Australia's Next Interest Rate Shock Is Hiding in Plain Sight|APS154

A month ago, the market was betting that the Reserve Bank of Australia would hike rates again in June. That bet has completely fallen apart. All four of Australia’s biggest banks, CBA, Westpac, NAB, and ANZ, are now calling the same thing: June 16th, no change. And the market agrees, pricing in a high chance of a hold.

Sounds like a done deal, right? It’s not. Because two things should keep you up at night. First, Westpac changed its prediction. What did it see that made it back off? And second, June isn’t the date that matters. August is. Whether your mortgage rate goes higher comes down to a single number.

Two Data Releases That Changed Everything

Two sets of numbers came out in May, and they turned the whole conversation on its head.

First up, let’s talk about jobs. On May the 21st, the ABS dropped the April employment report, and the numbers were ugly. Unemployment jumped to 4.5%, the highest reading since November 2021, a four-and-a-half year high. The economy shed close to 20,000 jobs in a single month, the first decline in five months. And youth unemployment shot up to 11.1%. That’s more than one in ten young Australians out of work.

Now, here’s how much that number mattered. On the same day it landed, NAB, one of the Big Four, ripped up its “June hike” forecast and pushed it to August. A single data release made a top-tier bank flip its call within hours. That tells you everything about how sensitive the situation is right now.

Here’s how to think about it. Hiking rates is the RBA’s way of slamming the brakes on an economy that’s running too hot. But when the labour market starts cooling off on its own, the RBA doesn’t need to step on the brakes again. The engine’s already losing speed. You might be sitting there thinking, “My job is fine, this doesn’t affect me.” But think again. When a bank looks at your loan application, it’s not just looking at you. It’s looking at the whole employment picture behind you. That picture is getting shakier, and when it does, banks tighten up. Your pay hasn’t changed, your savings haven’t changed, but the amount you can actually borrow could be quietly shrinking. Because the bank sees a shakier economy, and it prices that in.

Right now, APRA’s serviceability buffer is still sitting at 3%. In plain English, when a bank tests whether you can handle a loan, it takes the actual mortgage rate and adds 3% on top. With rates at 6.3%, the test rate is 9.3%. Your repayments get stress-tested at that level. Now think about what happens if the RBA pushes the cash rate to 4.60% in August. That test rate climbs with it. The slice of borrowing power you lose to a single rate hike might only be $20,000 or $30,000, but that can be the exact gap between affording the property you want and missing it.

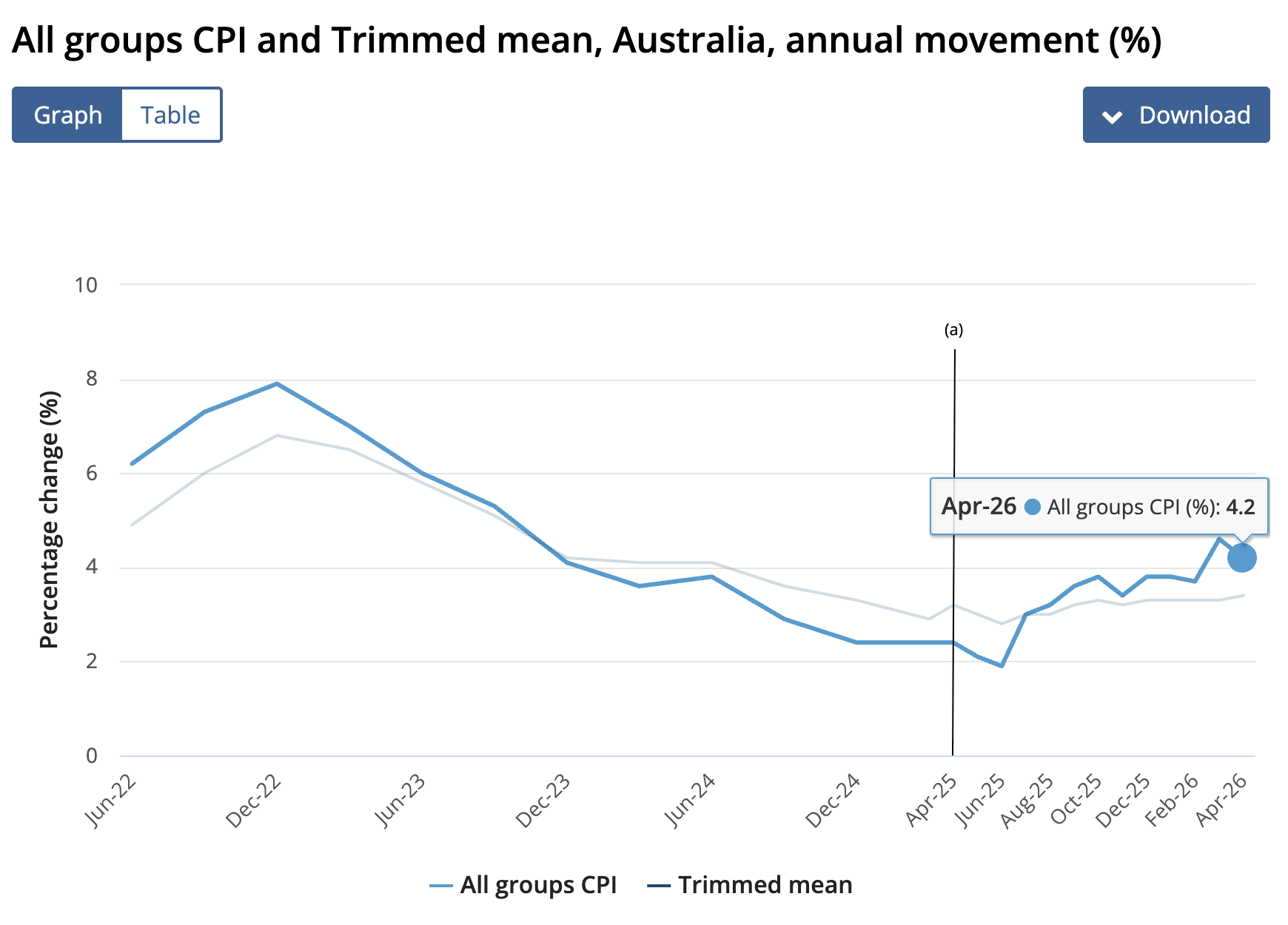

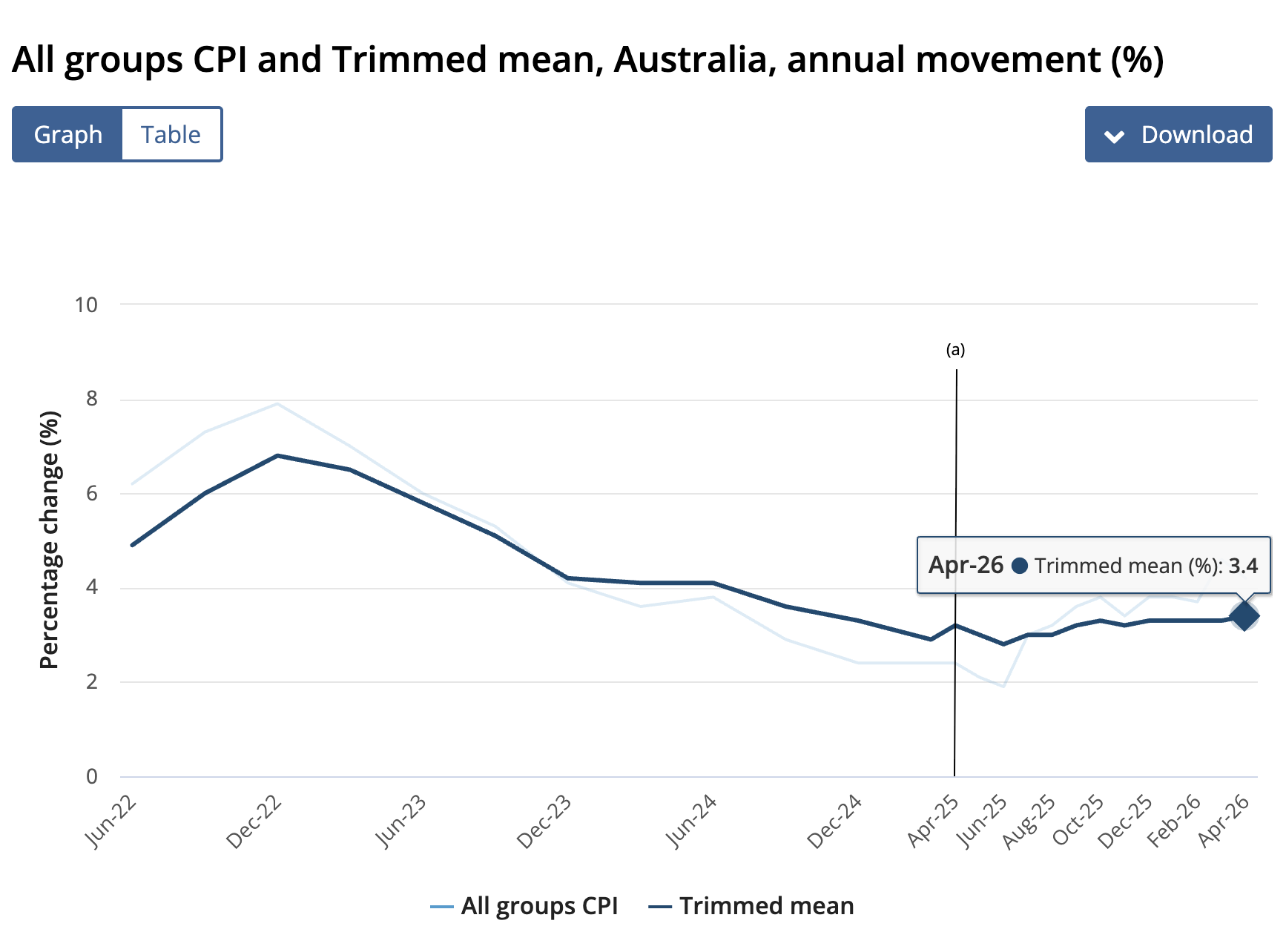

Now let’s talk about the other number: inflation. On May 28th, the ABS reported that April headline CPI dropped from 4.6% to 4.2%, beating the market’s expectation of 4.4%. On the surface, that’s great news. Inflation coming down plus unemployment going up gave the RBA plenty of room to sit on its hands in June. But here’s the thing: while all four banks agree on a June pause, when you look at what they’re saying about August, the picture cracks wide open.

So what dragged that 4.2% number down? The answer is fuel excise. The government slashed fuel excise in half at the end of March, chopping more than 26 cents off every litre. Petrol prices dropped 7% in April alone, and that pulled the whole CPI reading lower. But this is a temporary fix. On July the 1st, full excise comes back. When that happens, headline inflation in the second half is almost certain to bounce back by 0.3 to 0.5%. I’m not saying the sky is falling. I’m saying the June number looks calmer than reality actually is, and the second half of the year tells a very different story.

Has the Rate Peaked?

Alright, so all four banks say “hold” in June. Everyone’s getting along. But look past June into the second half of the year, and you’ll see two camps that could not be further apart.

Let’s start with the doves, the ones who think the hiking cycle is done. CBA, the Commonwealth Bank, Australia’s biggest lender, believes 4.35% is the ceiling. Their view is we’re now in a long hold, and rate cuts won’t show up until 2027 at the earliest. ANZ is in the same boat: topped out, nothing more to come. These two banks are basically saying, the war is over.

Then there’s the hawks. NAB, the bank that tore up its forecast the day the jobs data came out, still thinks the RBA will hike once more in August, taking the cash rate to 4.60%, and then hold. And then there’s Westpac. Westpac is the most aggressive of the lot. It’s calling for hikes in both August and September, pushing rates all the way to 4.85%, with no cuts on the table until 2028. The logic from their chief economist Luci Ellis is clear, and honestly, it’s hard to dismiss. Core inflation, the Trimmed Mean, is still trending upward, and once fuel excise comes back in July, that pressure builds even further.

Now here’s the part most people miss. The headline CPI we just talked about fell from 4.6% to 4.2%, but CPI is jumpy. Oil prices move, and CPI follows. The Trimmed Mean CPI strips out the volatile stuff and shows you what’s really going on underneath. That’s the number the RBA actually bases its decisions on. And it went from 3.3% up to 3.4%. That means the ripple effects of higher fuel costs are already spreading through the broader economy.

So stop and think about this for a second. Four of Australia’s biggest banks are all looking at the exact same data, and their conclusions range from “it’s over” all the way to “two more hikes are coming.” If you feel lost trying to figure out where rates are heading, join the club. They can’t agree either.

Who’s right and who’s wrong? August will sort it out. Banks use models to come up with these numbers. But there’s another group putting real money where their mouth is. Let’s see what they’re betting.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

Real Money on the Line

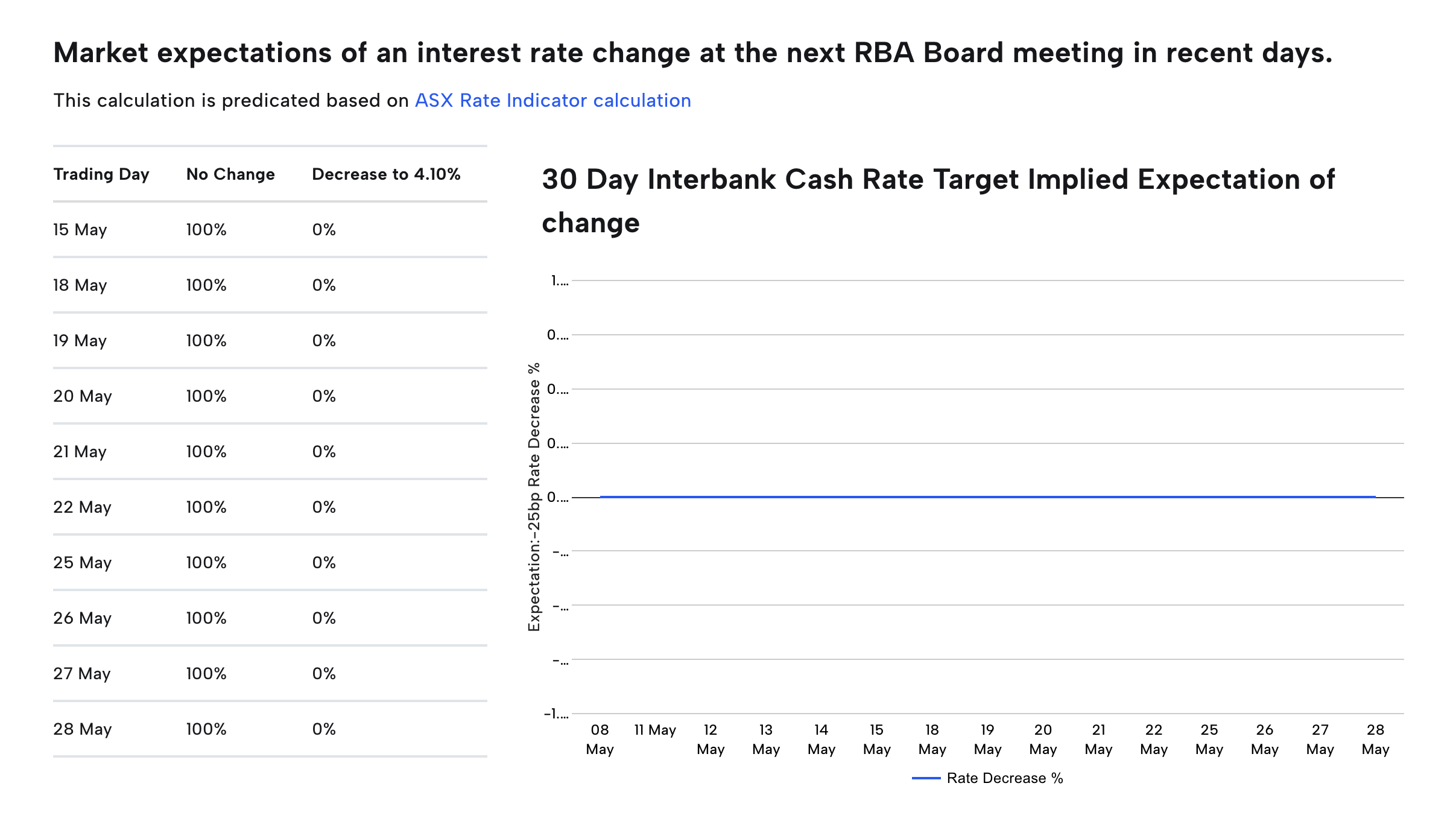

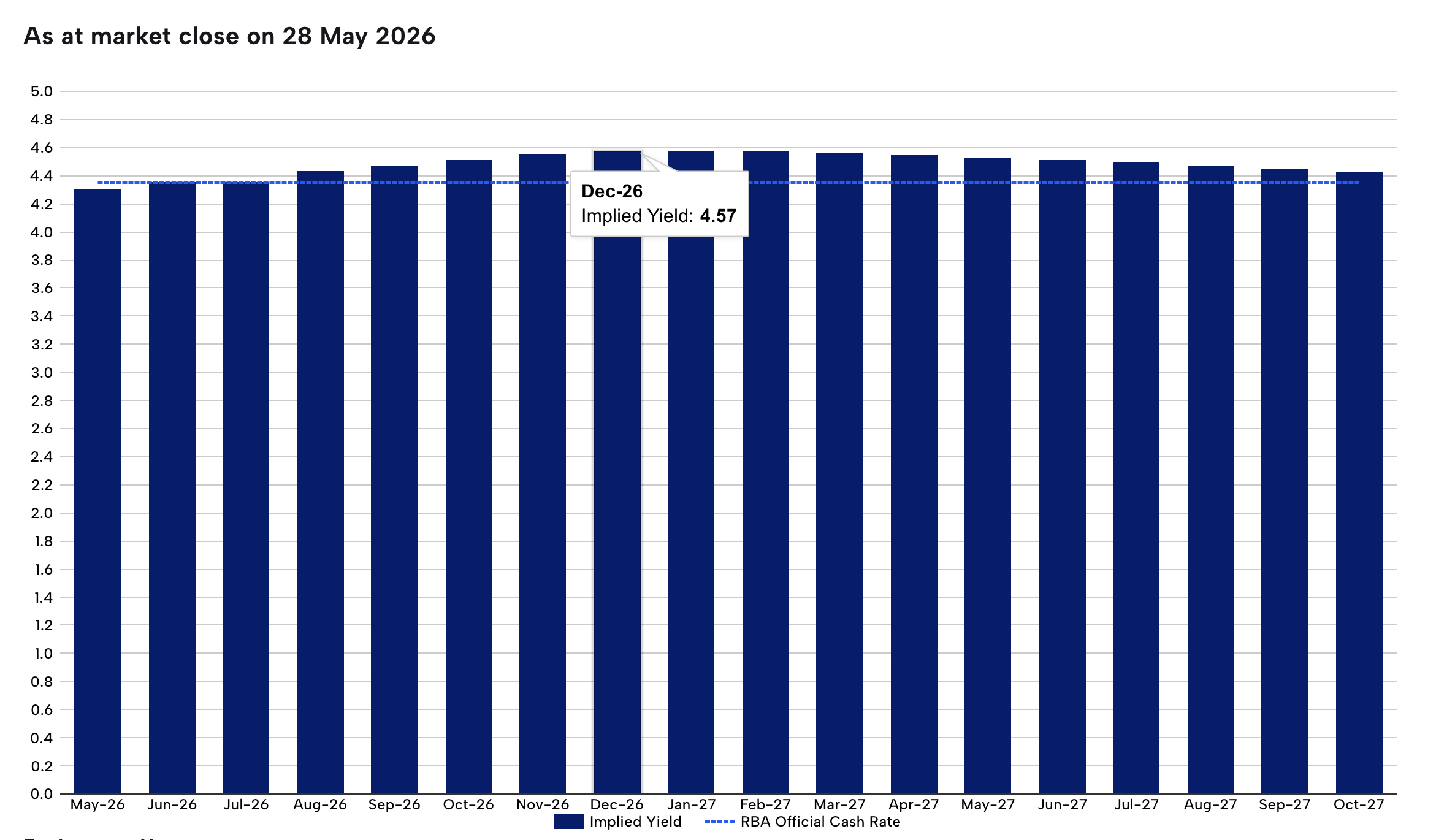

There’s a tool called the ASX RBA Rate Tracker, and it works like this. Traders buy and sell contracts called 30-day cash rate futures. The price of those contracts reflects how likely they think a rate change is. The ASX converts that price into a probability. So this isn’t someone’s opinion. This is money talking, and money tends to be honest.

As of May the 28th, the market was giving June a 100% chance of a hold.

But here’s where it gets interesting. Before the April unemployment data came out, the market was still giving a 13% chance of a June hike. The second that data landed, the probability vanished. And the market’s current bet is that the cash rate will end 2026 at 4.60%. That means the market sees one more hike coming in the second half.

So you’ve got banks running their models, the market putting down real cash, and both are pointing at the same conclusion: June is locked in, but August is still very much alive.

What You Should Be Watching

A lot of people are going to hear “Big Four plus the market all agree, no June hike” and jump straight to the conclusion: rates have peaked, cuts are right around the corner. That would be a mistake.

No hike in June does not mean the top is in. The market’s own year-end pricing of 4.60% has another hike baked right into it. Core inflation, the Trimmed Mean, isn’t just sitting still. It’s climbing. In April it hit 3.4%, the highest since September 2024. On top of that, fuel excise comes back in July, so inflation pressure in the second half is more likely to go up than down.

The real game is in August. And there are four signals you should be watching closely.

First, keep your eyes on the Q2 core inflation data. The quarterly CPI numbers come out at the end of July, right before the August meeting. If the Trimmed Mean keeps climbing and pushes through 3.5%, an August hike is practically a done deal. The RBA’s own forecast has Q2 hitting 3.8%, and if that number lands, a hike is for sure.

Second, watch oil prices. Brent crude was sitting around US$91 at the end of May, partly on the back of US-Iran ceasefire talks. But that ceasefire hasn’t been signed yet. If Brent pushes back above US$100 and holds there for two weeks or more, the hawks’ case for another hike gets a whole lot stronger.

Third, there’s the fuel excise snapback on July the 1st. This is the biggest inflation time bomb ticking in the second half of the year, and I’m not being dramatic about it.

Fourth, pay close attention to the meeting minutes coming out on June the 17th. More important than the rate decision itself is the language the RBA uses about August. Read the minutes. The wording tells you more than the outcome.

At AusPropertyStrategy, when we build investment plans for our VISION Gold Members, we follow one core principle: don’t gamble on whether rates go up or down. Follow the cycle signals. That means reading where the RBA sits in the hiking cycle, what stage the economy is at, and then making your move. Right now, rates are high and choppy, and the direction isn’t clear yet. You shouldn’t be making a one-way bet. When you’re picking a city and timing your entry, interest rates are always a key factor, and right now, that factor is pointing straight at uncertainty. June will probably be a hold, but the door for August is still wide open. In a window like this, the timing of your entry carries more weight than usual. I’m not saying try to pick the exact bottom. I’m saying you need to know how many bullets you’ve got left and how far they’ll reach.

The way I see it, there are two things worth doing right now.

First, go back and recalculate your borrowing power. It’s not a fixed number. Every 0.25% rate move shifts your maximum loan amount. On an $800,000 loan, if August brings another hike, the amount you can borrow today could drop to $770,000. That $30,000 gap doesn’t sound like much, but it can be the difference between reaching the property you want and watching someone else buy it.

Second, if you’re planning to buy within the next six months, go and get a pre-approval now. Lock in the current assessment criteria while they’re still the same.

As soon as the rate decision drops, I’ll put out an instant breakdown video covering what it means for mortgage holders, for people getting ready to buy, and I’ll update my call on where August is heading. If you want to catch it first, subscribe and hit the bell.

And if you’re tired of trying to guess rates and timing on your own, and you’d rather have a professional team help you work out your borrowing capacity and your buying window, VISION Gold Membership could be the starting point you need. The link is in the description below.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs