Australia’s 30-Year Property Super Cycle Is Over! I Read the Full Report | APS156

Last month, national house price growth hit zero. And just like that, every major outlet ran the same headline: “Australia’s 30-year property super cycle is over.” A 5,000-word report by AMP Chief Economist Shane Oliver went viral. He said prices would drop 5%, the house bubble had hit 36%, and all five engines behind three decades of growth had stalled. But I went through Oliver’s original report, word by word, and what I found was nothing like what the media was pushing out. His analysis is sharp; he lays out real problems. But towards the end, he wrote one paragraph that changed how I see the whole picture. And here’s the kicker: almost nobody who covered this report ever quoted it. So, where is the market actually heading? Let’s pull the whole thing apart.

The Market Has Changed

Before we dig into the report, let’s set the scene with three numbers.

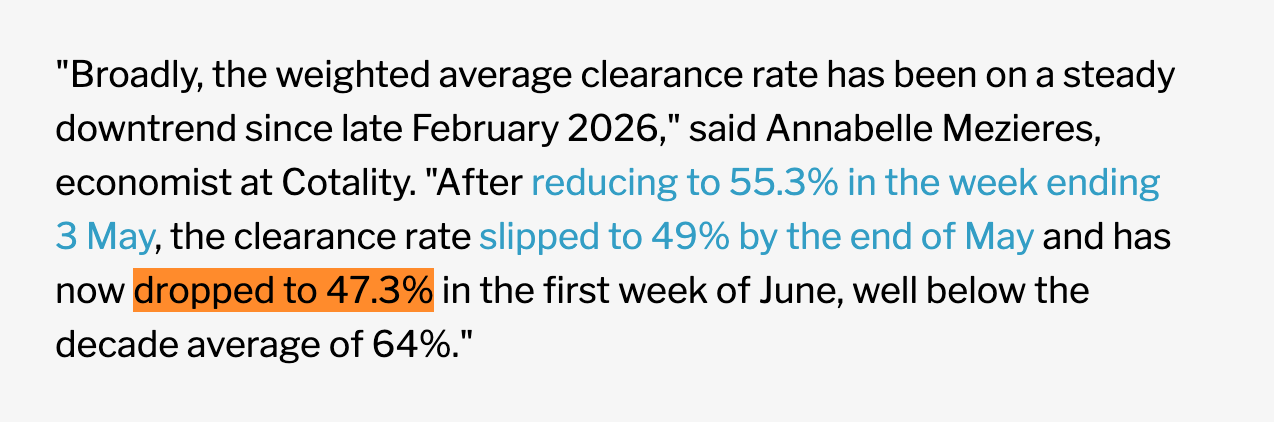

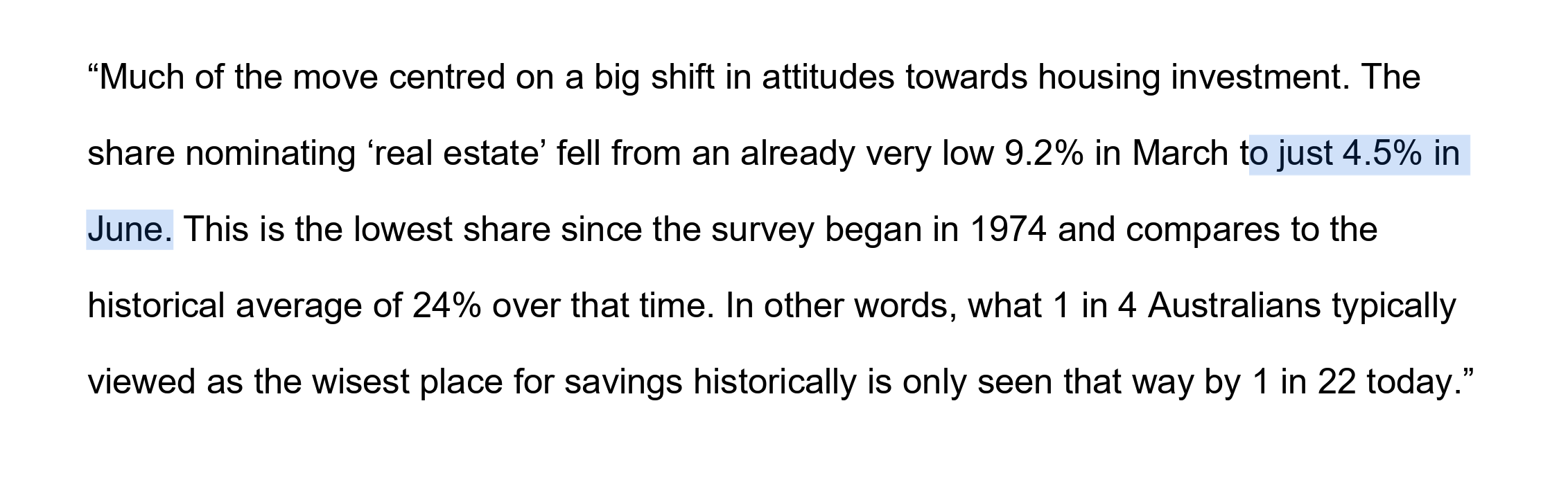

Number one: 0.0%. National price growth in May was completely flat. Capital city prices dipped 0.1%, two straight months of decline. Number two: 47.3%. That’s the national auction clearance rate, against a ten-year average of 64%. We’re pinned below 50%, the lowest since the COVID lockdowns. Number three: 4.5%. Westpac and the University of Melbourne have run a survey for 52 years asking, “What’s the smartest way to save?” Only 4.5% picked property, a 52-year low. The average is 24%. In plain English, out of fifty people surveyed, only one still thinks property is a good bet.

So price growth has stalled, buyers are watching from the sidelines, and confidence is basically gone. And the spread between cities keeps getting wider. Perth is up 26% over the past year, and Sydney managed just over 2%. That’s a tenfold spread.

Now think about what that feels like on the ground. If you’re a first-home buyer, your parents could pick up a house on three or four times their salary. Today, that’s close to 9-14 times. Mortgage repayments chew through 45.9% of pre-tax income nationally, and in Sydney it’s above 54%. With clearance rates cooling off and prices softening, you might finally catch your breath. If you’re an investor carrying multiple mortgages, rates have climbed from 3.6% to 4.35%, repayments have jumped by hundreds a month, and the Budget just tightened the tax breaks. But in Perth or Brisbane, you can’t even get your hands on anything affordable without a fight.

It’s the same country, but three completely different experiences. The market is splitting apart faster than ever, and Oliver isn’t asking whether prices tick up or down next month. He’s asking the bigger question: have the structural forces that pushed prices up for 30 years finally run out of steam?

What the Report Actually Says

Oliver calls the current situation a “perfect storm,” with rates rising, affordability worsening, buyer confidence collapsing, and tax changes hitting investors all at the same time.

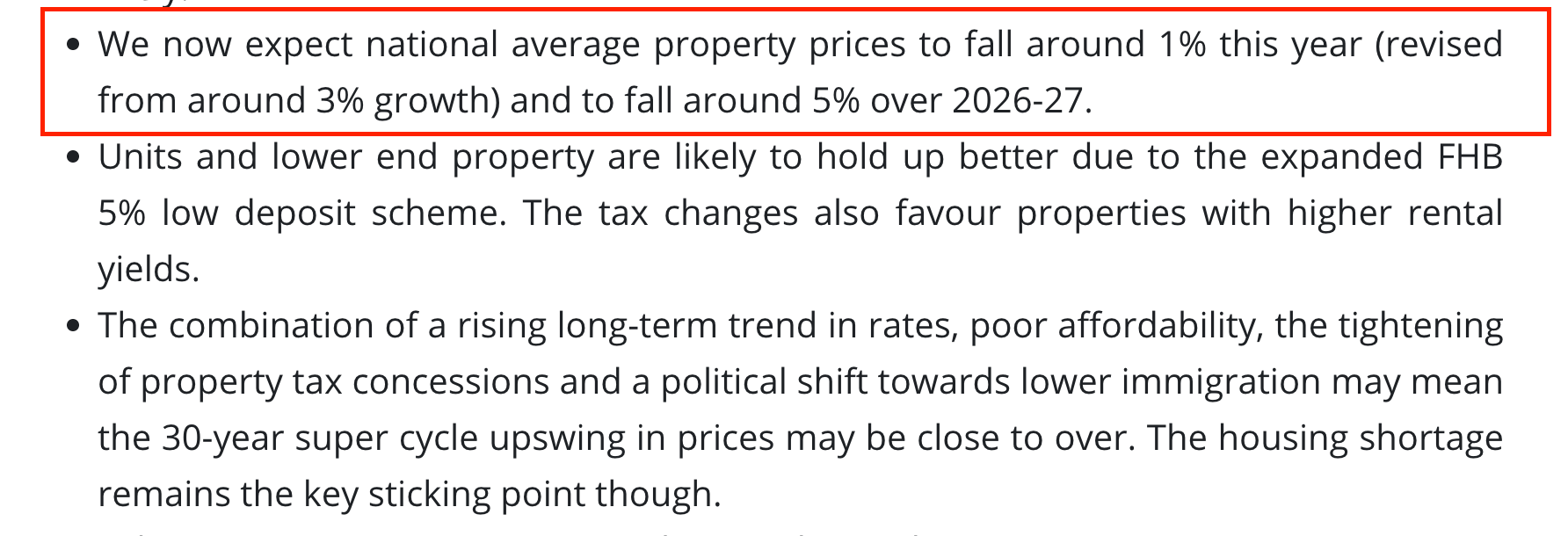

He’s forecasting a 1% drop in 2026, and 5% down by the end of 2027. That’s 5%, not 20%. On a million-dollar property, you’re looking at $50,000 off the top. Now for context, CBA and NAB are still forecasting 5% to 6% growth this year. Westpac recently revised down to flat. The gap between these forecasters is nearly 7%, and nobody knows who’s got it right.

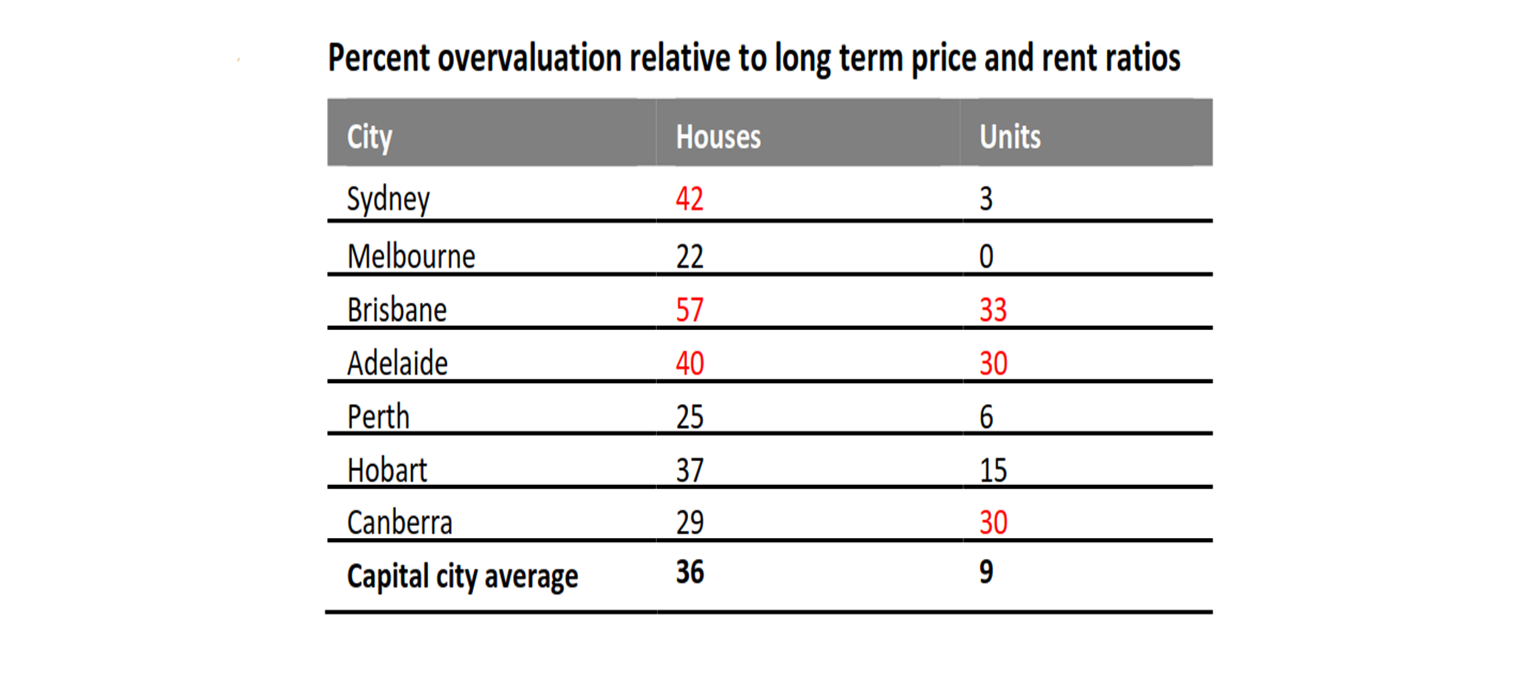

Oliver also looked at valuations by calculating price-to-rent ratios across every city and property type, sort of like a PE ratio for property. Houses are overvalued by 36% on average, apartments only 9%. Brisbane, Sydney, and Adelaide houses are the most exposed.

But think about it this way. That 36% comes from comparing today’s ratio against the long-run average. If Australia’s housing shortfall is baked into the structure of the market, then what counts as “normal” has been permanently pushed higher. If supply keeps falling short of demand, “36% overvalued” might just be the new baseline. That’s my take.

Oliver flagged something most people missed. Before the May 12 Budget, prices were still ticking up. All of the decline came after the Budget dropped. That tells you something: this wasn’t the natural cycle doing its thing, it was a policy shock that knocked confidence sideways.

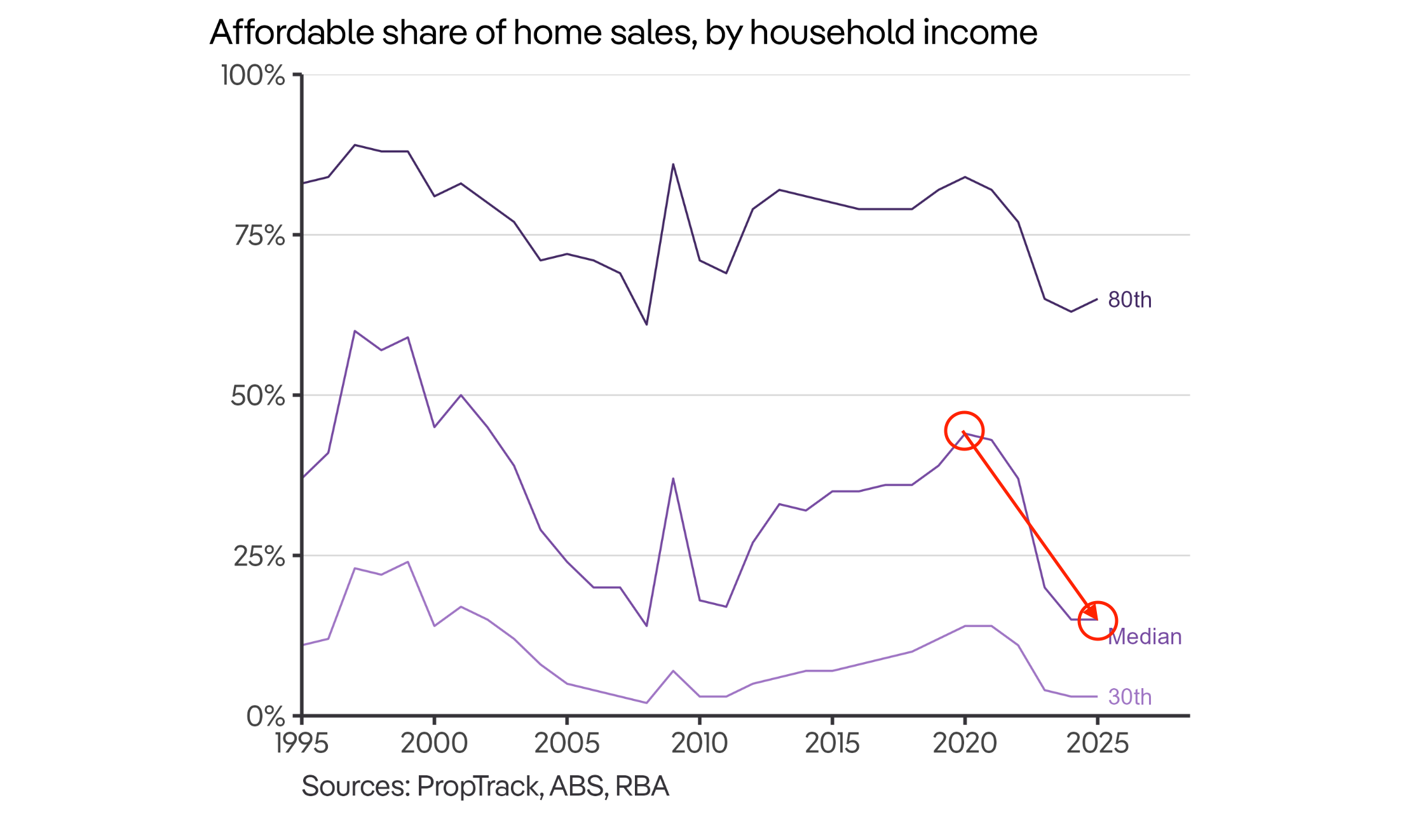

Only 14% of middle-income families can now afford a median-priced home. Three years ago it was 43%. How is the market still standing? The answer is parents chipping in with deposits, plus the 5% deposit scheme. But here’s the catch: bringing the deposit down doesn’t mean you can afford the property, it just means you’re carrying more debt.

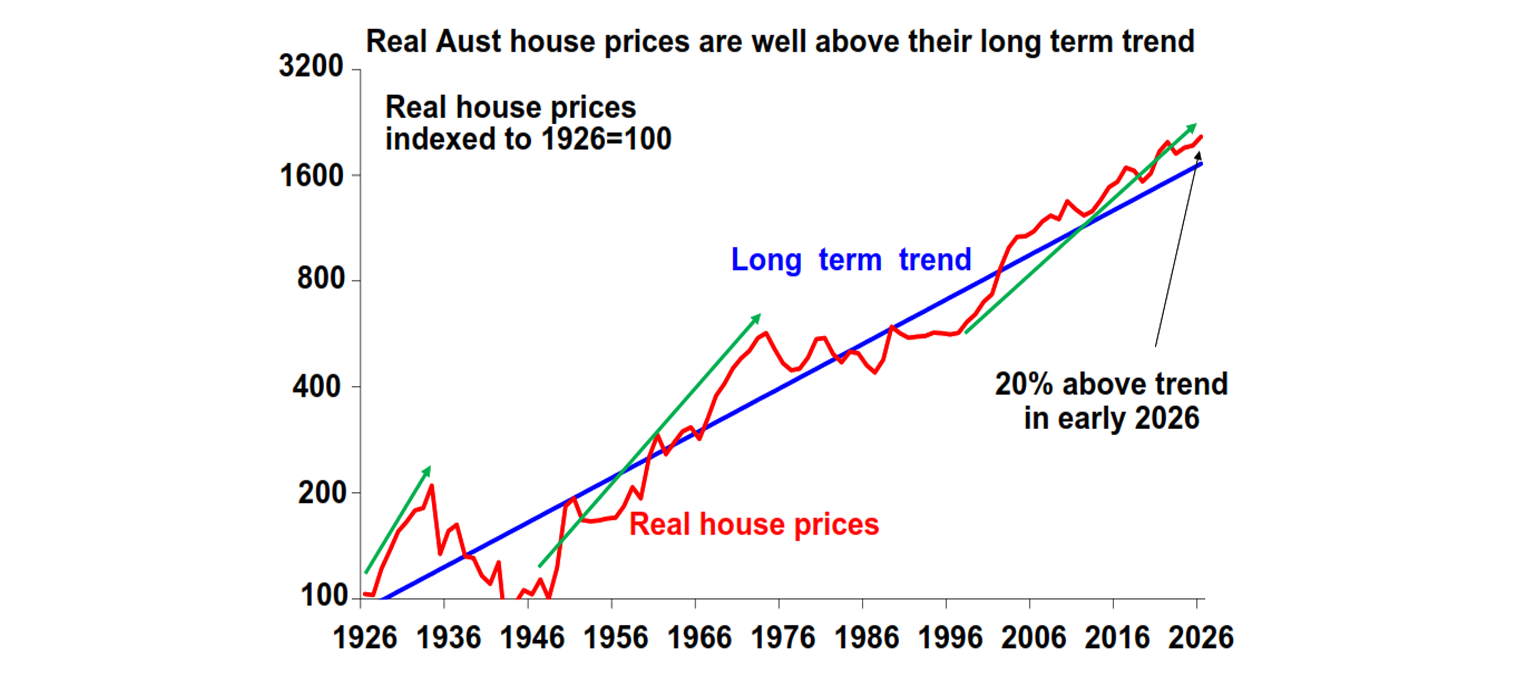

Oliver calls it a perfect storm. But there’s a huge gap between a perfect storm and the end of the world. And his analysis doesn’t stop at today’s numbers. He goes all the way back 100 years. Over the past century, only three super bull markets have played out, and every single one ended in a way that caught people off guard. This hundred-year chart is, in my opinion, the most important part of the whole report.

Three Times in 100 Years

Oliver charted 100 years of real house prices, with inflation stripped out, against the long-term trend. This chart has lived through the Depression, two world wars, 17% rates, the GFC, and COVID.

Over that century, real prices grew at roughly 3% a year, about in line with GDP. But the growth wasn’t smooth. Strong decades were followed by flat or falling ones. Oliver picked out three super bull markets.

The first was in the 1920s. The post-war economy boomed, and then the Depression crushed prices for close to 20%. The lesson is clear: when an outside shock lands on top of structural weakness, the fall runs deeper and lasts longer than anyone can think of.

The second ran from the 1950s to the early 1970s, and this one matters most for where we are now. Post-war migration and the baby boom pushed real prices from 50% below trend to 50% above. Then the 1970s brought stagflation, population growth slowed, and rates shot up to 17%.

Now here’s what most people get wrong about this. The bull market didn’t end with a crash. Prices just drifted sideways for over 20 years. Your house might have ticked up two or three percent a year on paper, but strip out inflation and the real return was close to zero. For example, buy a place for a million in 2026, and by 2046 it might be “worth” $1.5 million. That looks like a 50% gain. But with 3% annual inflation, that $1.5 million buys roughly what a million buys today. Your paper wealth goes up, but your real wealth stays flat.

Why didn’t it crash? Because Australians will do almost anything to hold onto their homes. Unless mass unemployment forces people to sell, nominal prices are extremely hard to break. But inflation, that slow and invisible erosion, is the one thing you can barely defend against.

If the third super bull market ends the same way, the old “buy and sit on it” strategy won’t cut it anymore. You’d need to lean on cash flow and smart property selection to earn real returns. And here’s the thing: it was exactly that 20-year flat stretch after the second cycle that set up the launch pad for the third one.

The third kicked off in the mid-1990s and pushed prices about 20% above trend. This is the 30 years you and I have lived through. What powered it? Oliver broke it down into five engines.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

The Five Engines

Engine one: interest rates. Over 30 years, mortgage rates fell from 17% down to around 2-3%. Every time they came down, buyers could borrow a bit more. Oliver says this engine has stalled. The RBA sits at 4.35% with three increases this year, and not one of the big four banks is calling for a cut. Westpac says rates could climb to 4.85%.

Engine two: lending standards. After decades of loose lending, the rules are being tightened up. Banks are cracking down on fake applications, and loans are getting harder to push through.

Engine three: dual-income households. ABS data shows the female participation rate sitting at 62.8%, a historic high. Dual income is already the standard, and there’s no extra fuel left in this tank.

Now, stalling and slowing are different things. The first three have stalled completely. The next one is still running, just losing speed.

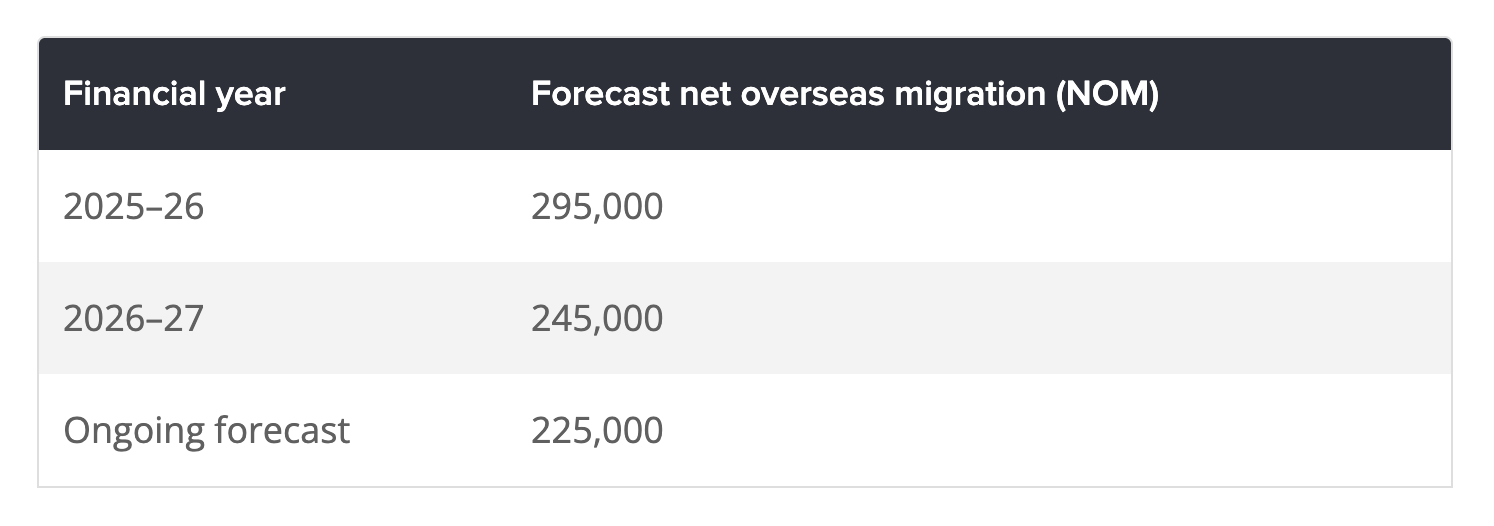

Engine four: immigration. Net Overseas Migration peaked at 538,000 in 2022-23. The government wants it down to 225,000, the Coalition put forward 165,000, and the Budget locked in 245,000 for 2026-27 dropping to 225,000 after that. That’s a 55% cut from the peak, and both major parties are falling over each other to prove who can cut harder.

But even at 225,000, the housing shortfall hangs around 200,000 to 300,000 dwellings. Australia only builds about 180,000 homes a year. NHSAC estimates the Housing Accord target will come up about 260,000 short. Immigration is slowing down, but we're still not building fast enough to close the gap. Demand is still running ahead of supply, and that's exactly why Oliver pulled back from calling the super cycle dead.

Engine five: the 1999 CGT reform combined with negative gearing. Oliver says the current government has weakened this one. And this is the engine that nearly everyone is misreading. That misunderstanding could be costing a lot of people an opportunity they don’t even know is sitting right in front of them.

The Part Nobody Quoted

So now you’ve seen all five engines and where they stand. After laying them out, Oliver wrote something near the end that the media never reported: “Caution is needed in calling an end to the super cycle.” He admitted that five years ago, he thought the cycle was done, but the migration surge and lack of housing supply gave it another run.

Then he put down what I believe is the most important line in the whole report: “Until the housing supply shortfall is better addressed, it is premature to declare the super cycle over.”

That one sentence gives you a test. The super cycle lives or dies based on the supply gap. Not interest rates, not buyer confidence, not the tax changes, but whether we can actually build enough homes. And right now, at the current pace, that gap won’t close over the next few years. If anything, it could get wider.

I’m not saying property prices can’t come down. They absolutely can, and in some markets they already are. But I am saying that calling the end of a 30-year structural cycle requires the supply problem to be fixed first, and the data tells us we’re nowhere close.

Oliver also listed four things to keep your eye on: rate direction, the Strait of Hormuz, unemployment, and investor demand. His bottom line is this: if unemployment doesn’t spike hard, crash predictions are almost certainly wrong. You need mass forced selling for a real crash, and as long as the job market holds, Australians will eat instant noodles before they hand over the keys.

Negative Gearing Was Not Abolished

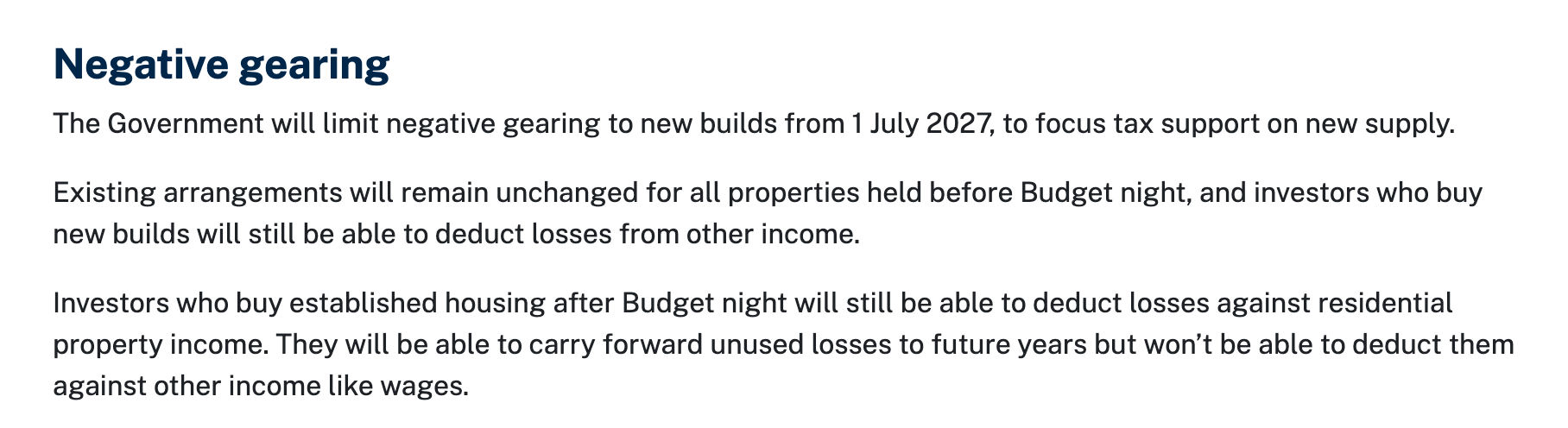

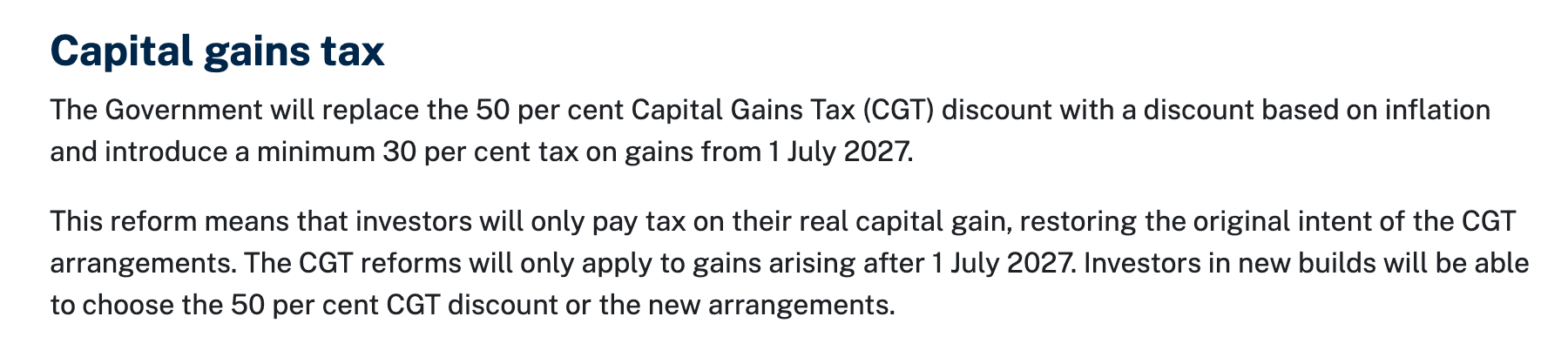

Now let me clear something up, because almost everyone has the tax reform wrong. Negative gearing was not abolished, it was restricted. From 1 July 2027, for second-hand investment properties bought after 12 May related property capital gains, not your salary. Anything you held before 12 May stays fully protected under grandfathering.

The CGT discount wasn’t killed off either, it was swapped. The old 50% discount is gone, replaced by inflation-adjusted cost base calculations with a minimum 30% tax rate. In some cases, especially long holds with high inflation, the new system could work out better. Talk to your accountant. This applies to individually held properties only, and companies, trusts, and SMSFs play by different rules.

The legislation hasn’t fully passed either. It’s through the House of Representatives but still in the Senate, with a window for amendments before 22 June.

And here’s the part that changes everything: brand-new properties are completely unaffected. New builds, including house and land packages, keep negative gearing and the option for the 50% CGT discount.

Look, the government’s tax lever is pushing capital out of second-hand stock and into new construction, boosting supply. That’s the exact same variable Oliver identified as the key to the super cycle. The logic lines up from both directions.

Once rental losses can’t offset your salary, a second-hand investment has to stand on its own financially. The old playbook of buying a low-yield second-hand place and subsidising it through tax breaks is done. Oliver himself pointed out that the reforms “favour existing properties with high rental yields,” and they obviously favour new builds too. So stop asking whether you can still invest in property. The smarter question is: which type should you invest in under the new rules?

The Rules Have Changed

So when you put it all together, the direction is clear. New house and land packages tick every box: tax advantage, supply contribution, and strong returns. That’s where the policy is pointing.

Sydney and Melbourne are going through an adjustment. Perth is still pushing up. Every city sits at a different point in its cycle, and you need to look at each one individually, not as one national market.

Already hold investment properties? They’re protected under the Budget, and those are now irreplaceable “tax scarce assets.” Hold the strong ones, use refinancing to sort out cash flow. But if something hasn’t moved in ten years and the cash flow is about to crack, let it go and rotate into something more efficient.

For timing, Oliver gave the roadmap: watch RBA minutes for rate direction, the Strait of Hormuz for oil prices, ABS data for employment, and clearance rates for demand. Base decisions on leading indicators, not gut feel.

I’m not saying you can time the bottom perfectly. Nobody can. What matters is whether you’re picking the right type of property, in the right city, at the right point in the cycle. Under the old rules, you just needed guts. Under the new rules, you need precision.

Oliver’s report is worth your time, but don’t let it send you into a panic. The forces driving prices have weakened, but until the supply gap is fixed, the super cycle can’t be called dead. The probability of a crash is close to zero.

For 30 years, being brave enough to jump in was all you needed. Going forward, the way you make money has changed. You need to know what you’re buying, where, and at what point in the cycle. The days of buying blind and coming out ahead are behind us. But for people who learn the new rules and do the work, there’s a door opening right now. You don’t just need vision anymore, you need a calculator and an investment strategist working with you.

If you’ve watched today’s video and want to figure out what this means for you, book a free 30-minute Discovery Session. There’s no cost and no pitch. We’ll help you see where you stand and what comes next. The link is in the description.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs