The Market Is Going Wild Again | In 2030, You'll Regret Not Buying a Property Today. [APS082]

If you had bought a property in Australia back in 2020, five years later—today—you'd definitely be thanking your past self. As long as you didn't make a mistake, your property value has already gone up by 50% to 70% during these five years. If you buy a property now, chances are—you'll still be thanking yourself when you look back five years from now. Because right now, the market is already showing very clear signs of an upward trend. And this momentum is very likely to continue for another 1 to 2 years. 'History Doesn't Repeat Itself, but It Often Rhymes' So, in this video, let's break down what's happening in the Australian housing market and what's likely to unfold over the next 12 months. All the ingredients that fuel price growth in Australia are now back in place.

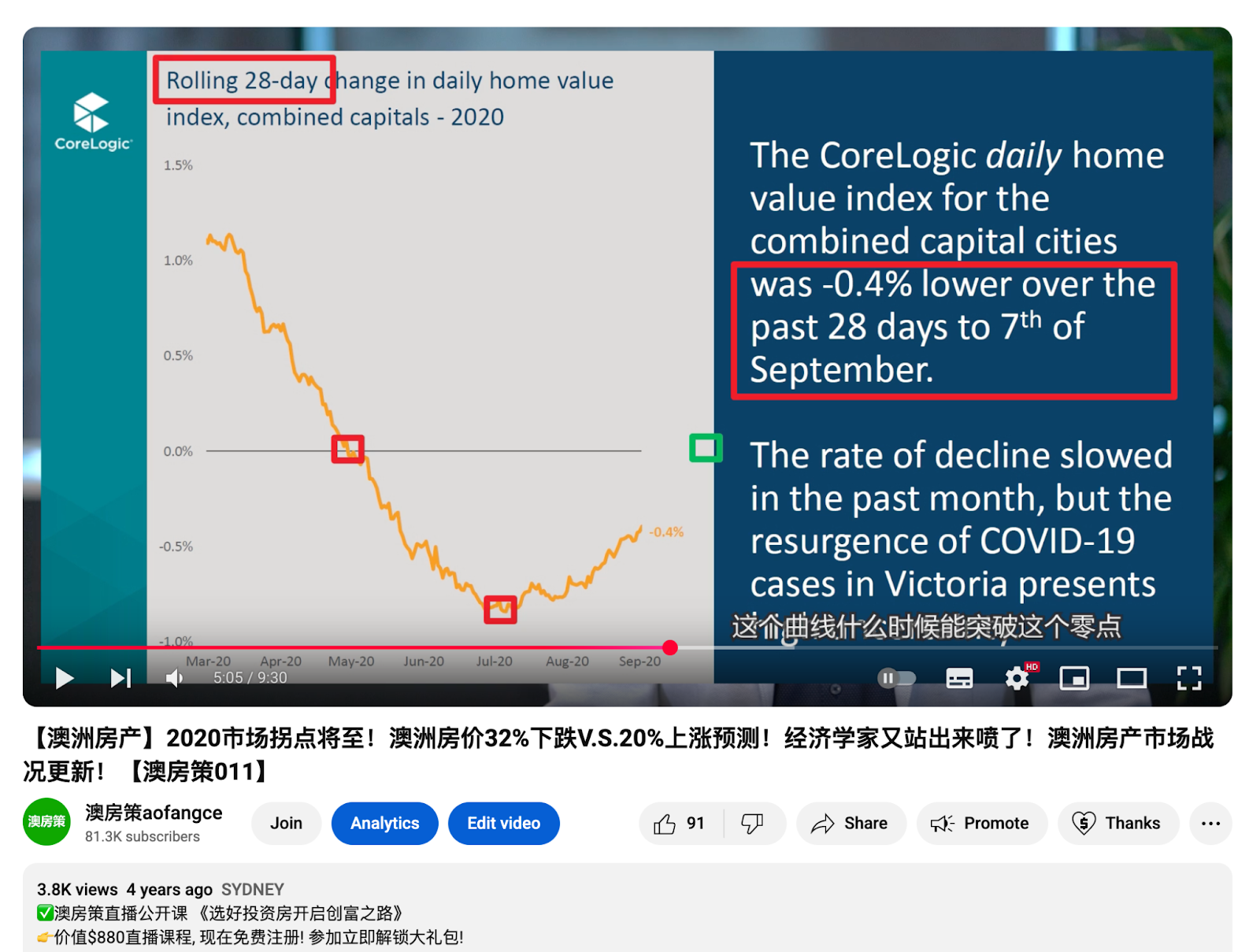

A Video from 5 Years Ago

While going through past episodes from my other real estate investment channel, I came across Episode 11—recorded five years ago. It was September 2020. At that point, Australia had already passed the most worrying stage of the pandemic. What we saw then was that the national housing price index had entered a correction phase around March 2020. The decline accelerated through July and then started to slow down by September. At that time, economists were split into two camps. Among the Big Four banks, three predicted that property prices across Australia would fall within the next 12 months. The most extreme forecast even projected a 32% drop. Only one bank predicted a rise—of 20%.

But in that video, I said this: a property boom in Australia was about to begin. The turning point was near. As for the result—well, we all know how that turned out. At its worst, the housing market in 2020 only dipped by 2.3% compared to pre-pandemic levels. And after that came a powerful rally, with the national market climbing nearly 30%. In certain areas, specific properties even doubled in value. Although there was a correction again in 2023, the market soon hit new highs afterwards. And now, in May 2025, we are seeing signals that look almost identical to those from back then. And this time, the signs are even clearer: A brand new wave of housing price growth has already begun.

By the way, in case you're wondering how I achieved this badge of 100K subs with only 13K subs, I have an Australian property investment channel in Mandarin with 80K subs and a financial investment channel in Mandarin with 340K subs.

Australian Property Market Accelerates in May

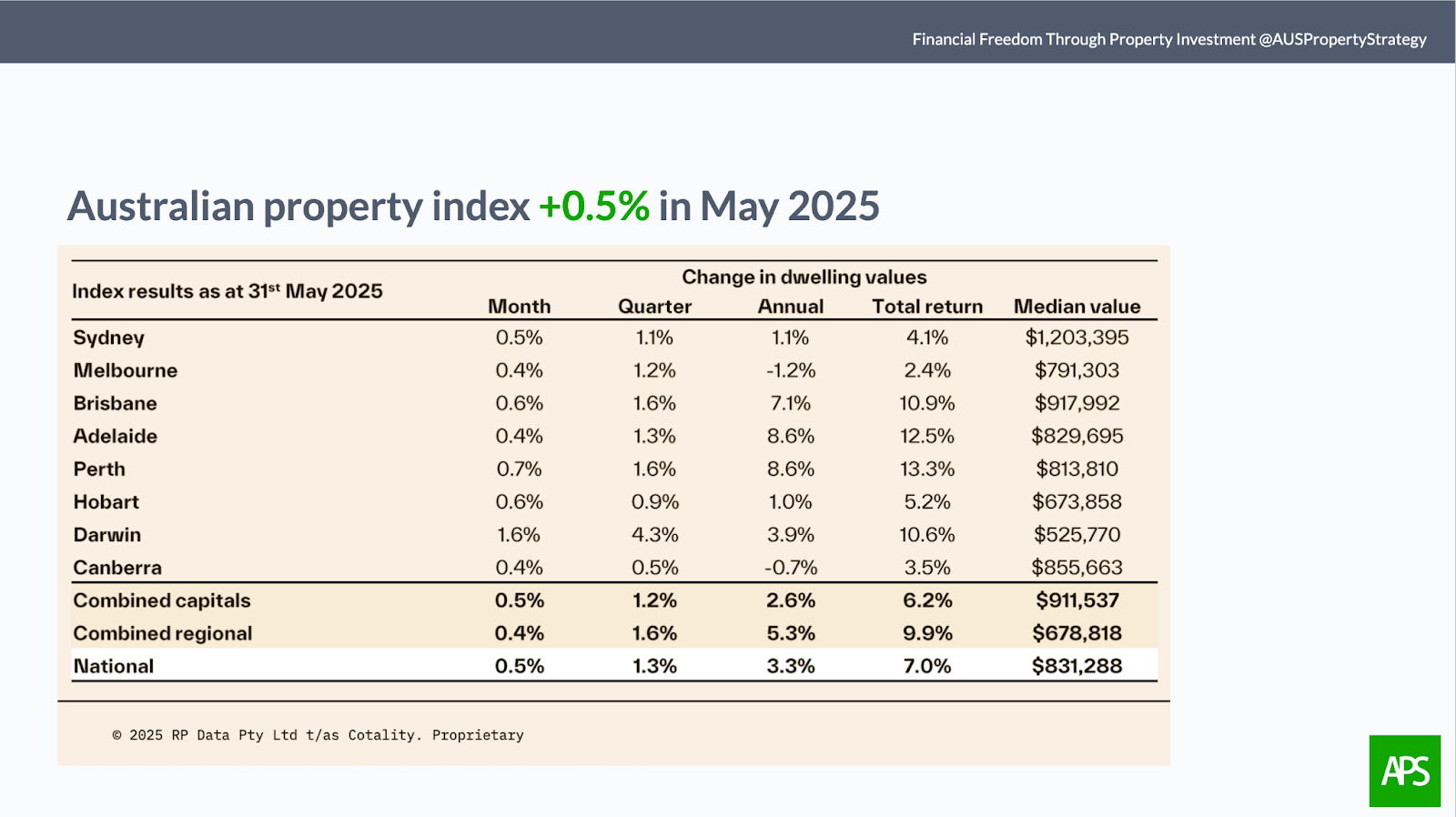

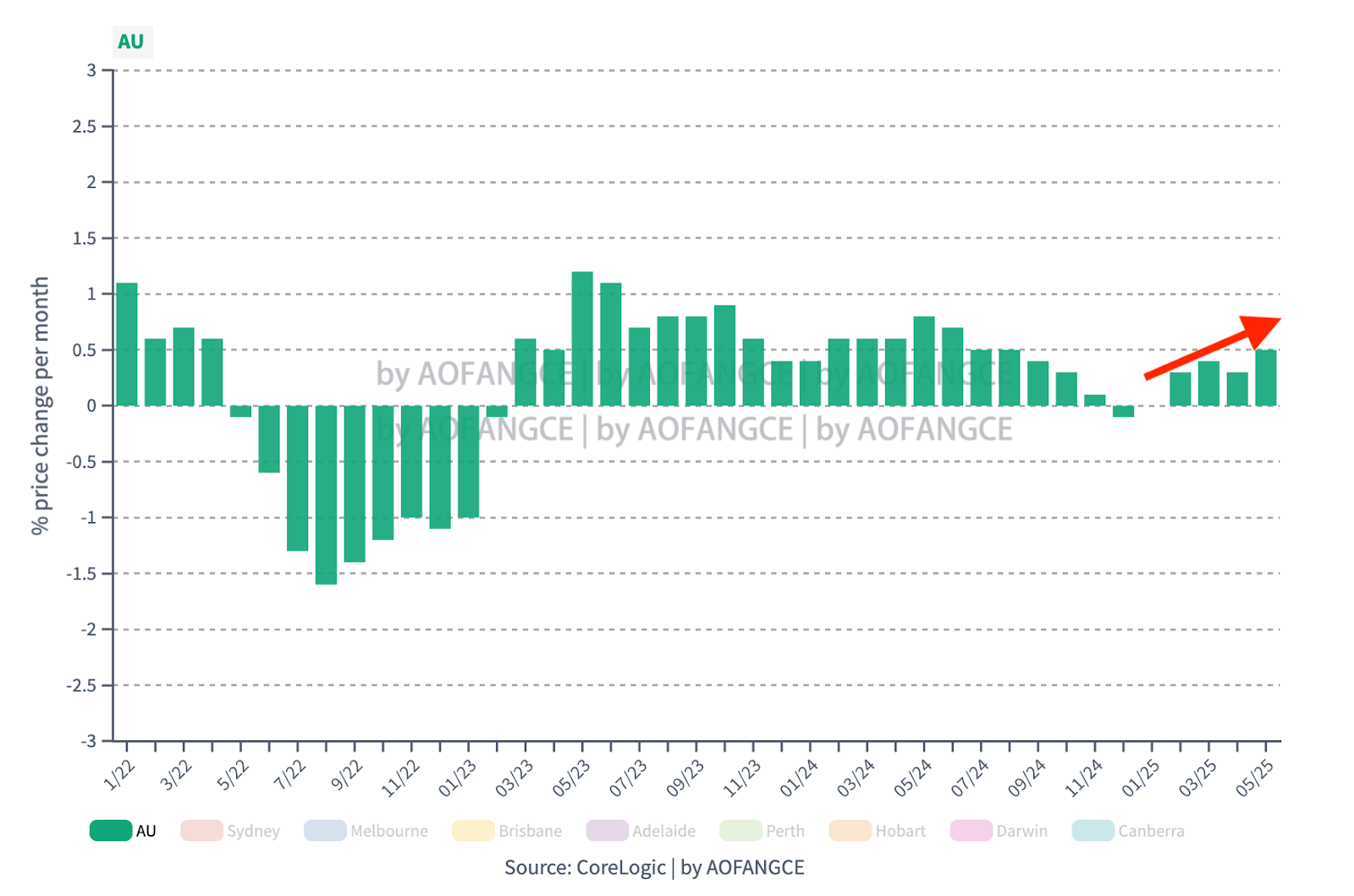

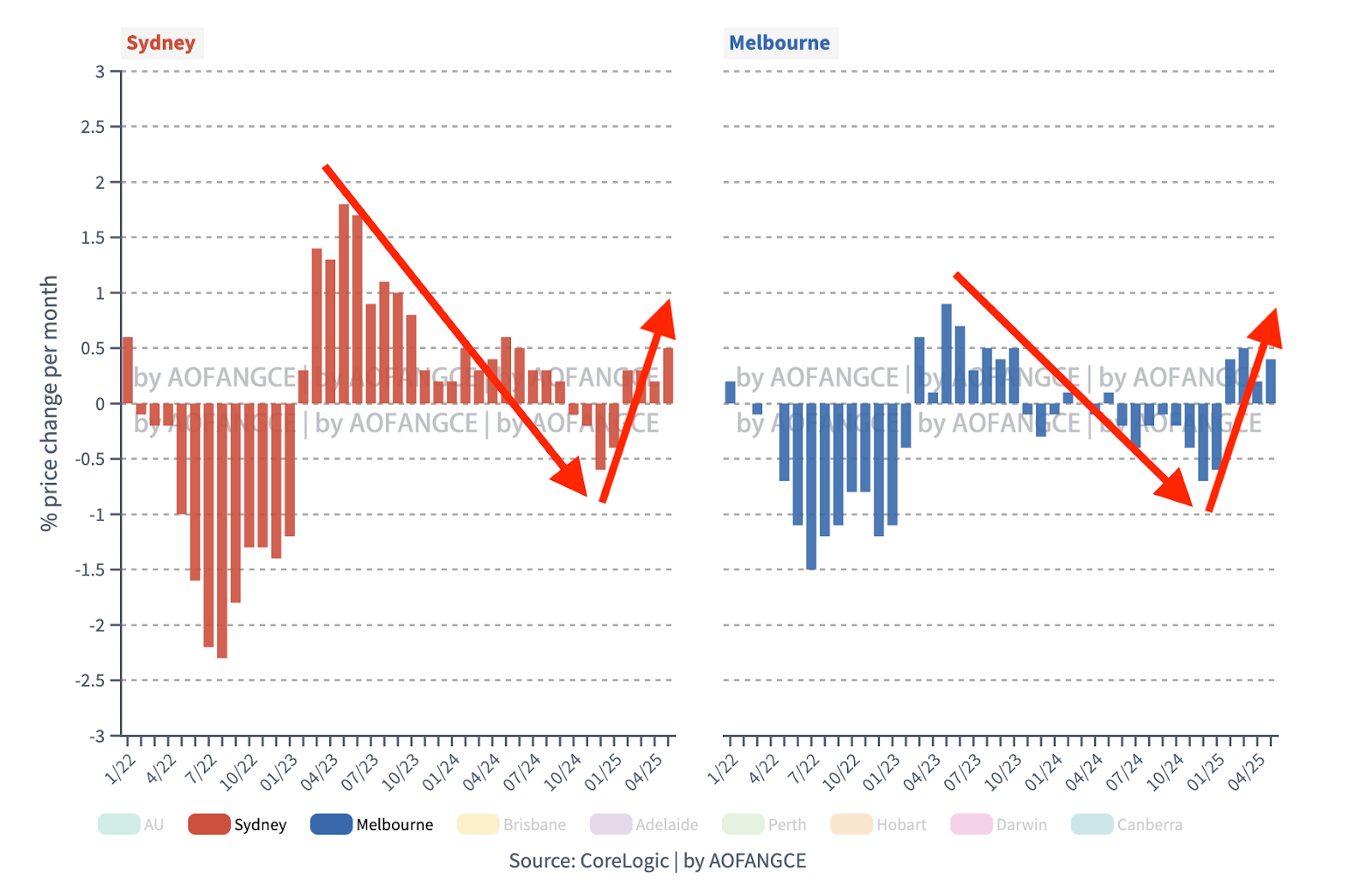

Let's get straight to the point. After hitting rock bottom with a 0.1% drop in December 2024, the Australian housing market began to rebound. In January, February, and March, prices rose steadily and at an accelerating pace. There was a slight slowdown in April, mainly due to election uncertainty and the fading effect of February's interest rate cut. But with the election now behind us and another rate cut in place, May saw a 0.5% increase in national housing prices. If we connect the dots from January through May, the trend clearly shows accelerating growth.

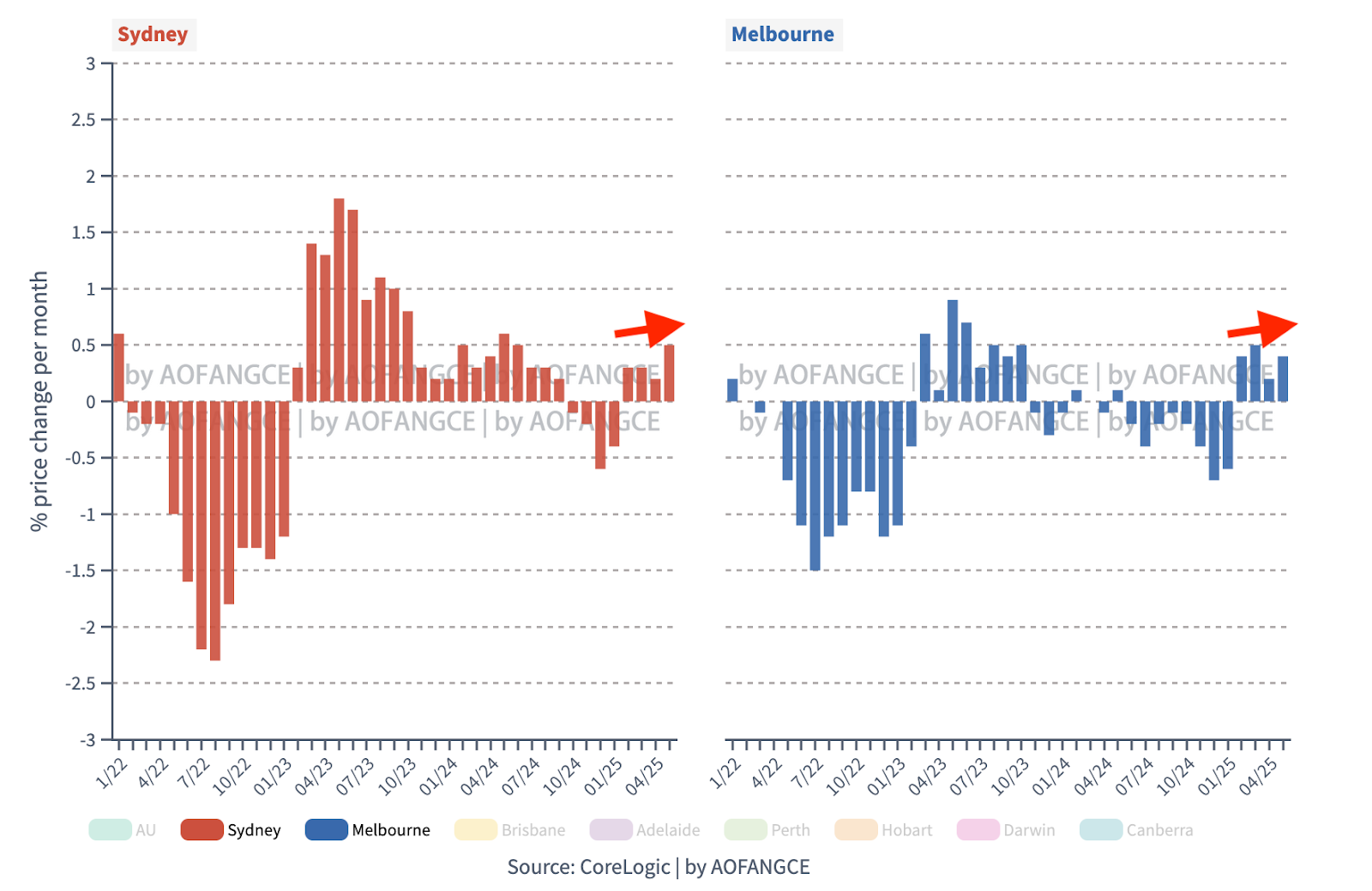

In May, Sydney's property market rose by 0.5%—a sign of continued momentum. Melbourne followed the same trend, up 0.4% in a single month. If you zoom out and look at the broader picture, you'll see a distinct V-shaped recovery. Sydney hit its last peak in April 2023, bottomed out in January 2025, and is now clearly entering a new growth cycle. Melbourne's rebound isn't as steep, but the trajectory is similar.

So, when is the best time to buy? That would be November last year. But let's be honest—most people didn't buy then. Why? Because at the time, all the news headlines were negative. Everything people saw or heard about Sydney and Melbourne was bad. This is exactly why the average person struggles to get the timing right: they just absorb all market noise. Meanwhile, many of our VISION members—guided by our investment strategists—started buying in Sydney and Melbourne between September last year and January this year.

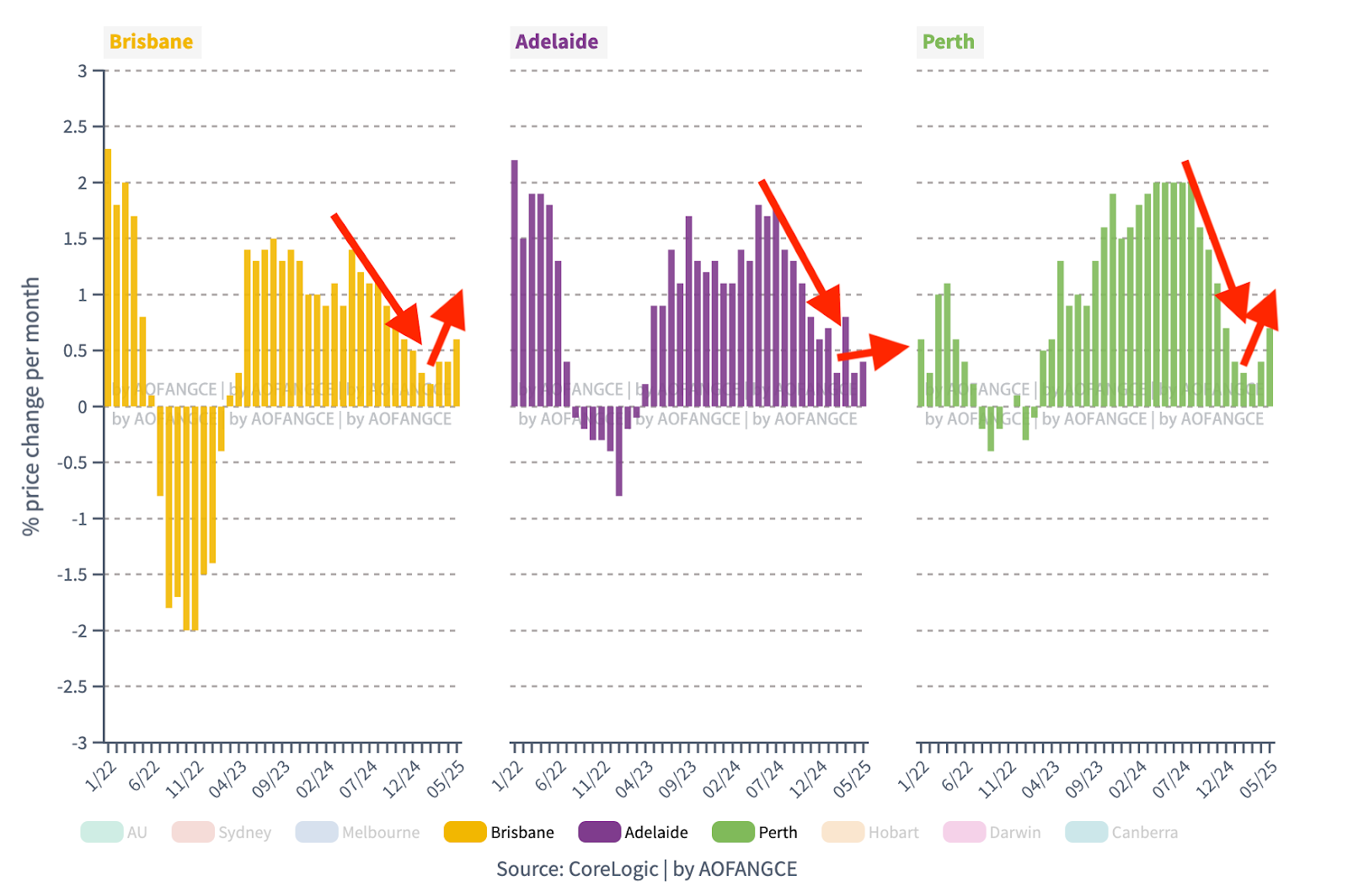

Now let's look at the three mid-sized cities—Brisbane, Adelaide, and Perth. All three have been rising steadily for over two years. While growth momentum hit a low point in February this year, prices were still rising that month. Then came three straight months of accelerating growth in March, April, and May.

In May alone, Brisbane saw a 0.6% increase—breaking through the flat line threshold, which is +-0.5%. Perth rose 0.7%. Adelaide lagged slightly at 0.4%, but the direction is clear. Brisbane and Perth have already completed a full V-shaped recovery without any period of negative growth—exactly as we predicted in our livestream five months ago. Adelaide is entering the same reversal phase now, and unless something drastic happens, it's not far behind. Many people have been asking since two years ago—when these three cities started surging—'How much longer can prices keep rising?' The underlying message is that they're scared to buy. But now it's clear: those who ignored the noise and saw the big picture made decisive moves—and likely gained 50% or more. If you're still asking, 'Can prices keep going up after all this?', then maybe property investing just isn't for you. To truly understand market trends, you have two choices: Either you do your own research and draw your own conclusions. Or you can seek help from a professional investment service like AUSPropertyStrategy. The worst thing you can do is refuse to study the market and refuse to invest with expert advice—yet still run around listening to gossip, chasing headlines, and watching those low-quality, AI-generated short videos. Look around you. How many people who failed in property investment fall into that category?

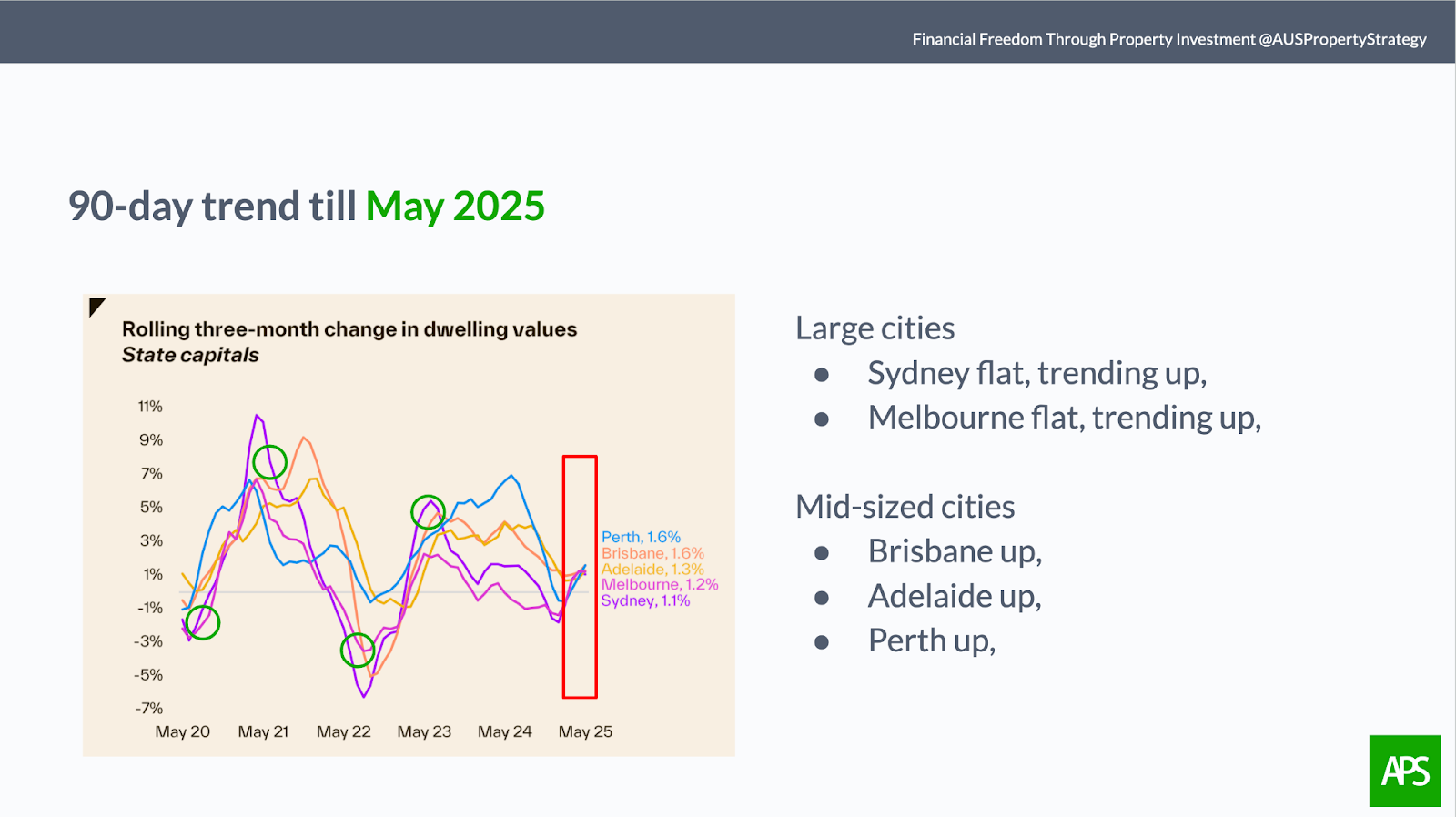

So, that's the month-on-month breakdown for each city. If you want to identify long-term trends, the best tool is the rolling 90-day price movement chart. When you stretch the view out to a quarter, the ups and downs smooth out, and the trend becomes much clearer.

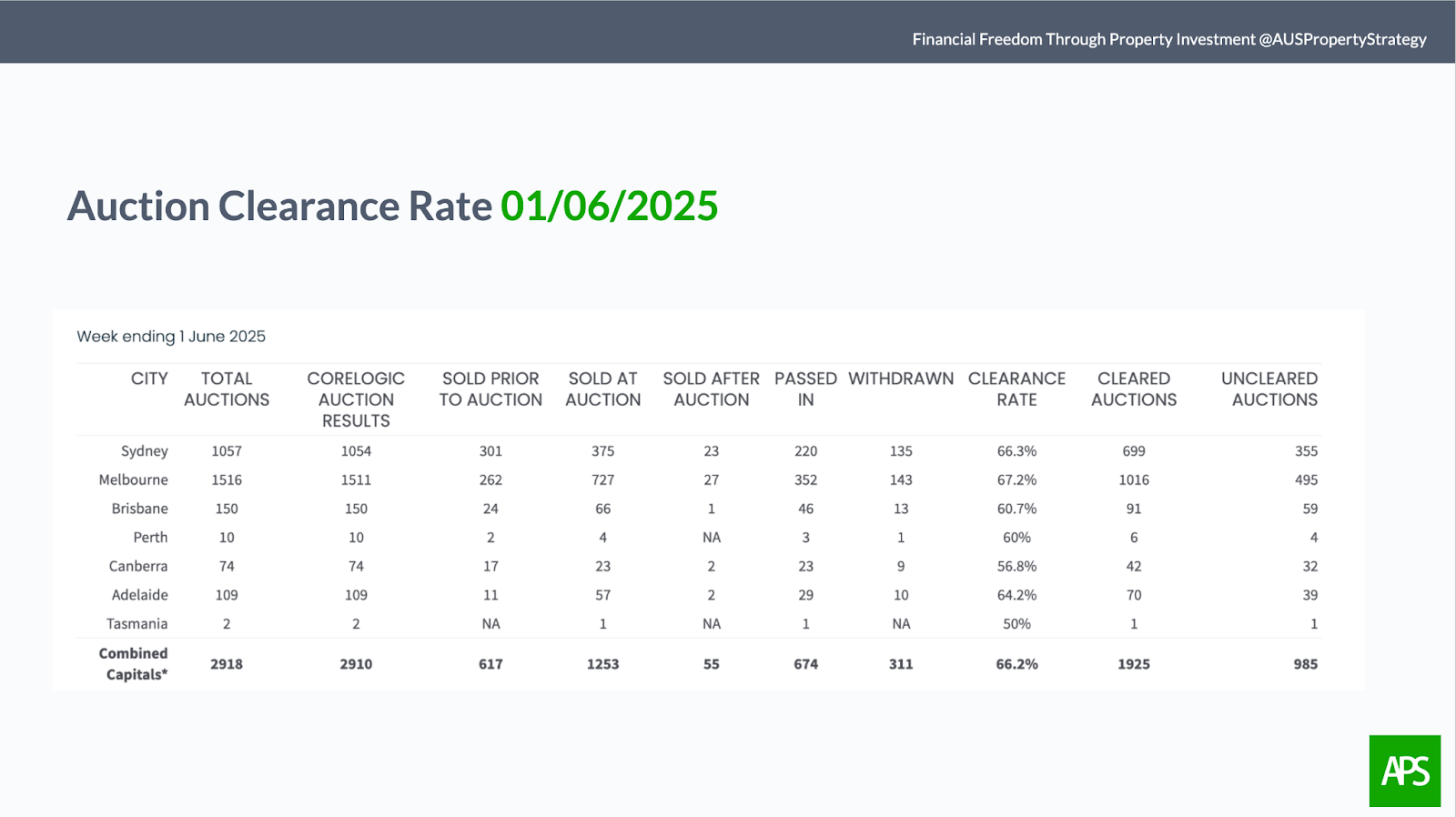

And right now, the charts show it well: both large and mid-sized cities across Australia are already in an upward cycle. Auction clearance rates in May were also impressive. The number of auctioned properties jumped by 150% compared to April, and clearance rates climbed by 6%. More volume, higher prices, stronger clearance rate—this is a classic recipe for a property boom.

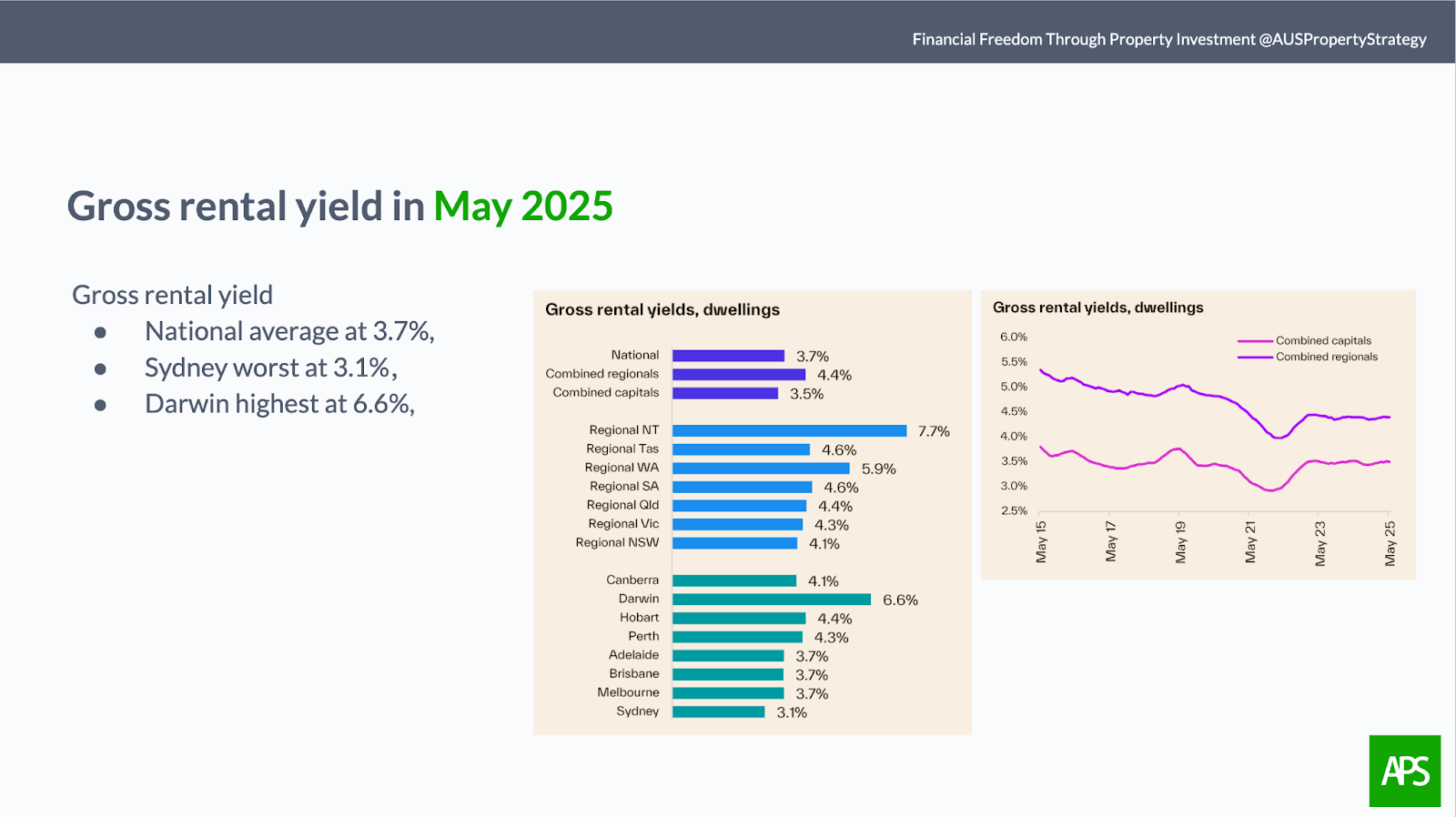

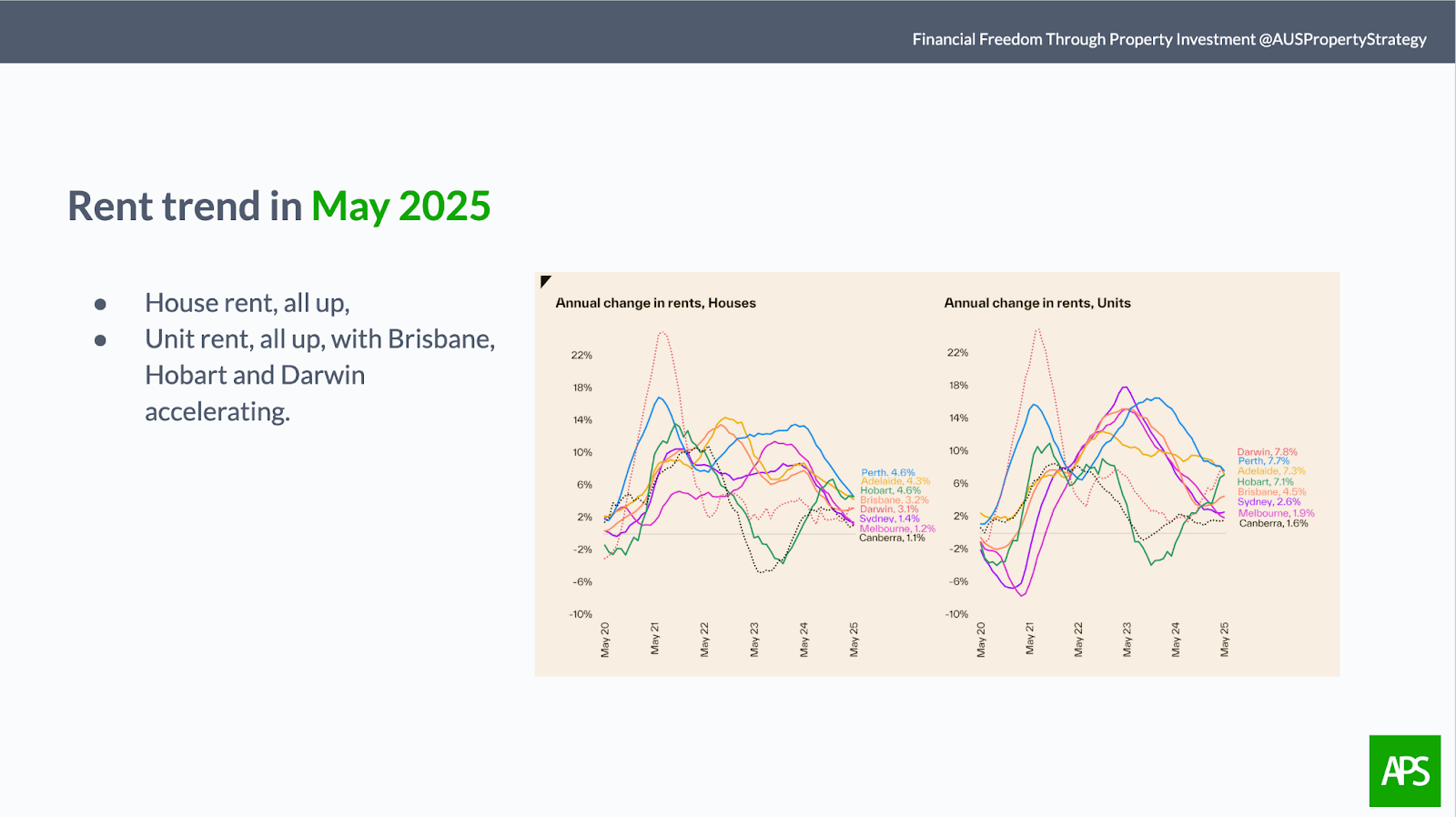

As for rental yields—there hasn't been much change. Rental yield, or the rent-to-price ratio, is calculated by dividing annual gross rent by the property price. For example, if a million-dollar property has a 3% rental yield, that means it earns $30,000 in gross rent per year. In May, the national average yield was still at around 3.7%. Sydney had the lowest yield at 3.1%—mainly due to its high property prices. The highest yield remains in Darwin at 6.6%. Adelaide, Brisbane, and Melbourne all sat around 3.7%. You might be wondering—at this yield level, is it even possible to have positive cash flow when buying a property in Australia? At current interest rates and assuming an 80% loan-to-value ratio, nearly all cities are still in negative cash flow territory. The only difference is how negative. The good news? Rents are still rising across all cities, and interest rates are expected to fall further. That means many properties could move from negative to positive cash flow over the next year. The longer you hold the property, the less financial pressure you'll feel.

But everything we've discussed so far is all that’s happening right now. Real property investing is about the long game. It's about seeing the road ahead. The clearer and farther you can see down that road, the more confidence you'll have in the decisions you're making today. So what lies ahead for Australia's economy in the near term—and what could the property market look like in the next 3 to 5 years, or even longer? Let's find out.

The Australian Economy

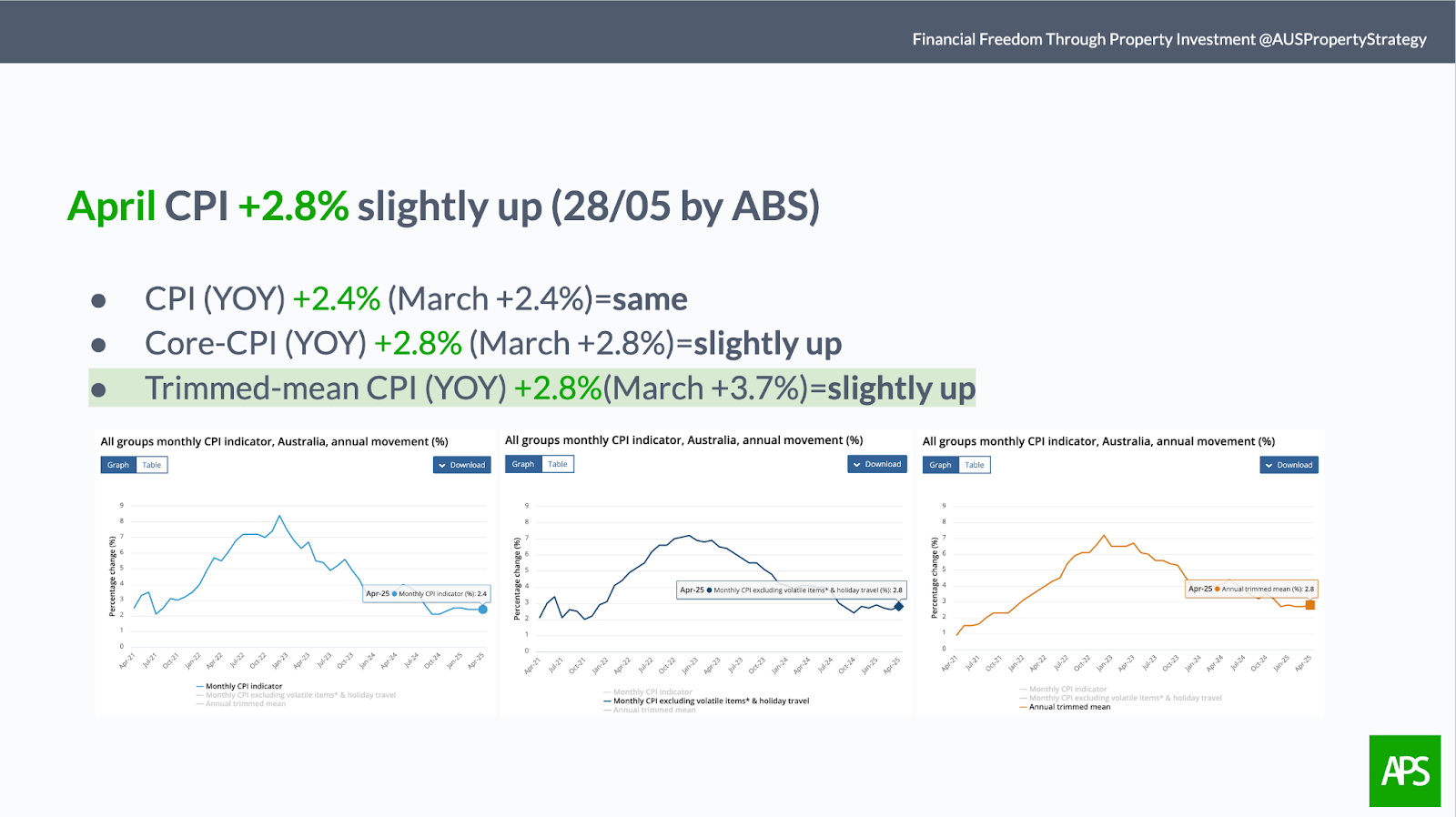

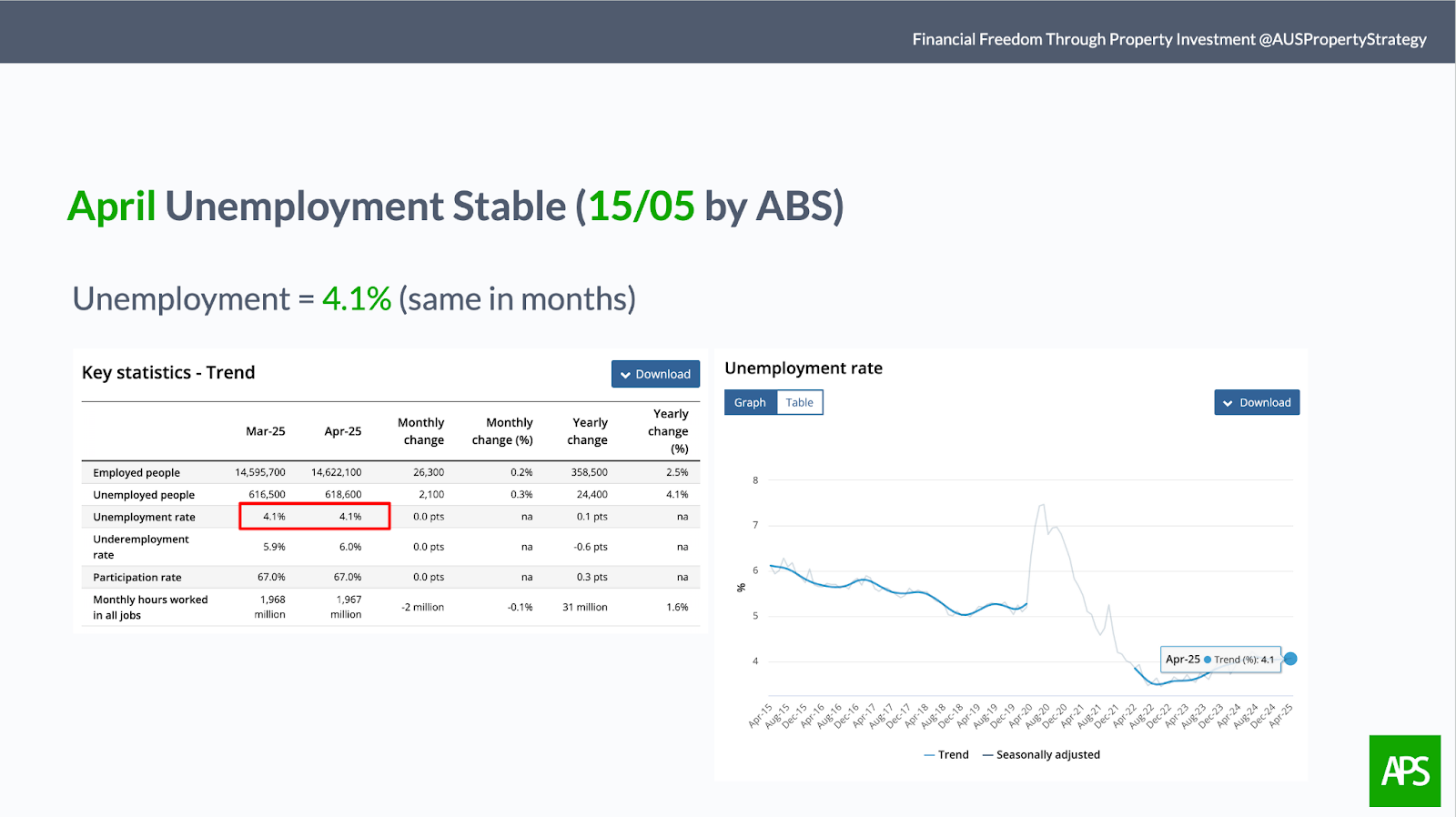

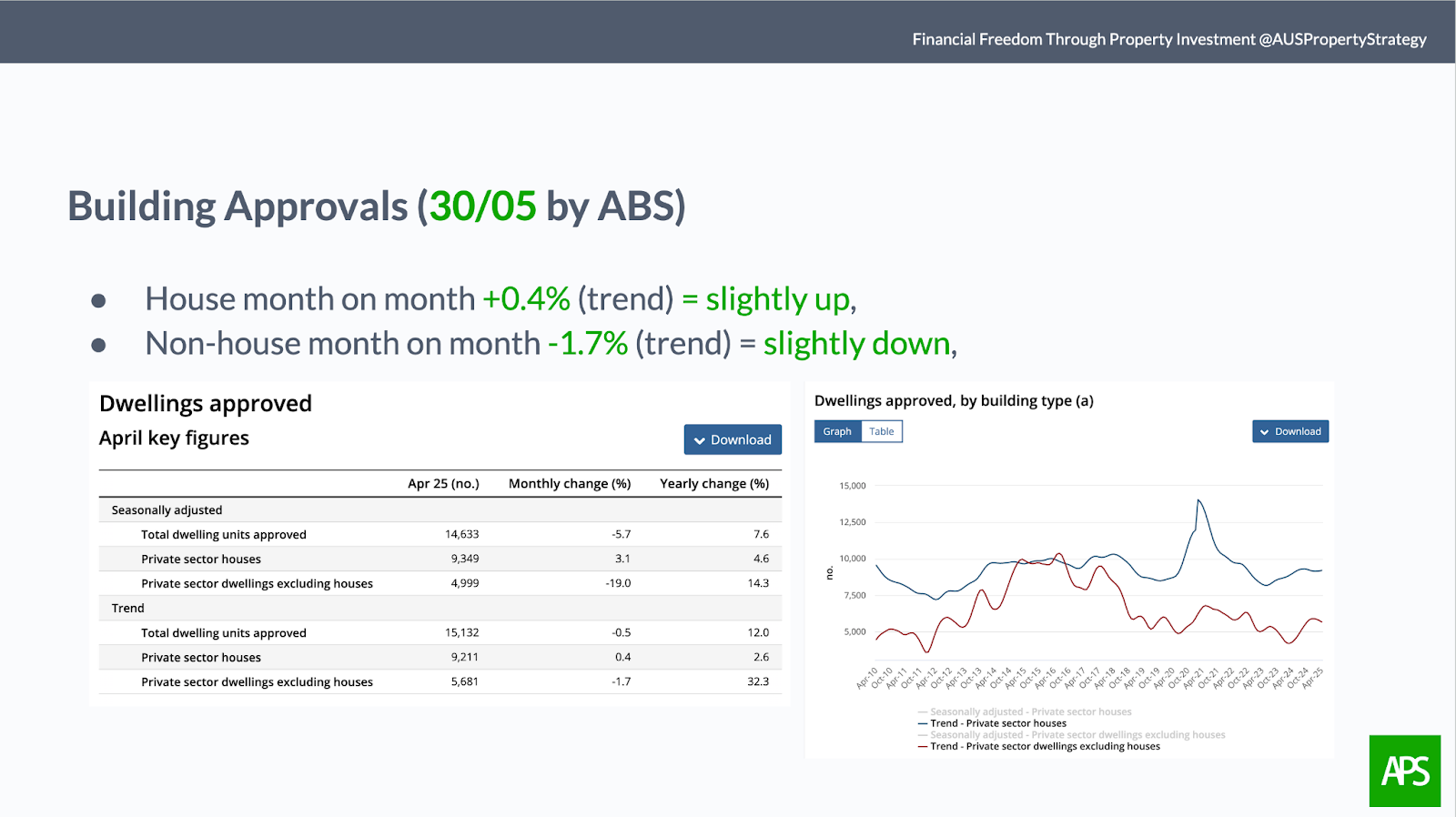

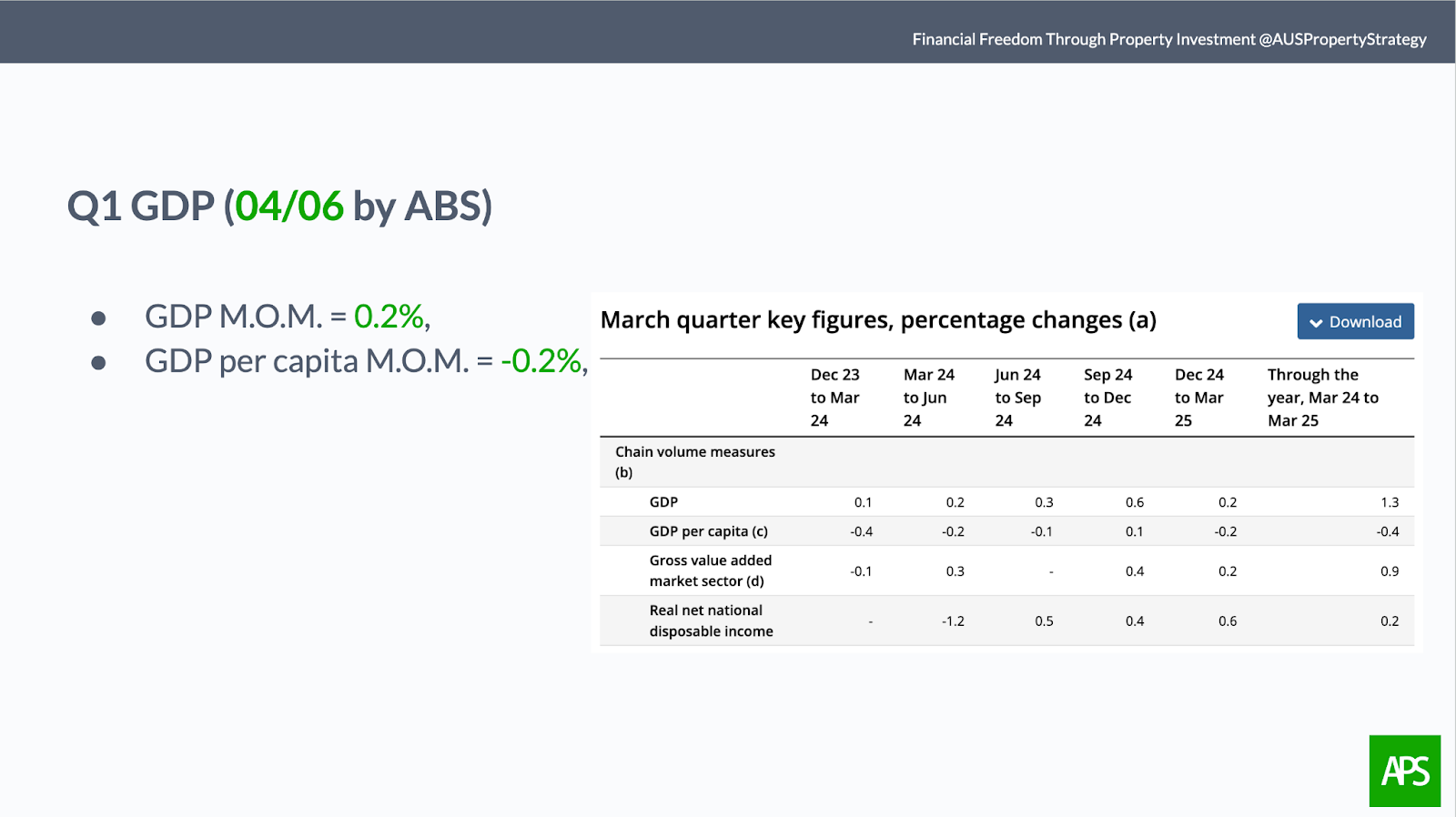

Let's take a look at the current state of the Australian economy. According to the latest report from the ABS, the trimmed-mean CPI rose by 2.8% year-on-year in April. That's slightly higher than March, but still within the RBA's 2%–3% target range. So, this won't have any impact on interest rate decisions. Construction costs did rise in April, but not by much. If the cost of building increases significantly, it will push property prices up even faster. Unemployment remains steady at 4.1%, holding that level for several months. The number of building approvals is slightly up from last month, but nowhere near enough to change the supply-demand dynamic. As for GDP, Q1 figures show a return to the long-term trend—basically flat. Quarter-on-quarter, GDP rose 0.2%, while per capita GDP actually fell by -0.2%. Put all these numbers together and they tell a clear story: The Australian economy is in a stable flatline.

The Reserve Bank of Australia has two key mandates:

1.Keep inflation between 2% and 3%. If it's too low, stimulate. If it's too high, tighten. 2.Maintain stable employment. And right now, with unemployment holding at 4.1% for months, there's no issue there at all. So, will the RBA cut rates? The answer is yes—definitely. There are two reasons: First, to stimulate growth and speed up the economy. Second, to reduce government borrowing costs. Right now, the Australian government is pulling every lever to increase tax revenue and raise funds through bond issuance to cover its budget deficit. But borrowing money means you eventually have to pay it back. Before bonds mature, new ones must be issued to cover the repayment. In that situation, low interest rates are critical. High rates mean even more stress just to cover interest repayments.

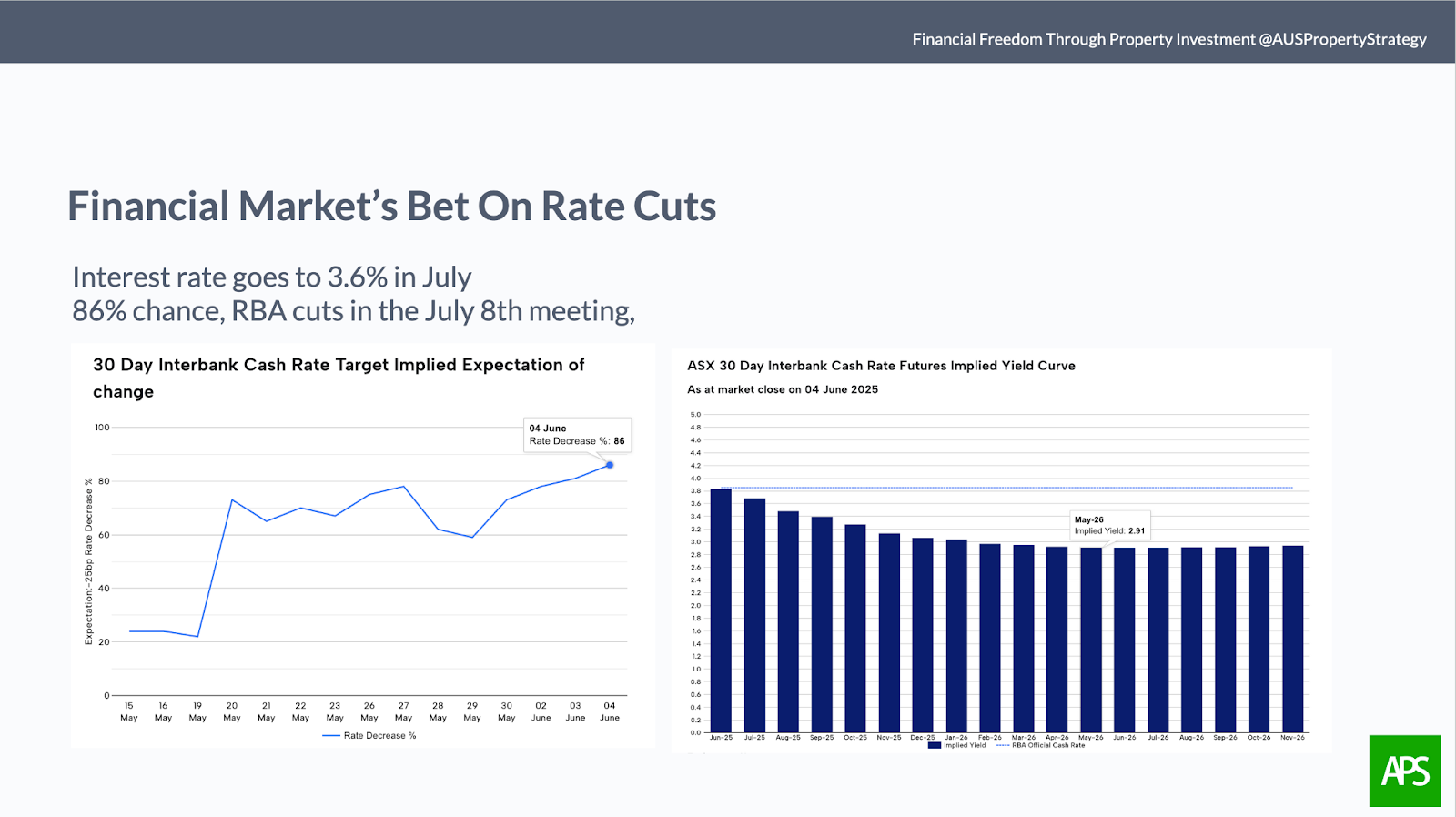

As it stands, the Australian financial market has priced in an 86% probability that the RBA will cut rates at its July 8 meeting—almost a done deal. Most economists forecast that the RBA will cut rates 3 to 4 times in the next 12 months, totalling between 0.75% and 1%. Meanwhile, Australian consumer confidence rose 2 percentage points in May, reaching a level of 92. All of this points to one conclusion: The direction of the Australian housing market is now highly certain, and we're heading into a stable price growth cycle that will likely last for at least 12 to 18 months.

Now, some of you might still be asking: 'Should I buy property now?' If you've watched any of my market updates in the past 6 months, you'll know I always say the same thing—and this time is no different:

If you're buying a home to live in, timing doesn't matter. You'll be living there for 10 or 20 years. What matters is whether the property suits your life—your commute, shopping, groceries, kids' schools—not market timing.

If you're buying for investment, you must think long-term—10 to 20 years. Whether you time it perfectly or not doesn't matter. What matters is how long you hold it. That's what determines whether you make money in the end.

If your goal is to profit from long-term capital growth, to generate steady wealth with the right tax strategy and asset allocation, then it really doesn't matter which major or mid-sized city you buy in. What matters is how well your portfolio is structured to align with your personal financial plan.

But—if you're the type who wants to catch the next boom, who's looking for a timing opportunity—well, now is that moment.

If you don't know where to buy or what kind of property to buy, it's simple: Join our VISION Membership and let us help you build your investment portfolio.

Sure, some haters will say: "Of course, you're saying the market is good—you're in the property business! You make money when people buy houses!" But AusPropertyStrategy has always told it like it is. We call the market based on facts. Go check our past videos—you'll find we've also predicted downturns before.

Think about it—what fast track to wealth is there for the average Aussie? If you're a university graduate, a starting salary of $55,000–$60,000 is considered normal. That's just enough to survive. After two years, if you're earning $80,000, you can afford the occasional dinner out or a short holiday. Making over $100,000 is already rare. In big companies—like banks, insurers, or large corporations—you might get to $170K–$180K after 10 years. But then comes the tax bill. Once you calculate, there's not much left.

Running your own business? Unless you're building the next Airwallex or Canva, big money is out of reach. Most people buy themselves a job—covering shifts when the chef or wait staff are off. A whole year of grinding, and there's barely any profit. So, after all that, what's left? Property. That's the one path to wealth that still works for ordinary Australians. Whether you accept it or not, whether you like it or not, that fact doesn't change.

Will Prices Fall in the Next 5 Years?

So, will prices fall in the next 5 years? In the short term, sure—prices can go up or down. But in the long run, Australian property always trends upward. Even if there's a 3-month dip within a 5-year period, if the rest of the time it's rising—would you still buy? What if prices fall 5% briefly but rise 50% over 5 years—would you still buy? The doomsayers might say, "See, I told you!" during short-term dips. But in the long run, it's those who stay positive—and stay invested, reap the real rewards.

Five years ago, when my other property investment firm was just starting out, a couple joined our VISION Membership. They were among our very first members. During the pandemic, they moved from Sydney to work at a mine in Perth. They had a home of their own and three investment properties. You could say they were doing alright financially. But those three investment properties were all losing money. They didn't have time to deal with them. Instead, they just worked harder to cover the losses. They had been laid off by a Sydney-based company during COVID—moving to Perth was out of necessity, not choice.

Over the past five years, we helped them sell off those underperforming investments and gradually acquire five new properties in different states across Australia. Just a few days ago, we held their annual portfolio review. Result? Over $3 million AUD in capital gains over these few years. And their cash flow is now positive—thanks to three of their properties being managed by our own short-term rental company. Six months ago, both husband and wife quit their jobs. Mining work was never about passion—just survival. Now, they're financially free. He travels, takes photos, and writes novels. She runs a small bakery and lives a life she loves. Every time I visit Perth, she brings me fresh handmade bread and pastries. This is what we've always been talking about at AusPropertyStrategy, Financial Freedom, Retirement Freedom and Travel Freedom.

And if you start your property investment journey now, then five years from today, you might be the one thanking your present-day self.

Watch the video version of the blog on YouTube.