed much in two years and every pre-reform tax benefit stays intact. If you go second-hand, push further out to detached houses with a high land-value share, but make sure you run the tax numbers before you commit.

Now let’s talk about Melbourne, with an $820,000 median, down 2.3% from its peak, making it the cheapest of all eight capitals. That price point alone is a built-in buffer. Melbourne has the biggest new-build pipeline in the country, about 30% of the national total, so there’s real room to cash in on the triple tax advantage. But not every new build stacks up. Developer markups and completion delays are real risks, and the suburb you pick matters way more than the product itself. People keep asking me when Melbourne will finally start moving. Look, the value is clearly there, but holding costs and state-level taxes in Melbourne are the highest in the country, and the state government’s finances are under serious pressure. A recovery is coming, but the upside stays limited until there’s a shift at the state level.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

Brisbane comes in at a $1.12 million median, with 19.7% annual growth and 119% cumulative growth over the past decade. Yields sit between 3.7% and 4%, well above Sydney and Melbourne, so the dependence on negative gearing is lower and the reform impact here is pretty manageable. The data speaks for itself. The real question is where you should be buying right now. The 2032 Olympics, Cross River Rail, and Brisbane Metro are all underway, and land-and-house packages near those corridors have a clear growth story for the next five to ten years. But 19.7% a year won’t last forever, and chasing inner-city resales at this point carries real risk. The way I see it, the smartest play is brand-new land-and-house in the middle ring and near suburbs, where you pick up the full triple advantage, ride the infrastructure growth, and keep your yields well above Sydney and Melbourne with far less holding pressure.

Perth is sitting at a $1.04 million median, with 26% annual growth, properties moving in 10 days on average, vacancy at 0.6%, inventory 40% below the five-year average, and yields at 4.3%. The reform impact on Perth investors is among the lightest of all capitals. That said, 26% in a single year is extreme, and a slowdown into 2027 is very likely, although slower growth isn’t the same thing as a downturn. Perth’s problem has never been finding buyers; it’s been finding stock. Brand-new land-and-house packages here are one of the most solid options under the new rules. Just don’t ignore the concentration risk around mining. Never put all your eggs in one city, and that’s the heart of our VISION all-weather approach: always think national diversification.

Adelaide has a median just past $1 million, with yields at 4.3%, vacancy at 0.7%, and annual growth of 12.2%. Under the new rules, its edge actually gets bigger, because reasonable prices combined with high yields keep your holding pressure low and your dependence on negative gearing even lower. If your budget is tighter, this city deserves a hard look. The only things I am concerned about are whether it holds up long-term and the economy.

Hobart has a tight vacancy rate of 0.5%, with rents up 15.2% year-on-year, which is good for cash flow but hard to scale beyond one or two properties. Darwin leads the country on gross yield at 6%, but thin liquidity and single-sector dependence make it too volatile for a reliable long-term hold. Canberra is steady and dependable, but it won’t give you any real breakout upside.

Every city has its own window. The difference comes down to which one you’re standing in front of. And by now you can see it: the opportunity hasn’t gone away, it just looks different than it used to. The era of blindly stacking 10 properties on tax subsidies is fading. But can you still get there? This next part is what matters most.

The New Answer to Ten Properties

Can you still build a 10-property portfolio? Yes, but it’s getting harder every year, because several forces are squeezing at the same time. Second-hand property losses can no longer offset your salary, which adds over $10,000 a year per property in real out-of-pocket costs. APRA capped high-leverage lending from February this year, so once your debt-to-income ratio goes past six, banks can only approve 20% of those loans each quarter, which means your borrowing power just shrank. And the trust income-splitting path has narrowed to a minimum rate of 30%.

The old playbook of “stack 10 and lean on subsidies while you wait for prices to double” is getting very hard to pull off. But has the underlying logic of property investment actually changed? It hasn’t. Capital growth times leverage times holding period equals wealth. That formula hasn’t moved. What’s changed is you need to be sharper about what you buy, where you buy, and what structure you use. Five to seven genuinely well-chosen properties could outperform 10 average ones over 20 years.

That’s not a precise number; it’s a shift in thinking. The old mindset was “buy more.” The new mindset is “buy right,” and then stack as many as you can on top of that. Every single property needs to pass the stress test on its own: is the location right, is the type right, is the structure right, and can it stand on its own feet without subsidies propping it up? That lines up exactly with our Golden 21 Rules, and under the new rules, properties that tick those boxes have a bigger edge than they did before.

On property type, brand-new land-and-house packages are the only investment right now that keeps all three reform benefits intact. You get full negative gearing and the choice between old and new CGT methods in your favour, but it only counts if you’re buying first-hand from the developer or builder. There are three traps to watch out for: the developer’s asking price doesn’t always match market value, completion delays are a genuine risk especially with off-the-plan apartments, and a “near-new” property bought from someone else doesn’t count as new under the rules.

Ownership structure now matters ten times more than it used to. SMSFs come out as the biggest structural winner because all three reforms pass right by them. Companies are also unaffected by CGT indexation, since they never had the 50% discount in the first place. Getting your structure wrong now costs real money, because the old tax cushion that used to absorb your mistakes is gone. This is exactly why structure has been the number one step in our VISION Gold Membership from day one.

Now, one more variable I haven’t touched on. These reforms haven’t passed the Senate. The Coalition says they’ll scrap them, and the Greens want something tougher. The rules are set to kick in on 1 July 2027, but the next federal election has to happen by 2028 at the latest, so there is a real scenario where these reforms pass and then get rolled back. My advice is to prepare as if the new rules are coming, but build in enough flexibility to adjust. If the policy gets reversed, all you’ve done is over-prepared by one step. But if you bet it won’t pass and then it does, you’ve got no fallback. Our 5-4-1 Rule says 50% comes down to location, 40% to your holding period, and 10% to timing. That‘s true no matter what happens.

What You Should Do

If you already own property, don’t panic. Everything bought before Budget night is permanently locked in under the grandfather clause on negative gearing. Your existing investment properties have become scarce assets under the new rules, because any second-hand property bought going forward will never get that same protection. Don’t rush to sell. If you’re holding through a trust, get your accountant onto it now and make full use of the three-year restructuring window. And think seriously about realising some capital gains before 30 June 2027 to lock in the 50% discount while it’s still on the table.

If you’re building your portfolio, it’s time to adjust your direction. The target isn’t “collect 10 properties,” it’s “make every single one bulletproof.” Brand-new land-and-house packages in Brisbane, Perth, and Adelaide offer the strongest value under the new rules, and Sydney’s window could open up further over the next six months.

If you haven't entered the market yet, the bar is higher, and there's no way around that. But you're up against fewer competitors than you have been in years. Some investors are pulling back because of the reforms, which means fewer people are going after the same stock. Start with a brand-new land-and-house package to take advantage of the triple tax break. And consider rentvesting. You rent where you live and invest somewhere else, because it might be the most practical starting point for working Australians right now.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs