Your Money Is Not Safe: Australia’s Tax Overhaul Might Devastate Investors [APS089]

Have you ever thought about this: after working hard for an entire year, half of your income might end up in the hands of the Australian government? Australia’s tax system is on the verge of undergoing the biggest transformation in decades. And this change won’t just affect your tax returns—it could directly impact your property investments, your superannuation, and every single dollar in your pocket. Many people assume that since personal income tax rates haven’t changed this year, life might stay relatively stable. But what they don’t know is that the government has already prepared a whole new set of policies. Even more alarming is what’s about to happen in August: the Economic Reform Roundtable in Canberra. Don’t underestimate this meeting. It could mark a major turning point for Australia’s entire tax structure and property market over the next ten years. For example, the GST rate might jump straight to 12.5%, and even everyday essentials that were once GST-free could now be taxed. In real estate, long-standing policies like negative gearing and capital gains tax discounts are also likely to face drastic overhauls at this meeting. So here’s the real question: Will these reforms actually benefit you in any meaningful way? Or is this just another excuse for the government to reach deeper into your wallet? And more importantly, what can you do right now to prepare to protect your assets, and secure your investment returns? In this video, I’m going to walk you through the most up-to-date, comprehensive, and practical analysis. By the end, you might just start rethinking every investment you currently hold.

I studied accounting at the University of Sydney. After graduation, I worked in the field for a while—but honestly, I didn’t like it. I felt like I was dealing with numbers all day long, and it was just too dry and boring. So I switched careers and entered the real estate industry. It wasn’t until I bought my first investment property that I truly started diving into tax research—because it saved me a lot of money. Now, I actually enjoy studying taxation. The types of taxes, how they’re collected—they're all directly tied to your investment returns. If the government takes more, investors make less. It’s that simple. To help our VISION members maximise their investment returns, we keep a close eye on all tax changes—both at the federal and state/territory levels—and helps members prepare in advance. Take the Division 296 superannuation tax as an example. We’ve already helped our members restructure their investment portfolios to avoid it completely.

In this video, we’ll only talk about federal-level taxes—the national ones. We won’t go into the various state-level taxes like land tax, land tax surcharges, stamp duty, or first home buyer grants. Those are extremely complex, and every state or territory has its own rules and calculations. If you're interested in that part, please leave a comment below, and I’ll do a separate video on it.

Personal Income Tax

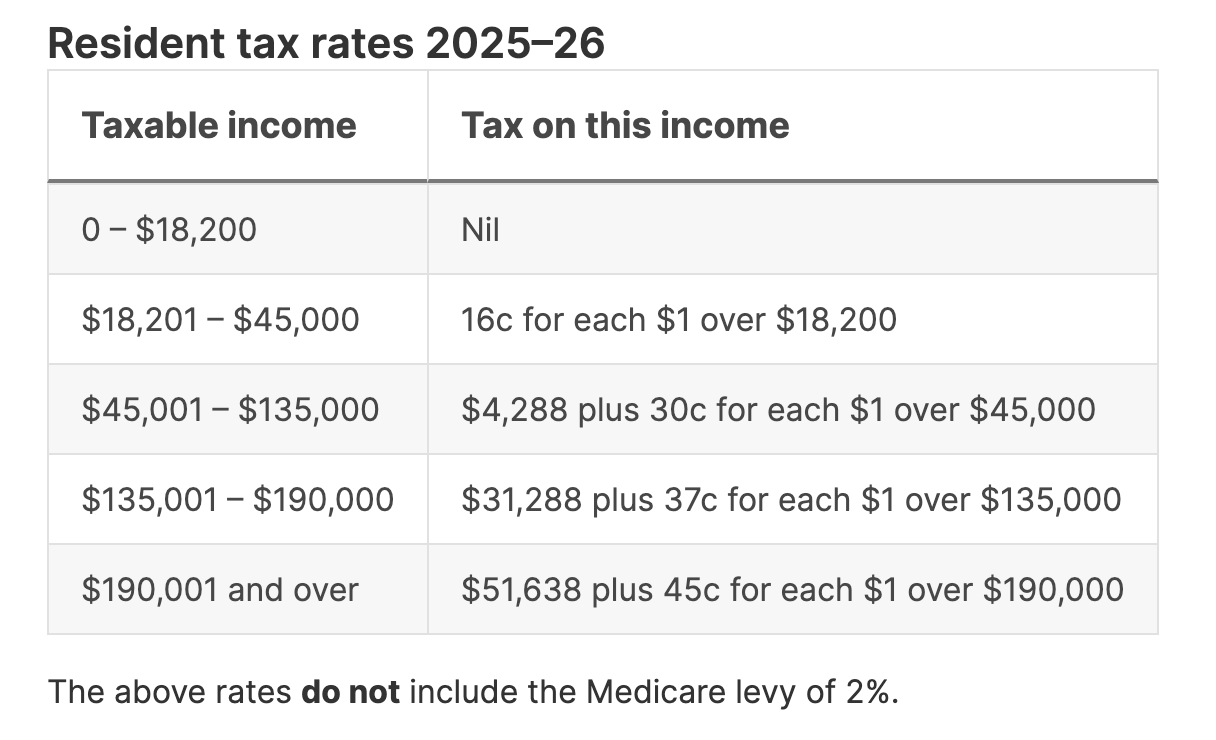

Let’s start with personal income tax. For the 2025–26 financial year, the tax brackets and rates remain exactly the same as in 2024–25. Income under $18,200 is tax-free. Between $18,200 and $45,000, the tax rate is 16%. A common tax strategy is still valid—like using a family trust to hold your assets or business, and distributing profits to beneficiaries in your family who don’t have other income. This still works. The rules haven’t changed, and a 16% rate is quite low. From $45,000 to $135,000, the tax rate is 30%. This is the same as the corporate tax rate. For companies that pay only 25%, it’s slightly higher—but the difference is minimal. So in this income bracket, whether you keep profits in your company or distribute them to yourself doesn’t really make a big difference.

Then we move into the higher tax brackets: $135,000 to $190,000 is taxed at 37%. Above $190,000 is taxed at 45%. If you’re in one of these two brackets—congratulations, you’re doing well financially! But you’re also paying a lot in tax, which means you must learn how to reduce your tax burden. For salary earners, there really aren’t that many tax deduction methods besides using negative gearing when you invest in property.

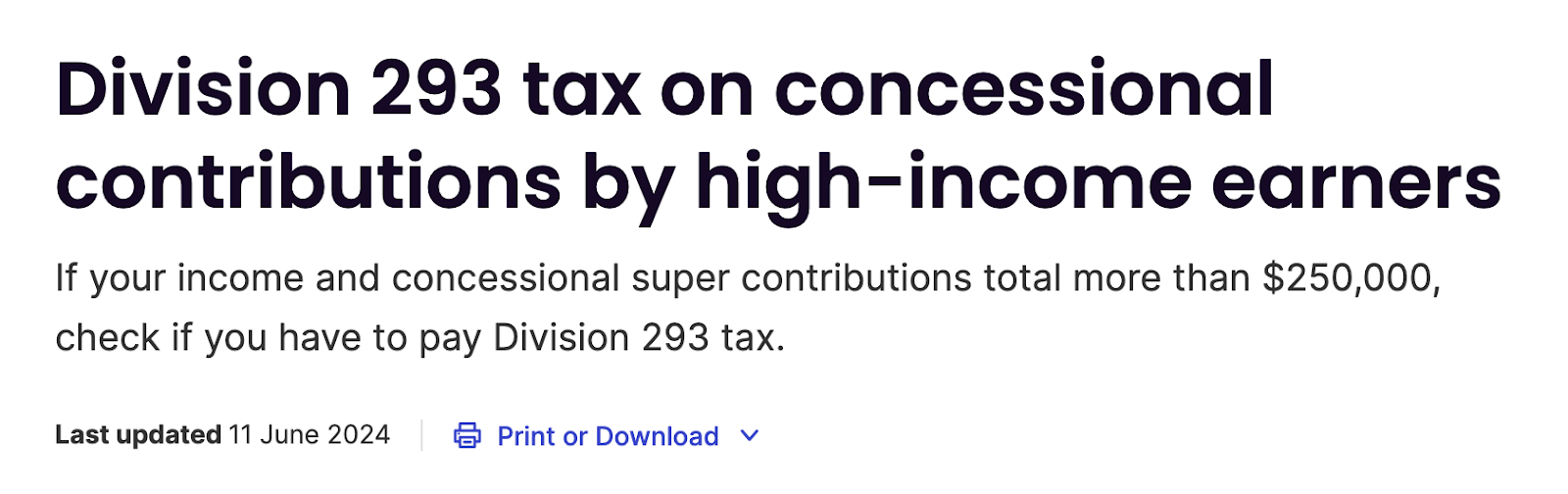

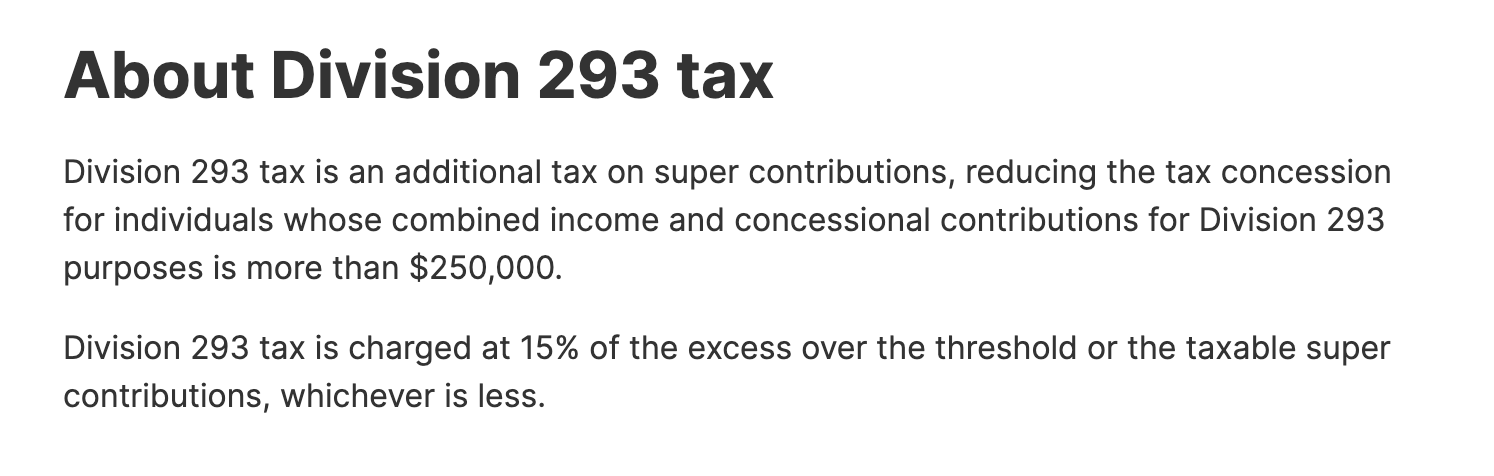

If your income exceeds $220,000, you’ll also need to be careful about a special tax for high income earners called Division 293. Here’s how it works: if your pre-tax income plus superannuation contributions exceed $250,000, the excess is taxed an extra 15%. There are some extra rules but knowing the extra 15% is more than enough for now. This tax is incredibly annoying. No accounting software currently calculates it automatically—it needs to be done manually by your accountant. Often, people don’t even know they owe this tax until the ATO sends them a bill. And by then, it’s too late to make adjustments to your reported income. That’s why it’s so important to have a good accountant.

From what I’ve seen, many accountants don’t offer any tax planning advice. I once asked them why—and the most common answer I got was: “As accountants, we represent the public interest. We’re not supposed to help clients pay less tax if that means the federal government collects less.” Honestly, I think it’s either because they weren’t paid enough to care, or they just don’t have the knowledge. If your accountant falls into that category, take my advice: dump them now. Don’t even look back. You need an accountant who’s proactive, who’s willing to advise you on legal ways to reduce your taxes.

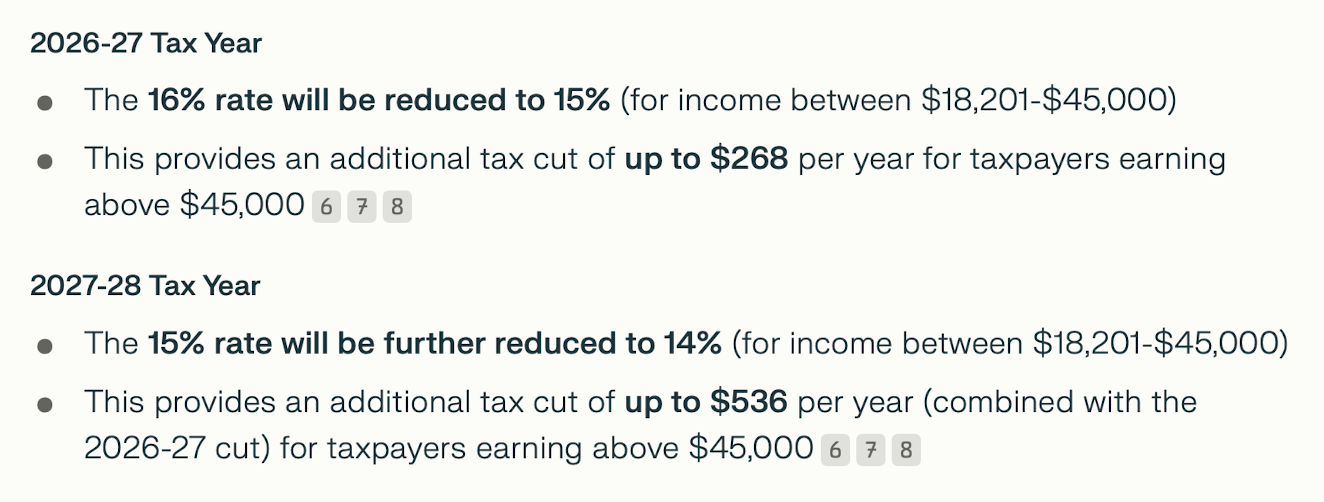

Even though income tax hasn’t changed for this financial year, starting next year, the 16% bracket will be lowered to 15%, and the year after that, down to 14%. You might save around $300 to $500, give or take. But honestly, waiting around for tax cuts from the government isn’t as practical as learning how to manage deductions and structure your finances wisely. That’s what really makes a difference.

Foreign Resident Capital Gains Withholding Tax (FRCGW)

Starting in 2025, the Foreign Resident Capital Gains Withholding Tax will increase from 12.5% to 15%. And now, it applies to all property sales, regardless of the sale price. Previously, if the sale price was under $750,000, it was exempt. But that exemption has now been completely scrapped.

Now don’t confuse “foreign resident” with “foreign citizen.” Whether you hold an Australian passport or have permanent residency doesn't matter here. A "non-tax resident" refers specifically to someone who is not paying tax in Australia. The ATO has a separate set of criteria for determining this, which is different from how residency is judged in areas like immigration, student visas, or stamp duty surcharges.

Let me give you a quick example: A non-tax resident sells a property for $1 million. At settlement, the buyer is supposed to transfer funds into their solicitor’s trust account, which then pays the bank and the seller. But under the new rule, the buyer’s solicitor must first withhold $150,000 and send it to the ATO. Only after that can the rest go to the seller and the bank. Why? Because the government is worried the seller might take all the money, leave Australia, and never pay capital gains tax.

There’s a simpler way to look at this: Anyone—whether an Australian or a foreigner—who sells a property in Australia, needs to apply for a Clearance Certificate from the ATO. If you get the certificate, it means you’re a tax resident, and the withholding tax doesn’t apply. But if you can’t get it, then the ATO will treat you as a non-resident, and you’ll be required to pay the 15% withholding tax. At the end of the financial year, you can then lodge your return and claim a refund or pay any shortfall.

Now, you might ask: “What if my property didn’t go up in value?” “What if I actually lost money?” “What if I’m in debt and can’t afford to lose 15% upfront while I wait for a refund?” In these cases, you can apply to the ATO for a Variation Notice. If approved, it allows you to pay less withholding tax upfront. How much less? Well, it depends on your cost base, meaning the total cost of purchasing and selling the property. This needs to be assessed case by case.

Superannuation Contributions

With the new financial year starting, this is good news for most employees. Employer superannuation contributions have increased from 11.5% to 12%. This marks the final step in the super reform plan that began in 2021. Will it increase again in the future? Possibly—but as of now, there are no official plans. If you earn $150,000 a year, that’s an extra $750 into your super. It might not look like much now, but over time—especially with compound interest—this could turn into a significant boost to your retirement savings after 40 years.

From the employee’s perspective, this is great. But for employers, it’s another added cost. From what I’ve observed, more and more employers are shifting from “base salary + super” packages to “total salary package”, meaning your salary and super are bundled together into a fixed total. There’s one thing I never quite understood: If an employee’s productivity hasn’t gone up, why are we increasing their wages? Of course, as an employee, everyone wants a raise. But when employers don’t want to pay more, the government steps in—raising minimum wages and mandatory super contributions. Maybe that’s one reason why Australia’s productivity has remained so weak.

Think about this: What it costs to hire one Australian employee, you could hire three people in China, or roughly the same in Malaysia. So for any job that can be done remotely, companies are naturally going to look overseas first. And some big companies—like the banks—employ entire teams of local IT staff who barely do any real work.This “high-pay, low-output” culture is especially common in large corporations, particularly in the banking sector. If you had an employee who spent their 8-hour day eating snacks, chatting, and constantly going to the bathroom—wouldn’t you fire them? But in many big Aussie companies, they don’t. Why? Because there’s not enough competition. If people were at constant risk of losing their jobs, you’d see a lot more getting done. But in Australia, the Labor government and the unions would step in right away. So I honestly don’t expect productivity to improve in this country anytime soon.

There’s one more major change to super: If your super balance exceeds $3 million, you’ll now be hit with an extra 15% tax—and that includes unrealised capital gains. If you want a full breakdown of this rule, check out [APS081].

All of the tax changes I’ve just talked about are either already in effect, or almost guaranteed to happen. But starting next month, the Australian federal government is entering a full-blown tax reform era. Some tax systems that have been in place for decades may be completely overhauled—and every single change will have a direct impact on the wealth and investment returns of Australians across the board.

Economic Reform Roundtable

When it comes to tax reform in Australia this year, the biggest story—is the Economic Reform Roundtable. You can think of it as a high-level summit hosted by the Australian Treasury, set to take place from August 19 to 21 in the Parliament House in Canberra.

Everyone attending the event is personally invited by the Treasury, and the plan is to have 25 key participants. As of the time we're recording this video, 11 of them have already been confirmed, including the Minister for Productivity, the Liberal Party's Shadow Treasurer, several prominent business leaders and union representatives.

According to the official narrative, the goal of this roundtable is to boost productivity, strengthen Australia's resilience to global uncertainty, and make sure the federal budget is sustainable. In simple terms: How can we produce more while losing less money in government spending?

But what hasn't been publicly emphasised is that most of the agenda is actually focused on one thing: reforming the federal tax system. And this is where I want to sound a warning: Don't be fooled by the word "reform." When we hear the word "reform," most people assume it means changing things for the better. But in my view? The same action, if it leads to improvement, that's a reform. But if it doesn't? That's just a chaotic and costly disruption for the sake of looking busy. So let's go through the major tax reforms that have already been leaked to the public ahead of the meeting, and you decide for yourself—Is this a real reform, or just a costly mistake?

Goods and Services Tax (GST)

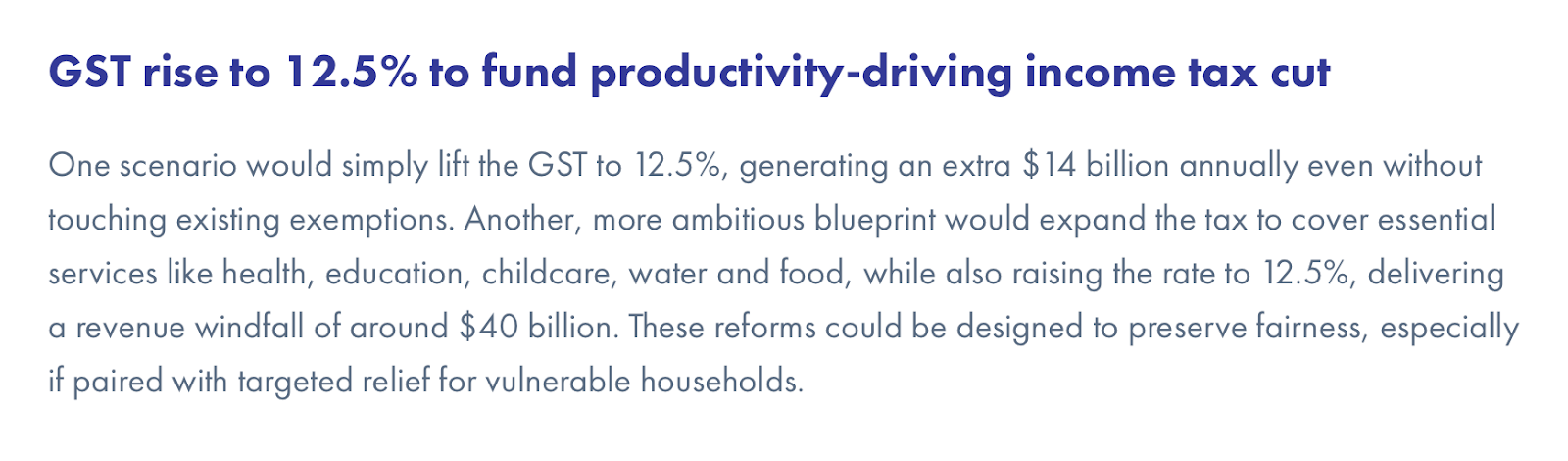

One of the core proposals on the table is this: Should Australia's GST rate be raised from 10% to 12.5%? And should items that are currently exempt from GST—such as water, milk, eggs, school tuition, gold and even the sale of small businesses—now be taxed as well?

Let's take a step back. GST was introduced on July 1, 2000, and has never been adjusted since then. With the exception of essential goods and health services, everything else in Australia has been subject to a 10% GST. Here's how it works: Each state and territory collects the GST, then passes it on to the federal government, which then redistributes it back to the states and territories. Some get more, others get less.

When GST was first rolled out, it had a massive impact on both society and the economy. For consumers, the logic was simple. Whether you're buying goods or services, you're suddenly paying 10% more out of nowhere. That means prices effectively jumped 10% across the board.

Unsurprisingly, this triggered a wave of inflation. Although the inflation eventually calmed down over the next few years, at the time, it was very real and very painful. For businesses, it wasn't just a matter of updating prices. They also had to upgrade their compliance systems, update their accounting practices, and spend a lot of money on admin and training. For regular people, buying the same items cost more, which means their purchasing power fell, and their standard of living dropped.

In response, the government introduced a series of measures to try and make sure people's real income didn't fall. These included significant income tax cuts, increased welfare payments, and the first-ever First Home Owner Grant, designed to help people get into the housing market. And what happened next? Well, we all know the story. Property prices in Australia entered a massive boom.

Property Investment–Related Taxes

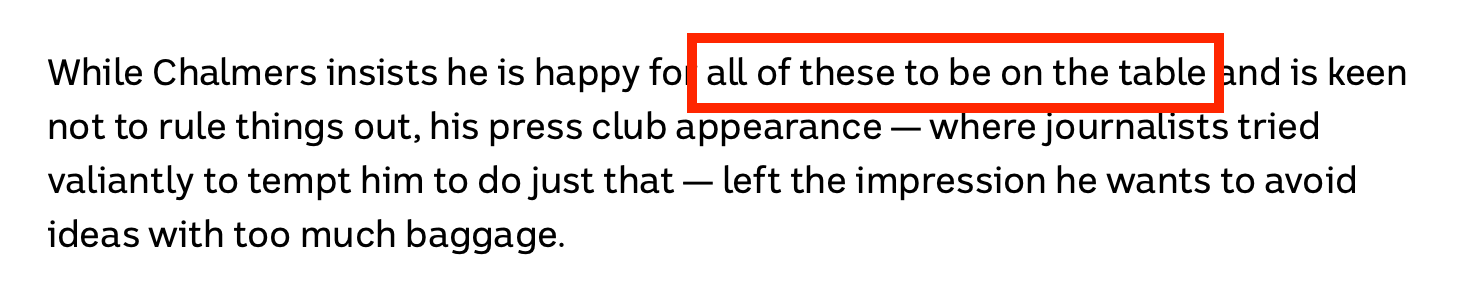

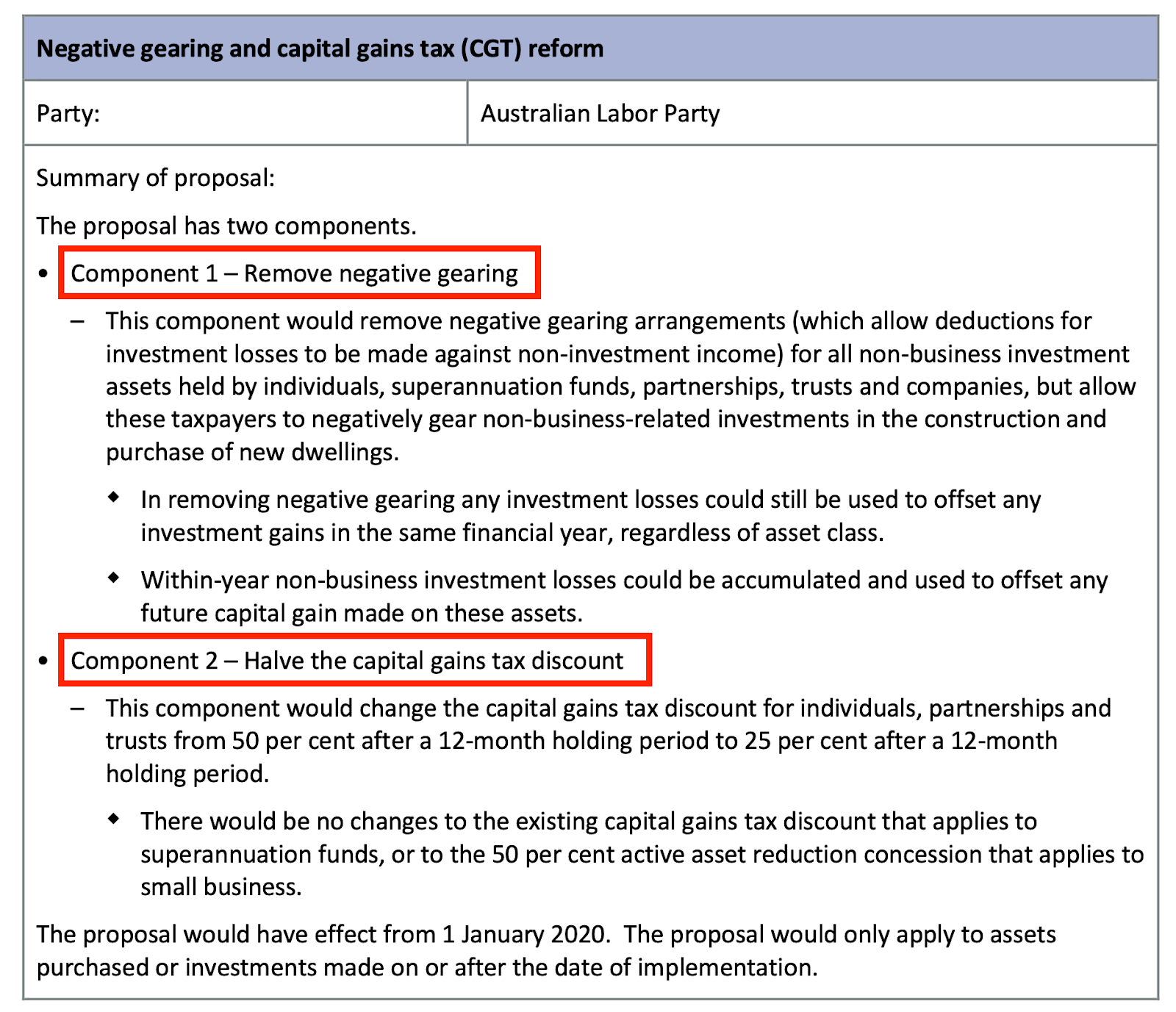

The one chairing the Economic Reform Roundtable is the current Federal Treasurer. And during an interview, he said: "Everything is up for discussion." Now, that is probably the scariest thing he could've said. What's the most lucrative industry in Australia for everyone? It has to be real estate. But here's the thing—many of the taxes related to property are state-level taxes, not federal. That includes stamp duty, stamp duty surcharges, land tax, land tax surcharges, and development-related levies. These are all controlled by the state and territory governments. The federal government can only touch two things: Negative gearing and Capital Gains Tax (CGT).

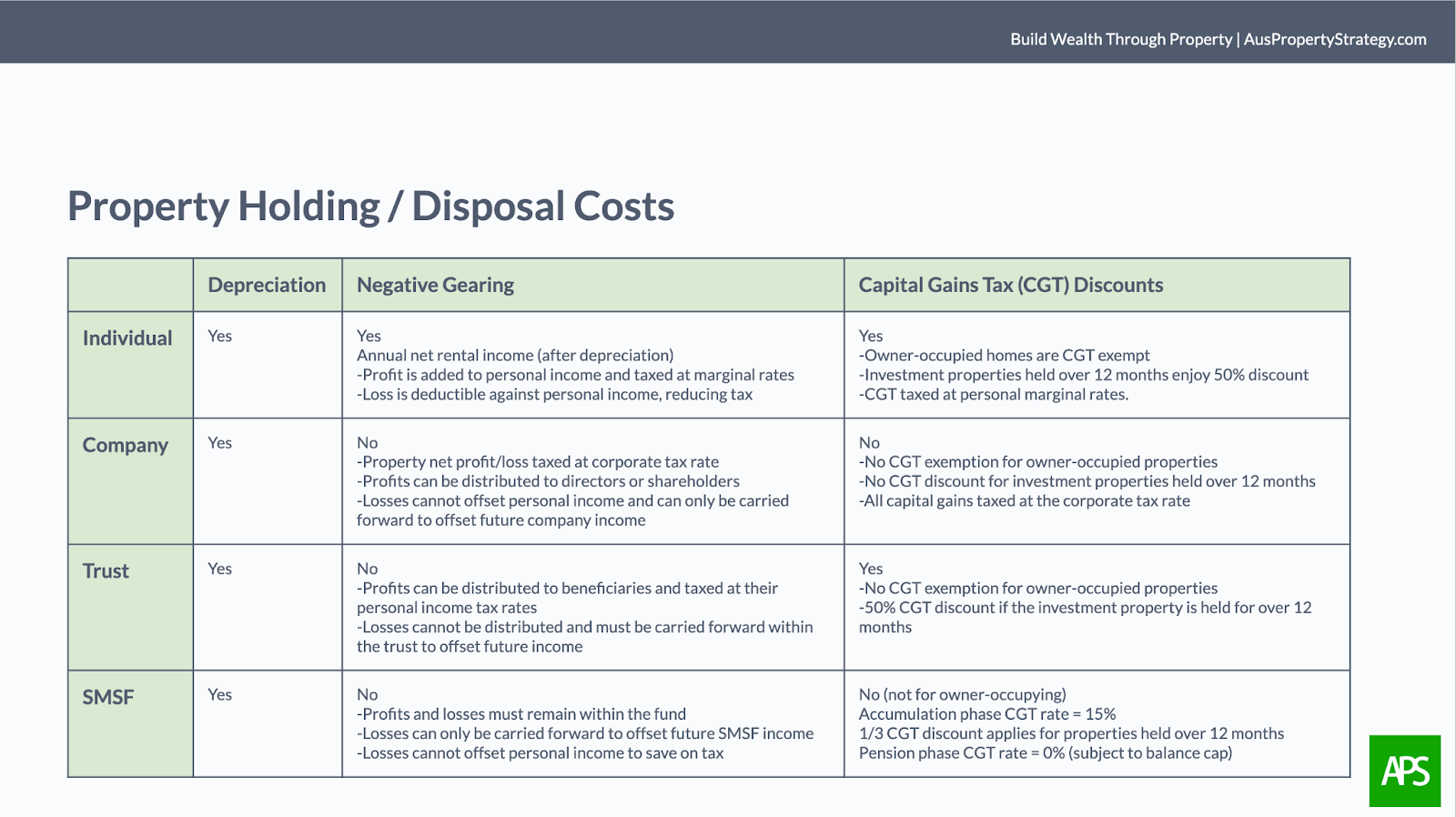

Negative gearing allows you to offset losses from investment properties held in your personal name against your taxable income, which reduces your income tax. This benefit only applies to individuals—not to companies, not to trusts, and not to SMSFs. CGT discounts, on the other hand, allow people who own properties under personal names, trusts, or SMSFs to pay reduced tax or no tax at all on profits made when the property is sold. These are all regulated by the federal government and collected by the ATO, so the federal government has full control.

If negative gearing is abolished, investor behaviour will dramatically change. Right now, high-income earners often buy brand-new properties to maximise depreciation, and the resulting paper losses help them reduce their taxable income. If negative gearing is removed, that tax strategy disappears—meaning high-income earners will end up paying more tax. And since new properties are often cashflow negative in the early years, the appeal of buying brand-new homes will drop. Right now, even if your property is cashflow negative, at least the tax benefits from negative gearing soften the blow. Without that buffer, investors will start chasing positively geared properties only—because if the cash flow is weak, the holding costs are painful and unsustainable. This policy shift could hit the detached house market the hardest.

Now, what if the 50% CGT discount for individuals holding property for more than 12 months is removed? Then, there's no tax benefit to holding a second-hand property in your personal name. It would be more tax-efficient to buy under a company, a trust, or an SMSF. This change would essentially raise the entry barrier for new investors, forcing them to structure their purchases through more complex entities. And if the CGT discount were to be scrapped across all ownership structures, personal, trust, company, or SMSF, then investors would have nowhere to hide. At that point, you'd really have to stop and ask yourself: "Is property investment even worth it anymore?" Without the 1/3 demand of property investors, there will be fewer properties on the market for rent or sale. And the price will go up a lot.

How likely is it that the government will touch negative gearing and CGT in this round of tax reform? Well, the Labor Party has always wanted to.

Back in the 2019 federal election, Labor's official campaign policy included both of these reforms. They lost. But in 2022 and 2025, they stopped mentioning them and even publicly promised not to revisit those ideas. They won. But promises are just promises; they are meant to be broken in politics. If the government holds power securely, it can change its stance at any time.

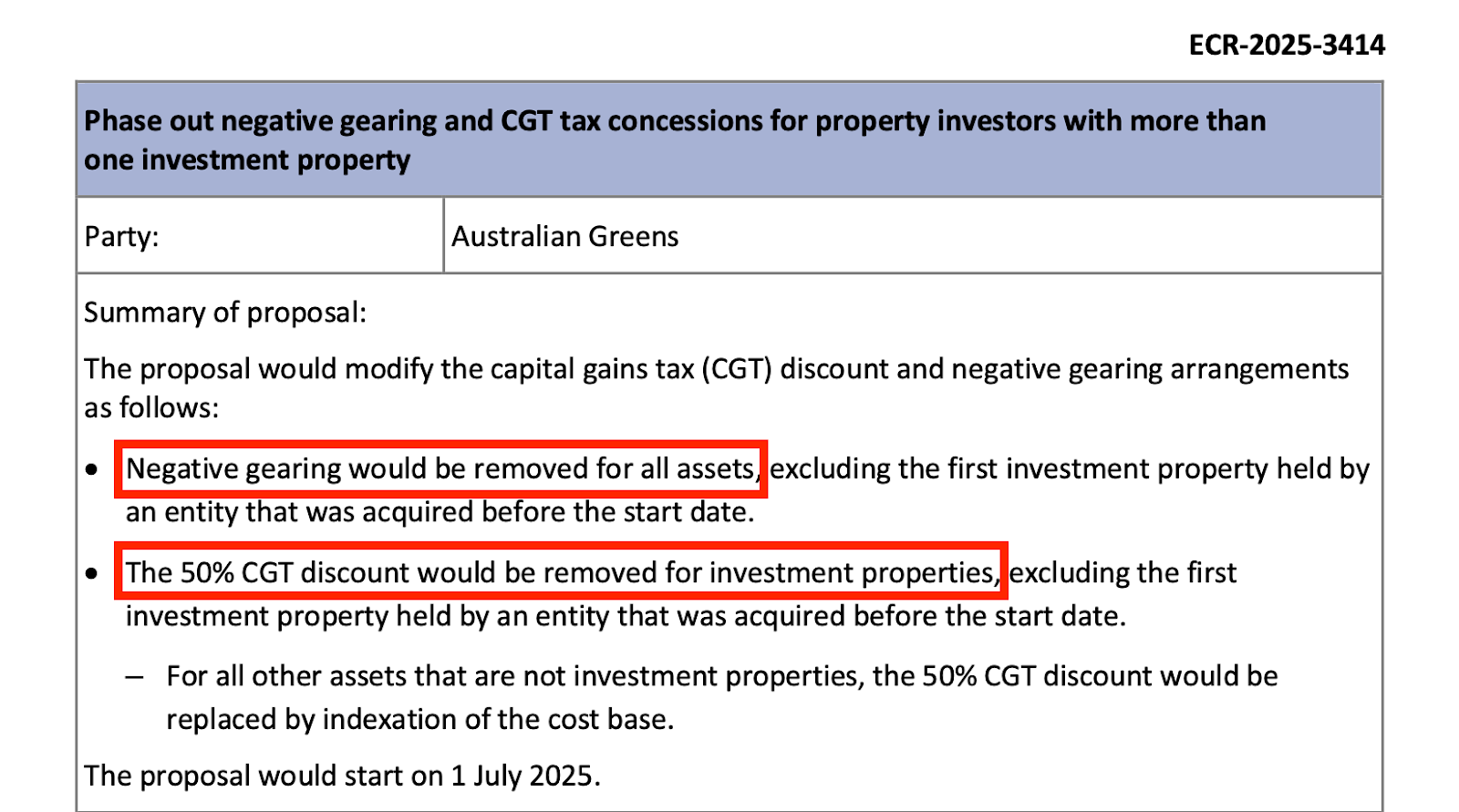

Is it likely they'll roll out all these changes at once? Almost zero chance. But will they implement them step by step over time? That's actually very possible. And let's not forget the Greens—Their tax reform agenda is even more aggressive than Labor's. They've proposed lowering the Division 296 super tax threshold from $3 million to $2 million and completely abolishing both negative gearing and the CGT discount. So, if you're a property investor and you're still supporting Labor or the Greens, you're basically betting against your own property portfolio. Now, to be fair, all of this is still under discussion. Nothing is final yet. We'll know more by the end of August when the roundtable wraps up.

Watch the video version of the blog on YouTube.