Why living in Australia has become impossible and how to break out of your current life [APS090]

Australia has long been seen as one of the top destinations for migration. It has a vast land with rich natural resources, a stable economy, and one of the highest average incomes in the world. From any angle, it seems like a dream destination. But over the past 20 years, something strange has been happening—more and more Australians are choosing to leave their own country and start a new life elsewhere. "Are Australians really unable to afford a home in their own country?" Unfortunately, the answer is yes—for many. Despite having a relatively high income by global standards, Australians face one of the most unaffordable housing markets in the world. Owning a home has become a distant dream, not a basic right. It's not just about housing. Living standards in Australia have been declining for years. Wages have stagnated while costs keep rising. And you're hit with endless taxes and levies. For many, Australia no longer feels like a land of opportunity—it feels like a financial trap. If you're already living in Australia, ask yourself this: Do you truly want to stay here long-term? Do you see a future with stability and growth—or endless struggle? This episode is about why the Australian dream is dead and how you need to rethink everything.

Australia's Housing Problem

Australia is the sixth largest country in the world. In terms of land size, it's about the same as the entire United States—minus Alaska. Yet the population is just 27 million, which is roughly the same as the city of Shanghai, China. Most of the people live in just five major cities, and two of them—Sydney and Melbourne—are home to 40% of the country's population. In the 2025 ranking of the world's top 10 least affordable housing markets, Hong Kong came in first, with median house prices 16.7 times the median income. Sydney was second at 13.8 times, and Melbourne ranked seventh at 9.7 times. But here's the shocking part—Brisbane, Adelaide, and Perth have now all overtaken Melbourne in house prices. That means all five of Australia's major cities have entered the global top ten for housing unaffordability. It's no longer just Sydney and Melbourne. It's the entire country.

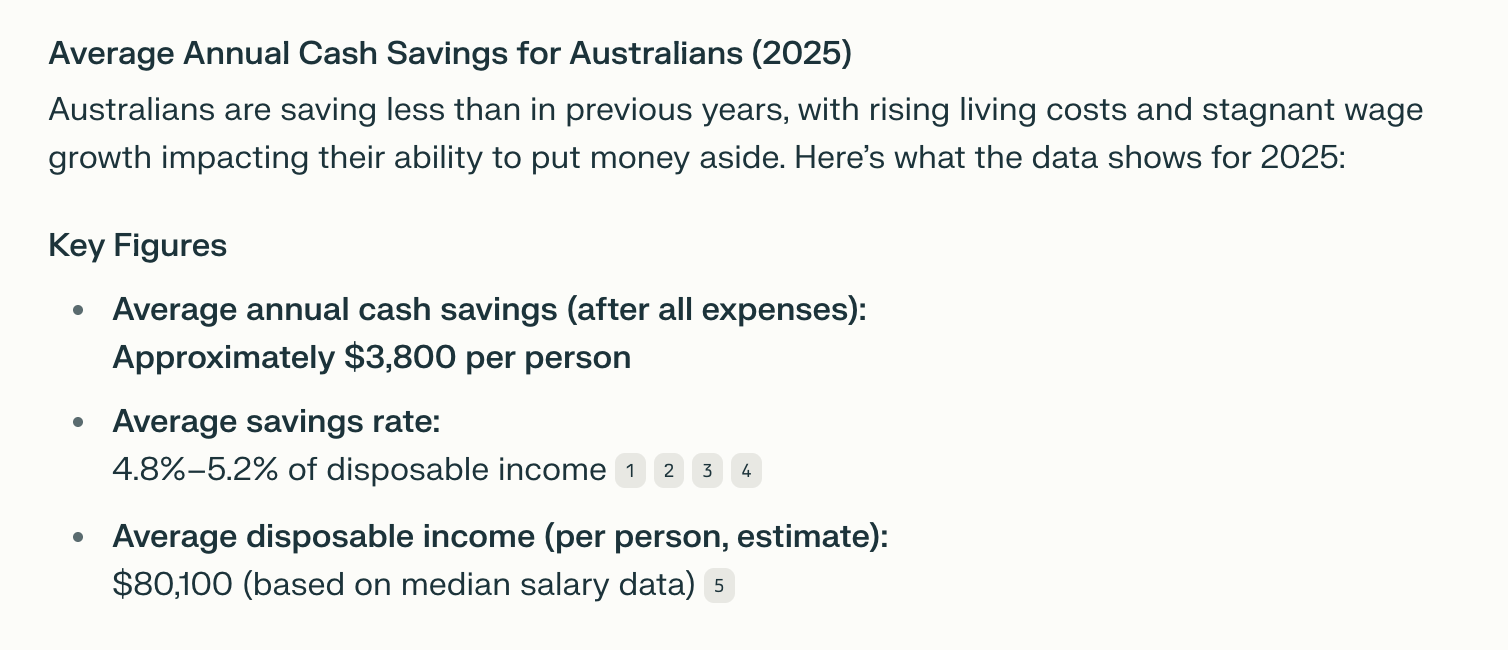

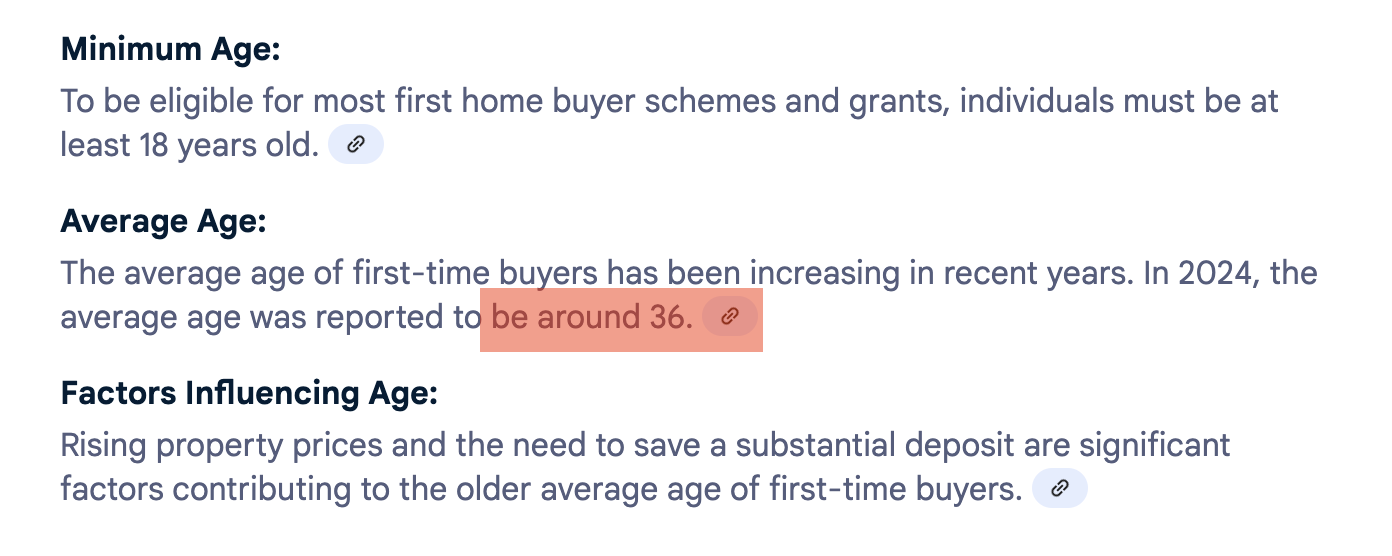

Based on Australia's average annual savings—about $3,800 per person—it would take 42 years to save up a 20% deposit for a standard $800,000 house. Even if a young couple worked and saved together, it would still take them 21 years. With help from parents on both sides, the burden can be eased somewhat. But still, the average age at which Australians are buying their first home has now been pushed back to 36 years old.

If buying a home is out of reach, can you just rent instead? Sadly, that's even harder. As more people give up on the dream of home ownership, rental demand is soaring. No matter what property you go to inspect, you'll find dozens of people lining up outside. This pressure on the demand side has sent rents skyrocketing to the point of being just as unaffordable as owning a home. For everyday Australians, the "Australian Dream" is slipping further and further away.

The housing crisis is not unique to Australia—much of the Western world is feeling the pressure. But what makes Australia different is how rapidly things have changed. Once upon a time, homes were affordable, and ownership was widespread. But that story is being rewritten.

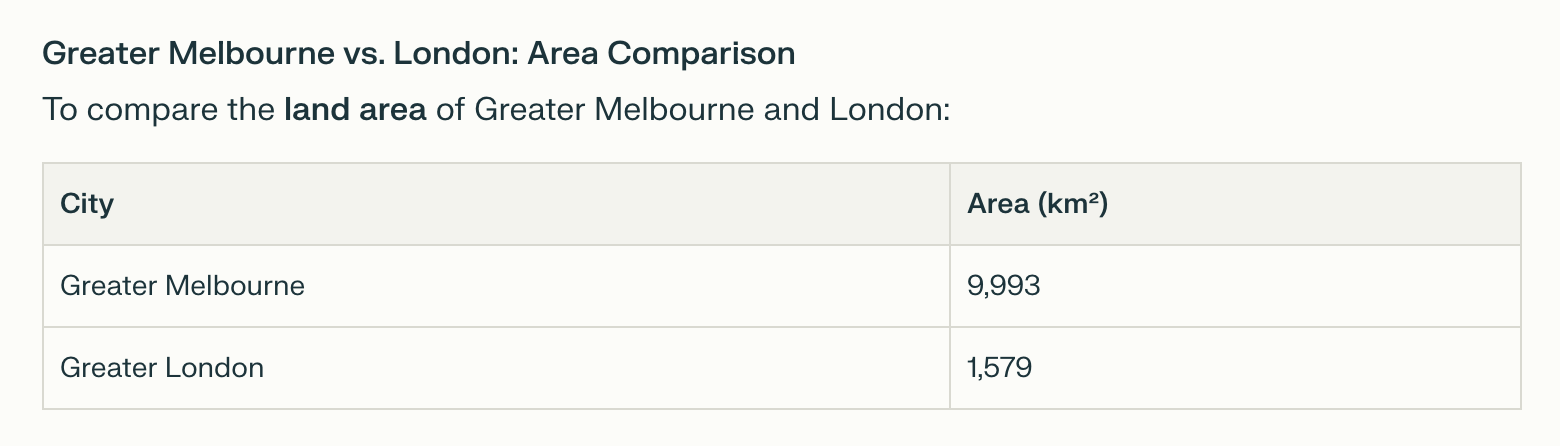

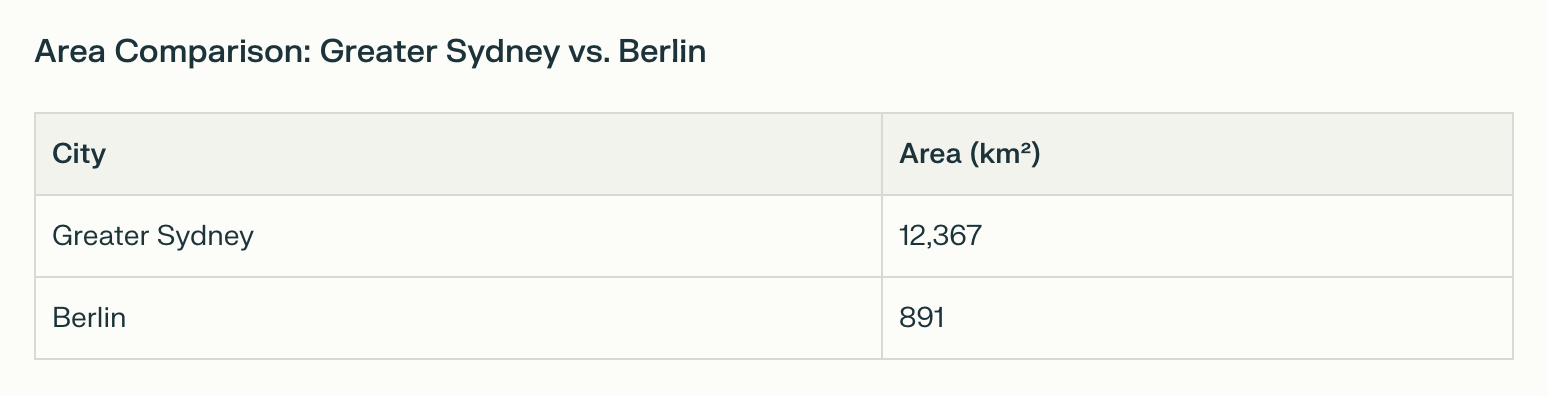

Back in the 1950s, Australia led the world in living standards. The economy was booming. And this was the era when the idea of the "Australian Dream" was born. To own a freestanding home on a 1,000-square-meter block of land, with a garden and a locally-made Holden car in the driveway. Mass car production made vehicles affordable for average people, so the focus turned to housing space. Cities began to sprawl outward. By 2025, Greater Melbourne is six times the size of London but has fewer people. Sydney is even more extreme—it's 14 times the size of Berlin.

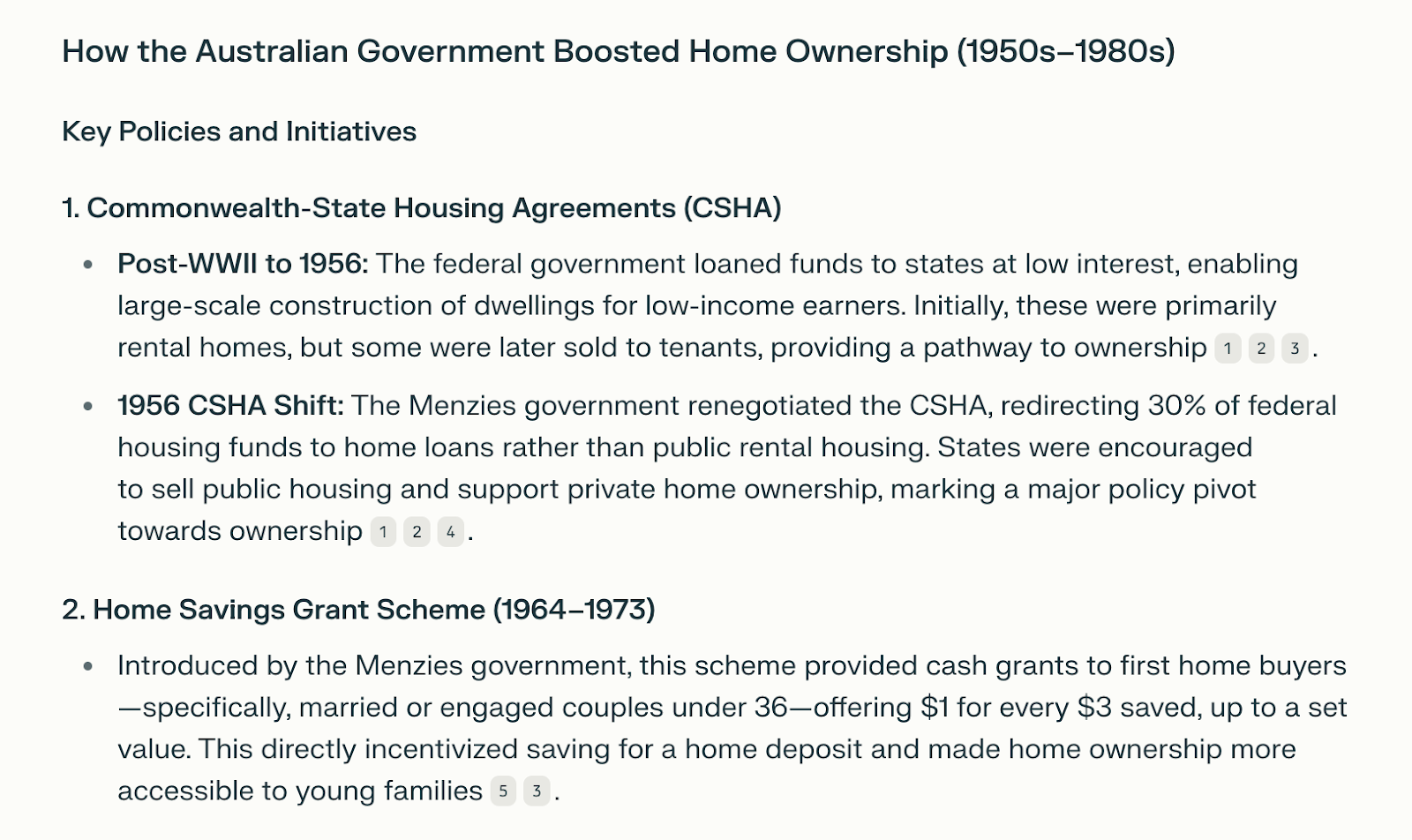

Between 1947 and 1966, the percentage of Australians who owned their homes rose from 52% to 73%—the highest among developed countries at the time.

Why did this happen? Because the government built homes directly, sold them on the market, and helped buyers with loans and subsidies. For example, between 1947 and 1956, the government built homes for low-income families and later sold them to tenants at low prices. The federal government supported home loans for individuals and encouraged state and territory governments to sell public and affordable housing on the open market. This helped increase homeownership dramatically.

The "Australian Dream" took root: owning a home means living a better, wealthier, and more stable life. And it wasn't just an idea—it was backed by public policy.

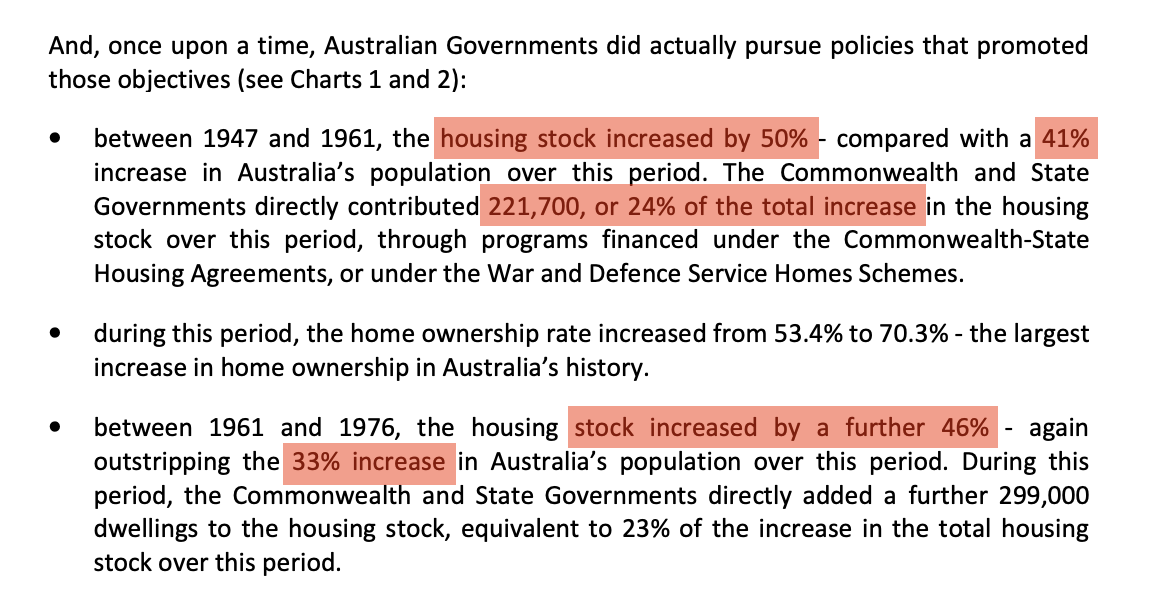

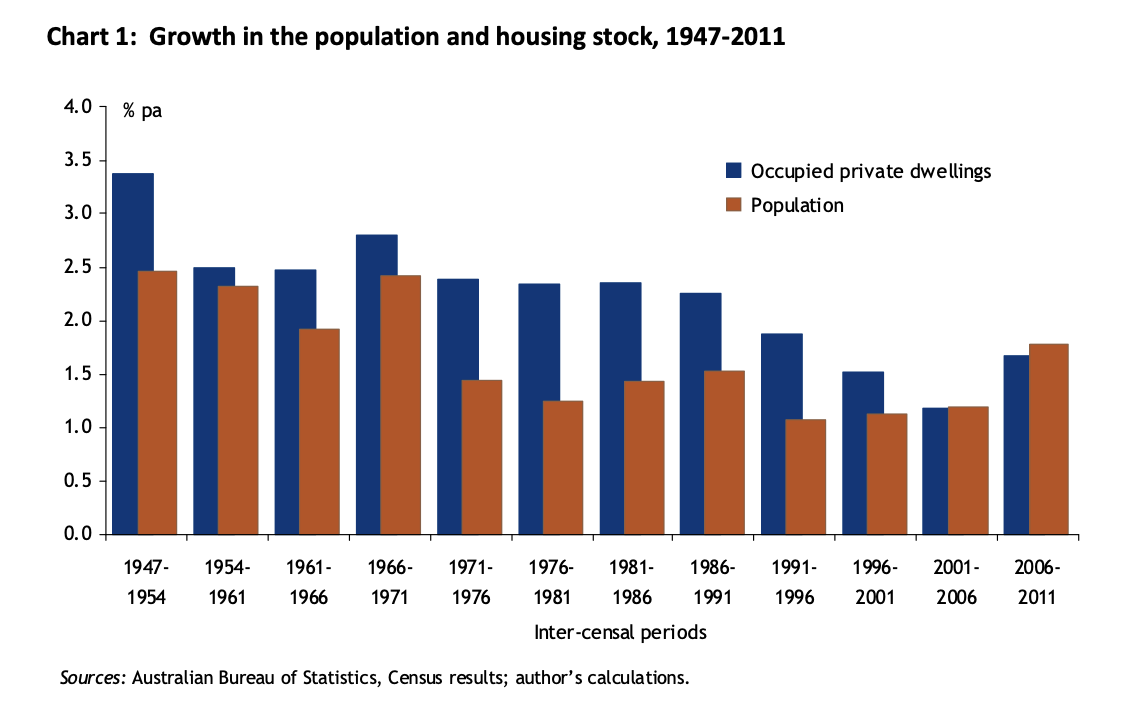

Between 1947 and 1961, government sales of housing increased the available stock by 50%, while the population only grew by 41%. Between 1961 and 1976, the housing supply went up 46%, while the population grew by just 33%. In other words, the government deliberately outpaced population growth with housing supply. And it worked. Homes stayed affordable. People could buy.

For many decades, the housing supply has kept pace with population growth. Even when prices rose, most people could still afford a home. But everything changed around the year 2000.

From 1991 to 2001, Australia's population grew by 11.5%, and housing supply rose by 18.3%. Still good. But then it shifted. From 2001 to 2011, population growth jumped to 15.9%, while housing supply only rose by 15.2%. For the first time since World War II, Australia's population was growing faster than its housing stock. And that's when the market started to get out of control. Since the 2000s, property prices have risen faster than ever before. Homes have become increasingly unaffordable. And by 2025, housing policy has become one of the most heated topics in politics.

As public anger grew, the political focus shifted—to immigration. People began to blame the housing crisis on rising migrant numbers. This has led to a political environment increasingly hostile toward migrants, even though the roots of the housing crisis go much deeper. Housing affordability is no longer just a financial issue—it's become a political battleground.

Is Immigration Really to Blame?

But is immigration truly the only reason for Australia's skyrocketing house prices? Let's rewind to the 1980s. Back then, housing was considered a basic right for every Australian. But that's when everything started to change. Housing began to shift—from being a place to live into a tool for making money. The government started encouraging people to buy a second or even third property for rental purposes, hoping to increase the supply of rental homes—because the number of public housing units built by the government was falling year after year. At the same time, tax policies handed enormous advantages to property investors.

The most iconic example? Negative gearing. This policy made the rich even richer while pushing ordinary wage earners further behind. Why can't people afford homes? Because you're not just competing with other homebuyers—you're also up against an army of investors with easy financing and tax breaks.

And that's not all. In the past decade, interest rates were slashed again and again, until they were practically zero. What happens when rates hit zero? Borrowing becomes too easy. Everyone rushed into the property market. And naturally—prices exploded. The government talks about helping first-home buyers. They hand out grants and discounted loans—which only fuels demand even more. It looks like help for young people on the surface, but in reality, it just drives prices up. And the result? First-home buyers still can't afford to buy.

So what about the housing supply? If we could build enough homes, maybe things wouldn't be so bad. But here's the reality: The number of public housing units fell from 20,000 in 1978 to just 3,000 by 2023. In an era of surging house prices and soaring rents, the government pulled back the most basic form of housing security. Meanwhile, when the private sector tries to build, it hits wall after wall: layers of red tape, strict planning regulations, and the local opposition."Not in my backyard!"—a phrase that's become every developer's worst nightmare.The result? The people who need housing the most are forever waiting for homes that never get built.

At the same time, waves of migrants continued to arrive. As soon as the pandemic ended, immigration surged to record highs—In 2023 alone, over half a million people moved to Australia. But have you ever asked: Where are they going to live? Who is building their homes? Can our infrastructure even keep up? Since COVID, the cost of construction has risen by 40%, while project timelines have grown by 18%. The building industry is already stretched to its limit. Yet in the middle of all this, the government expanded its immigration program even further, with barely any consideration for the housing market's capacity. The sole purpose? To artificially inflate GDP so it doesn't fall on paper.

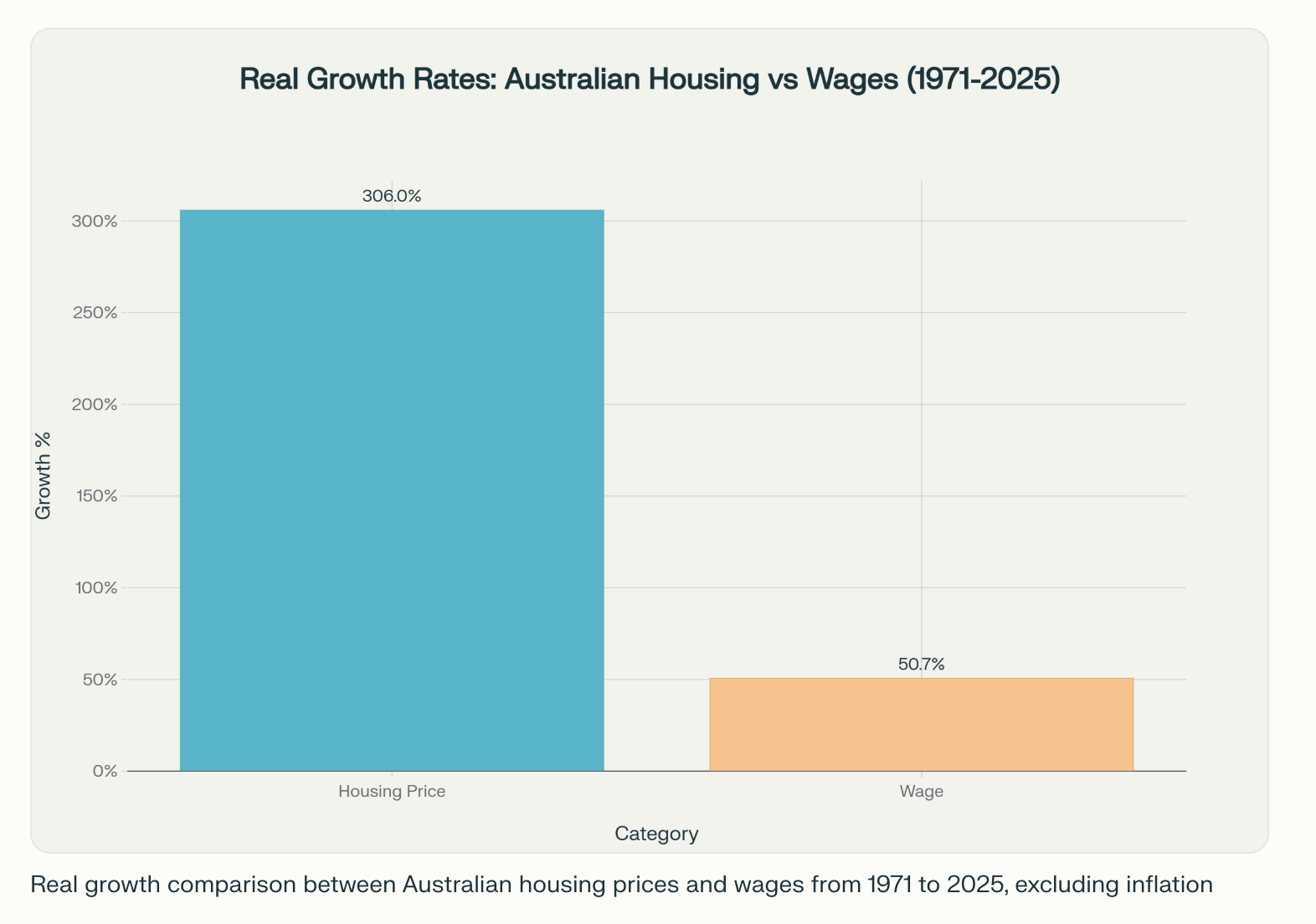

We're watching the Australian Dream fall apart in real-time. According to the latest data, since 1971, house prices have risen by at least three times after adjusting for inflation. But real wages? They've only gone up by 50%.

Today, a full-time minimum wage earner has to spend 68% of their income on rent. Saving for a deposit is almost impossible. Even if you earn $100,000 a year, you're still paying 40% of it on rent. Owning a home used to be the first step toward building wealth. Now, it's an unreachable dream. More and more people are being forced into lifelong renting while multi-property owners grow even richer. On one side are landlords—the wealthy class. On the other side, everyday Australians are trapped in the rental cycle. This divide has become deeply embedded in Australian society.

The housing crisis isn't just about immigration. It's a structural disaster caused by many forces:

None of these problems can be solved in isolation. To truly fix the housing crisis, we must restructure the entire supply-demand system. As viewers of my previous videos will remember, this structural imbalance won't be fixed in the next 20 years. For more details, check out [APS084], where I explained it in depth. If you can't beat the system, join it, invest in properties and become rich.

Housing is the first reason why ordinary people might no longer be suited to migrate to Australia—And why even many locals are finding life increasingly difficult. But the next two reasons will make you give up on Australia altogether.

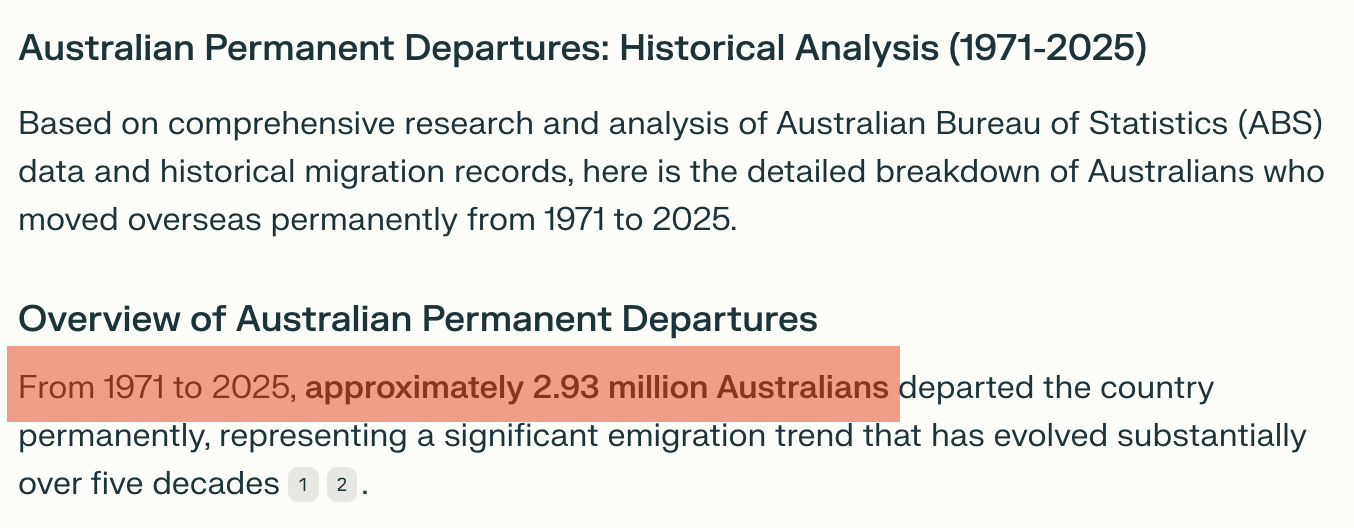

These three factors have led to a rapid surge in Australians permanently leaving the country—especially after the pandemic.

The Money Problem

For many years now, Australians have been under immense pressure—falling incomes, shrinking real wages, fewer job opportunities, and rising living costs. All of these combined are making life increasingly difficult and drastically reducing Australia's appeal to migrants from abroad.

According to the latest Wage Price Index (WPI) from the Australian Bureau of Statistics (ABS), nominal wages rose by 0.9% quarter-on-quarter and 3.4% year-on-year in Q1 2025. But inflation rose by exactly the same amount—0.9% quarterly and 2.4% annually. After adjusting for inflation, real wages grew just 1.0%, the lowest level since 2009. At first glance, wages are rising. But once you strip out inflation, the actual purchasing power is almost unchanged. In the 2024–25 financial year, real disposable income for households only grew by 0.7%—far below the 1.5%–2% levels seen around 2005. Australians have less money to spend, and the energy in society has faded compared to 20 years ago.

As of May 2025, the official ABS unemployment rate remains at 4.1%. But that's not the full story. Labour force participation has dropped significantly. Many people have stopped looking for work altogether and are now hidden unemployed—people who don't even show up in official statistics. Low-skill jobs, temporary work, and part-time roles are on the rise, while stable, high-paying, full-time positions are getting harder and harder to find. And it gets worse. With current interest rates, costs like mortgage payments, private health insurance, car insurance, and home insurance have all jumped sharply. The number of people living paycheck to paycheck—"the broke by payday" class—has increased by 15% since before the pandemic.

In today's Australia, with stagnant real wages, rising expenses, and tight budgets, working hard is no longer enough to get ahead. Even if you earn $100,000 a year, life still feels squeezed. Sky-high house prices, soaring everyday costs, and low wage growth—this toxic mix is killing the quality of life for regular Australians. Australia used to be a land where you could "settle down and live well." Today, that promise has collapsed. And now, taxation issues are making the situation even more severe—some might say, even hopeless.

The Tax Problem

In recent years, both federal and state governments have been introducing more and more taxes—on individuals and businesses. Existing tax rates are going up. New taxes are being introduced. Old tax breaks are being rolled back. In the next three years, Australia's tax overhaul could touch GST, Division 296, negative gearing, and even inheritance tax—policies that were once off-limits.

Currently, Australia's Goods and Services Tax (GST) is set at 10%. While the federal government hasn't officially proposed a hike in 2025, academics and think tanks are actively pushing for it. They want to expand GST coverage to include things like private school tuition, private health insurance, water, milk, and eggs. This would add $1.8 billion in tax revenue every year. And beyond that, there's talk of increasing the GST rate to 12.5%. All of this extra tax ultimately goes into the pockets of state and territory governments.

The federal government is now pushing Division 296—a policy targeting retirement savings. If your superannuation balance exceeds $3 million, you'll be hit with a 15% additional tax on investment earnings. That alone would be controversial. But what makes it alarming is that this is the first time Australia is taxing unrealised capital gains. Let's say you buy a property for $1 million. A year later, it's worth $1.2 million. Even though you haven't sold the home, you'd still need to come up with the cash to pay tax on the $200,000 gain. The same rule applies to stocks. If this becomes the norm for super funds, it's only a matter of time before the government extends it to trusts, companies, and even personal investments.

Australia abolished inheritance tax back in 1978, becoming the first developed country to do so. For many migrants, this was a major reason to move here—a place where you could pass on your legacy tax-free.

But now, think tanks are calling for its return. They argue that tax-free inheritances concentrate wealth in the hands of only a few people, exacerbating inequality, and want to introduce a tax on estates exceeding $2 million—excluding the primary residence. As of now, Australia's major political parties—Labor, Liberal, and the Greens—have publicly said they won't consider an inheritance tax.

But here's the catch: Over the next 20 years, $3.5 trillion is expected to be passed down in Australia. If the economy slows, government debt explodes, and inequality worsens, how long can that promise hold?

And let's be clear: Even without a formal "inheritance tax," many hidden taxes still apply.

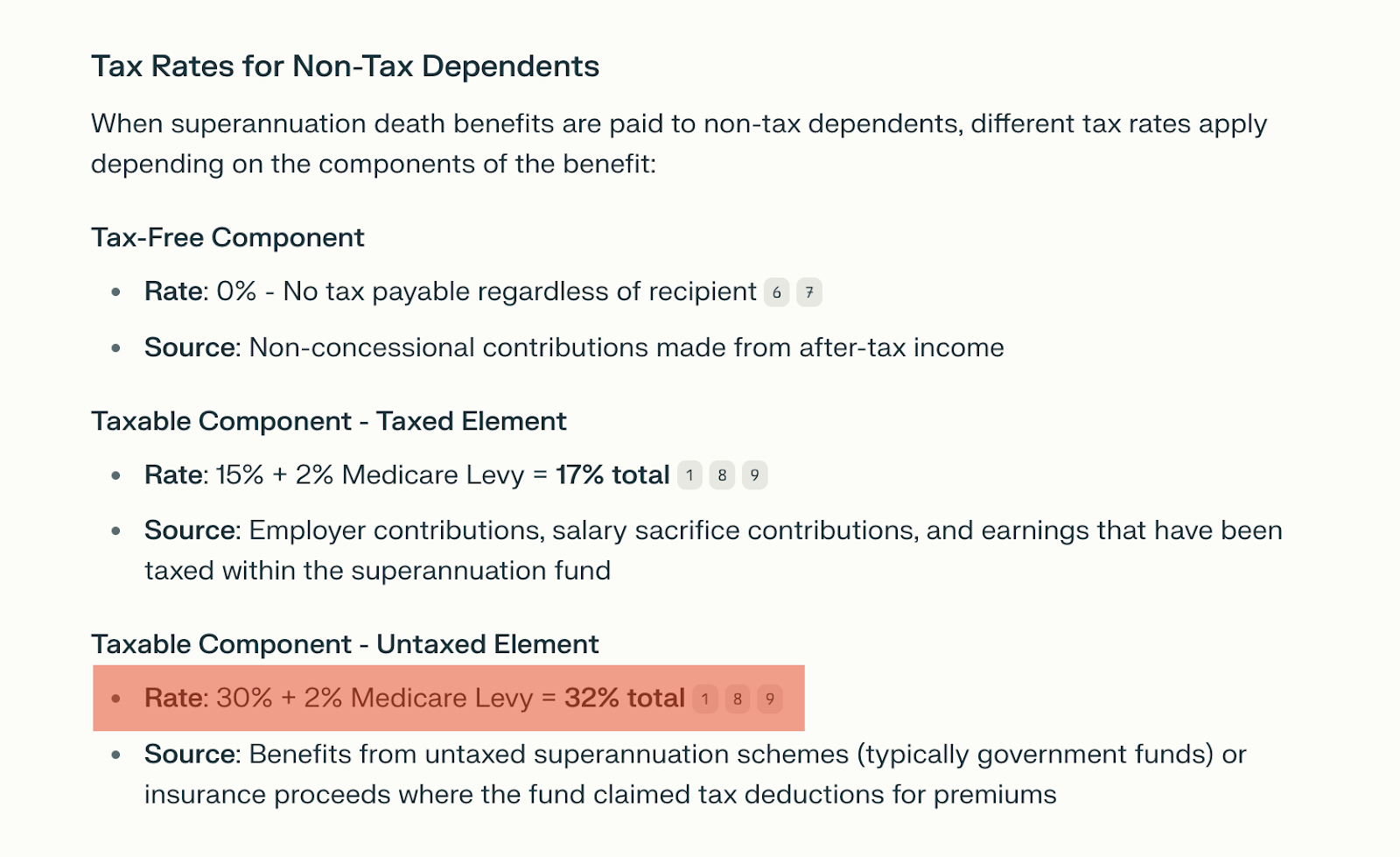

For example, if superannuation is passed to adult children, they may have to pay up to 32% in tax—a stealth inheritance tax in everything but name.

High housing costs. High cost of living. High taxes. Stagnant real wages. And now, expanding tax policies with higher rates. No wonder more and more Australians are choosing to leave and build new lives elsewhere.

So where are they going?

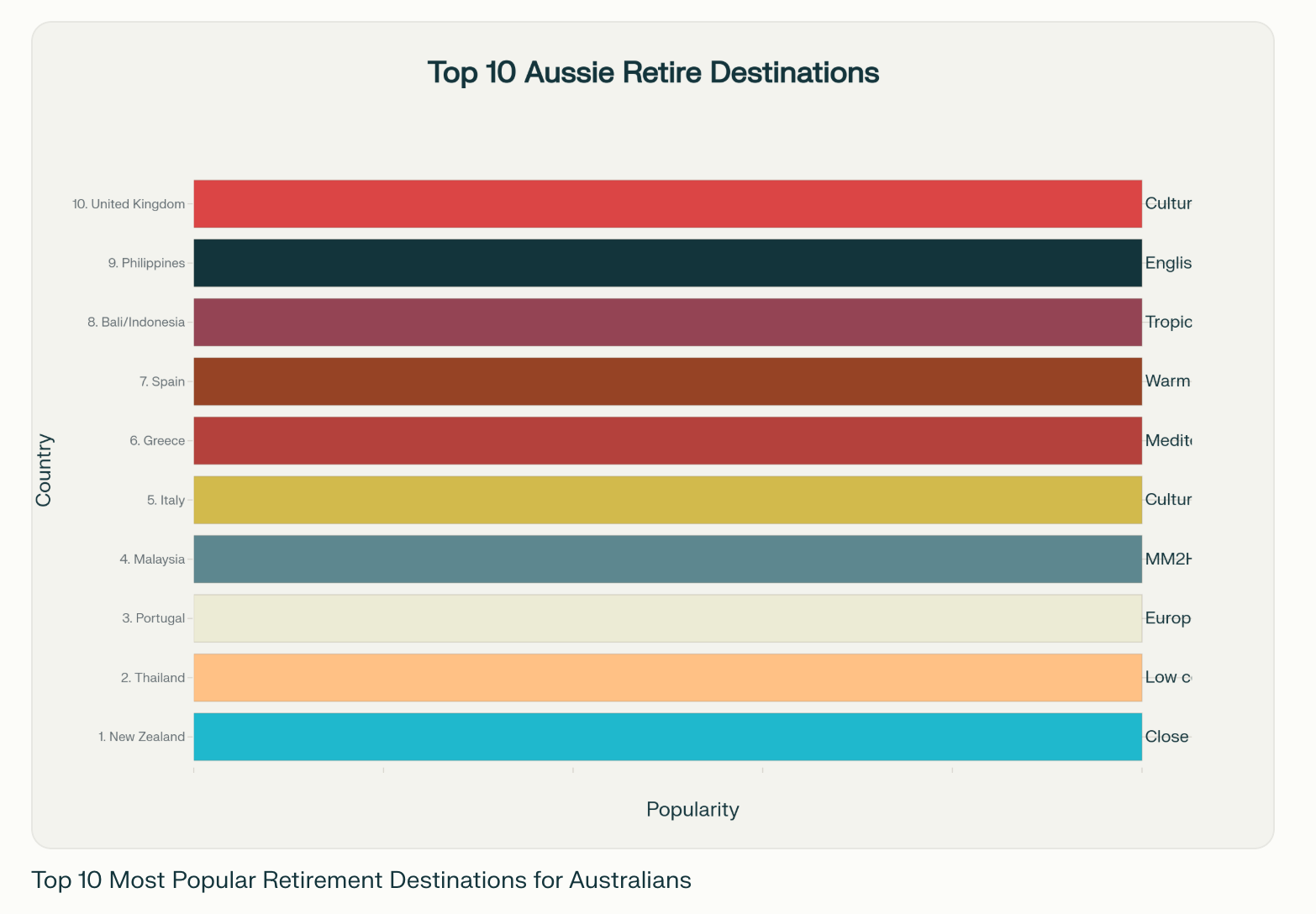

If people can no longer afford to live in Australia—if retirees are packing their bags—where are they all going? Well, here's what the data says.

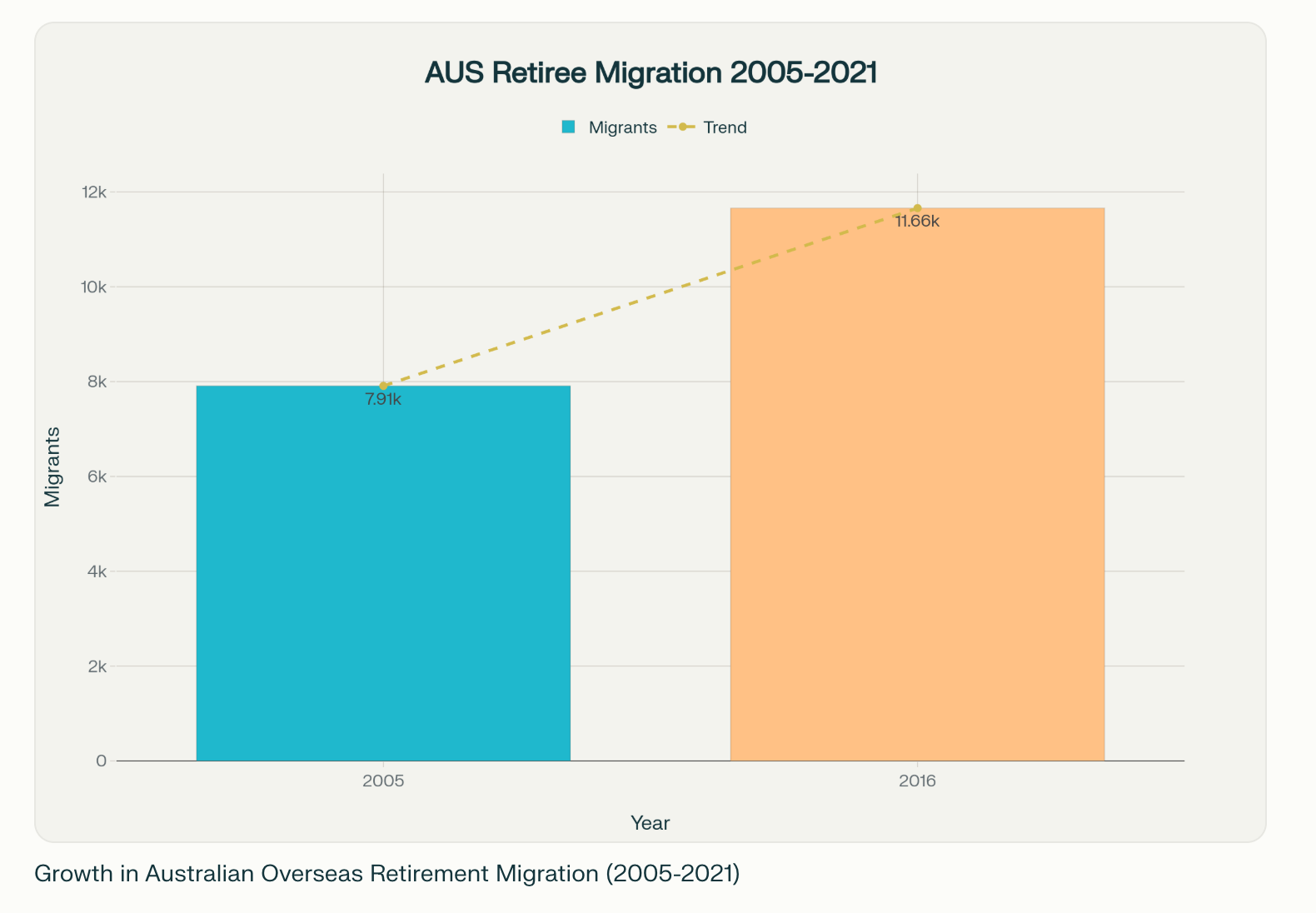

Since 2005, the number of Australian retirees relocating overseas has skyrocketed year after year. The top ten destinations? New Zealand, Thailand, Portugal, Italy, Greece, Spain, Bali, the Philippines, and the United Kingdom. Other popular options include Vietnam, Cambodia, and several South American countries. There are many reasons behind this trend. But for most people, it comes down to five main factors: Healthcare standards, Cost of living, Property prices, Climate and lifestyle, and whether the destination is a convenient hub for regional travel. But two reasons stand out above the rest: 1. Low taxes, 2. Easier access to Australian pensions while living overseas. Money is the number one factor. People are looking for places where their savings stretch further and where they can enjoy life without being crushed by financial pressure.

I would recommend anyone who wants to migrate to Australia to rethink their plan. Is Australia really the place you want to live? For everyday Australians, there are two ways to break out of your current life. 1. become a property investor and become wealthy; 2. Start planning to go overseas where your money can last longer.

Watch the video version of the blog on YouTube.