Unlock 10 Times Borrowing Power | Key for Anyone to Own 10 Properties [APS085]

You and your colleague both earn $80,000 a year. Why is it that when you apply for a home loan, you're only approved for one property, but your colleague somehow gets approved for two? And why is it that in the news and all over social media, you keep hearing stories about everyday employees who manage to buy 10, even 20 properties? The banks won't lend to you—but they'll lend to them. Why? You earn the same, and you work just as hard, so why are they growing their wealth through real estate while you're stuck, unable to move forward, no matter how much you try?

The real difference? You haven't understood the one powerful strategy that all seasoned investors in the Australian property market are using—the infinite loan strategy. This one trick can unlock your borrowing capacity completely. It allows you to keep buying more properties, expand your portfolio, and fast-track your wealth building. If you get it right, your journey to financial freedom can truly take off.

Loan Limits for Everyday People

Let's skip the fluff and cut straight to the point. No theory today—just a real-life example. When it comes to buying investment properties, most ordinary people can't get past owning two. But why is that the case? Where exactly is the bottleneck? And more importantly—how do we break through it?

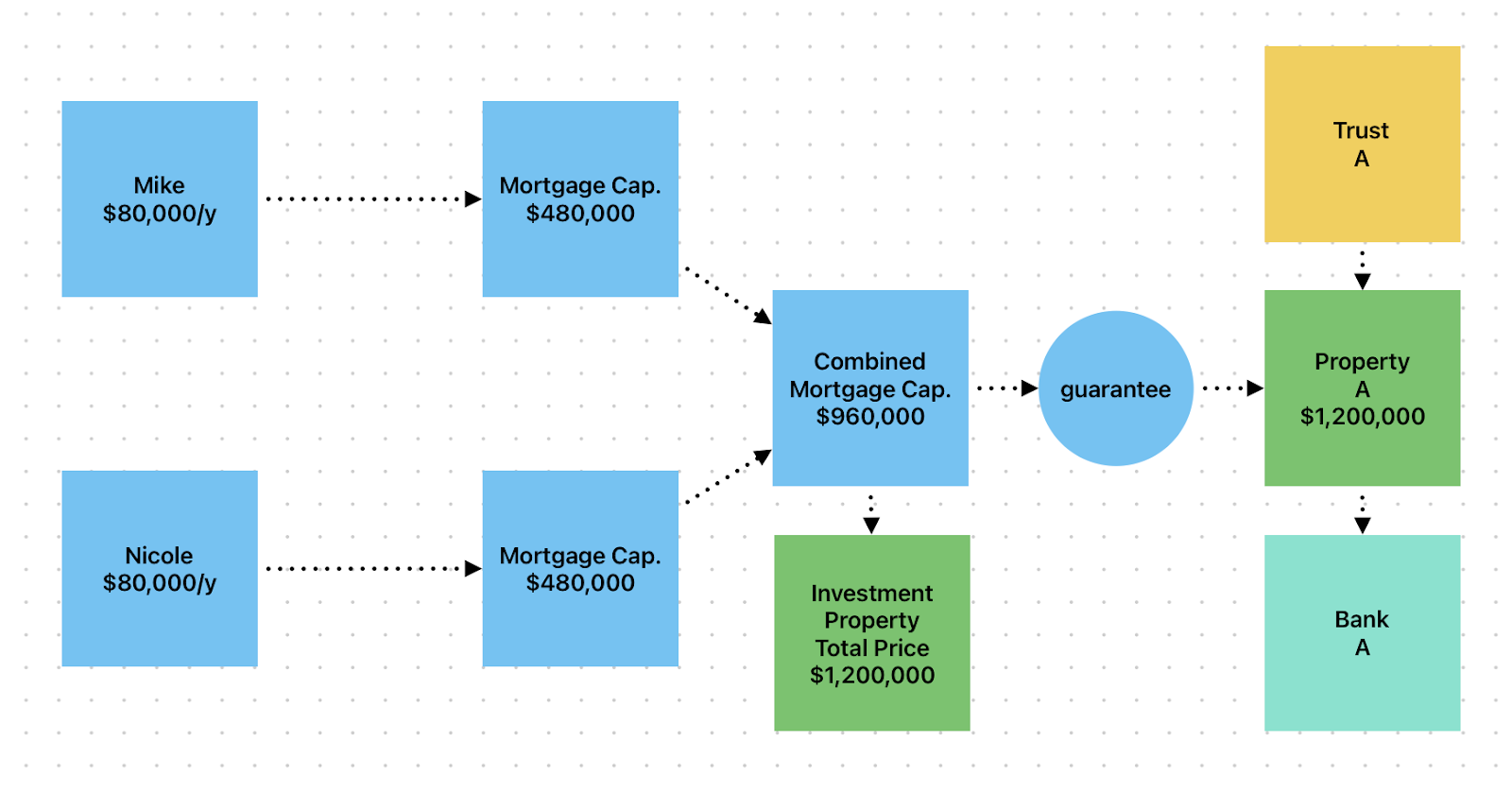

Let's take Mike as an example. He earns $80,000 a year—that's before tax and super. When assessing loan eligibility, banks subtract your personal expenses from your income: things like daily spending, rent, and transport. To keep things simple, we'll ignore expenses and assume he has no other debts. As of the time of this video, an investor's loan capacity is roughly a bit over 6 times their annual income. Let's use a flat multiplier of 6 for simplicity. So, Mike can borrow $480,000.

Assuming an 80% loan-to-value ratio, that gives him buying power for a property worth up to $600,000. Now, just to clarify—if Mike were buying a home to live in, not an investment property, his borrowing power would only be around 5 times his income, meaning he could afford a property priced around $500,000 under the same conditions.

Now here's the problem: Mike's borrowing power is maxed out. If he tries to buy another property under his own name, the bank simply won't lend to him. So what now?

Well, Mike's wife Nicole also earns $80,000 a year. If they buy property together, Nicole adds another $480,000 in borrowing power to the table. Now, as a couple, they can borrow up to $960,000, which means they can purchase up to $1.2 million worth of property. They could choose to buy one property worth $1.2 million or two properties worth $600,000 each—as long as the total doesn't exceed that $1.2 million limit. But what if even that's not enough?

Here's one possibility: They could ask Mike's and Nicole's parents to act as loan guarantors and contribute their own borrowing capacity. That could increase the total loan amount further. But of course, whether parents are willing to help and how much they can contribute depends on individual circumstances—so we'll leave that out for now.

There's another important factor we've skipped: rental income. If you're buying an investment property, it generates rent, and that rental income counts toward your personal income. For example, a $1.2 million property with a rental yield of 3.5% would bring in $42,000 in annual gross rent. That's additional income in the eyes of the bank—and more income means more borrowing power. Using the same 6x multiplier, that $42,000 could translate to an extra $252,000 in borrowing capacity. However, for the sake of this example, we assume Mike's rental income is offset by his own rent payments—so we'll exclude that boost in borrowing power for now to keep things simple.

Also, factors like interest rate cuts, lower serviceability buffers, or rising rents can also help improve your borrowing power—but these are all outside your control. The market is what it is—you simply have to respond.

So, based on all this, it seems that this couple's investment ceiling is around $1.2 million. But with just that amount, it's nearly impossible to hit any kind of serious wealth goal—let alone retire early on rental income. The math just doesn't add up. So here's the real question: How can everyday people go beyond that limit—boost their loan capacity and grow their investment portfolio further?

How Everyday People Push Forward

If you want to borrow more from the bank, there are only three ways to do it: increase your income, reduce your expenses or do both at the same time. Now, if you're still working a 9-to-5 job, trading time for wages,

this won't be easy—because to make it happen, you'll have to make some sacrifices. And those sacrifices might cost you a bit of happiness in your day-to-day life. At work, you'll need to fight for promotions and pay raises. On the spending side, you have to run your life on the bare minimum. Every month, go through your credit card statement line by line. Ask yourself: Can I switch to a cheaper mobile provider? Can I stop driving and take public transport instead? Can I cut out dining out altogether? Some white-collar workers at big companies need two coffees a day. But have you noticed? A regular-sized coffee these days costs five to six dollars. That's over $3,000 a year just on takeaway coffee. Of course, this is just an example. How much you can save comes down to your own willpower and determination—and, more importantly, just how badly you want to buy that next property. Reducing expenses also includes maximising your tax deductions. I've explained this in detail in a previous episode—check out [APS075]. Most Chinese investors I meet are very proactive about maximising tax deductions. But among local Australians, I've seen some rather surprising behaviour. Some people in their 40s, earning between $150,000 to $200,000 a year, are still renting, and when it comes to tax time, they choose not to claim any deductions—they're happy to just pay more tax. At the same time, they can't control their spending, blowing money left and right, ending up with no savings—and then complaining that they can't afford to buy a property. Well, maybe try spending less, claiming more tax, and saving more. Of course, this part falls under personal finance, and if you're interested, I can do a full episode just on that. Also, if you have any other debts besides your mortgage—like credit cards, car loans, or "buy now, pay later" balances—paying them down a bit can also boost your borrowing power.

Now, for those with a more proactive mindset, some people start exploring side hustles after work. Starting a small business. And who knows? Maybe it'll turn into something big one day. You'll never know unless you try. Starting a company entity and launching a side hustle can do more than just generate income. It also opens up a whole new world of tax deductions. And here's something many people don't know—after holding the company for two years, it can actually increase your personal loan capacity. Why? Because the company is yours, and you decide how much salary to pay yourself. You want to raise your income? Pay yourself more. Higher income = higher borrowing capacity. One important tip: you must register for GST from day one—only then will the banks recognise your business income.

So yes—promotion and pay rises, smart personal finance, and entrepreneurship can all effectively improve your loan capacity. But each of these paths requires a different kind of skill. Getting promoted requires professional ability. Managing money requires discipline. Running a business takes courage, business sense, and a bit of luck. So what about people who don't have any of these skills? What if you're just a regular person? How do some people manage to buy 10, 20, or even 30 properties and build a real estate portfolio worth $10 million? How did they do it? Well, that's what we're going to talk about next—and this, right here, is the core of today's episode. If you understand this method and get a professional team to help you execute it, then your borrowing capacity won't just be like Mike and Nicole's $960,000. If you play your cards right, you could hit $9.6 million, or maybe, just maybe… even "unlimited."

Cracking the Loan Code for Everyday People

So how is it that someone earning the same salary as you is able to borrow many times more? The answer lies in a trust structure—and an unspoken understanding with the banks. The top-level mortgage brokers in the industry don't just know the rules. They understand the legal and regulatory frameworks of the banking system, they know the differences between banks, and most importantly, they know how to leverage those differences to increase your loan limits.

But using a trust structure to boost your borrowing capacity isn't something you can do alone. You'll need the combined expertise of a top-tier mortgage broker and a property-focused accountant. And the good news is, at AusPropertyStrategy, every VISION member has access to a whole five-person support team: an investment strategist, mortgage strategist, property accountant, financial planner, and legal advisor. Our mortgage team is led by Thomas Tang, one of Australia's highest-volume mortgage brokers and a recipient of the MPA award. He specialises in solving complex lending issues for our clients. The accounting team is headed by veteran CPA Winnie Xia. Together with the rest of our team, they work seamlessly to provide comprehensive support. We've already helped many clients successfully use trust structures to increase their loan capacity significantly. But again—this is not something you can pull off alone. You need a strong, experienced team behind you. So now let's walk through how a trust structure boosts your borrowing power—and why it allows everyday people to buy multiple properties.

Let's go back to the example from earlier. Mike and Nicole each earn $80,000 a year. Together, their combined borrowing power is $960,000, which means—at an 80% loan-to-value ratio—they can afford up to $1.2 million in property. For most people, this is the ceiling. But what if, instead of buying a property in their own names, they first set up a trust?

Here's how it works: They create Trust A. The trustee is a company, and Mike and Nicole are its directors. The beneficiaries? That can be decided at any time. If you're curious about how trusts work, check out [APS024]

Trust A then buys Investment Property A, using Bank A for the loan. Bank A reviews the documents and sees that Mike and Nicole have a combined borrowing power of $960,000. They agree to let the couple guarantee the trust loan. That allows Trust A to purchase up to $1.2 million in property.

Now, one small note: In personal names, you can claim negative gearing to reduce taxable income—but this doesn't apply to trusts. So, technically, borrowing power through a trust is slightly lower. But to keep the example simple, we'll ignore that difference here. What's important is this: Loans under a trust must be personally guaranteed, but they don't reduce your personal borrowing capacity—as long as the trust property is cash flow neutral or positive.

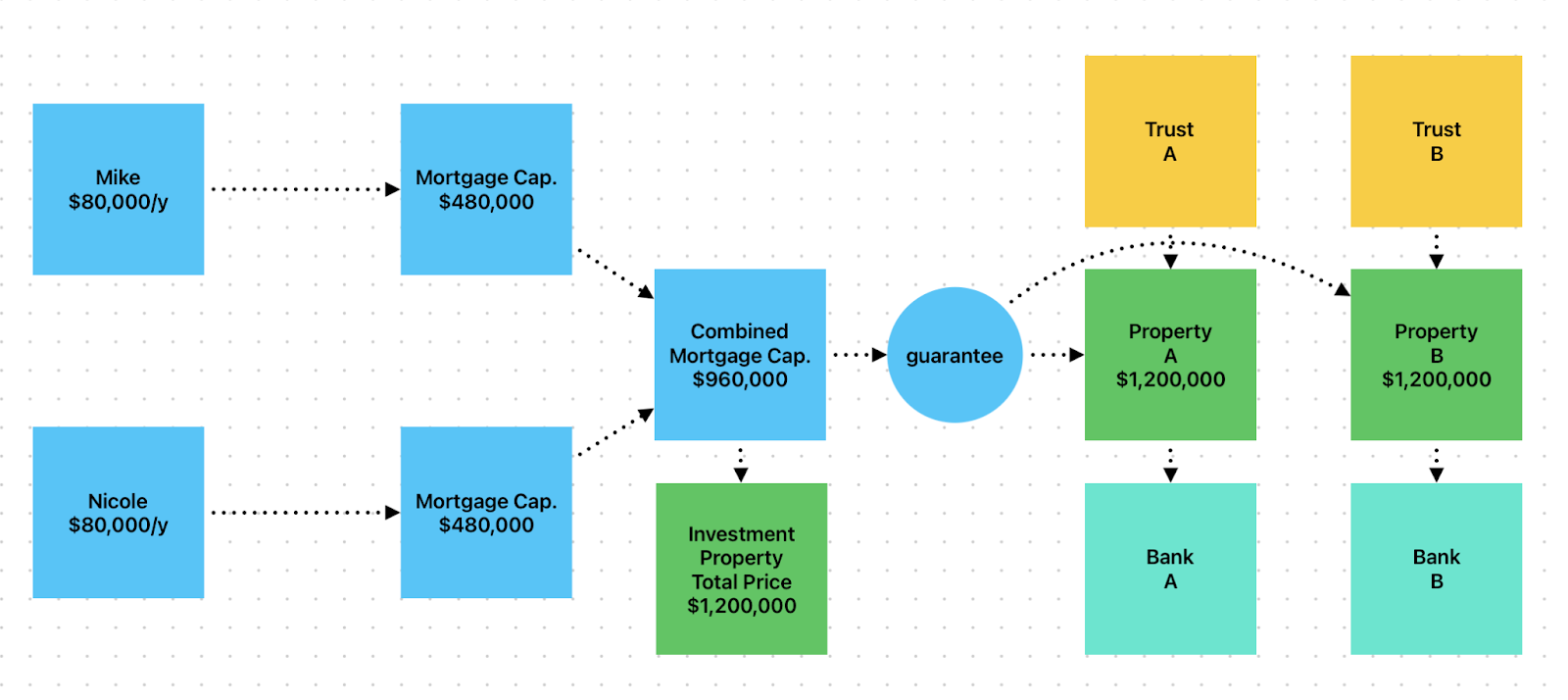

So in this case, even though Trust A now holds a $1.2 million property, Mike and Nicole can still buy another $1.2 million property in their personal names. But here's the catch: If the property inside the trust is negatively geared (i.e. losing money), Mike and Nicole would need to inject personal funds into the trust to cover the shortfall. And if that happens, banks will no longer treat the trust as a separate entity. They'll see that cash flow as part of Mike and Nicole's personal obligations, which will reduce their borrowing power. So how do we solve this?

Option one: Only buy positive cash flow properties inside the trust. But in 2025, that's extremely difficult. Why? Because interest rates are still relatively high, and those cheap, high-rent suburbs from a few years ago have already had their price surge. Rental yields have dropped sharply. Let's be honest—the era of bargain-hunting is over. Option two: Lower the loan-to-value ratio. Instead of borrowing 80%, drop it to 60%. Yes, this works. But it requires a lot more cash. For example, a $1.2 million property with 80% LVR only needs $240,000 in cash. At 60% LVR, you need $480,000 in cash as a deposit. And we haven't even included stamp duty and other upfront costs yet. If you're interested in the full list of 17 property-related costs in Australia, check out [APS042].

In practice, we rarely use these two methods. Instead, we prefer the following three techniques, which are far more effective:

If the trust property is negatively geared, just inject after-tax cash into the trust. Because it's after-tax money, it won't show up on any financial statements—banks won't even see it.

When selecting properties for the trust, we make "short-term rental potential" a key selection criterion. Our own nationwide short-term rental platform has been running for over 3 years. We can provide same-day estimates on short-term rental returns to guide buying decisions. In many cases, properties bought as long-term rentals turn out to be short-term gems. This helps boost cash flow—often turning negative cash flow situations into break-even or positive returns.

Use our in-house accounting and lending services to present a clear picture to the banks. Even if the property is slightly cash flow negative, we can often reassure lenders in ways that prevent it from affecting your personal borrowing limit.

Now, at this point, you might be thinking: "Okay, so all this lets me double my buying power—from $1.2 million to $2.4 million. But you said people could buy 10 times more or even reach 'unlimited.' Aren't we still a long way from that?" Well—this is where the magic happens.

Mike and Nicole set up Trust A, bought Property A, and got financing from Bank A. Next, they set up Trust B, buy Property B, and get a loan from Bank B—again using their same $960,000 in personal borrowing capacity as the guarantee. That means Trust B can now also buy a $1.2 million property. Here's the key insight: Mike and Nicole's personal borrowing capacity can be used to guarantee multiple trust loans as long as the properties within the trusts generate cash flow that's either neutral or positive. In other words, this strategy can be copied and pasted over and over. Suddenly, expanding your borrowing power doesn't seem so impossible, right?

Now you might ask: "But wouldn't the banks know that I'm using the same guarantee across multiple trusts? Even if they're different banks, don't they share information?" In theory, yes. But in practice, here's what we've seen: Even when loan officers are clearly aware that the guarantee is being used multiple times, they still approve the loan. Why? Because banks want to do business. They want you to borrow more. As long as there are no explicit regulations prohibiting it, most banks will let it go through. It's legal. It helps the bank grow. And as long as your repayment ability checks, why would they stop you?

By now, many of you are probably getting excited. So this is how people on the same salary as me can borrow so much more! Yes—this is what they're doing. But let's be clear: This strategy isn't magic. There are still plenty of conditions and complexities behind the scenes. And that's exactly why you need a strong, professional team to pull it off for you.

The Limitations of Buying a Property Through a Trust

Now that we've solved the problem of getting loans to buy a property, the next question is—where does the cash come from? For everyday employees, no matter how hard they work or how much they save, even if they try to start a business on the side, it's still tough to save up the deposit for the next property in a short period of time. That's when you need to start thinking creatively.

If you already own a property and it has some equity in it, you can extract cash by refinancing or topping up the loan. If your investment property has gone up in value, you can do the same. But here's the problem: To increase your loan limit and pull out cash, you need to improve your borrowing capacity first.

In the previous example, let's say the property inside the trust rises in value from $1.2 million to $1.5 million. Mike and Nicole want to refinance and extract equity—but they already used up the entire $960,000 borrowing capacity when the trust originally bought the property. Now it gets awkward: The property has gone up in value—yet you can't pull any money out. That's why, when you buy your first trust property, you should leave some buffer. Buy slightly below your limit so you still have room to move. At the same time, work hard on your personal finances to increase your borrowing capacity so you're prepared for future equity extraction. You can also do some cosmetic work on your loan documents to make them look better and secure a higher loan amount.

At this point, someone might ask: "Do I really need to set up multiple trusts just to buy a few properties? Aren't trusts expensive to set up and maintain?" Yes, you're absolutely right. If you want to know how much it costs and the other benefits of setting up trusts—like asset protection and estate planning—check out [APS076], which explains it in detail. That episode also walks you through land tax thresholds, surcharges, and the setup and maintenance costs of buying through a company, a trust, or a self-managed super fund (SMSF). I strongly recommend that serious investors watch it more than once.

So—is it worth setting up a trust? Even after factoring in setup and ongoing costs, if you buy the right property with strong cash flow, then yes—it's absolutely worth it. Of course, that's where a professional team comes in—to help you make informed purchase decisions. Every VISION member at AusPropertyStrategy enjoys all-in-one support, including trust setup and management, property sourcing, financing, short-term rental services, and more.

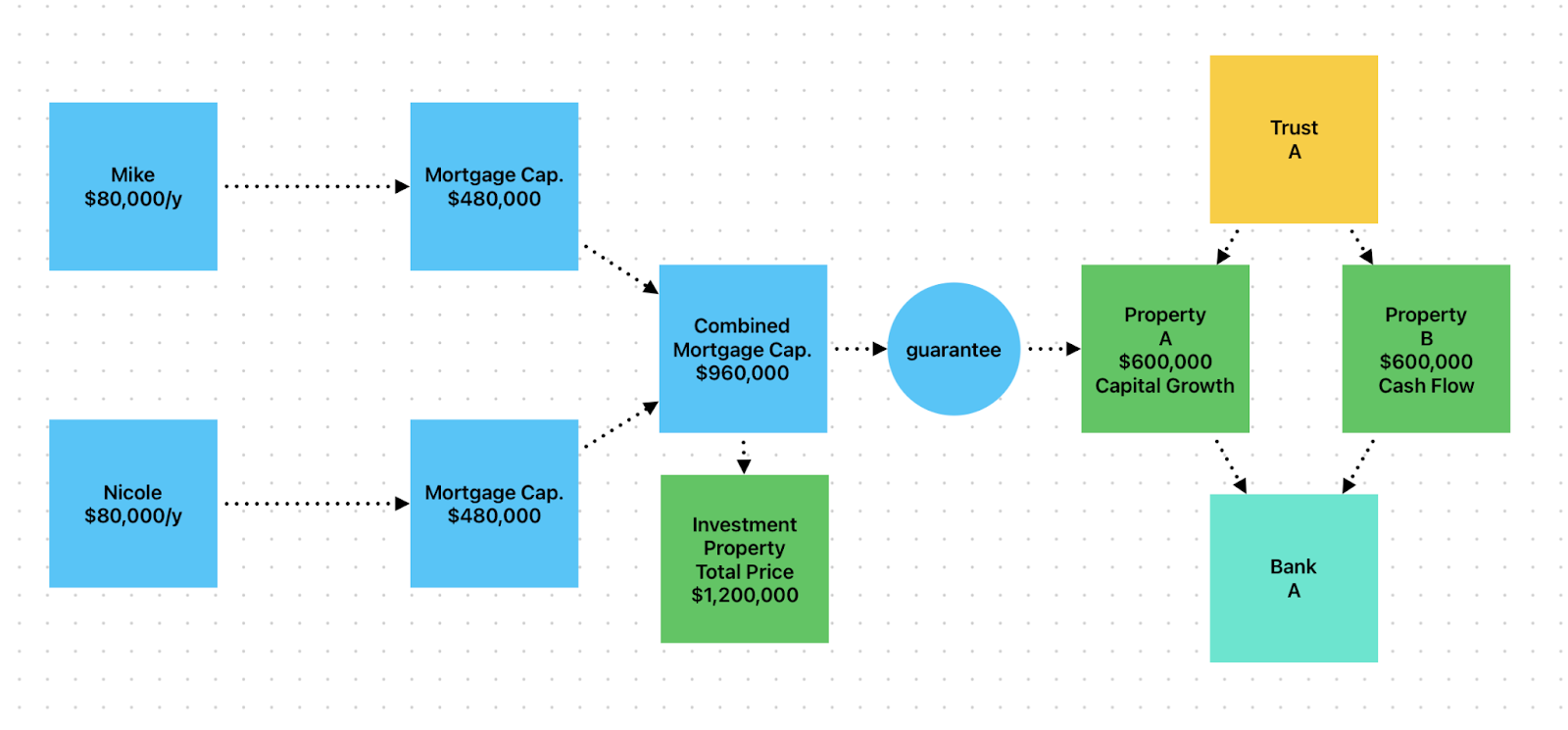

Let me give you a little spoiler: To balance cash flow and reduce the number of trusts, thus lowering your costs, you can use one trust to buy two properties: One focused on capital growth, the other focused on cash flow. The goal is to make the trust's cash flow break even or even slightly profitable. Because profits inside the trust must be distributed each year—and that adds to your personal taxable income. However, in practice, every situation requires a tailored strategy.

The Best Path for Everyday People to Build a Property Portfolio

Let's go back to the beginning. Mike and Nicole are starting from scratch, and their goal is to build a property investment portfolio. So what should they do first? Here's the first rule: I don't recommend buying an owner-occupied property first. Let's leave aside comfort and mortgage stress for now. The real issue is—a primary residence eats up your borrowing capacity. If Mike and Nicole buy a $1 million home to live in, they'll have used up all of their borrowing power. Here's why: For owner-occupied loans, the bank uses 5x their income to assess borrowing. For investment loans, it's 6x. If they buy a home first, at best, 5 to 6 years later, once their incomes have increased slightly, they might be able to buy a cheap investment property. Another 10 to 20 years down the road, once their superannuation has built up to $300,000 or $400,000, they could establish a self-managed super fund to buy another small investment property. And… that's it. Game over. Their investment journey is blocked—entirely—by loan limits. Now, for most people, that's still a decent outcome. But, according to AusPropertyStrategy's standards, this strategy fails the test.

So—what's the better approach? Start by setting up a trust. Buy your first investment property at 20% below your max borrowing limit. Then, set up another trust and buy again. At the same time, actively improve your personal borrowing power—so you're ready to refinance and extract equity from the properties inside your trusts later on. Early on in the process, focus on capital growth properties. Later, shift toward cash flow properties. Cash flow helps you increase borrowing capacity, and good cash flow prepares you for early retirement. Once your investment portfolio is complete and your wealth goals are met, then use your personal loan capacity to buy a home to live in. And if there's an opportunity—set up an SMSF to buy one more investment property.

This approach helps you maximise your borrowing power to acquire more properties. Of course, this is an aggressive strategy. You need to manage your cash flow and repayments carefully and make sure every single purchase is the right one. At AusPropetyStrategy, every VISION member gets a tailored plan—because everyone's situation is different. There is no one-size-fits-all formula.

Some people might say: "Everything you're saying assumes property prices go up. What if prices fall?" Here's my take: In Australia, whether you look at the state level or the suburb level, prices go up and down in the short term, but over the long term, they always go up.

We take a long-term view, so short-term volatility doesn't shake us.

And you must invest across different states—to take advantage of different market cycles and land tax thresholds. That makes your portfolio more resilient. As for me—I'm bullish on Australian real estate for the next 20 years. But if you think prices will fall for the next 20 years, then property investment isn't for you.

Here's something interesting: I first shared this trust strategy two years ago on my other channel. Back then, no one was talking about it. After the video came out, mortgage brokers and social media creators started contacting me, asking how it worked. A bunch of copycats even began creating content on the same topic. But here's the thing: Many people know about this strategy, but very few can actually execute it. Why? 1. Most people don't have a good mortgage broker. Think about it: How long has your broker been in the business? Do they invest themselves? Have they personally used the trust strategy? It's risky to trust someone who's never done it. Most brokers are only trained to handle basic PAYG loans. They don't understand the more advanced stuff. 2. They don't have a good accountant. An accountant isn't just there to do your tax return. They need to build and manage your trust—and prepare for accountant letters when needed. Many accountants can't do it. Some only know how to use templates to sep up a trust. Some absolutely refuse to issue any accountant letters. 3. And even if you do find a good broker and a good accountant, can they communicate well with each other? Most of the time, they can't. That's why many people know the theory, but very few can apply it.

But here's the good news: Every single one of these issues has been solved with the upgraded VISION Membership. For our clients, from setting up a family trust, injecting capital, and preparing loan applications, it takes us about two weeks. For SMSF setup, rollover funds, and loan, also two weeks. It's fast—because we've done it so many times, we know every step inside and out.

If you'd like to see a full walkthrough of the numbers behind these strategies, leave me a comment. I'm happy to make a full breakdown. The only question is—are you willing to put in the time and brainpower to understand it? Or would you rather leave it to the professionals?

Watch the video version of the blog on YouTube.