Australia's Property Tax Rules Just Got Rewritten. After 30 Years | APS160

On 26 June, Australia’s tax reform bill got Royal Assent and became law, (Act No. 49 of 2026). That wasn’t a surprise. What caught everyone off guard is how much changed between Budget Night and the final legislation. The version announced on 12 May and the version that passed are not the same thing. Sections were deleted, rewritten, and added. The Greens managed to slip in a clause nobody saw coming. I’ve already done a full breakdown of the original Budget, so go back and watch that one for the background. Today I’m only covering what changed from Budget to law, and what those changes mean for your investment property. Things that looked serious then look less serious now. Areas that weren’t affected before got caught in the crossfire. Save this one. Every property decision you make from here starts with what’s in this video.

What Changed in the Bill

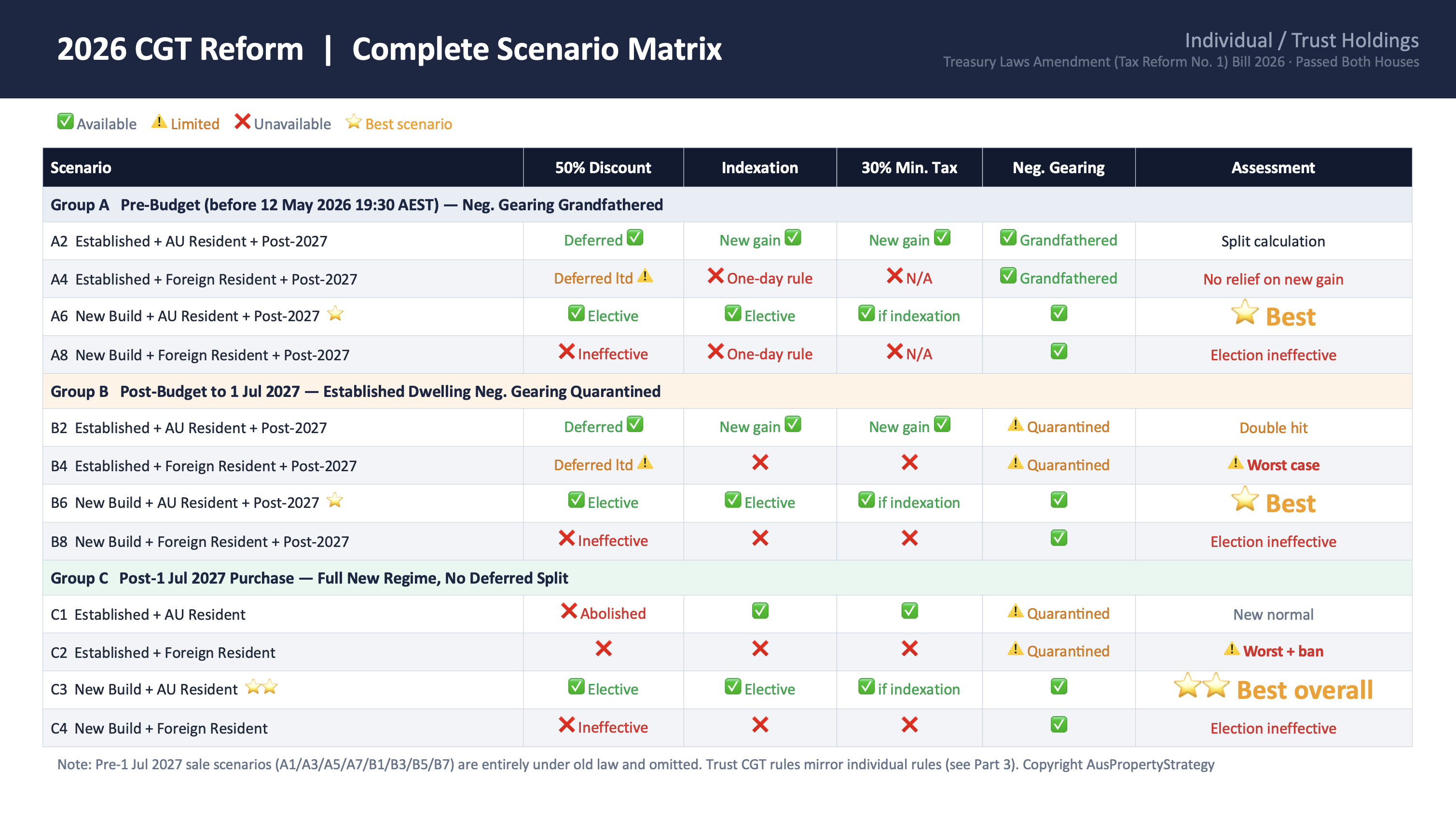

Quick recap of what stayed the same. The CGT 50% discount is being replaced by Cost Base Indexation, plus a 30% minimum CGT tax rate, both from 1 July 2027. Negative gearing is restricted to new builds only. Established dwellings bought after Budget Night can only offset losses against rental income, not your salary. You can carry those losses forward to offset the capital gain when you sell. All of that was in the Budget, none of it changed, and I went through it in the previous episode.

Now here’s what did change. Five things.

1. SMSF lending ban. This wasn't in the Budget at all. The Greens added it during negotiations with Labour. A Greens senator put forward an amendment to the Superannuation Industry (Supervision) Act that stops SMSFs from using Limited Recourse Borrowing Arrangements to buy residential property. Put simply, you can't borrow through your SMSF to buy a house anymore. The ban kicks in on 10 August. Existing loan arrangements are not affected. You can keep them, you can refinance with a different lender, but you can't borrow more. Buying residential property with cash inside your SMSF is still allowed, though whether that makes financial sense is a separate question.

Now the obvious question. Can you rush to set up an SMSF and get a loan through before the deadline? The short answer is, in most cases, I wouldn't recommend it. Setting up the SMSF shell isn't hard; it takes about a week. The problems are everything that comes after.

First, getting money in. If you've never made voluntary super contributions, you can contribute up to five years of unused concessional cap amounts. That goes in tax-free, but you'll pay 15% tax inside the fund. You can also put in after-tax money. Between a couple, putting together around $400,000 is doable, but whether you actually have that kind of cash is another matter.

Second, if you don't have enough and you've been contributing to an industry or retail fund, you'll need to roll that balance over into the SMSF. That process alone takes at least two to three weeks.

Third, SMSF lenders generally require two financial years of contribution history. If your SMSF was set up in the 2026-27 financial year and your previous fund doesn't have a strong contribution track record, getting a loan approved will be very difficult.

Fourth, SMSF loan approvals are already slow, and whether one can be approved before 10 August is a real question mark. Both the property contract and the loan agreement have to be signed before that date. Our lending strategists say applications needed to be in before 30 June to have a realistic chance, because banks and even non-bank lenders have already tightened the rules. By the time you're watching this, that date has passed. The reality is you'd be applying for a loan with no certainty that it gets approved in time.

Fifth, and this is the one that matters most. If you're only chasing the lending benefit and ignoring the quality of the property itself, you've got it wrong. We've built a model and found the threshold where SMSF property actually comes out ahead of financial investments. You need a 20-year average interest rate below 5.5% (7%-7.2% now for SMSF lending), annualised capital growth above 6%, gross rental yield above 4.5%, and you need to hold until retirement when the CGT rate drops to 0%. All four conditions at the same time. On top of that, you'd need to find a regional property in the $600,000 to $800,000 range that you're comfortable holding for 20-plus years, because that budget doesn't buy a decent metro house, and you'd need to find it within about 30 days. Over the past 30 years, regional detached houses in Australia have averaged less than 5% capital growth per year. The last couple of years looked good, but that's not the long-term trend.

If you've already got an SMSF, already started your loan application, and are already in the process of finding a property and negotiating, then yes, you can keep going. But time is extremely tight. Find something reasonable and move quickly.

One thing I need to point out. Buying property through super is far more complex than buying in your personal name. You need to think about whether you can hold for 20-plus years to get that 0% CGT rate in retirement. You need enough other financial assets inside the fund so that one asset doesn't dominate the portfolio. At current SMSF loan rates above 7%, with typical loan-to-value ratios of 50% to 60%, you'll almost certainly be running negative cash flow, so your annual contributions need to be enough to cover the holding costs. And then there are the family and life factors: relationship breakdowns, inheritance disputes, control issues, withdrawal rights, and the situation where a deceased member's assets have to be sold to pay out beneficiaries, which can trigger a 17% tax hit. These are questions that need a wealth planner, not just a buyer's agent, a real estate agent, or an accountant working in isolation. That's exactly why we put together a team of specialists across every area to serve our members.

I've heard accountants working with buyer's agents have been swamped these past few days, rushing clients through the "last 45 days" window. That's a marketing line, not financial advice. The things I've just laid out are the kinds of details those buyer's agents won't share with you, because it goes against their interests. I also run a buyer's agency, and I'm set up for SMSF purchases. But I'm not the same. I'm fact-driven, not commission-driven. Find the facts first, then see if the right direction can make you money, and I'll make some along the way. That's the business logic behind AusPropertyStrategy. What I don't want to see is people getting swept up by sales talk, then spending money and time setting up an SMSF under pressure, only to have the loan not approved in time, or to rush into a bad property, or to overlook retirement and family factors beyond the property itself. That's why I said, in most cases, I wouldn't recommend it.

2. Trust 30% minimum tax removed from the bill. This was one of the three pillars on Budget Night, a minimum 30% tax on discretionary trust distributions. It got pulled from the final law and pushed to a separate bill called Tranche Two. The start date is still listed as 1 July 2028, but in Australia, “announced and not legislated” has a long history of going nowhere.

Now here’s the trap. If you use a bucket company to receive trust distributions, and this 30% minimum eventually comes in, the company tax you’ve already paid won’t count as a credit. The combined effective rate can reach 62% or higher. On top of that, trusts holding investment property will face the same CGT changes as individuals. The 50% discount gets replaced by indexation. If you hold property in a trust, look at both changes together before you make your next move.

3. Widow tax legislative defect. Independent senator Pocock raised this during Senate scrutiny, and it could hit around 680,000 jointly held investment properties across the country.

Here’s the problem. You and your spouse jointly own an investment property bought before Budget Night. You have grandfathering protection. But if your spouse passes away, or you divorce and ownership transfers, the law treats that as a new acquisition. Grandfathering disappears. The Finance Minister, committed in the Senate to fixing this through Tranche Two. No one knows when that would happen.

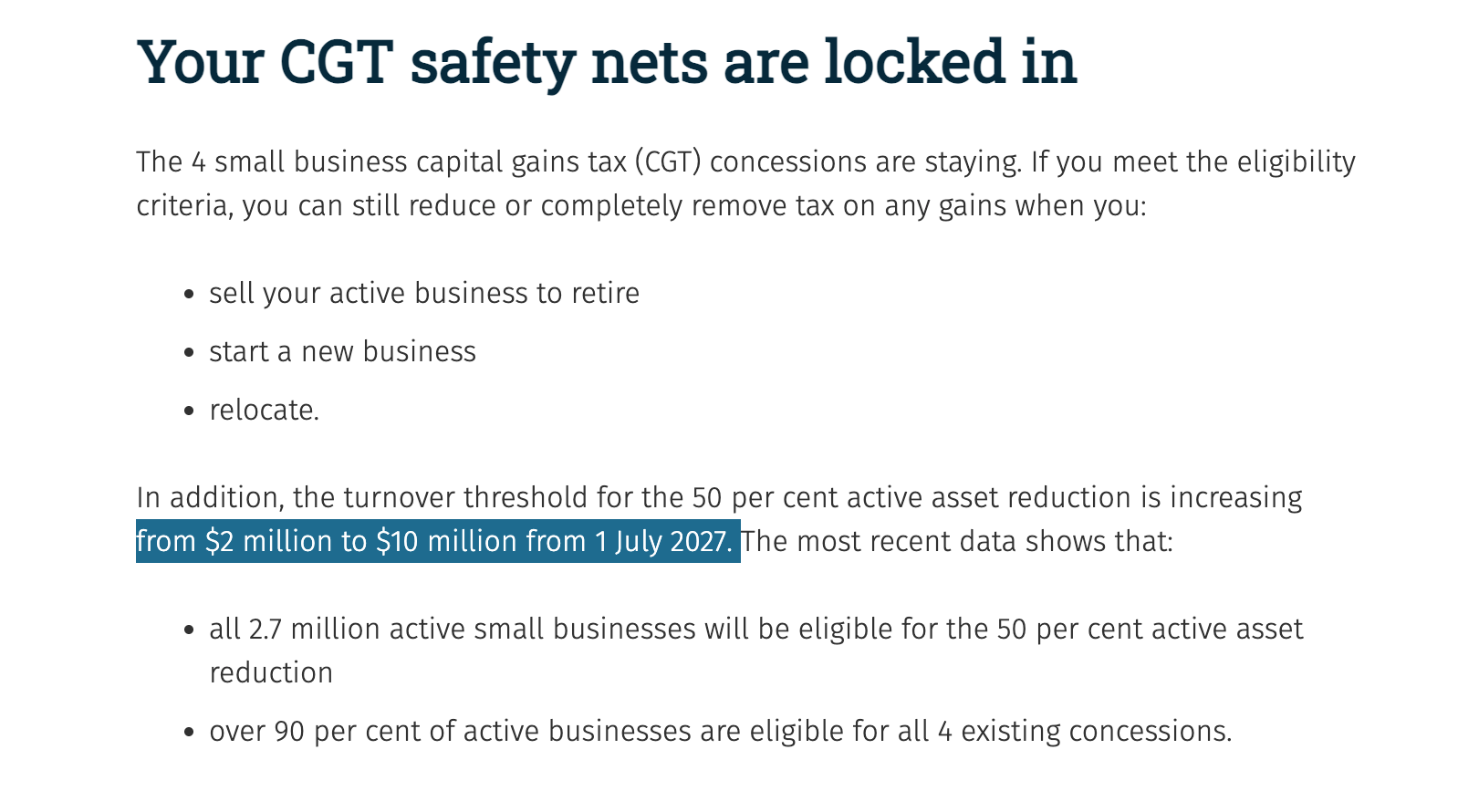

Points 4 and 5 quickly. The Greens stripped the Treasurer’s power to expand CGT discount categories by regulation, so any future changes need to go through the full legislative process. The back door for reversing the current direction is basically closed. And the small business CGT active asset reduction threshold went from $2 million to $10 million, covering roughly 2.7 million businesses. If you sell a business for a $1 million profit, you get the individual 50% CGT discount, stack the small business reduction on top, and your taxable capital gain drops to $250,000. Very generous.

So that’s what changed in the bill. Now the more important question. What does all of this actually mean for the property market, and what should you do about it?

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

Impact on Property Prices and Rents

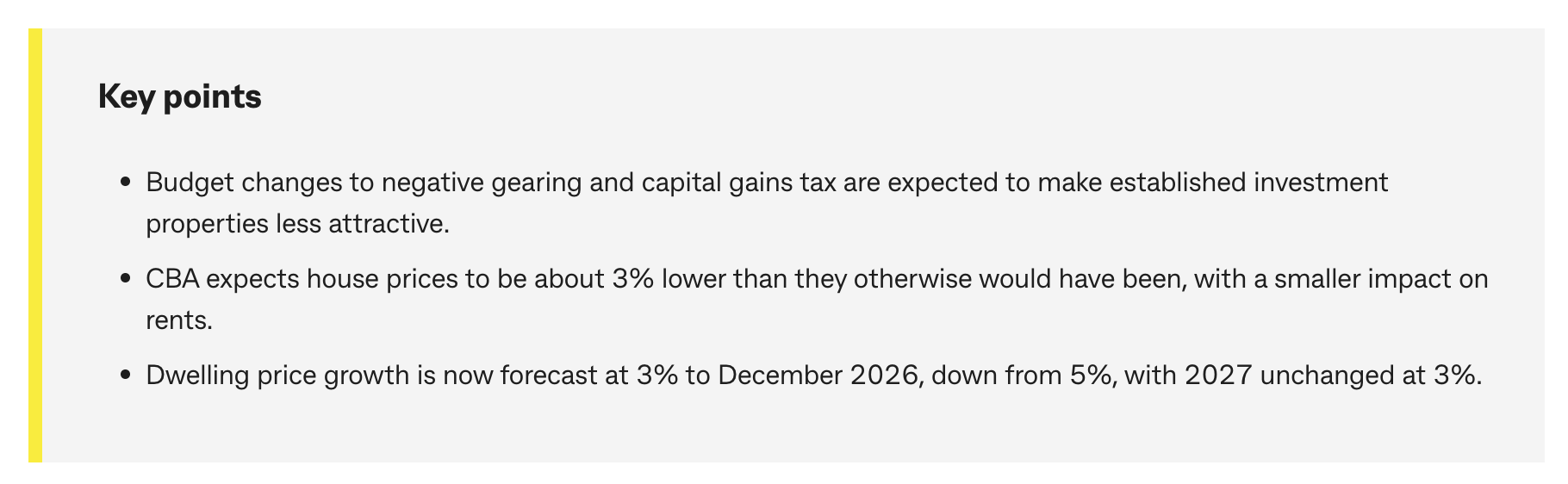

1. Established dwellings will see a lock-in effect. If you held an investment property before Budget Night and sell it, you lose grandfathering. Buy another established property and your losses are ring-fenced to rental income only. The maths doesn’t work either way, so a lot of investors will simply hold. That compresses listings and partially offsets downward price pressure. CBA modelled this and puts the impact at 3% to 5% lower growth than without the reform. That’s not a 3% to 5% fall, it’s slower growth. Those are completely different things. CBA’s latest forecast is that national prices will be roughly flat this year, down from their earlier prediction of 3% growth.

CBA also estimates the cash flow hit from ring-fenced negative gearing is equivalent to a rate increase of 0.9% to 1.55%. So if you buy an established investment property now, the holding pressure feels about the same as rates going up by 1% to 1.5%. New builds don’t have this problem.

2. New builds are the biggest winner from this reform. Negative gearing stays. And when you sell, you choose between the old 50% CGT discount and the new indexation method, whichever gives you a lower tax bill. Investor demand will shift from established to new-build, which is exactly what the policy was designed to do. Industry modelling shows the negative gearing restriction could cut new housing starts by about 22,700 over five years, and the CGT changes could cut another 33,000. So new builds end up with stronger price support than established. In every scenario, new builds come out ahead.

3. Rents. Treasury puts the rental impact at less than $2 a week. But there’s a precedent. When the Hawke government pulled negative gearing in 1985, rents only jumped in Sydney and Perth, where vacancies were extremely low. The national vacancy rate right now is 1.2%. Supply and demand will drive rents more than tax policy will.

Now for the most practical part.

What You Should Do Now

If you already own investment property purchased before Budget Night on 12 May, the message is simple. Don’t sell unless you have a very good reason. Grandfathering is the most valuable asset in your portfolio right now. You keep negative gearing while you hold. Sell, and you can’t get it back on an established replacement. New builds keep full negative gearing regardless of purchase date. On CGT, all established properties switch to indexation for gains after 1 July 2027. Gains before that date still get the 50% discount. New builds sold after 1 July 2027 get to choose whichever method works out lower. That’s a structural advantage.

A few things to do right now. Before 30 June 2027, get a market valuation on every CGT asset you hold. Your home doesn’t count. For investment properties, use a registered valuer. For listed securities, use the closing price on the day. CPA Australia estimates the national cost of these transition valuations will run between $300 million and $800 million. Valuers will be in very high demand. Book early. If you jointly own investment property, talk to your estate planning lawyer about the widow tax issue before doing any voluntary ownership transfers between spouses.

If you’re entering the market or adding to your portfolio, look at house-and-land packages or brand-new established townhouses. Here’s why. You pick up a double tax advantage: negative gearing on losses against your salary, and a choice of CGT methods when you sell. You won’t find a brand-new detached houses still with the builder or developer on the market. Don’t count on finding one. Brand-new completed townhouses do exist, and counter-cyclical stock is worth looking at. Sydney is a good example. By member request, we may trial a group-buy project for new Sydney townhouses in the coming weeks. Reach out if you’re interested. Established property has lost a lot of its tax appeal. If you buy established, you need to re-run your numbers based on ring-fenced losses and look for positively geared properties, which are very hard to find right now.

Now this is important. Not everything that looks new qualifies as “new residential premises” under the tax law. Major renovations don’t count. Granny flats don’t count. Off-the-plan properties resold before settlement don’t count. Under the 541 rule, 50% of the outcome comes down to location. But under the new tax system, getting the property type right matters a lot more than it used to.

Wrapping Up

The bill has passed and the rules have changed. Good policy or bad policy, that debate is over. Where you sit under the new rules and what you do next is what counts. We’ve already put together internal documents, reference guides, and financial models for our members. If you’re a VISION Gold Member, book a free consultation with your strategist to go over your portfolio and adjust your strategy.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs