31.6% Premium and House & Land STILL Wins! Buyer Agents’ Tricks Exposed | APS162

Last episode, our team put four full days into a complete investment model. Thirty-two dimensions, four price brackets, three holding periods, all stacked up against each other, house and land versus established, looking at after-tax net returns under the new tax rules. The result: in most scenarios, for most investors, house and land packages come out ahead.

I knew this was going to go against everything buyer’s agents have been telling people for years. “Rule number one: never buy new.” “Depreciation gets clawed back when you sell.” “Buy a cheap $500,000 established house, sit on it for three to five years, and flip it.” You’ve heard all of it, especially on social media, where everyone with a camera claims to be a property expert.

I waited six days before recording this follow-up. I wanted to see what came back in the comments and whether any buyer’s agents would put out a video to go after my numbers. Not one serious buyer’s agency came back with any quantitative research. Same old playbook: feelings-based marketing, cherry-picked examples dressed up as proof.

The wave of hostile comments I was expecting didn’t really show up either. That makes sense. When you put modelling and data on the table, there’s not a lot left to argue with. But there were some genuinely thoughtful replies that helped round out my analysis. So today, I’m going through the best comments, dealing with a few hostile ones, and giving you a condensed version of brand-new research. The question: how much more can you pay for house and land over established and still break even on net returns?

I’m pulling out the most representative comments and going through them one by one, because some are genuinely good questions, some are based on common misunderstandings, and some are just smears.

This first one is the most technical comment of the lot. The commenter raised two fair points.

Point one: “You compared 32 dimensions by count, not by weight. That’s a serious flaw.” I get what you’re saying. Capital growth should carry more weight than tenant preference, so counting “20 wins, 8 losses, 4 draws” doesn’t prove anything. But that comparison was just step one, a broad look at the full picture. The real answer came from the quantitative model in the second half of my video: after-tax net returns, cash flow, time value of money, Monte Carlo simulation. That model doesn’t need weights because every factor that can be put into numbers was already baked into the final result. And here’s the thing: the dimensions you can’t put a number on, like tenant preference, contract complexity, statutory warranties, if you try to force a weight onto those, the weight itself is subjective. So I put everything measurable into the model and let the numbers do the talking. If you think those should count in favour of established homes, go ahead. The win rate for house and land only goes up.

Point two: “A 300-square-metre block should grow slower than a 600-square-metre block.” You assumed established homes on 600 square metres grow 2% faster per year, 5% versus 3%. Where’s the evidence? I went through everything publicly available from the RBA, ABS, Productivity Commission, Cotality, HIA, PropTrack, and SQM. Not one independent study has ever compared growth rates for house and land versus established, head to head. The numbers floating around, “new builds 3 to 5% capital growth per year, established 6 to 8%,” all come from buyer’s agent marketing reports. They take one cherry-picked example, use it to stand in for a national average, and the whole thing is put together by people with a direct financial interest in proving established is better.

Now here’s what happens when you run the model with the same growth rate for both. Established loses every single time. Once growth is equal, tax, depreciation, stamp duty, maintenance, time value, all of it turns into pure upside for house and land. My analysis shows established needs to grow roughly 2% more per year just to break even with house and land. On a five-year hold, they need 3% more. Ten years, 2%. Twenty years, 1.2%. And under the new tax rules, investor money is going to shift from established to house and land, so the chance of those old exceptions showing up again drops a lot.

This next comment had a lot of likes: “Disappointed to see Alex pushing house and land after the tax changes.” Let’s stick to the facts. I don’t “push” anything. If you were a VISION Gold Member, you’d know that. We look at each member’s situation, build a plan that fits, lay out the numbers, and the member decides.

This is an interesting one. “The number one rule of property investment is never buy new.” Is that a law of nature? If you’re talking about apartments off-the-plan, you’re right about 80% of the time. But apartments in Brisbane and Perth shot up over the past four years. Nobody brings that up.

Someone else wrote: “You’re a buyer’s agent too.” Fair question. Part of my business does involve buyer’s agency work, but the logic behind it is completely different. I go where the facts lead, not where the money is. If I find something that goes against my own business interests, I put it out on this channel first, because that’s what the data shows, and then I adjust. Most other agents are stuck in one lane, telling you their product is the best, no matter what the numbers say. I run a membership model. The moment I take a membership fee, my job is to look after my members’ interests, not my own.

Now this one’s a sharp question: “House and land packages have builder collapse risk, right?” Yes, they do. Builder insolvency, DA delays, construction delays. I covered this in dimension 18 of the 32-dimension analysis, and I scored it as a win for established homes.

But here’s the thing: do you think established homes don’t have risk? The risk just shows up differently. You buy a 30-year-old house, and you might be dealing with structural cracks, asbestos, lead pipes, old wiring, and termite damage, none of which you can see before settlement. And established homes come with no statutory warranty. Your Building and Pest report says “all clear,” you move in, and the roof leaks. That inspection is a visual check only, and there’s no shortage of inspectors who rush through the job.

For house and land, that’s exactly why VISION Gold Membership exists: to screen the right land, the right builders, and bring risk down as far as we can. Over five years, not a single builder our members bought through has gone under. Land settlement delays run at about 3%. Construction delays at about 2%. DA changes at about 2%. Established homes, on the other hand, have a much higher chance of hitting you with post-purchase surprises that no due diligence could have caught.

This last comment is pure defamation, accusing me of taking fees from developers and builders while also charging buyer’s agency fees. Zero evidence. Under Australian defamation law, that carries real consequences. A preliminary discovery application means Google hands over your data to the court. If you’ve got evidence, put it out there. If you don’t, stop.

So with those comments out of the way, let’s get to the main part. House and Land Premium Analysis.

Want to know exactly where you stand and what your next property move should be? Book a VISION Blueprint Session — in 45 minutes, you'll walk away with a personalised Property Investment Blueprint built around your numbers, your goals, and your timeline. And if you want ongoing support from a team that handles everything from strategy to settlement, VISION Gold Membership is your next step. Link in the description below.

House and Land Premium Analysis

Our research over the past few days led to several breakthroughs, and every single one of them goes against what buyer’s agents have been claiming. I’ll put these out one by one as the responses come in. What I’m about to walk you through is the condensed version of our house and land premium study. The full version goes to VISION Gold Members and Masterclass students.

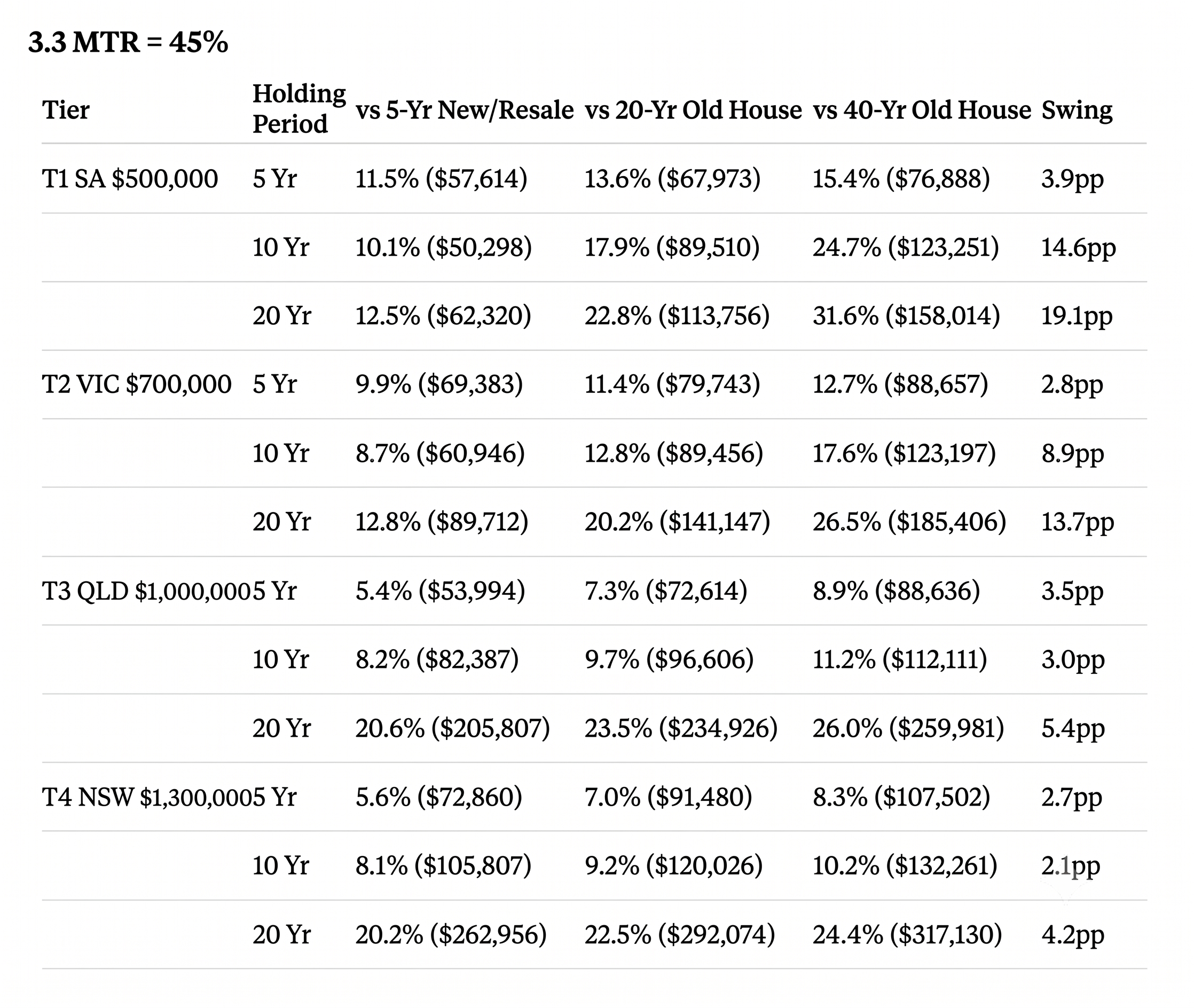

Most assumptions carry over from last episode, so go back and watch that if you haven’t. I split the analysis into four price tiers: under $600,000, $600,000 to $800,000, $800,000 to $1.2 million, and above $1.2 million. I picked one representative price for each: Tier 1 at $500,000, Tier 2 at $700,000, Tier 3 at $1 million, Tier 4 at $1.3 million. Three comparison scenarios: same area house and land versus a 5-year-old established house, neighbouring suburb versus a 20-year-old house, and different suburb in the same economic region versus a 40-year-old house. Then 5, 10, and 20-year holding periods at different marginal tax rates, comparing after-tax net returns.

Let me go straight to the results.

Against a 5-year-old established house, the break-even premium, that’s how much more you can pay for house and land and still come out even, sits between 4.7% and 8.9% on a 5-year hold. On a 10-year hold, it’s 6.8% to 8.1%, and it goes as high as 20% if you hold for 20 years. The longer you hold, the bigger the premium that house and land can carry.

Against a 20-year-old house, that premium gets noticeably bigger across all three holding periods.

And against a 40-year-old house, the gap really widens. The allowable premium ranges from 7.6% all the way to 24.4%. The $500,000 tier is the most striking: the premium there can run from 12.7% to 23.2%, the widest range of any price bracket.

Now let’s look at it from the other direction, by marginal tax rate. At 30%, the floor is 4.2% and the ceiling is 19.3%. At 45%, the floor goes up to 5.4%, and the ceiling hits 31.6%.

Key Takeaways

The pattern is clear. No matter the established house age, 5, 20, or 40 years. No matter the price tier, $500,000 to $1.3 million. No matter the marginal tax rate, 30%, 37%, or 45%. No matter the holding period, 5, 10, or 20 years. House and land can carry at least a 4.2% purchase premium and still break even. At the top end, that reaches 31.6%.

If you’re a lower-bracket investor buying in the $500,000 to $800,000 range, the biggest edge house and land gives you isn’t tax. It’s maintenance savings, modelled from 20 years of ATO data plus state government records, including major repair bills spread across each year.

If you’re a higher tax bracket investor buying above $800,000, maintenance savings still count, but what really puts house and land ahead is the tax structure: stamp duty on the land component only, negative gearing putting real cash back into your account every year, and the option to pick between old and new CGT methods when you sell. But if you’re on a 45% marginal rate and you insist on buying a cheaper, older, established home, you’re getting neither the tax benefit nor the maintenance savings. Your net return ends up the worst of any investor in any scenario.

So here’s your practical guide: house and land can carry roughly an 11% to 15% premium over established and still be the better pick. If your tax rate is higher, your holding period is longer, the established home is older, or the price is lower, all of those push the allowable premium up. The ceiling is 31.6%.

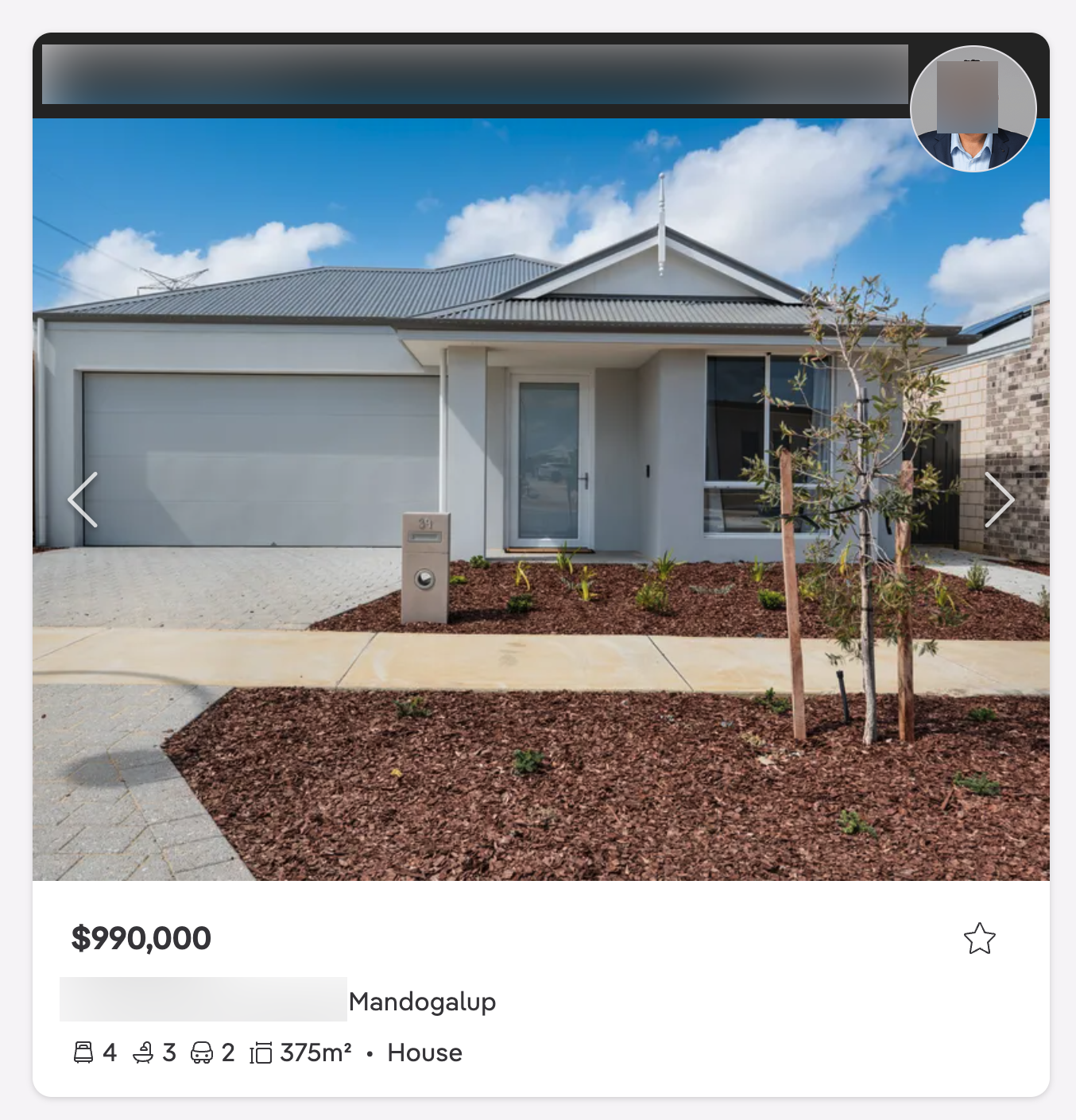

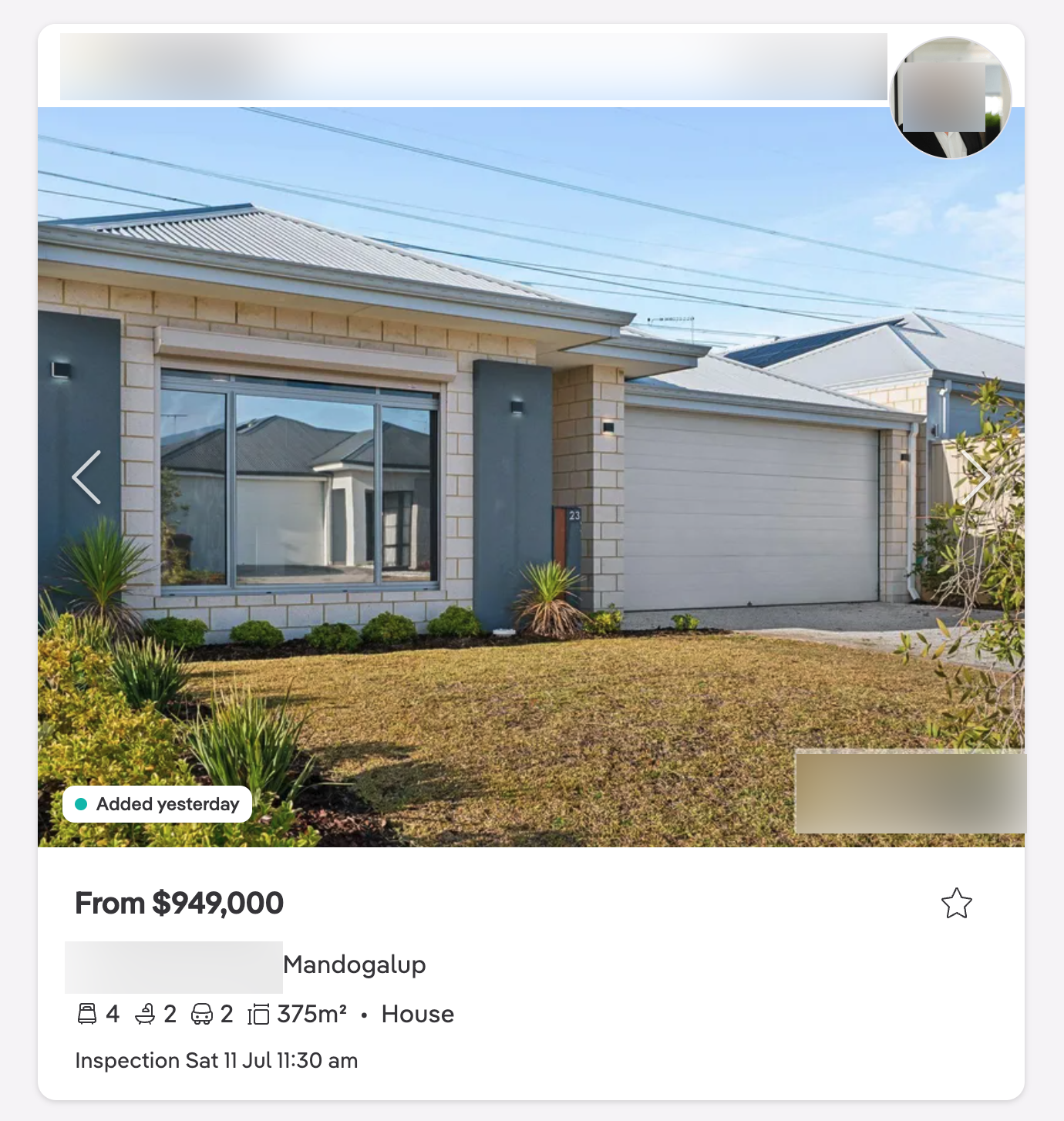

Everything above assumes there is a premium. But are there deals with no premium at all? Absolutely. And buyer’s agents will never tell you about these. Last month, we helped a member buy in Perth: 375 square metres of land, four bedrooms, for $977,000. Comparable established homes nearby were going for between $950,000 and $990,000. Where’s the premium?

Just because you can’t find a deal without a premium doesn’t mean they don’t exist, and it doesn’t mean I can’t find them. Even with a 15% premium on that Perth example, the contract price comes to $1.13 million, and as long as your tax rate is reasonably higher and you hold long enough, you still come out ahead.

Here’s what I want you to take away from all of this. Think independently. Look at the evidence.

Watch the video version of the blog on YouTube.

15 Minutes Free Consultation (Limited-Time Free Offer)

If you have any questions about Australian real estate, we invite you to use our 15 Minutes Free Consultation service. Once you have filled in the form, a professional property investment strategist will be in touch with you. They will assess your needs and provide fundamental advice. This service is designed to help answer general property-related queries. BOOK NOW.

VISION Membership

Our Flagship Service: VISION Membership. Your One-Stop Property Investment Manager – Build a Tailored Portfolio and Achieve Financial Freedom

Whether you're an employee, a professional, a business owner or even a new migrant, everyone has a financial goal for the future. The VISION Membership is designed to solve all the pain points in your Australian property investment journey through one single, comprehensive service.

By analysing your current financial situation and long-term goals, we'll tailor a property investment plan just for you. Our team will match you with the ideal mortgage structure, tax strategies, wealth planning, and legal support, empowering you to go further, faster, and smarter on your path to financial freedom.

VISION Membership is perfect for busy individuals who want a professional team to create, expand and manage their Australian investment portfolio. If you're looking for a dedicated team, including real estate investment experts, mortgage brokers, accountants, financial planners, and property solicitors, VISION Membership is your ideal solution.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

VISION Buyer’s Agent

No time for inspections? Tired of dealing with pushy selling agents? Unsure how much to offer or feeling nervous about auctions? Worried about buying the wrong property? If any of these sound like you, AusPropertyStrategy's Australia-wide VISION Buyer's Agent Service is here to help.

We provide end-to-end support to help you build an optimised property portfolio and achieve your financial goals—whether you're investing interstate, refinancing, or planning post-settlement leasing or resale. Our services cover everything from suburb research and property selection, to price negotiation, auction bidding, and post-settlement support.

Start with an obligation-free 30-minute discovery session on Zoom. BOOK NOW.

real estate australia,real estate investing,australian property,australian housing market,australian economy,australian property investment,australian property market,buying property,australian real estate,mortgage brokers brisbane,first home buyer,Australian Real Estate,Australian Real Estate Investment,Australian Property Investment,Real Estate Investment,Property Investment,Property Investment Australia,Passive Income,Positive Cash Flow,Australia Real Estate Investing,Australian Real Estate Investors,Australian Property Investors,Vision Wealth Mentors,Vision Real Estate Investors Australia,financial freedom, freedom through property investment,real estate investors,property investment,passive income,positive cash flow,real estate course,real estate courses,real estate training,australian property market,property investment brisbane,property investment sydney,melbourne property market,investing in brisbane,investing in melbourne,how to invest in property,buying properties,start investing in property,property investment strategy,how to buy investment property,property investing tips,best suburbs to invest in sydney,locations real estate,prime location,property growth by suburb,capital growth suburbs