CGT Reform: I Built 5 Models to Find the Best Tax Strategy, and It Changed Everything |APS151

Since the federal Budget dropped, the debate has only gotten louder. But not one institution has actually built the models, run the numbers, and figured out the best strategy for property investors under these new rules. A few outlets reported that a bank economist put together a model, but nobody ever saw the workings. All we got was the so-called “results.” So I did it myself. It took me three full days. I went through the Budget documents, dug into the tax legislation, built five mathematical models, and ran each one a thousand times. And look, I’m not saying this reform will destroy property investment in Australia. What I am saying is that the rules have shifted, and if you don’t understand how, you’ll end up paying thousands more in tax than you need to. Today I’m not holding anything back. I’ll walk you through every model as simply as I can, and if you take the time to absorb what I’m about to show you, you will have a serious head start on everyone else.

1. Choosing the Right Holding Entity

If you haven’t watched my last two videos yet, go back and watch those first, because otherwise this one won’t make much sense. Alright, straight into it. The first model answers one question: across six holding periods, from 1 year all the way to 20 years, which entity pays the least capital gains tax?

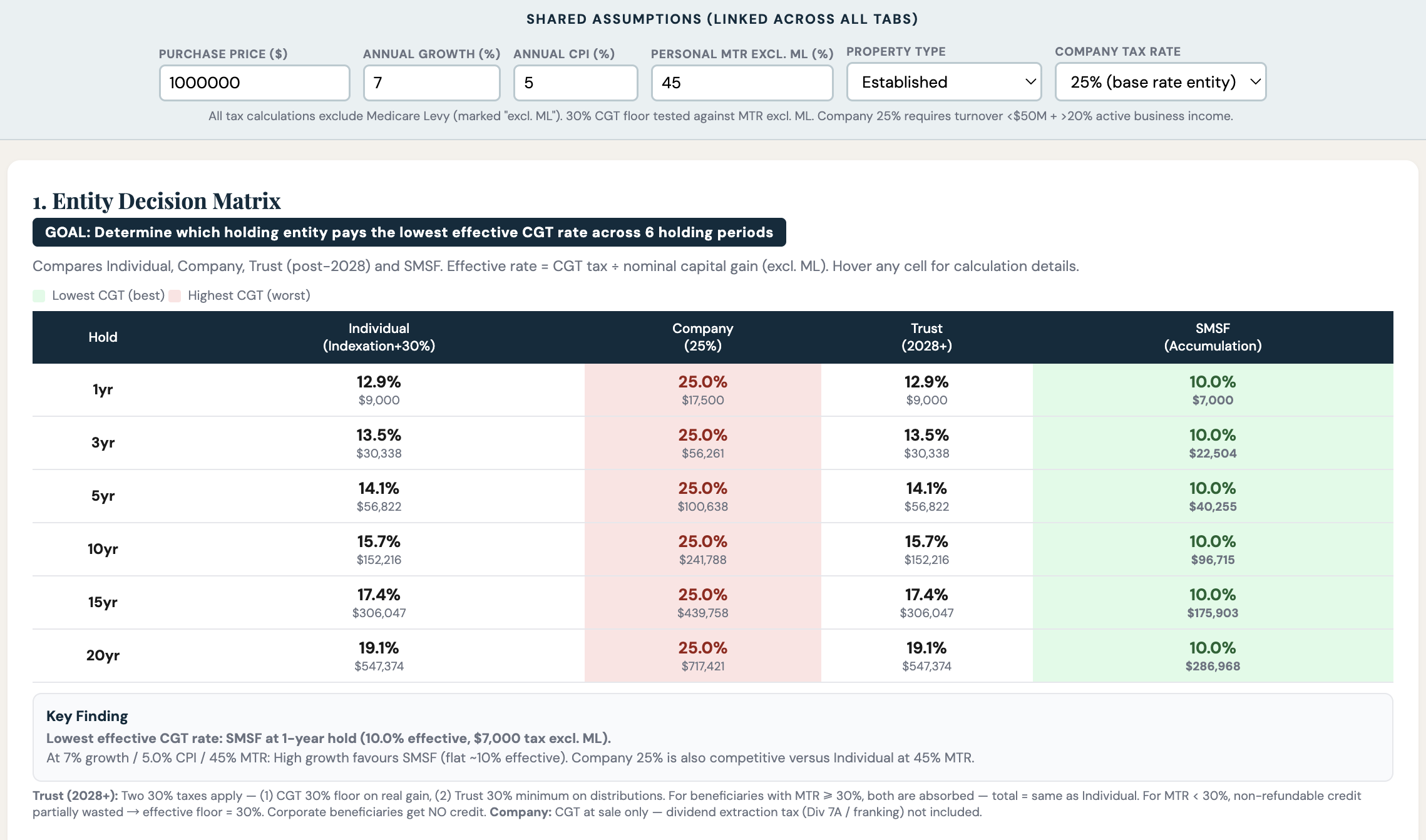

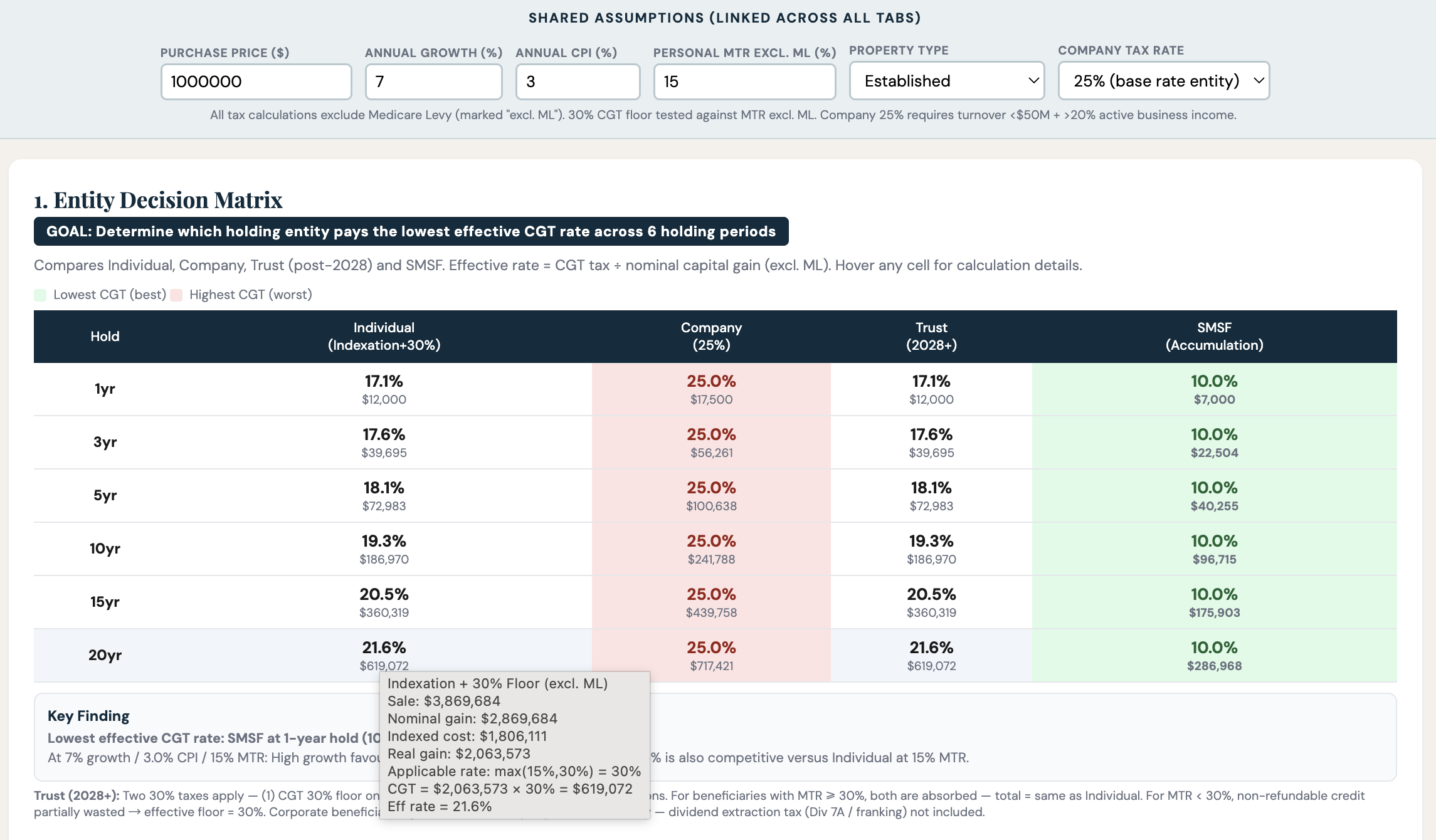

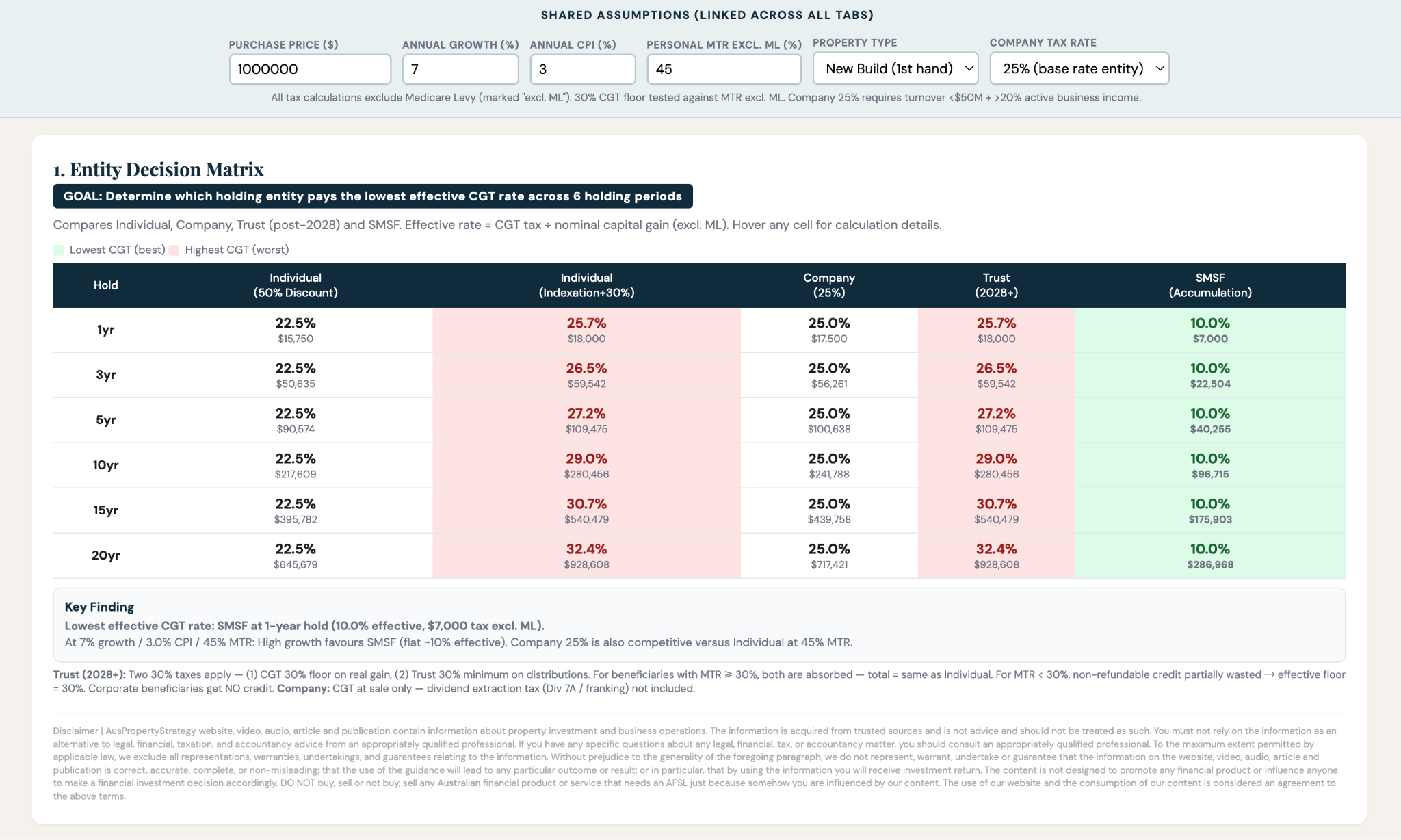

Here are the baseline assumptions, and these carry through to every model that follows. Purchase price is $1 million, annual growth at 7%, inflation at 3%, marginal tax rate at 45% before Medicare Levy, established property, and company tax rate at 25%. There’s one key benchmark to explain first: the Effective Tax Rate. When it comes to CGT, it’s the actual tax you pay on the gain, divided by the nominal gain, which is just the sale price minus the purchase price without adjusting for inflation. If you paid $30,000 in CGT on a $100,000 nominal gain, your effective rate is 30%, and that already factors in any discount. We’ll call this setup “Scenario A.”

Green on the chart means best, as in the lowest CGT. Red means worst. And across every holding period in Scenario A, the answer jumps right out at you. SMSF wins every time because once you’ve held for more than 12 months, the rate is a flat 10%, and that beats everything else hands down. Individual and trust ownership come in dead last at every point. Just to be clear, “individual” here means the post-Budget Indexation method, and “trust” means the position after the 2028 trust reform kicks in. The company sits in the middle at a constant 25%.

Then I started changing one variable at a time to stress-test the results. When growth dropped to 5%, SMSF still won, but the company became the worst because the individual’s effective rate under Indexation shrinks when real growth gets smaller. When inflation went up to 5%, individual and trust rates dropped further, but the ranking held.

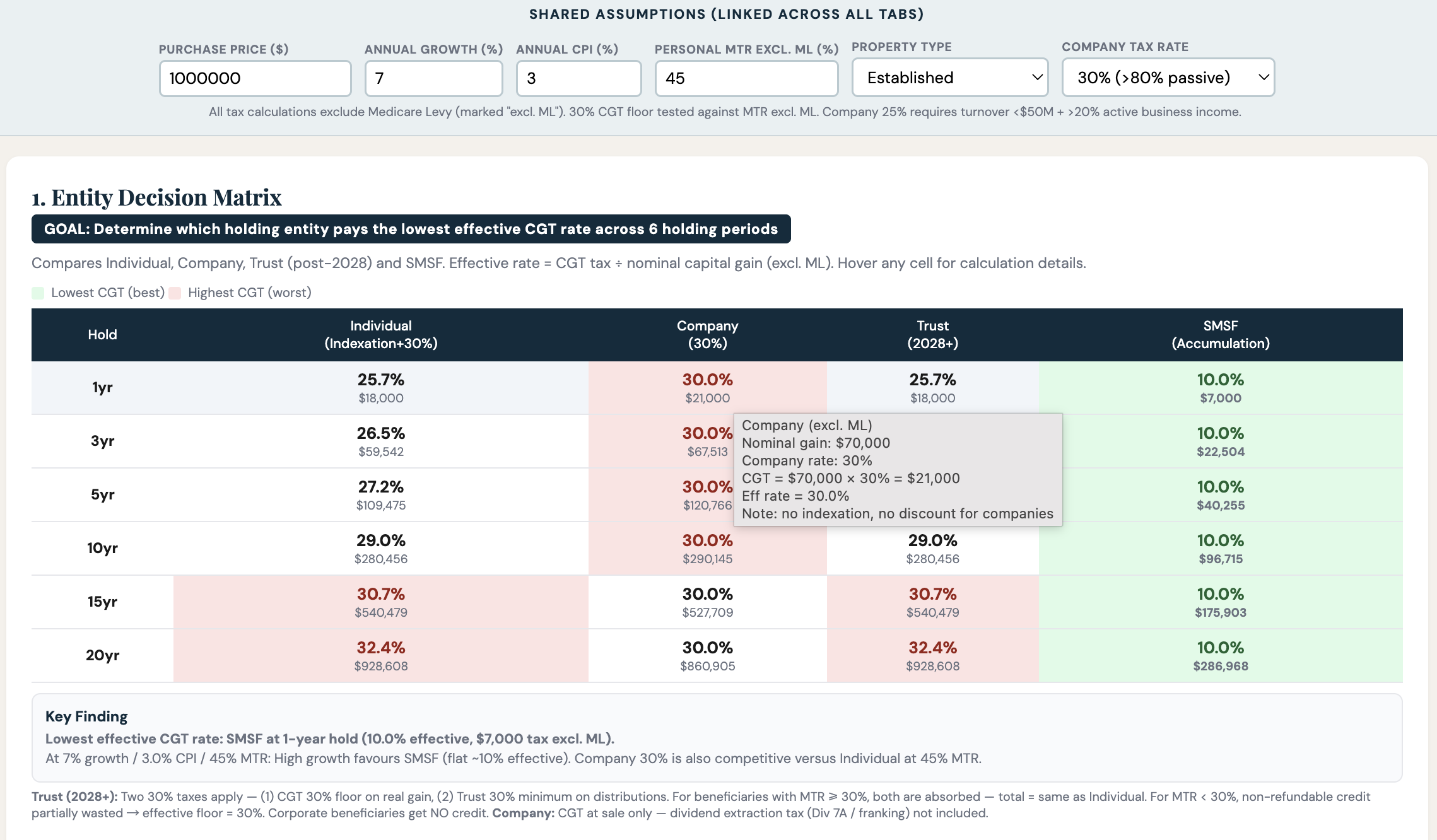

Now here’s where things get interesting. If the company tax rate is 30%, which is the actual rate for a company set up purely for property investment, the results shift. The company turns into the worst option for holdings under 10 years. But after the 10-year mark, individual and trust ownership become worse because their effective rates climb above 30%. And if the individual’s MTR is only 15%, the company is the worst option across the board because the individual’s rate never gets above 25%.

Let’s flip to “Scenario B,” where the property is brand new, meaning you can choose between the 50% CGT discount or the Indexation plus 30% minimum tax when you sell. SMSF is still the best, individual and trust are still the worst, but the individual using the 50% discount now beats the company.

If this is already making you rethink your structure, drop a comment below with your situation. I read every single one.

I ran 6,000 simulations in total, and a few clear patterns came through. The SMSF wins the most with its locked-in 10% rate, completely unaffected by growth, CPI, or holding period. It only loses when real growth after inflation sits around 0.5 to 1%. And that 10% is in the accumulation phase. If you sell during the pension phase, CGT is zero, full stop.

A company never comes out “best” in a pure CGT comparison, but that’s because the SMSF is always lower. Whether a company beats an individual comes down to new versus established. For new builds, the individual always wins because they can pick whichever works out lower, the 50% discount or Indexation, and both come in under 25%. For established properties, the individual can only use Indexation, and once the growth rate passes a certain threshold, the individual’s rate overtakes the company’s. At MTR 45% with CPI 2.5% over 10 years, the company pulls ahead once growth hits 6%. But at MTR 30%, you’d need growth above 11%.

Here’s one that caught me off guard. Indexation for individuals turns out to be a hidden winner in low-growth scenarios. When growth runs close to CPI, say 3% against 2.5%, Indexation nearly wipes out the entire capital gain, and the effective rate can drop to 5 or 6%, actually beating the SMSF’s 10%. But then again, if a property isn’t growing, you’ve got to ask yourself what the point of holding it is.

Trusts with high-MTR beneficiaries give you exactly the same effective rate as individual Indexation. And the 30% floor hits different people in completely different ways. It hammers low-MTR investors the hardest while high-MTR investors barely feel it. The government didn’t help the wealthy with this one, but they definitely took a swing at lower-income investors.

2. Choosing the CGT Calculation Method

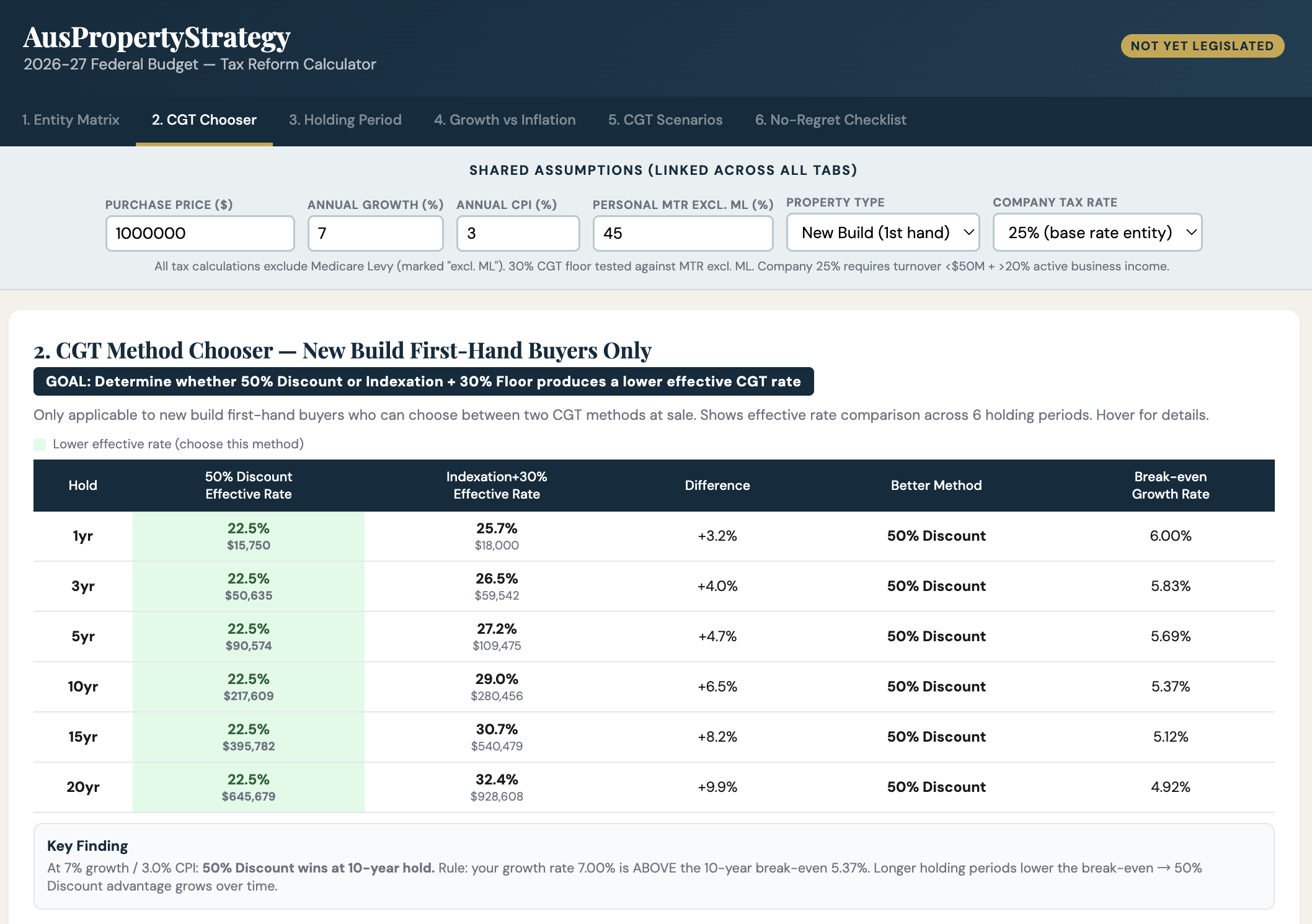

So now we know which entity works best. The second model tackles a different question: when you sell a new build, which CGT calculation method gives you the better deal? You don’t need to decide right now because you can choose at the point of sale, but so many people have asked, so I built the model.

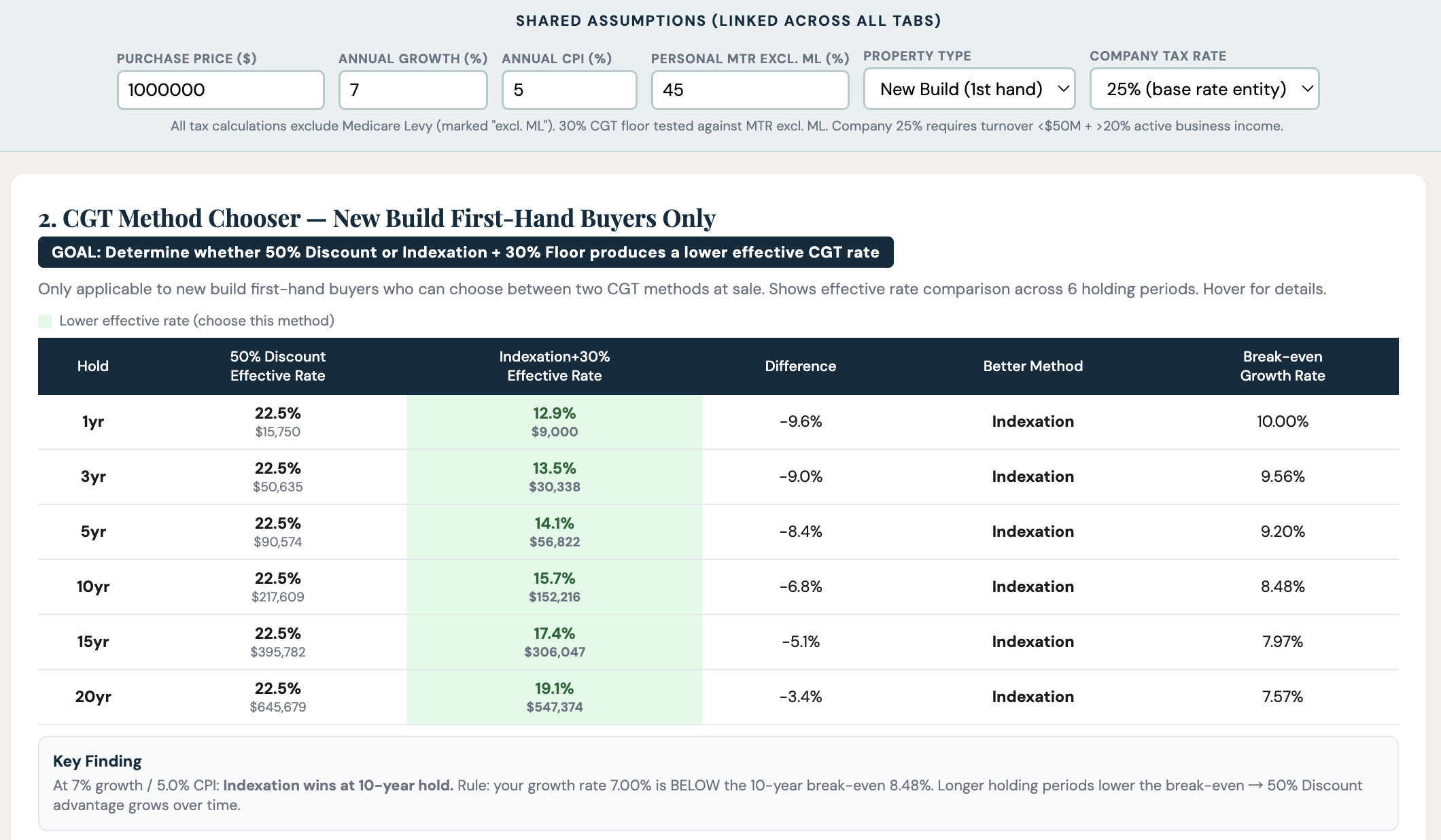

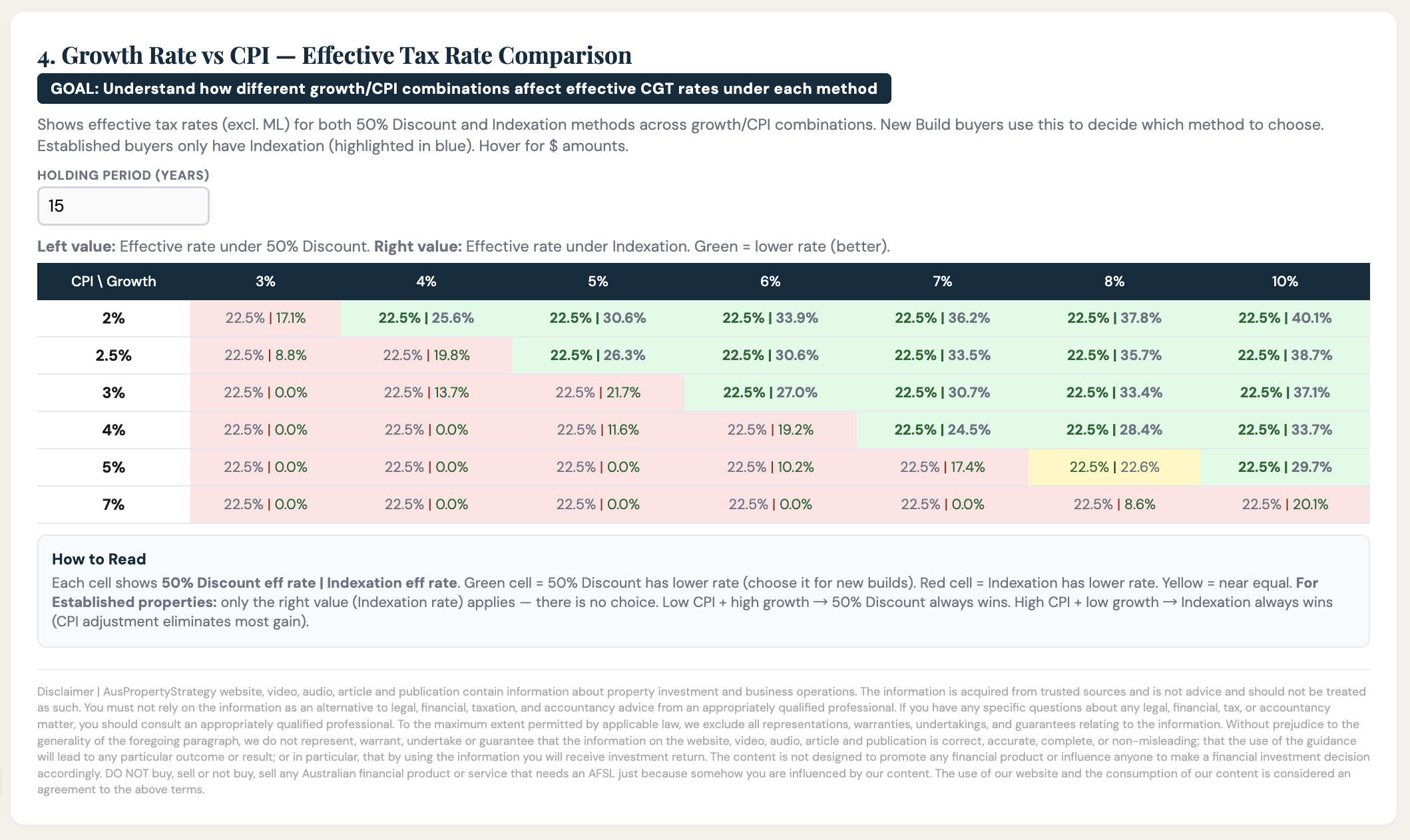

Under Scenario B, the 50% discount comes out ahead in most cases. The longer you hold, the bigger the gap, reaching 10 percentage points at 20 years. The breakeven sits at a growth rate of 4.92%. Above that, the 50% discount wins. But flip inflation to 5%, and the result reverses entirely in favour of Indexation.

What it boils down to is the gap between growth rate and CPI. When that gap is narrow, around 0.4%, Indexation wins. When it’s wide, around 5.5%, the 50% discount wins. The crossover zone sits between 1.5% and 5.0%. Below 1.5%, Indexation almost always wins. Above 5.0%, the 50% discount almost always wins. Anything in between needs to be worked out case by case.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

3. Finding the Optimal Holding Period

So we’ve covered which entity and which method works best. Now let’s look at how holding period plays into all of this. The third model asks: if you want to pay the least CGT, how many years should you hold?

Under Scenario A, SMSF is the clear winner and individual plus trust is the clear loser regardless of holding period. But bump the company tax rate to 30%, and you need to hold through a company for more than 10 years before it starts beating personal and trust ownership.

And here's the part that really matters. For every entity except the company and SMSF, effective tax rates go up the longer you hold. Compound growth pushes nominal gains way beyond what CPI accumulation can keep up with, so Indexation covers a smaller and smaller share of the total gain. In plain English, if you’re holding a high-growth established property in your personal name and relying on Indexation, the longer you hold, the worse off you are compared to the old policy. That’s a big deal, and most people haven’t figured that out yet.

Companies and SMSFs are completely unaffected by the holding period. But new builds held personally really stand out. The effective rate barely moves, averaging between 8.2% and 9.0% across all holding periods. You get to pick the better method at each point: Indexation in the short term because CPI hasn’t pulled away from growth yet, and the 50% discount long-term because compound growth makes the nominal gain much larger than CPI-adjusted costs. The two methods complement each other, and the new-build tax advantage over established properties widens from 4.6% at year one to 7.6% at year twenty.

4. Comparing the Two CGT Methods Across All Scenarios

The fourth model tested 924 different combinations of holding period, growth rate, and CPI. And the big picture is this: the 50% discount wins in 59% of scenarios, and Indexation wins in 41%. The longer you hold, the higher the win rate for the 50% discount.

But whether the old 50% discount or the new Indexation works out better depends on one simple test: is CPI greater than half the growth rate? If it is, then Indexation gives you a better deal. So all those people saying they won’t invest because the 50% discount is gone, or that buying established under the new rules is automatically worse, they need to think again.

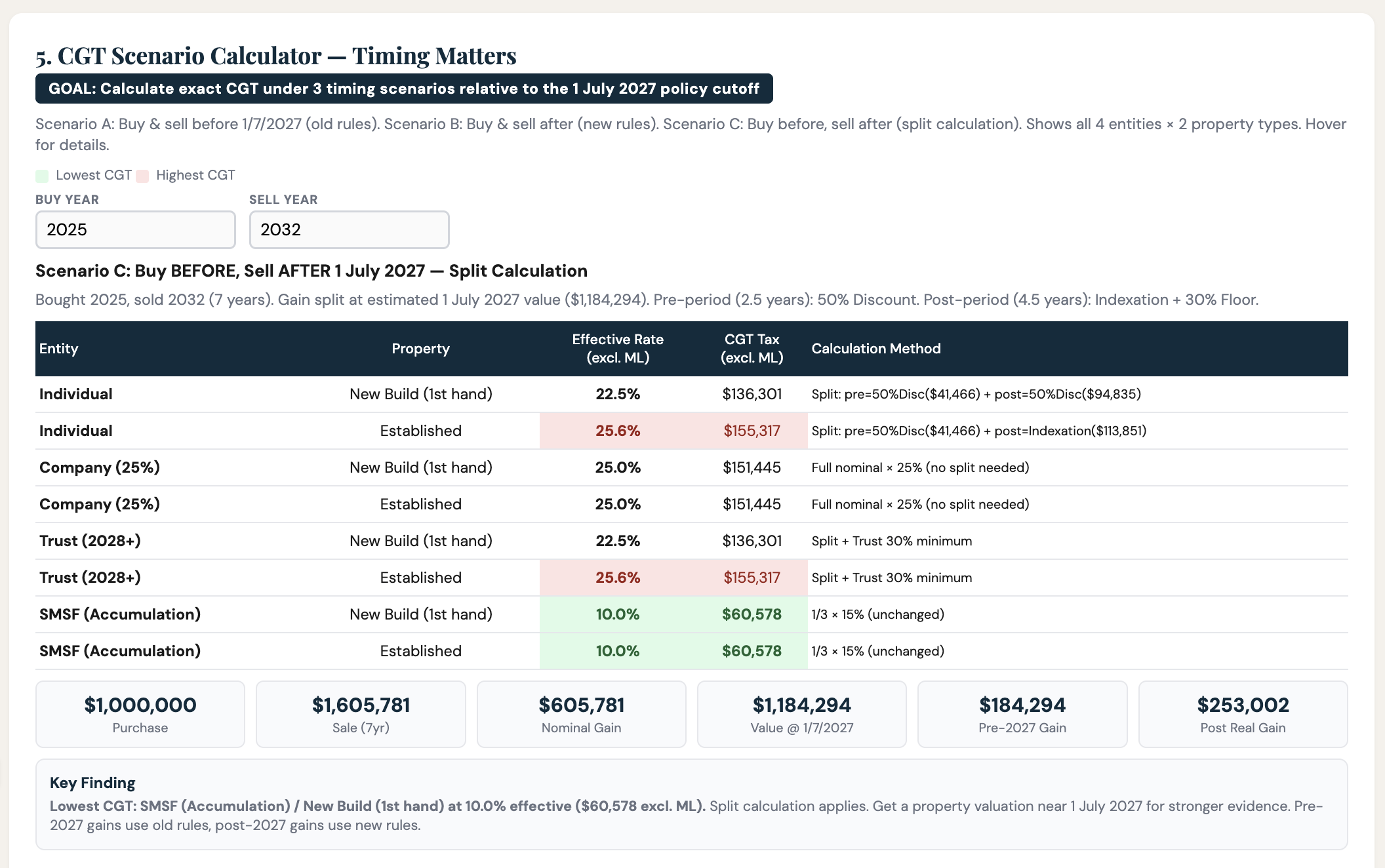

5. How Buy and Sell Timing Affects CGT

The fifth model looks at the 1 July 2027 cut-off. Does it matter whether you buy and sell before, across, or after that date?

Here’s the bottom line. SMSF is the best entity in all three timing scenarios, and buy-sell timing doesn’t change that. Companies aren’t affected either because there’s no discount, no Indexation, and no 30% floor for companies under either set of rules. On average, the individual’s effective rate under the new rules comes in 2.3% higher than under the old rules. This reform has pushed up the CGT bill for individuals holding investment property. And if you don’t take the time to understand what it means and find the best solution for your situation, the real cost will be much more than 2.3%.

Solutions: What You Should Actually Do

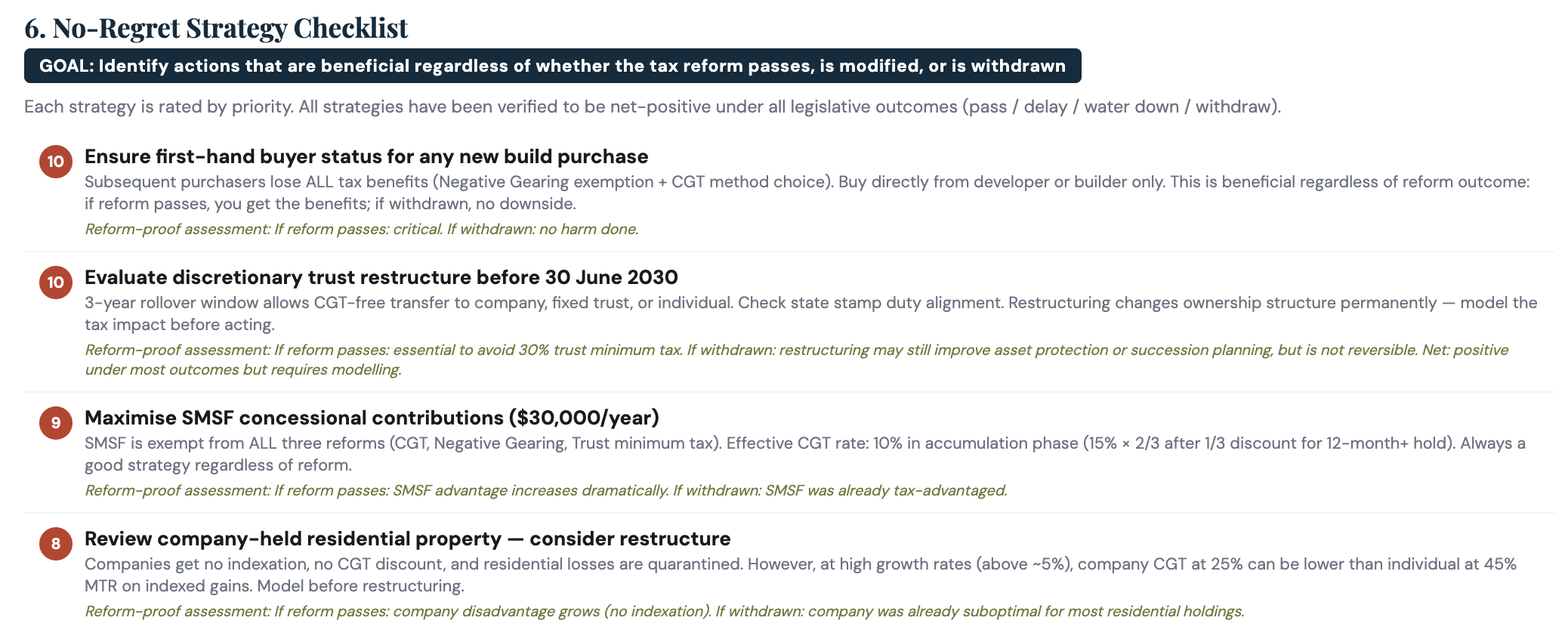

Alright, we’ve gone through all five models. So here’s where we’re at. Is there a strategy that wins no matter what happens next, whether the Senate amends the legislation, whether the government changes hands at the 2028 election, or whether the whole thing gets rolled back?

The answer is yes. I ran the models for a long time and identified 10 solutions. Here are the top four.

The clearest finding is this: buy new. As long as you’re buying brand new and holding long-term, you’re in the best possible position under this reform. Future policies are extremely unlikely to go after new builds because Australia is desperately short on housing, and the government can barely roll out enough incentives.

Second, if you’ve got property in a trust, don’t panic. Wait until the policy is fully locked in before you make any moves. The window runs through to 2030. And don’t write off trusts for the future either, because CGT is only one piece of the puzzle. Asset protection, estate planning, and increasing borrowing capacity haven’t changed.

Third, maximise your SMSF contributions. Under every scenario, an SMSF delivered the single best CGT outcome for residential property. Nothing else came close. Talk to a qualified financial planner about the rules and restrictions. VISION Gold Members can consult directly with our in-house financial planner.

Fourth, my gut feeling was that companies would beat individuals and trusts across the board. But the models showed that’s not always the case. Companies only win in specific situations; qualifying for the 25% rate comes with conditions, and getting finance through a company isn’t always straightforward. This one really does come down to individual circumstances.

This entire suite of models is my own original work. It’s one of many tools we use at AusPropertyStrategy to help members pick properties and make smarter decisions. I’ve rolled it out to our entire strategist team, and I’m confident it will help our members keep more of what they earn.

Before I go, one last thing. To all those property agents on social media who claim they use “data-driven analysis,” the ones from big finance backgrounds, the PhDs who switched into real estate, do you actually understand models? If you do, build one. Put it out there. Use it when you’re helping clients. Stop saying you’re data-driven and then guessing your way through every real decision. This is one of the big reasons why people don’t trust property agents, and why the feeling out there is that most property commentators are just making things up.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs