New Zealand Housing Market Just Collapsed. Is Australia on the Same Path? [APS084]

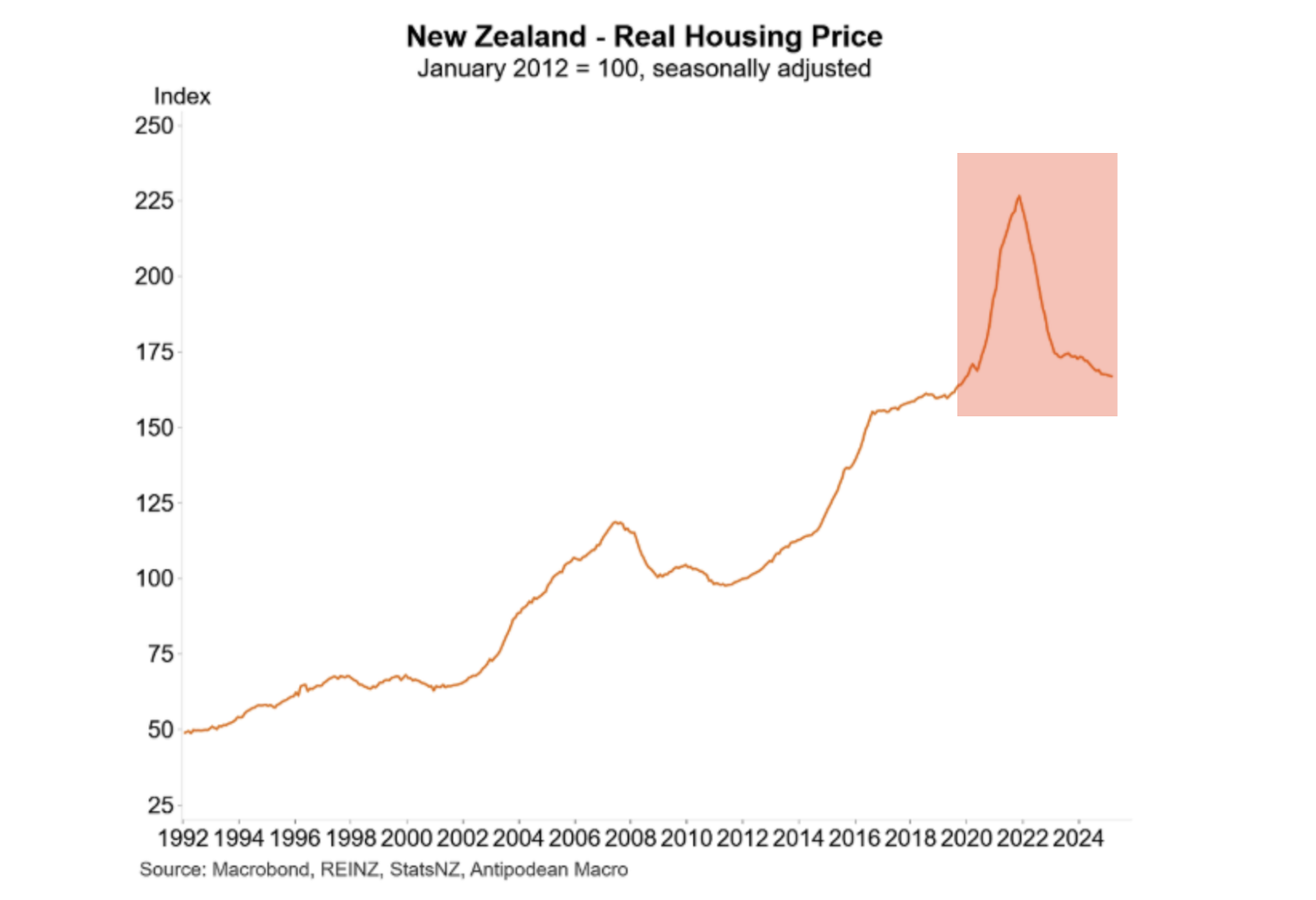

Following the pandemic, New Zealand experienced the fastest surge in housing prices in the world. At its peak, prices in some areas were rising as much as 30% in a year. But after reaching that high, prices have been falling. And as of the time we publish this video, property prices have already fallen back to pre-pandemic levels — and the downtrend hasn't stopped. In other words, it's been a five-year rollercoaster. A wild ride that ended in disappointment. What's more worrying is this — despite multiple interest rate cuts, there's still no sign of a recovery in the market. Many people are now starting to get nervous, especially after seeing property prices in Australia begin to rise again. They're wondering: could Australia suffer the same fate as New Zealand? Will cutting interest rates actually lead to a sustained price rise? And, of course, there are always those pessimists who have long believed the Australian market is doomed to repeat New Zealand's downfall.

To get to the bottom of this, I spent more than a dozen hours digging through data, reading reports, and researching trends. In the process, I discovered something — a key factor that most people have completely overlooked. And this, I believe, is the one crucial element that will determine whether Australia and New Zealand truly share the same destiny in property.

A Rollercoaster Ride

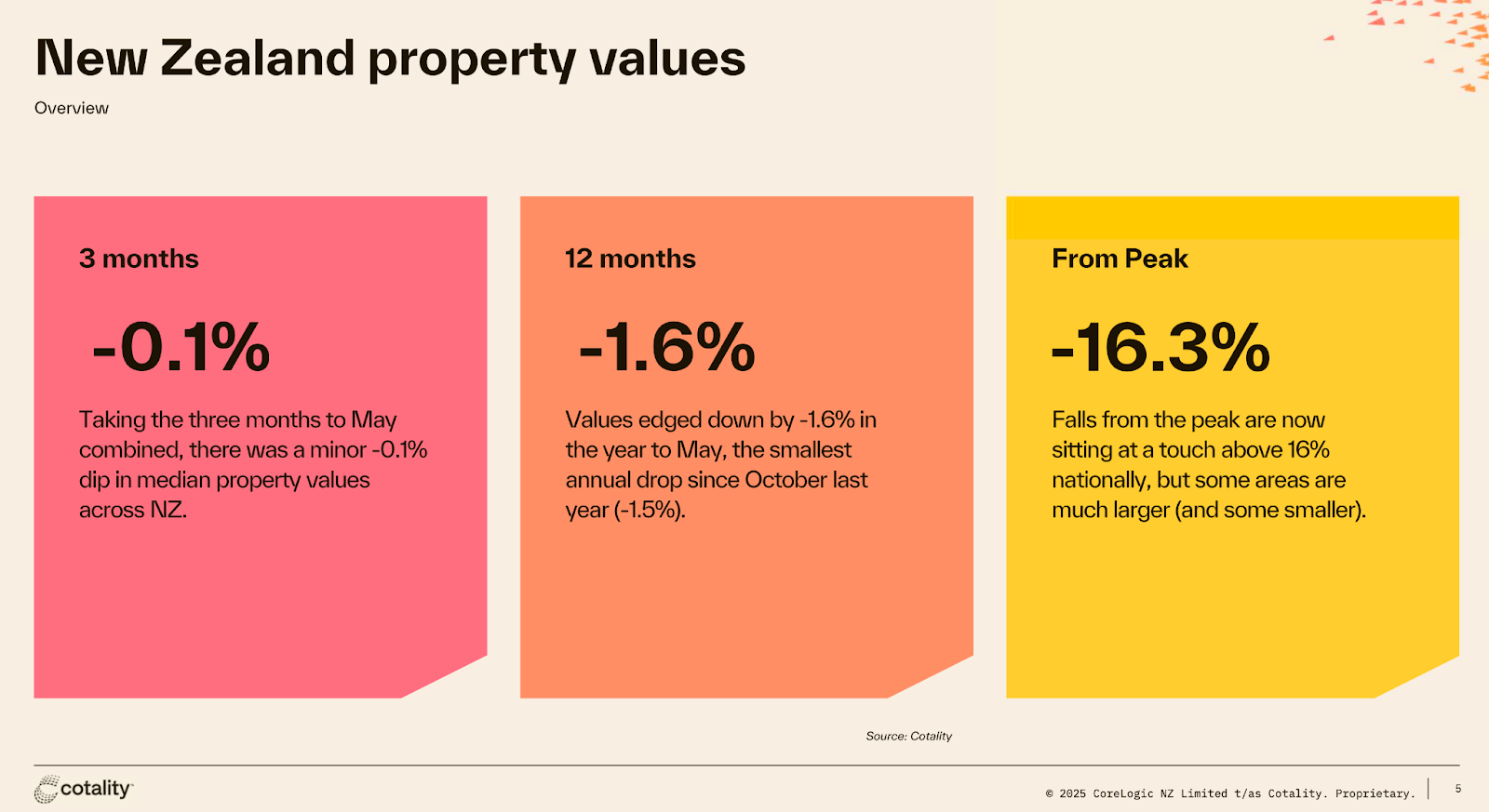

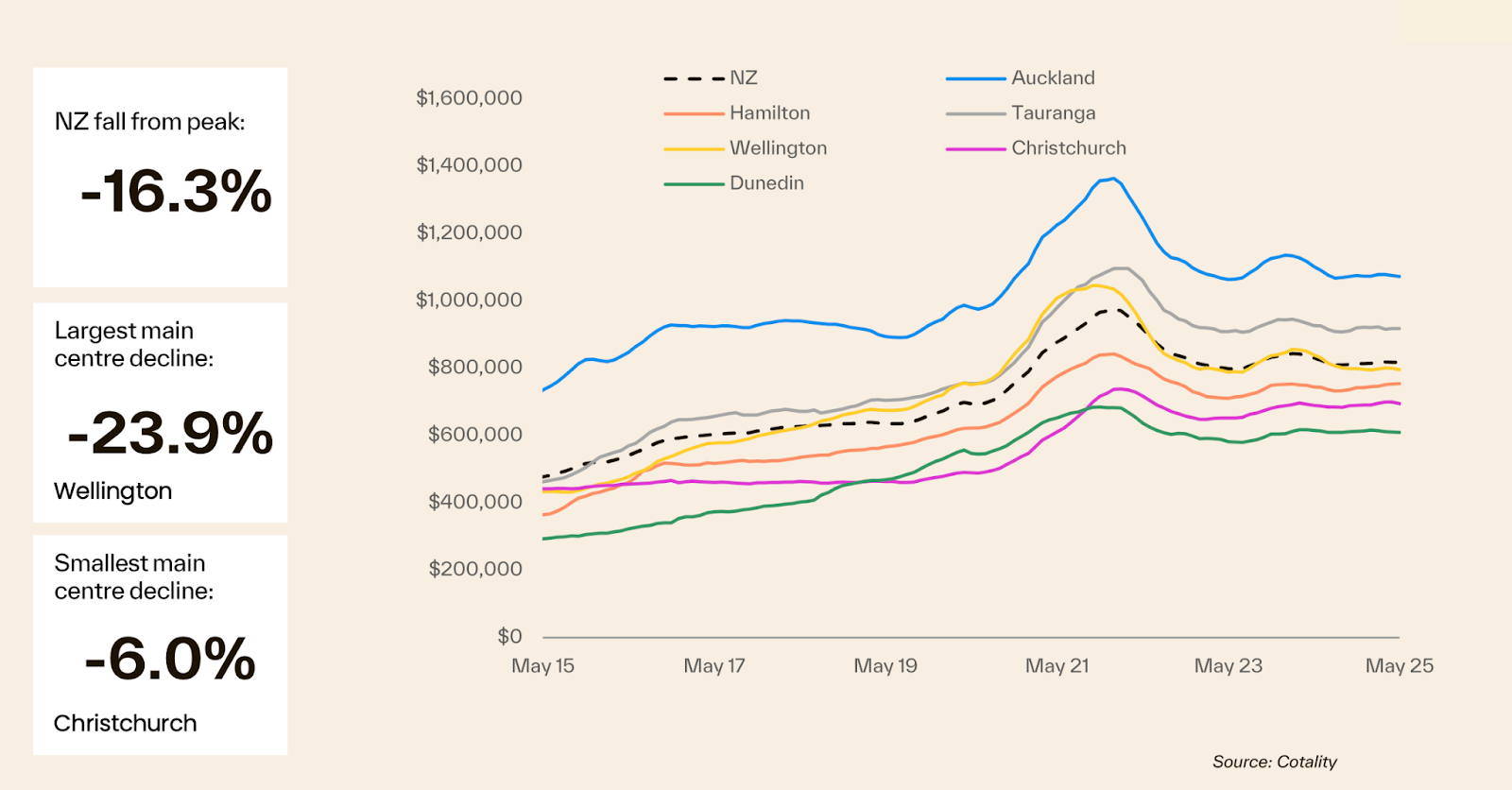

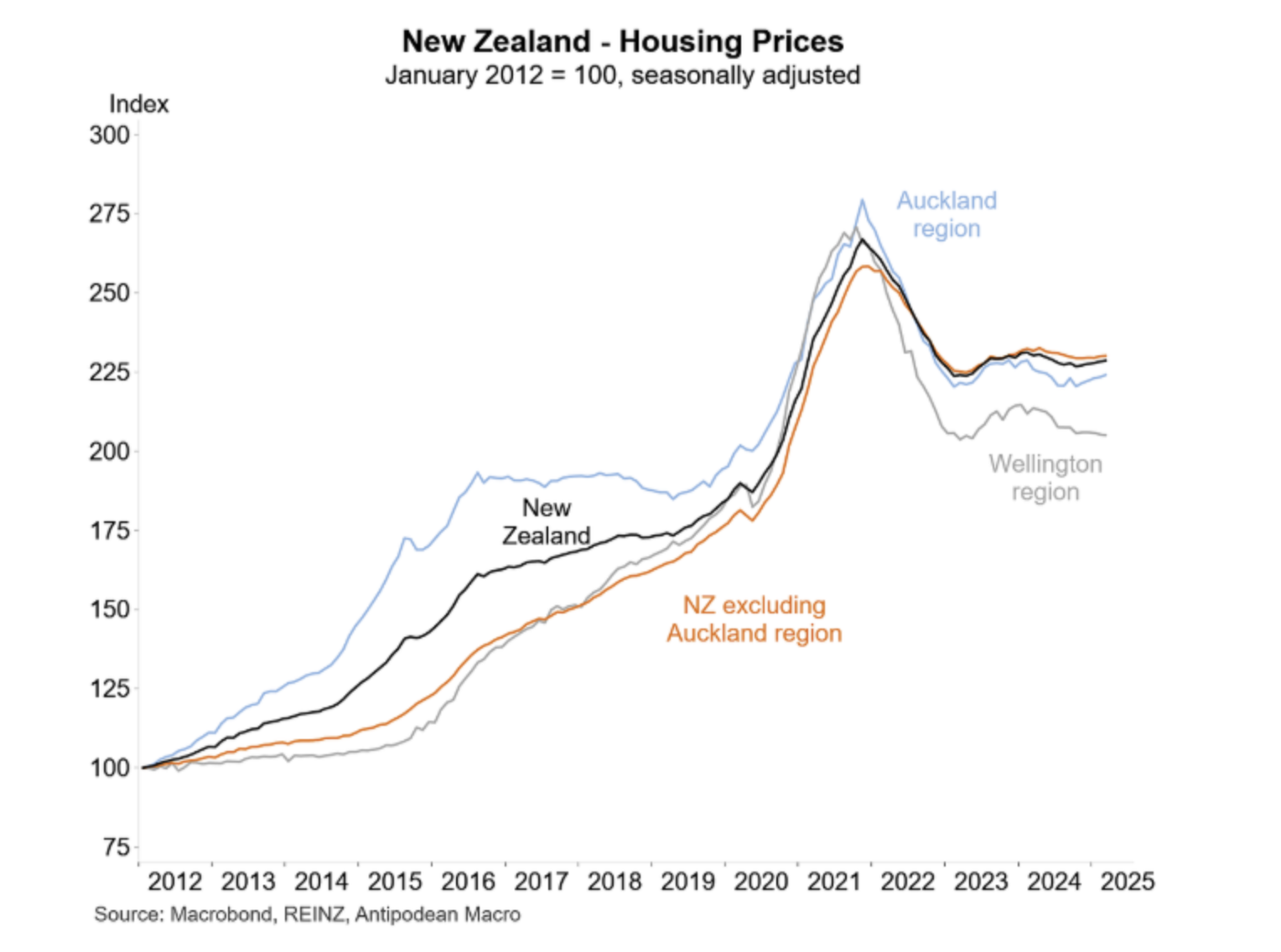

Let's get straight to the point. As of the end of May 2025, New Zealand's national property price index has fallen by 16.3% from its pandemic-era peak. Of course, different cities saw different levels of decline. Wellington took the biggest hit, with a sharp drop of 23.9%. Christchurch held up better, with a more modest fall of just 6%. However, across the board, every city's housing price is now lower than the peak reached during the pandemic.

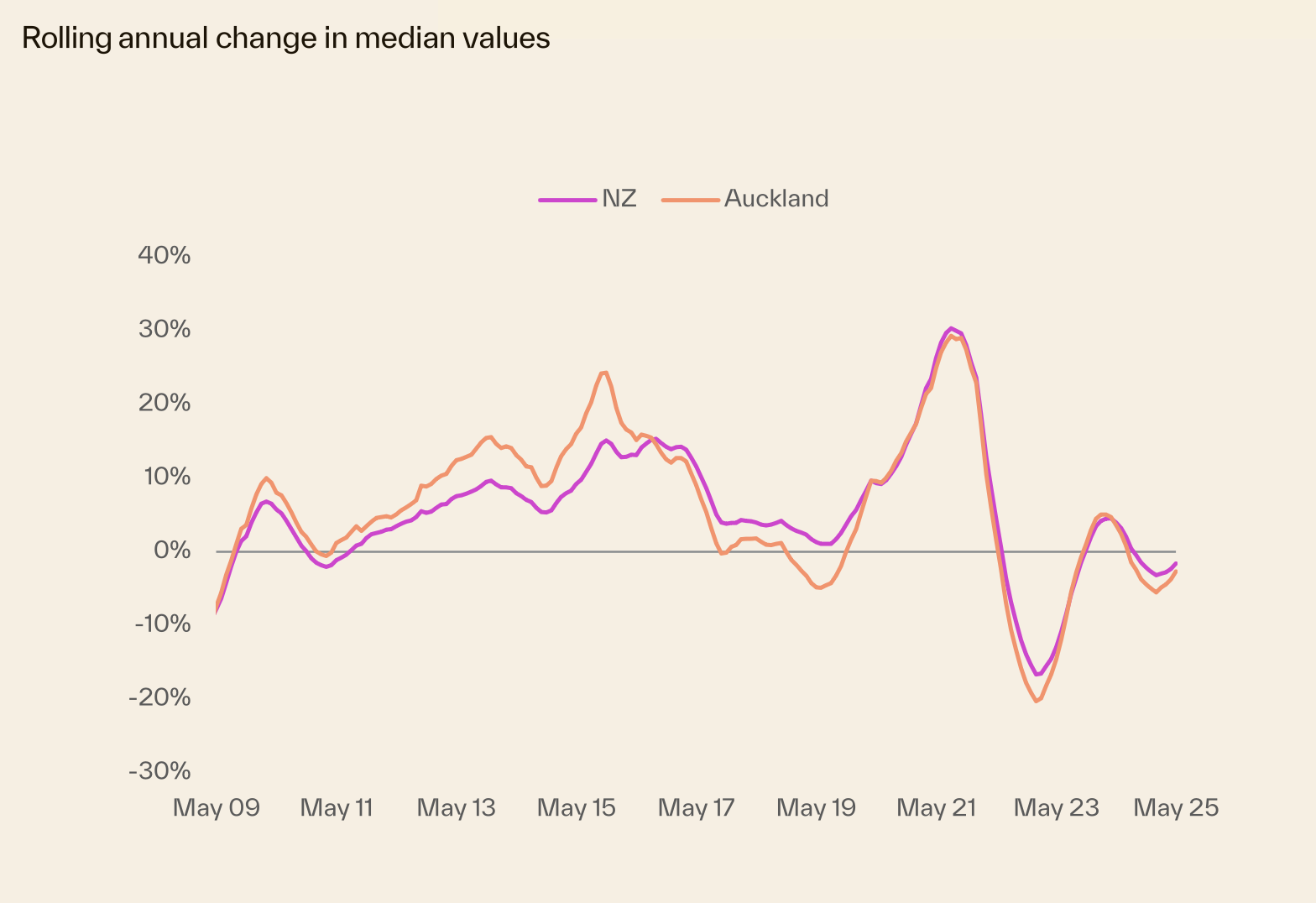

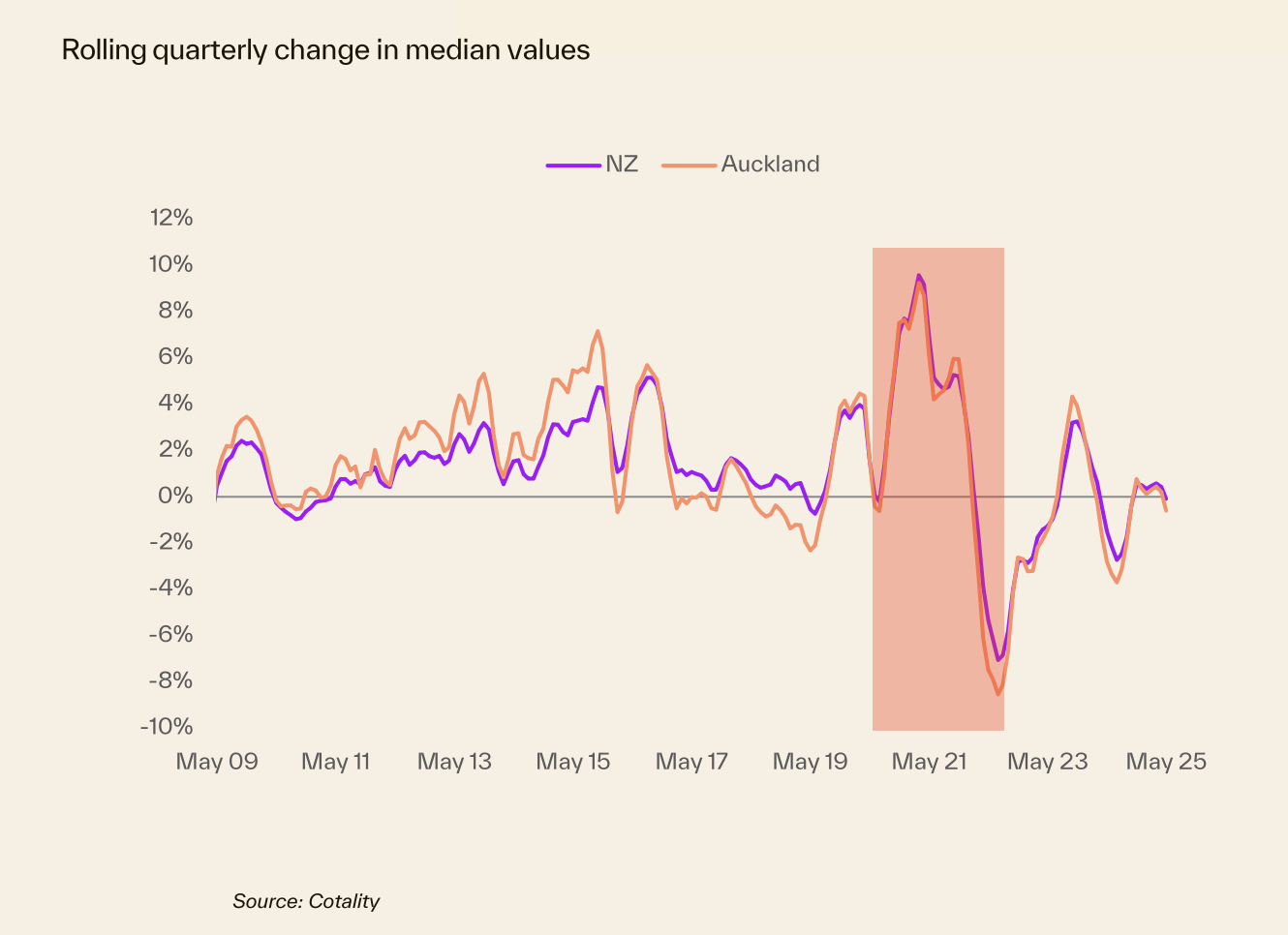

When we look at the annual trend chart, it becomes very clear — the national price trend closely mirrors Auckland's performance. And that's not surprising since Auckland makes up around 30% of New Zealand's entire housing market.

Prices began to rise gradually after the pandemic started in 2020. Around May 2021, the market reached a peak in growth, with annual price increases as high as 30%. But after that, the rate of growth started to slow. By around October 2021, the market had entered a downward phase. By April 2023, the annual price drop had reached nearly 20%. Frankly, calling this a boom-and-bust cycle isn't an exaggeration at all. After that, the decline eased somewhat. There was a slight rebound from late 2023 into early 2024 — but it didn't last. The market then slipped back into another downtrend, which continues to this day.

Now, let's compare that to Australia. From the early days of the pandemic through to October 2024, Australia's trend was similar to New Zealand's. But the actual price movement tells a very different story. At its highest, Australia's national housing market saw annual growth of around 25%. The largest annual decline? Only about 7%. In other words, the upswing was comparable to New Zealand's — but the downturn was only a third as steep. After re-entering an upward trend in early 2024, Australia's housing prices have been rising steadily ever since. Meanwhile, New Zealand has fallen back into decline.

So, over these five years, here's the result: Australia's housing market has gained 43% in value. New Zealand's market? It's back to where it started before the pandemic. You could say — the wealth came fast but vanished even faster. Five years of effort, and it ended up being a fruitless ride.

Now, here's the real question: Two neighbouring countries with similar cultures and deeply connected economies...Why did their property markets take such dramatically different paths?

1. Housing Affordability

Let's start with housing affordability. Since 2022, New Zealand has been in a prolonged phase of deflating its property bubble — and it's still not over. Why? Because housing prices soared too high in the first two years of the pandemic.

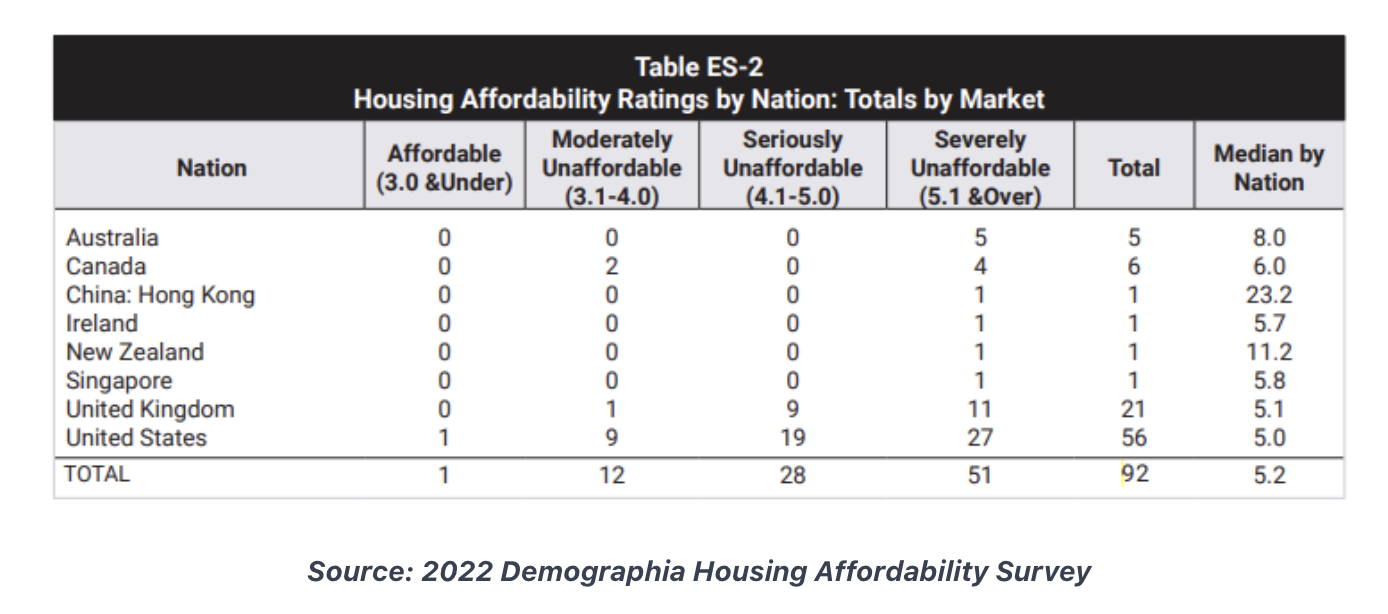

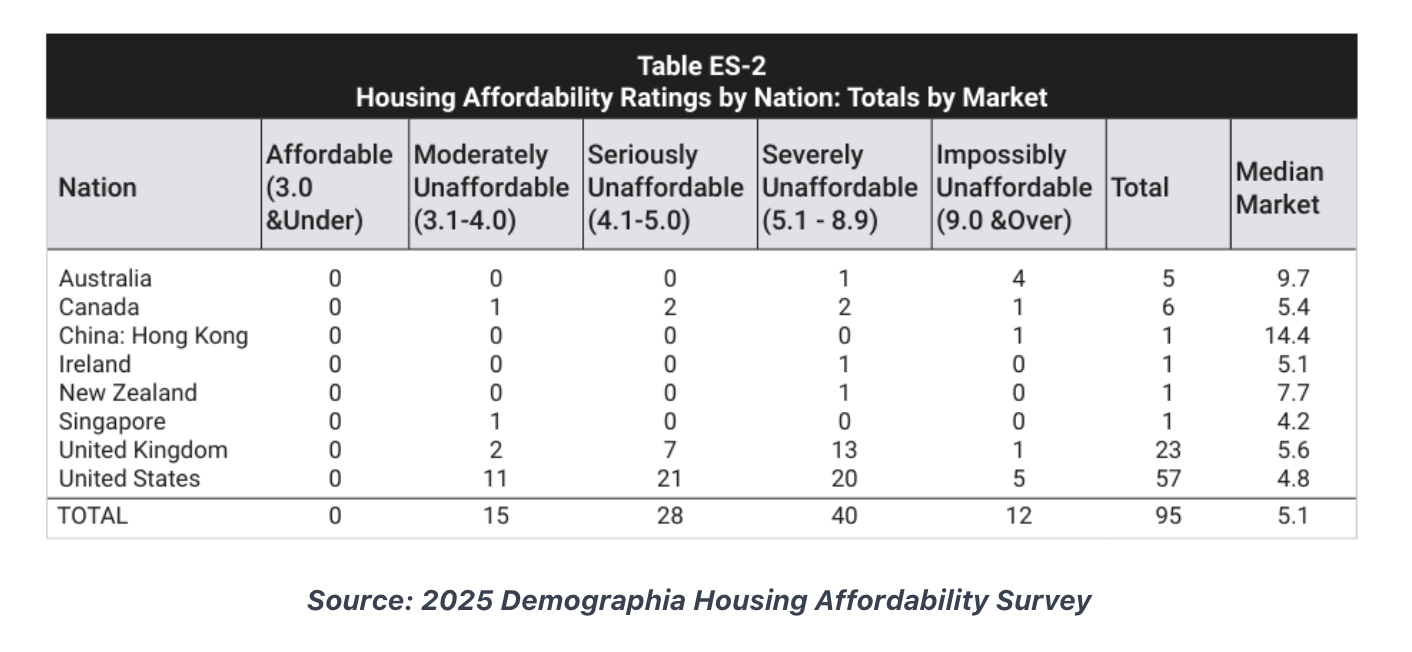

According to surveys, by 2022, the median house price in New Zealand was 11.2 times the median household income — the second highest in the world, right after Hong Kong at 23.2 times. At the time, the ratio in Australia was 8, in Canada, it was 6, and in the U.S., just 5.

Now, with prices having come down, by 2025 New Zealand's house price-to-income ratio has dropped to 7.7 times, ranking third globally. Hong Kong is still at the top with 14.4 times, followed by Australia at 9.7, Canada at 5.4, and the U.S. at 4.8.

So, looking purely at the numbers, housing in Hong Kong, Canada, the U.S., and New Zealand has become relatively more affordable over the past three years — meaning prices have fallen relative to income. But in Australia, homes have actually become less affordable — prices have outpaced incomes.

And here's the paradox: even though New Zealand's homes are now cheaper relative to income, people still can't afford them. Meanwhile, in Australia, homes are getting more expensive — yet people seem more willing to buy. So, what's going on here?

2. Mortgage Rates

During the pandemic, countries worldwide experienced severe inflation. To combat it, central banks entered into aggressive interest rate hiking cycles.

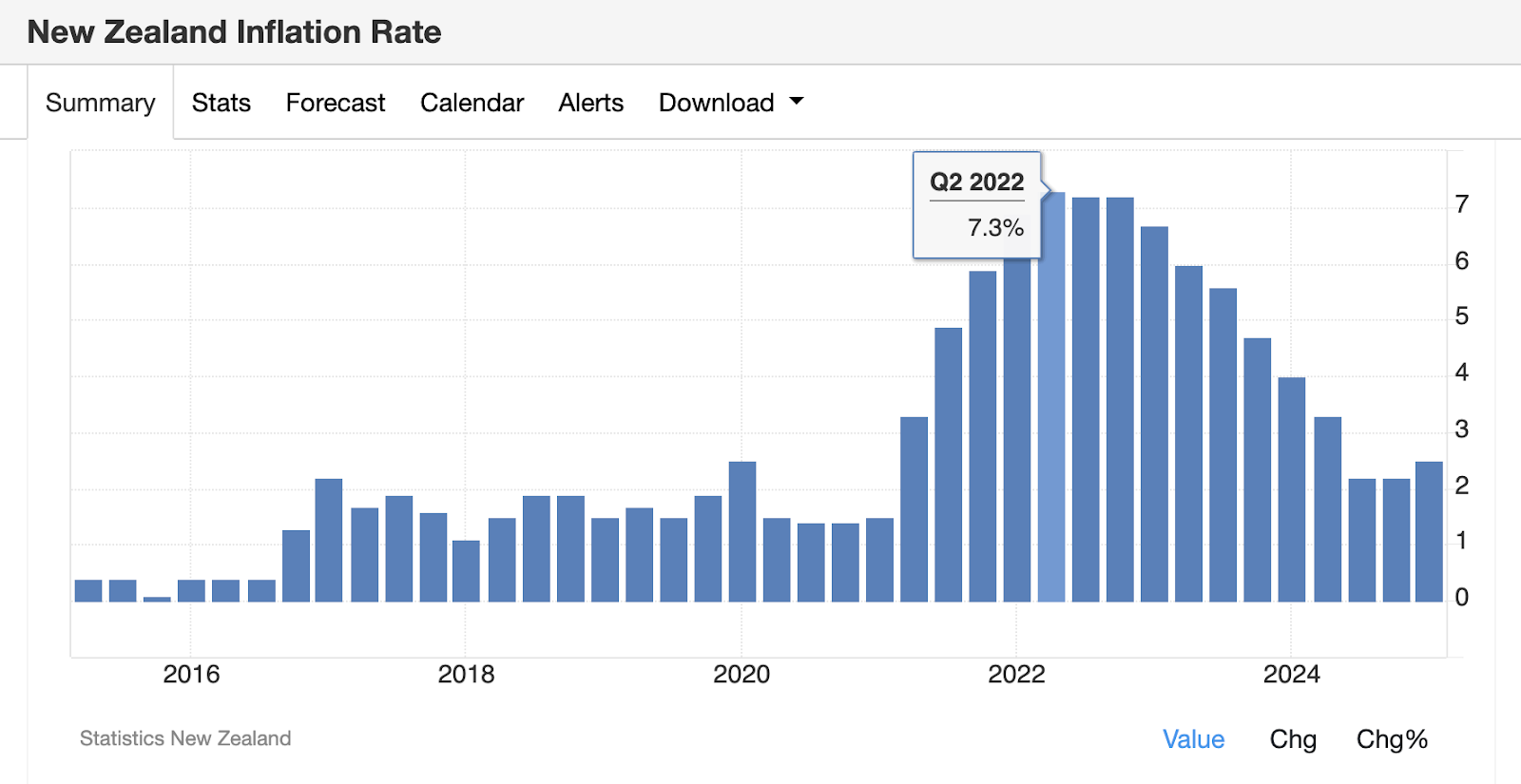

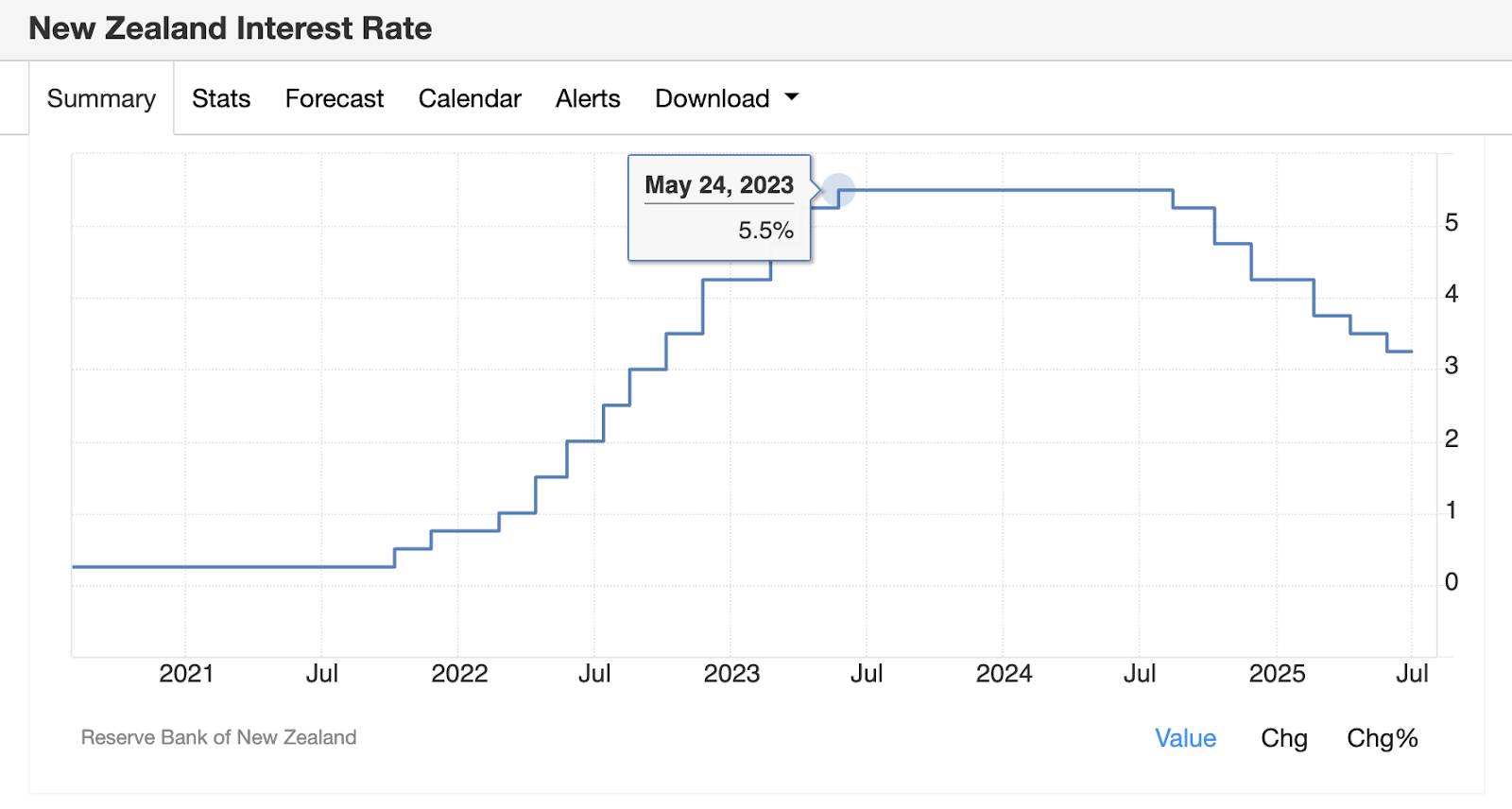

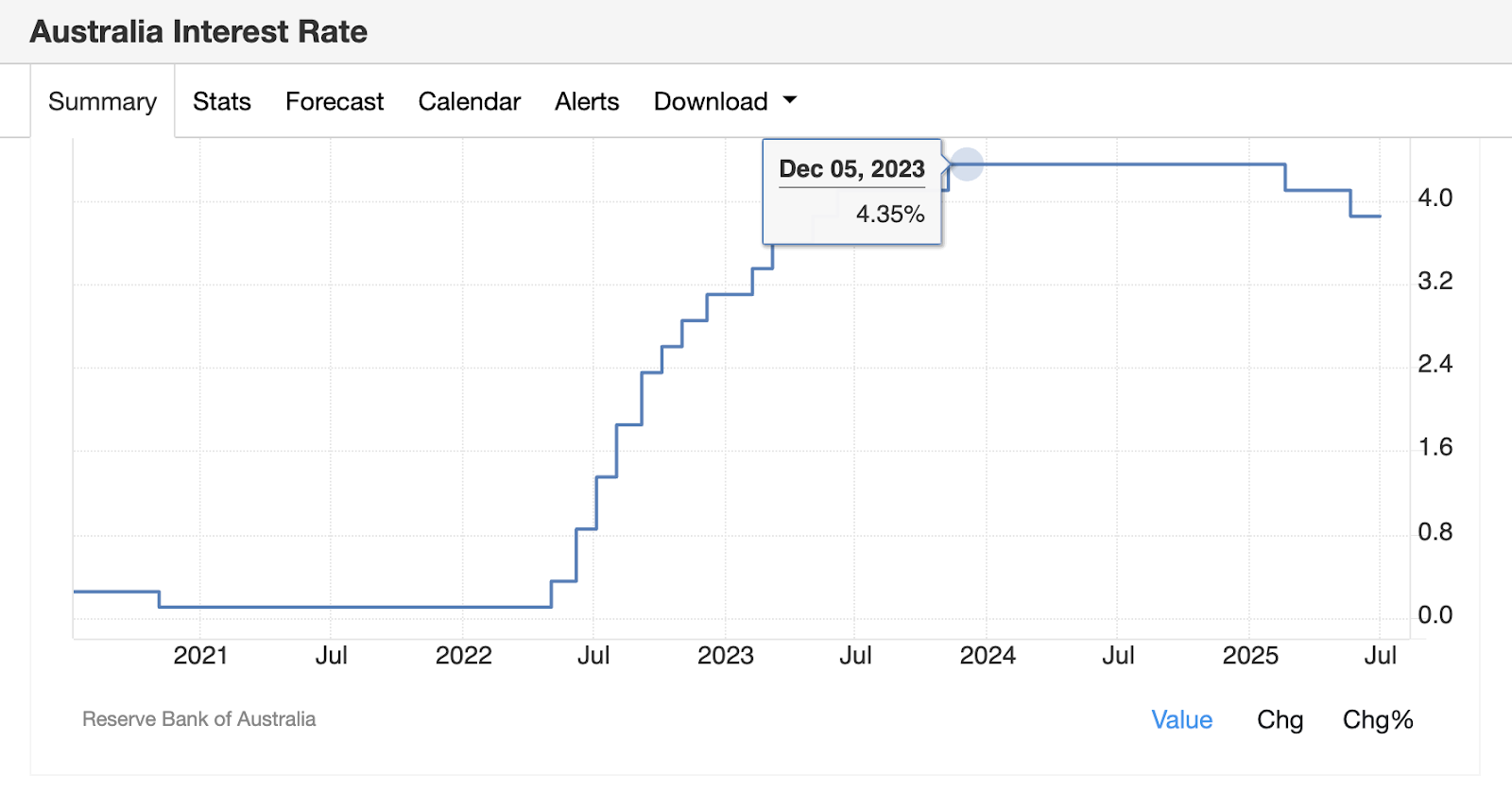

New Zealand's peak inflation hit 7.3%. Australia? Slightly higher at 7.8%. But the Reserve Bank of New Zealand pushed rates all the way to 5.5%, while Australia's cash rate only reached 4.35%. In other words, New Zealand hiked more aggressively — and kept rates higher for longer.

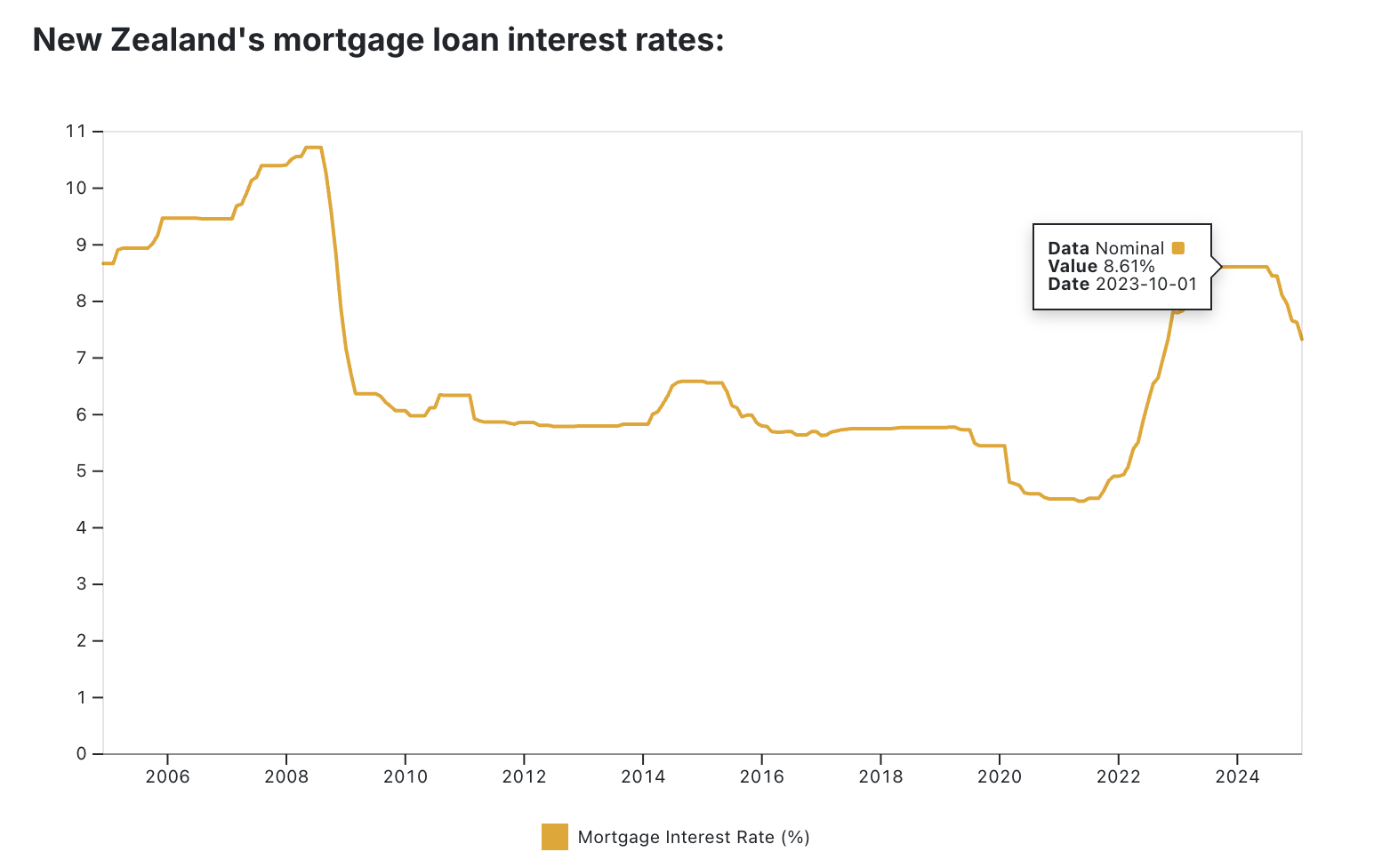

Mortgage rates followed suit. At one point, New Zealand's average mortgage rate hit 8.6%. At that rate, the only people who could still afford to buy were those borrowing very little and paying mostly in cash. But how many people actually have that much cash lying around? In contrast, Australia's mortgage rates peaked at 6.4%. This difference in borrowing costs is a major reason why New Zealand's housing market fell harder than Australia's.

3. Unemployment Rate

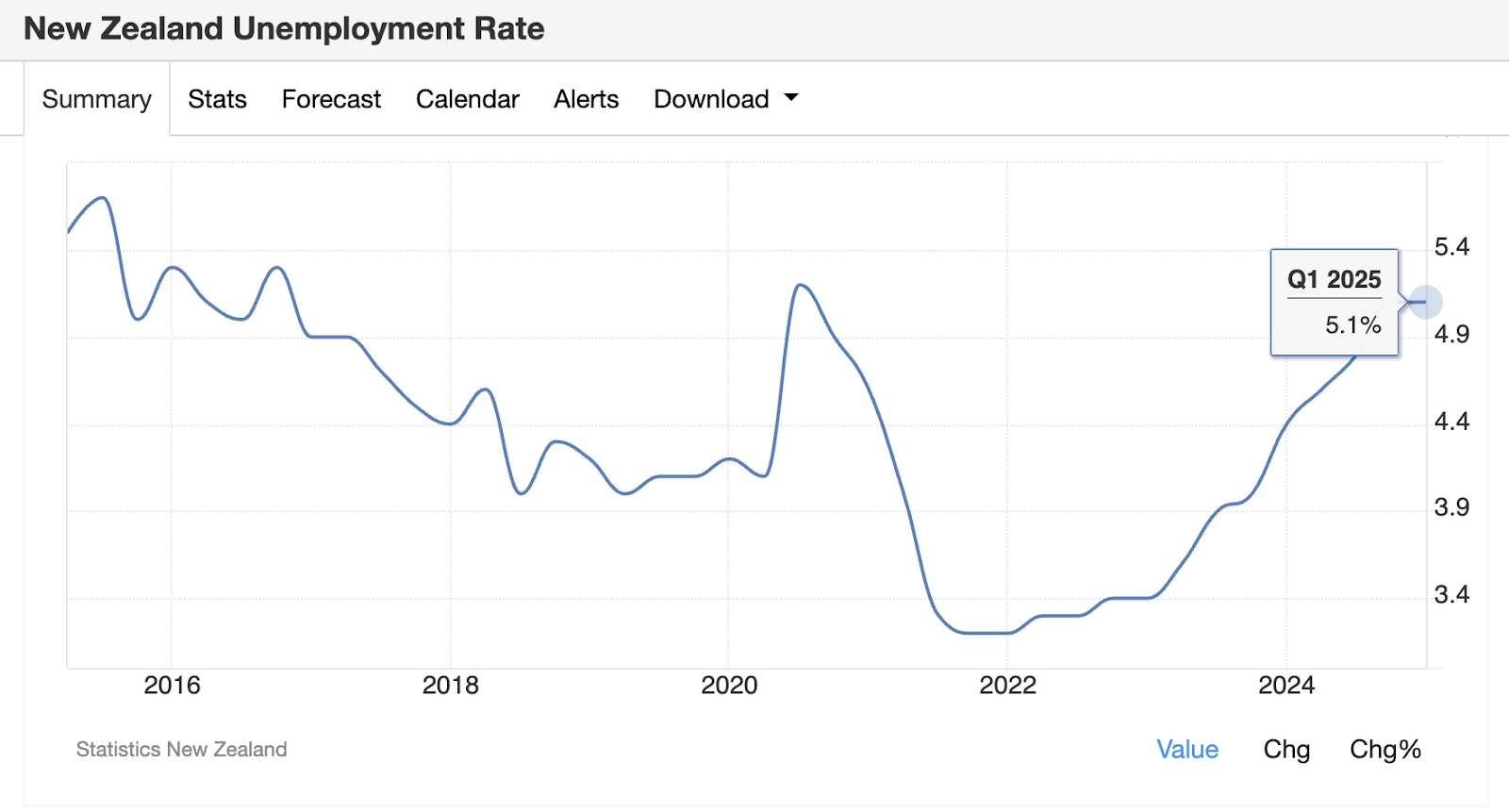

Another key indicator of economic health — and whether people can earn a living — is unemployment. At the start of the pandemic, New Zealand's unemployment rate spiked to 5.3%. After the government stimulus, it dropped to around 3.3%. However, from 2022 to the present, it has been climbing steadily — reaching 5.1%, almost back to the pandemic's worst levels. That gives you an idea of how bad New Zealand's job market is right now.

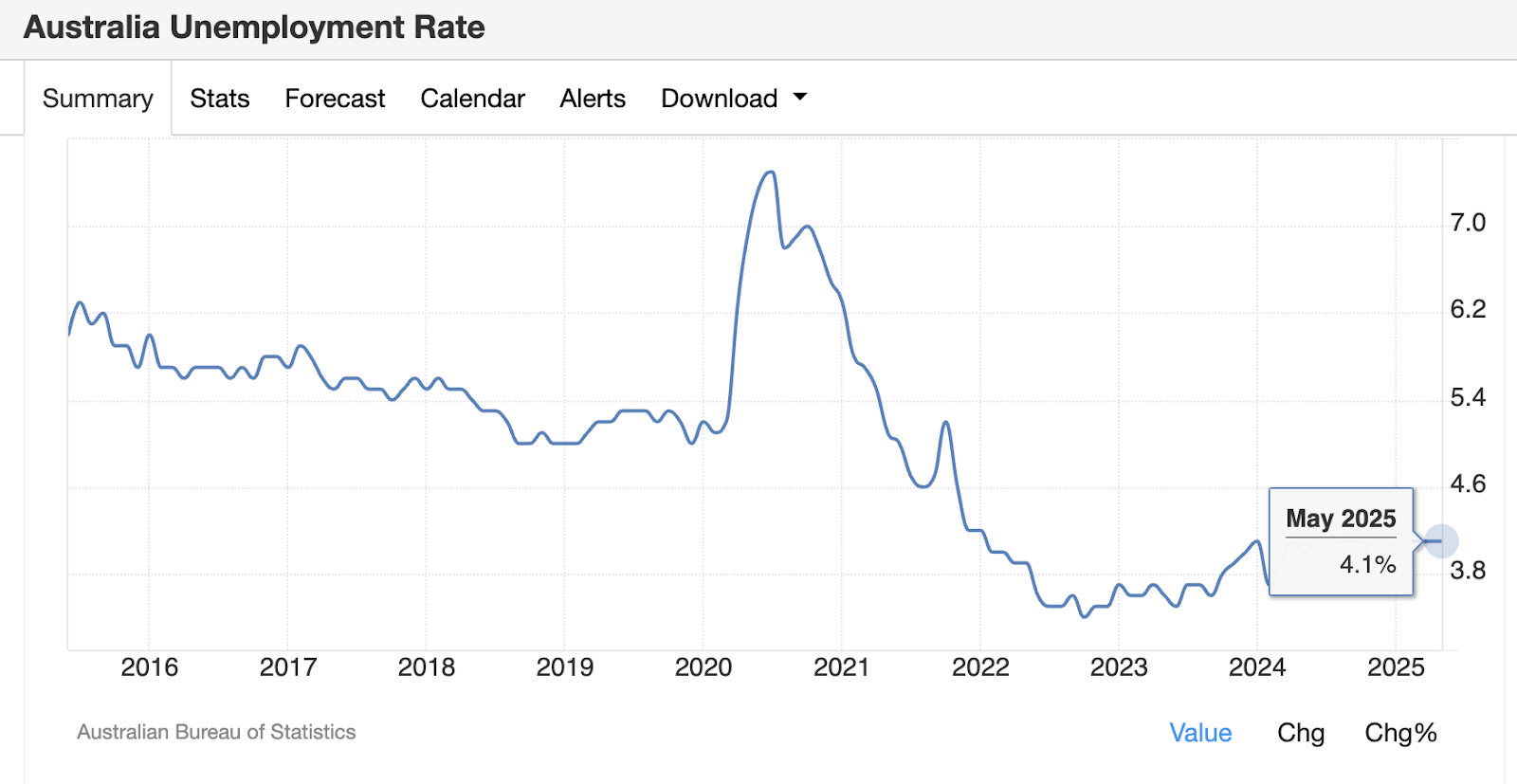

Australia, on the other hand, saw unemployment surge to 7.5% during the pandemic—but then it steadily dropped and has since hovered around 4.1%. That's not only lower than the pandemic peak — it's even lower than pre-pandemic levels. Australia's job market is remarkably stable, and almost anyone who wants a job can find one.

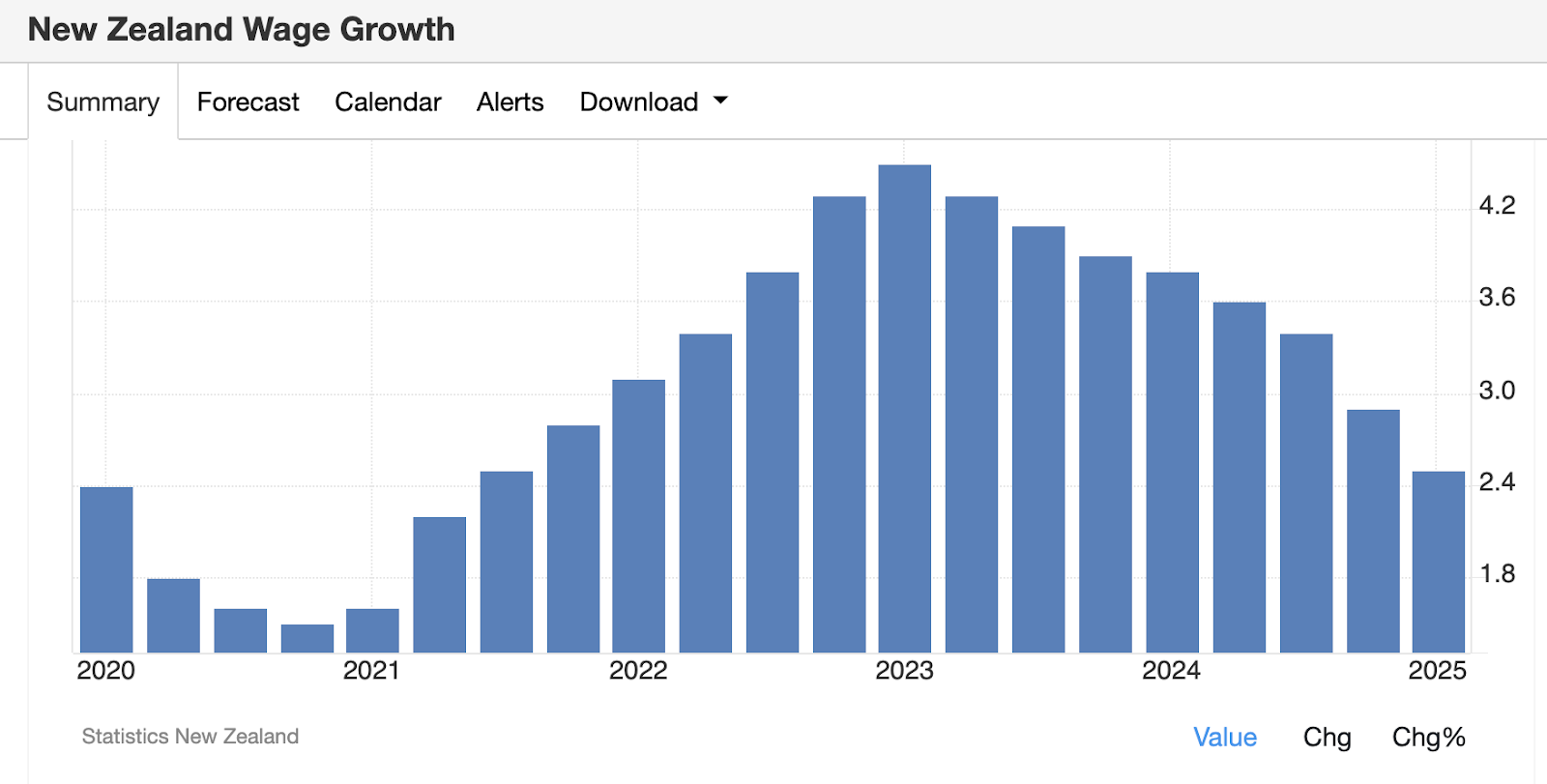

On top of that, New Zealand trails far behind Australia in both real wages and wage growth. Australians are earning more, and that means stronger spending power — they can afford to pay more for homes, even as prices rise.

4. Market Size

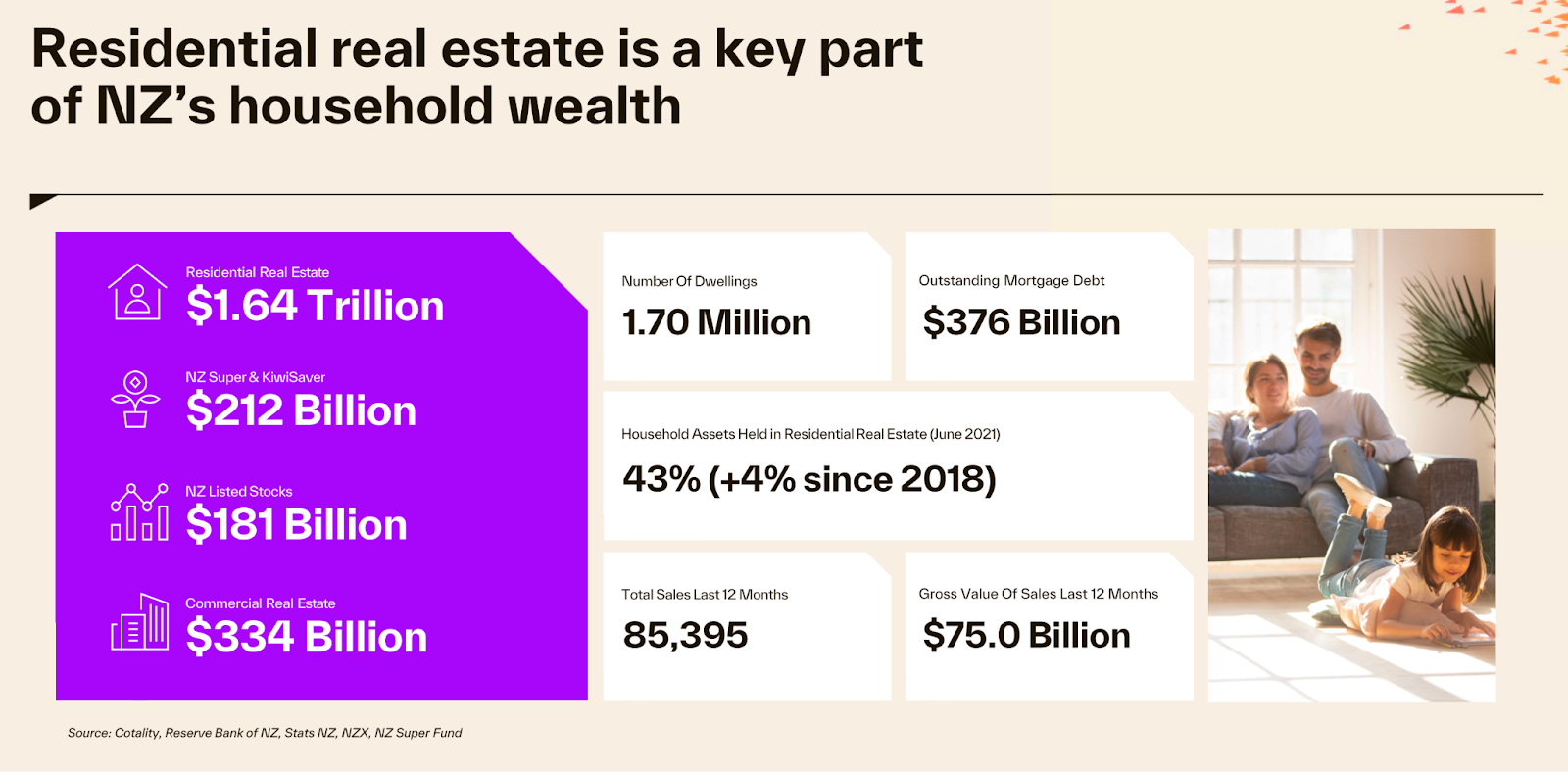

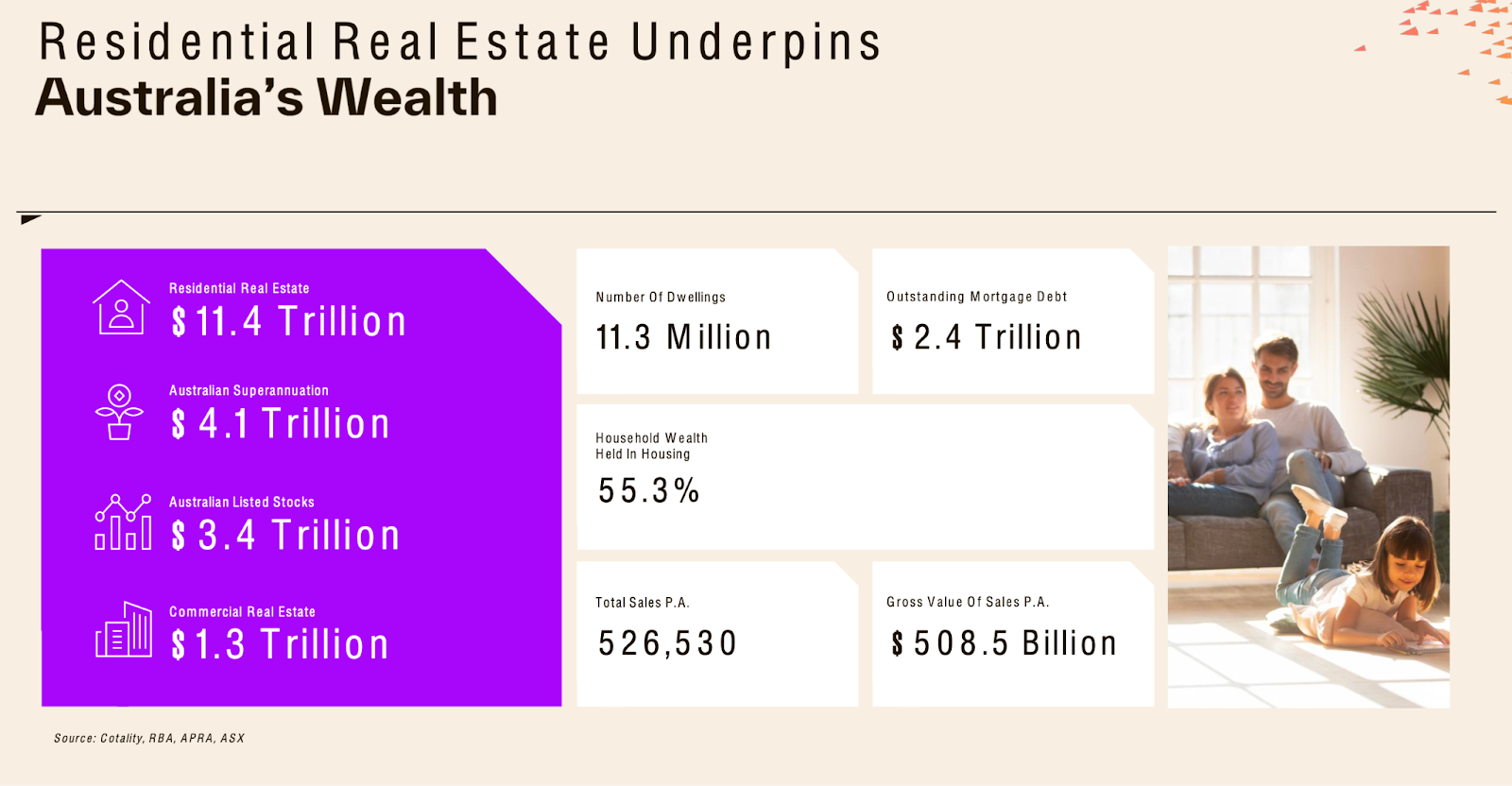

So why is it that New Zealand's housing market is crashing while Australia's has largely held onto its pandemic gains? A big part of the answer lies in market size. As of May this year, New Zealand's total housing market is valued at 1.64 trillion. Australia's? A whopping 11.4 trillion — nearly seven times larger.

Think of it this way: New Zealand is like Australia's ninth state, with Auckland as the capital — lots of people, but beyond that, mostly small towns. But in Australia, there are several housing markets of this size — each with its own cycle, balancing each other out. Some rise while others fall, and the national average stays on an upward trend.

So, next time someone tells you "New Zealand's crash is a preview of what's coming for Australia," you might want to reconsider. If property prices fall in just one state — say, Victoria — does that mean the entire Australian housing market will collapse?

5. Government Attitude

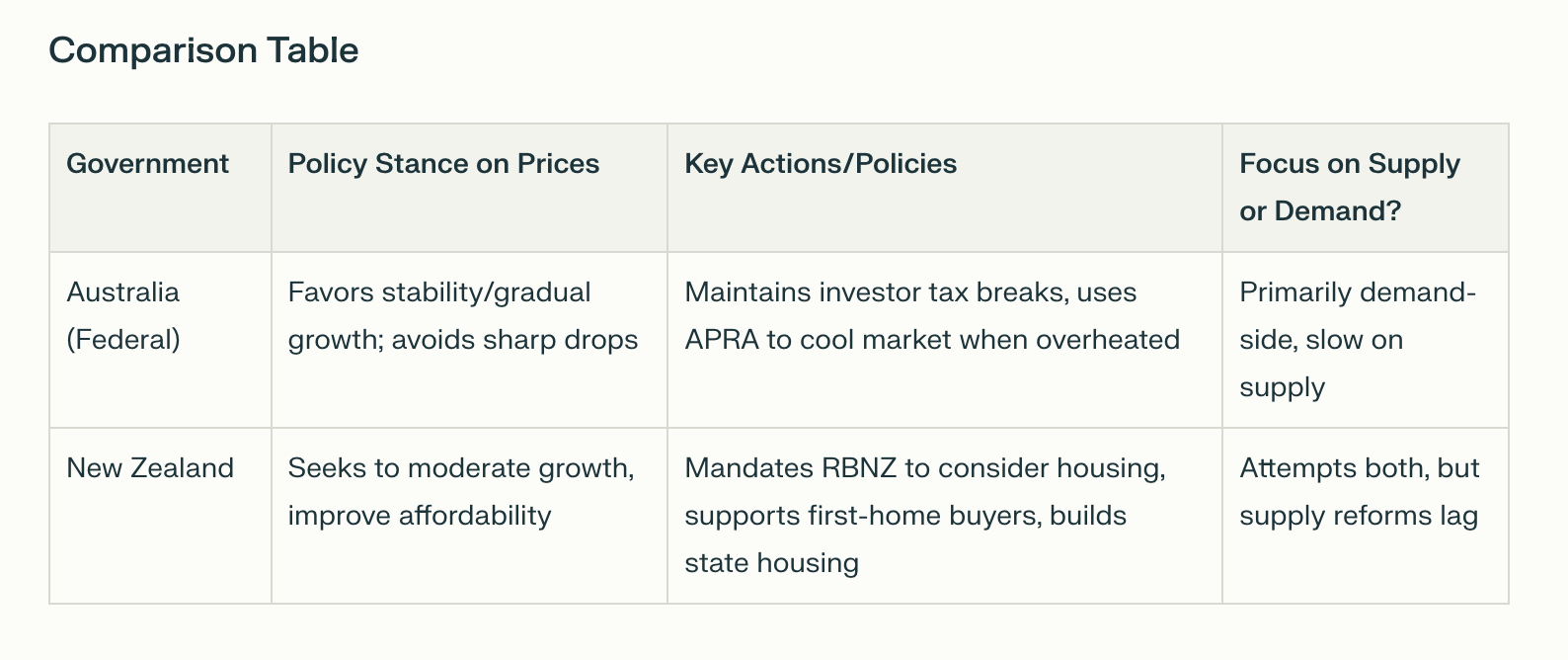

There's one more factor many people overlook — the government's stance. Australia's federal government wants house prices to keep rising in the long term. There are many reasons for this. For one, housing plays a massive role in the national economy. And let's not forget — most federal senators themselves own multiple properties. New Zealand's government, however, has taken a very different approach. They'd rather see prices slow down — or even fall — in order to make housing more affordable.

These two fundamentally different top-level mindsets shape their housing policies from the ground up. And policies, of course, eventually shape prices.

Now, all of these five factors are just appetizers. If you really want to understand why Australia and New Zealand's housing markets have taken such different paths, you need to dig deeper — into the core drivers: population and migration.

New Zealand's Population and Immigration

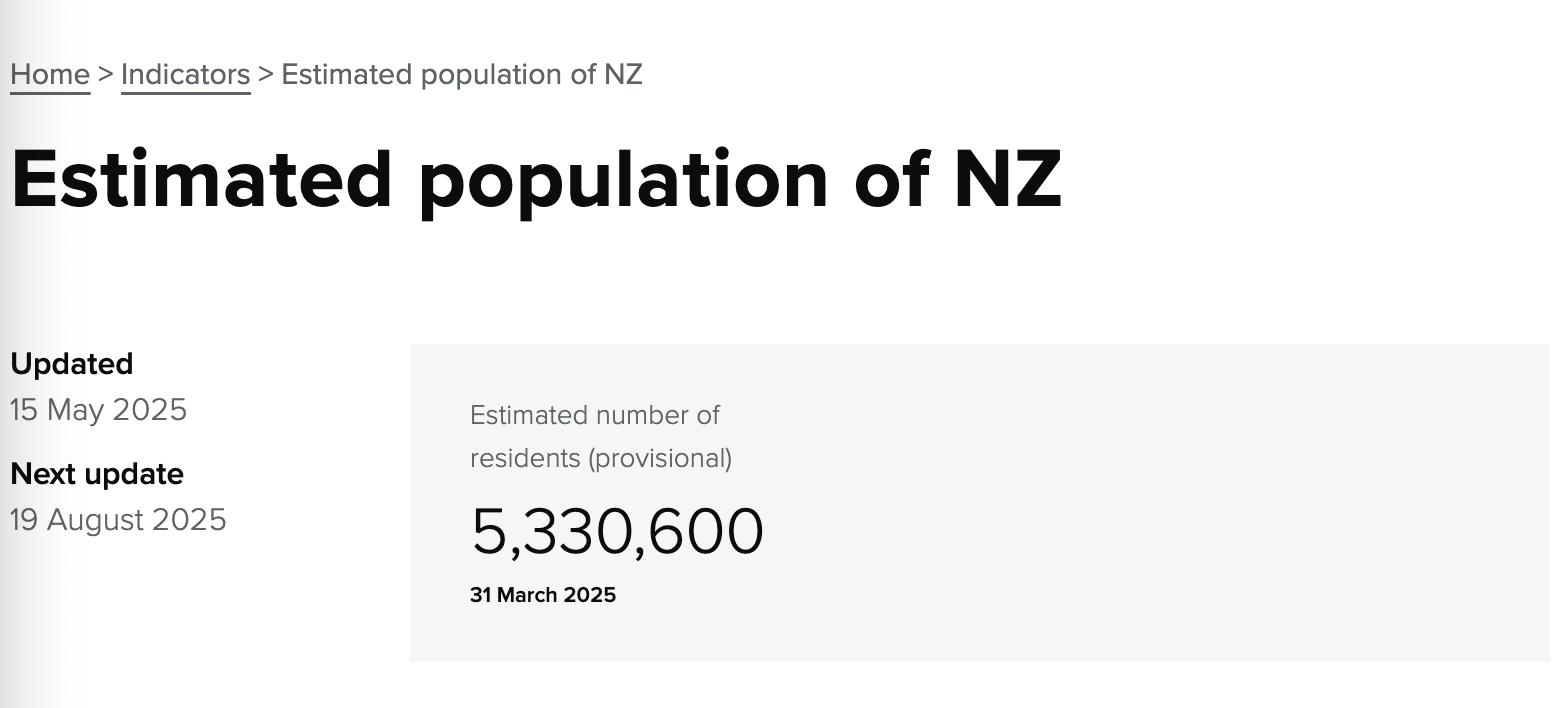

New Zealand's population is 5.3 million — that's not even as many people as in New South Wales. The population has been growing steadily, but what is it relying on to grow?

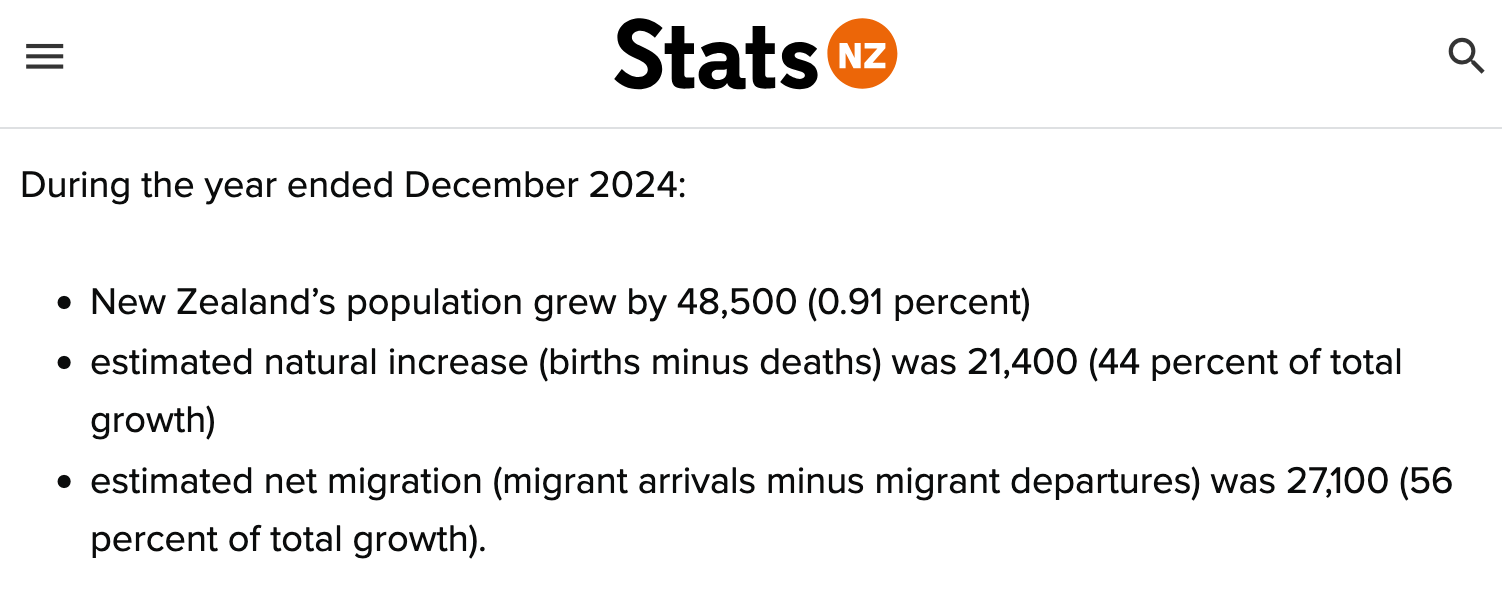

In 2024, New Zealand's population increased by 48,500 people in total. Among that, net natural increase (births minus deaths) accounted for 21,400 people — 44% of the total. Net migration contributed 27,100 people — 56%. So, at first glance, it doesn't seem like immigration is doing all the heavy lifting. But the number of net migrants each year fluctuates — sometimes high, sometimes low — while the natural increase is steadily declining.

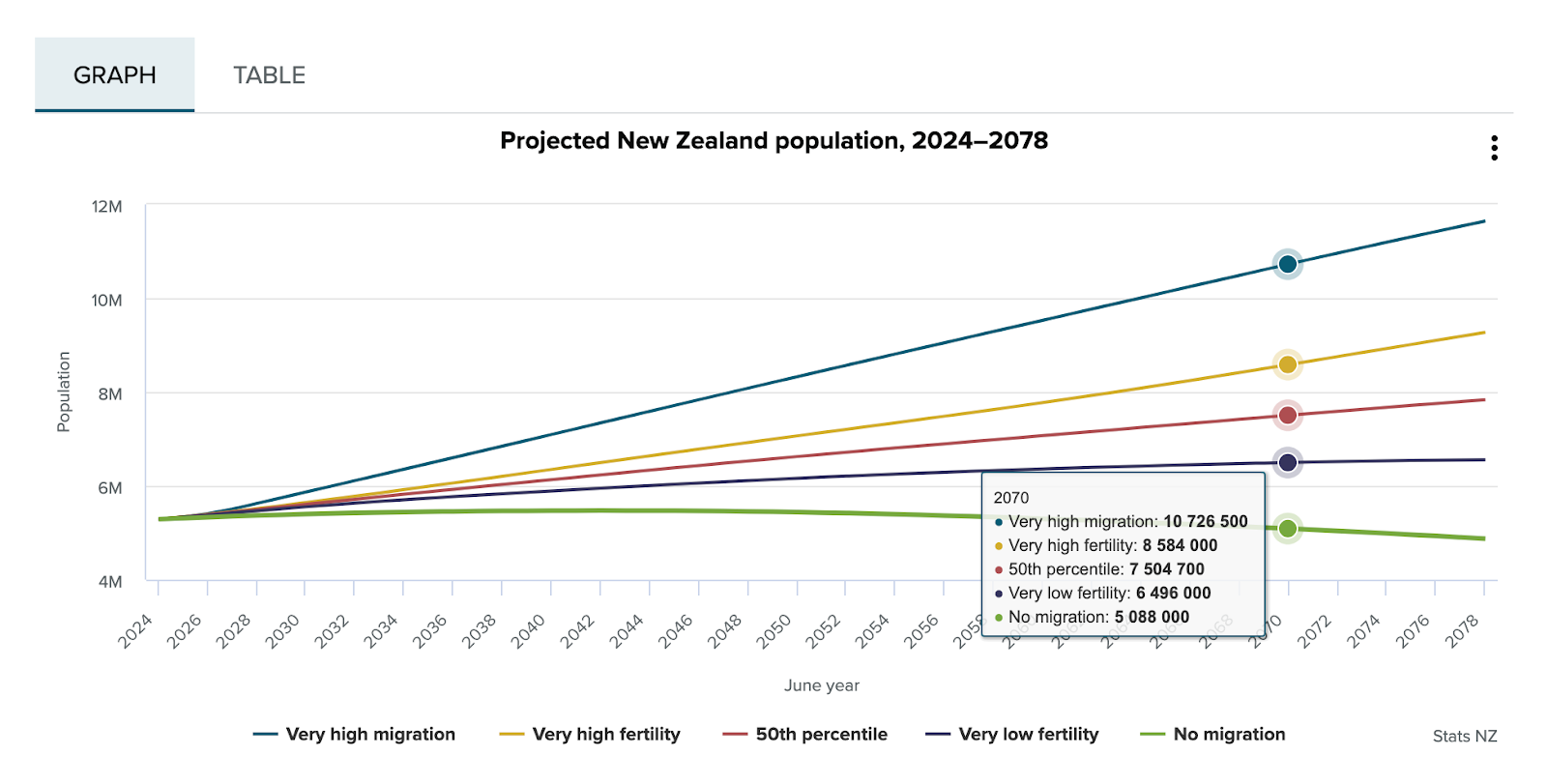

According to New Zealand's own official projections, by 2070, if immigration levels remain balanced, the population could grow to 7.5 million. But without any immigration at all, the population would actually shrink to 5.1 million. So, saying that New Zealand's population growth depends entirely on immigration — is really not an exaggeration.

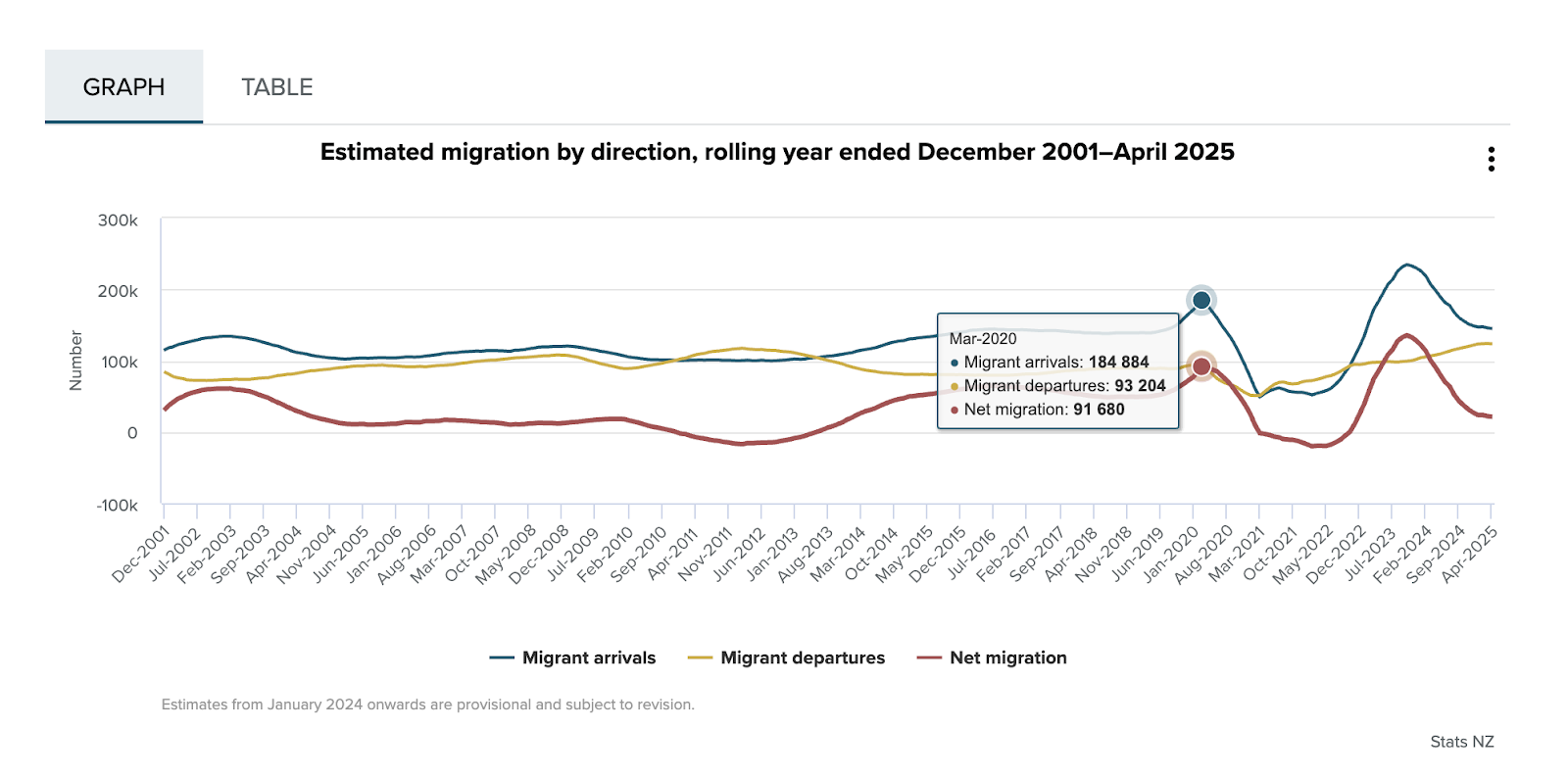

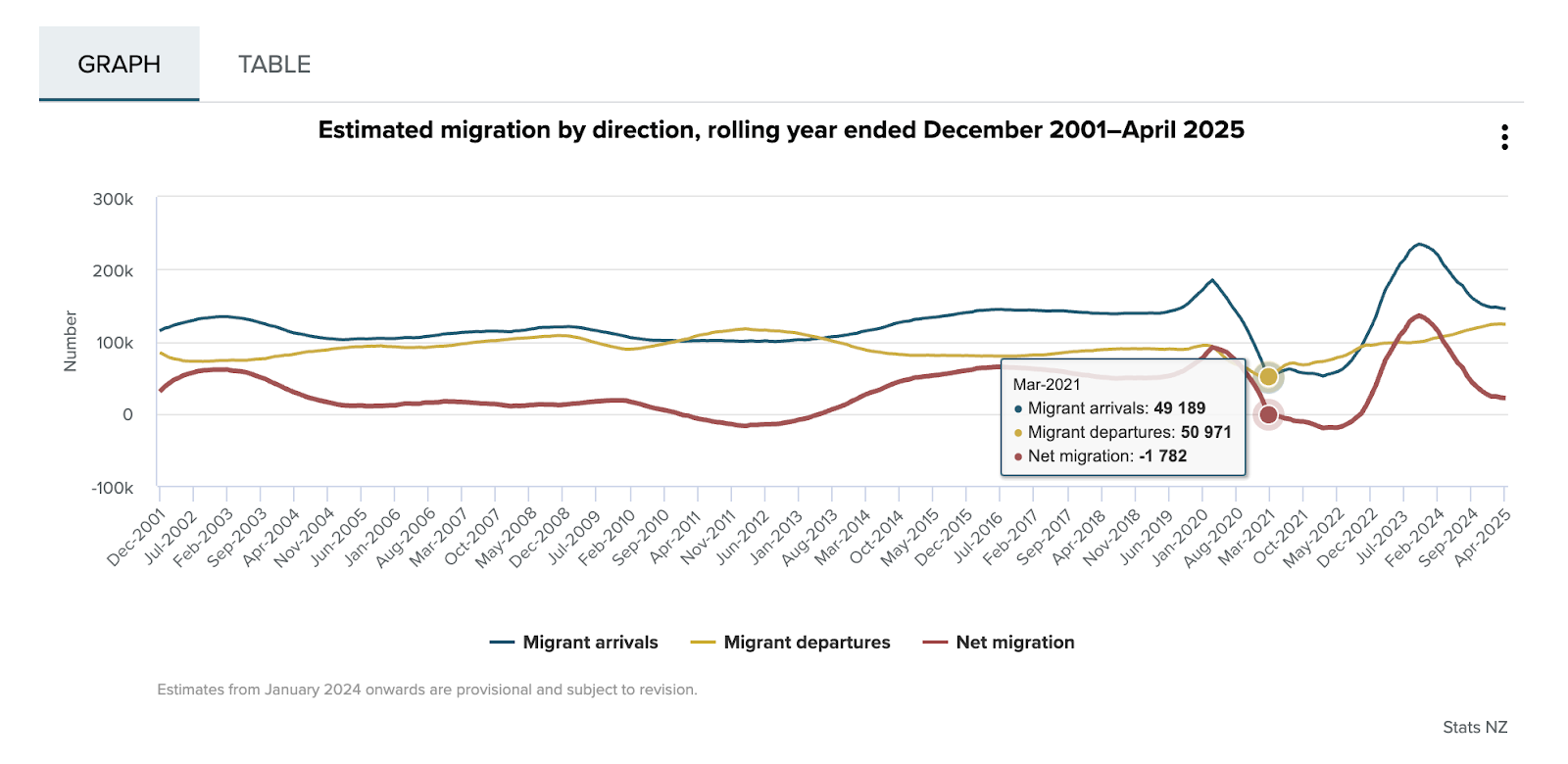

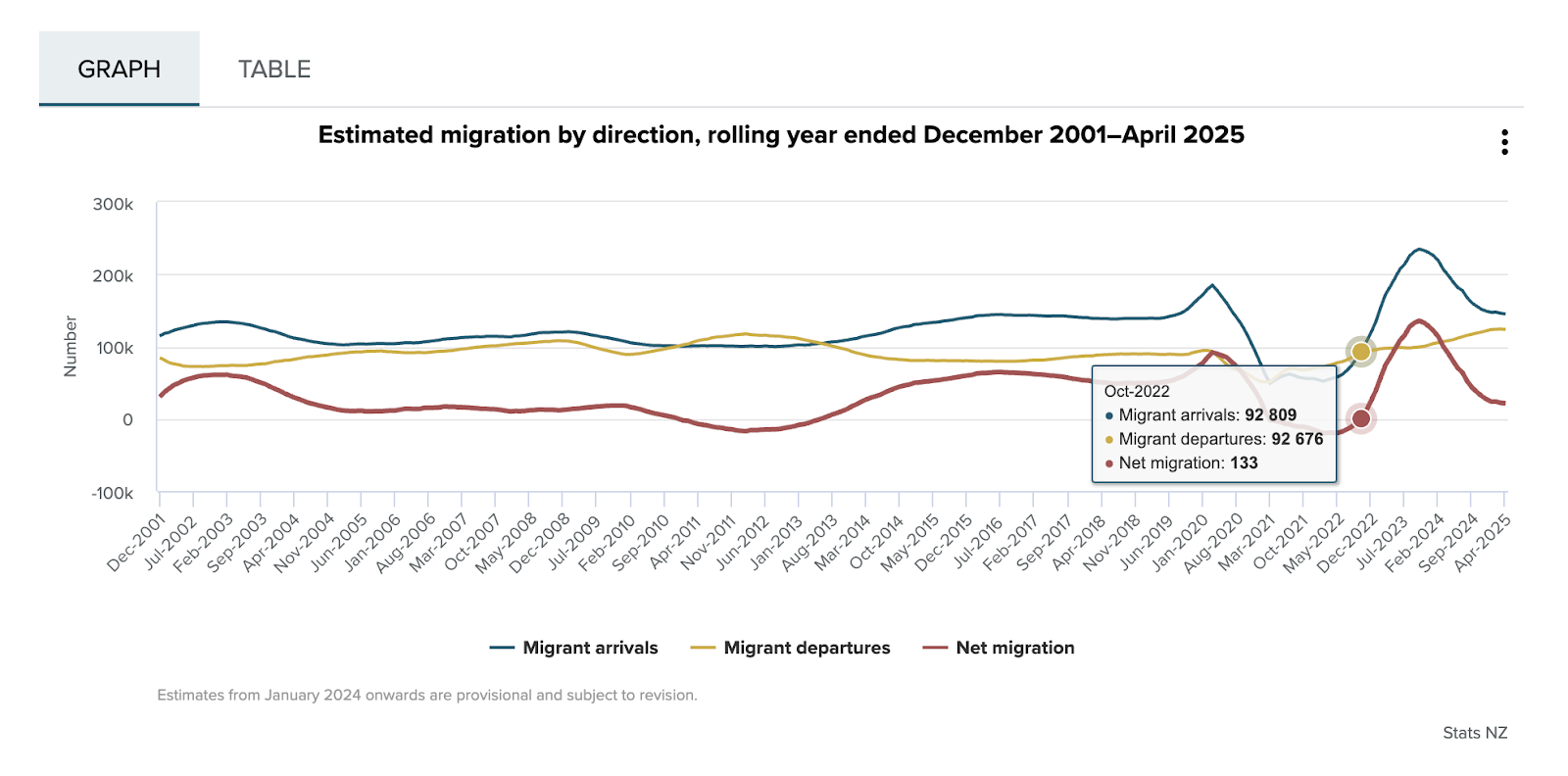

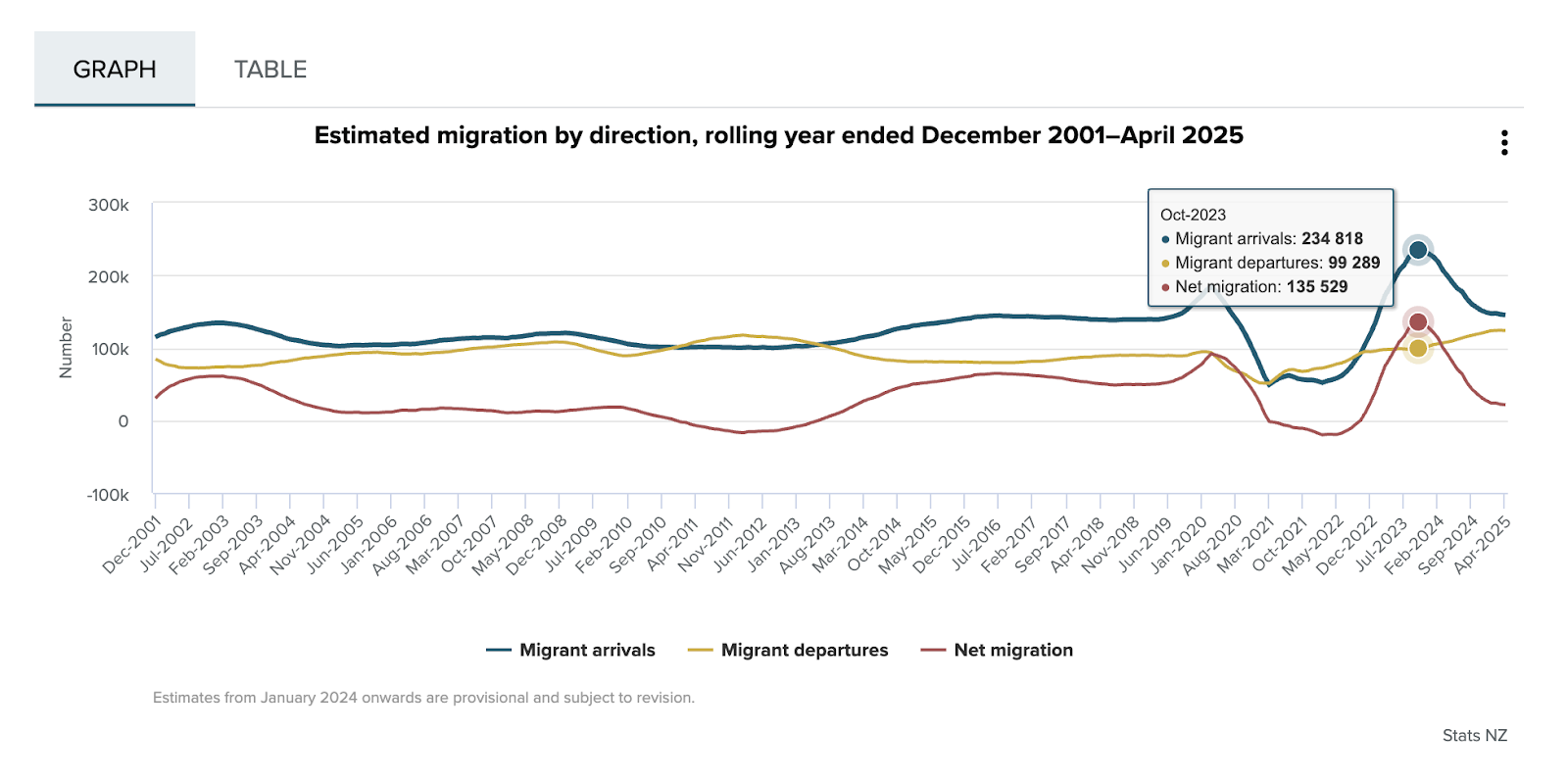

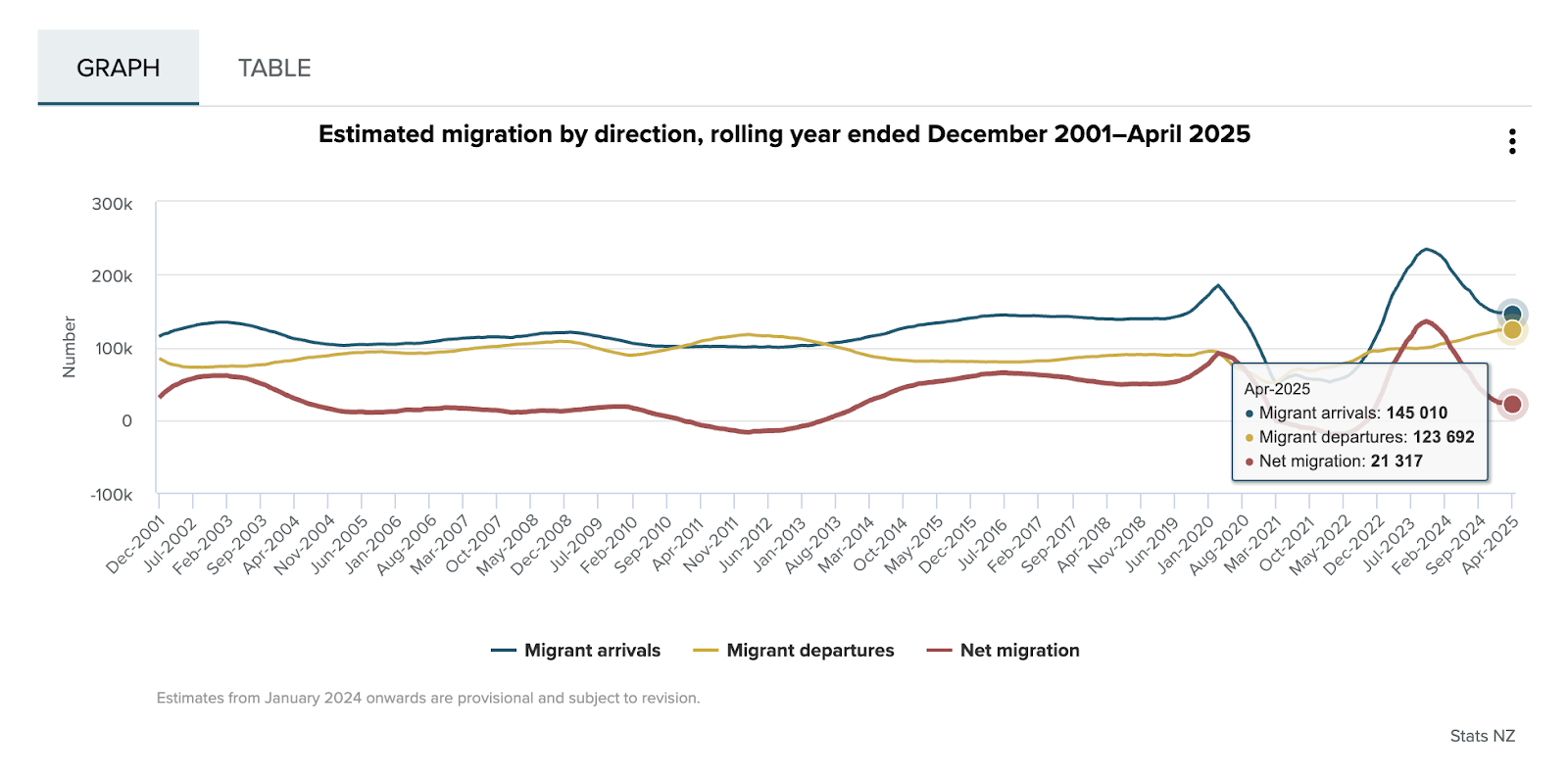

Now let's take a look at what's happened to immigration numbers since the pandemic began in 2020. At the end of 2019, New Zealand's net migration hit a record high. But within 12 months, that number dropped to zero. From March 2021 to October 2022 — a year and a half — New Zealand actually experienced negative net migration. Then, over the course of the following year, once the border reopened, the country welcomed 135,000 net migrants — the highest in history. But in the 12 months leading up to April this year, net migration fell back down to just 21,000 — the lowest figure in the past decade, pandemic aside. So, when immigration numbers swing from record highs to decade-lows, it's no surprise that housing prices went on a wild roller coaster ride.

Some might ask: "Wait a minute — didn't New Zealand close its borders on March 19, 2020, and only fully reopen on August 1, 2022? If there were no new migrants during that time, why did house prices surge first and then collapse?" The answer lies in finance.

It wasn't just New Zealand — property prices surged in almost every major developed country during that period. Even with no population growth, house prices rose — and that only happens when money is the driving force.

Early in the pandemic, New Zealand implemented a range of stimulus policies to stabilise the economy, including significant interest rate cuts. In effect, the government borrowed money, handed it to the public, and encouraged massive borrowing and spending. So what did people do with the money? Of course — they bought houses. As a result, between May 2020 and November 2021, property prices soared by 44%. But then came a surge in inflation.

To fight that and cool the overheating economy, the government began raising interest rates — and New Zealand became one of the fastest and most aggressive rate hikers among all OECD countries.

Mortgage rates skyrocketed. The loosened LVR (loan-to-value ratio) policies from the pandemic period were tightened again. Negative gearing was removed. All these factors combined drove property prices into freefall. Only after reopening the borders did the housing market begin to see signs of a turnaround. This was the first part of the cycle. It was nearly identical to what happened in Australia. But what came next was a different story.

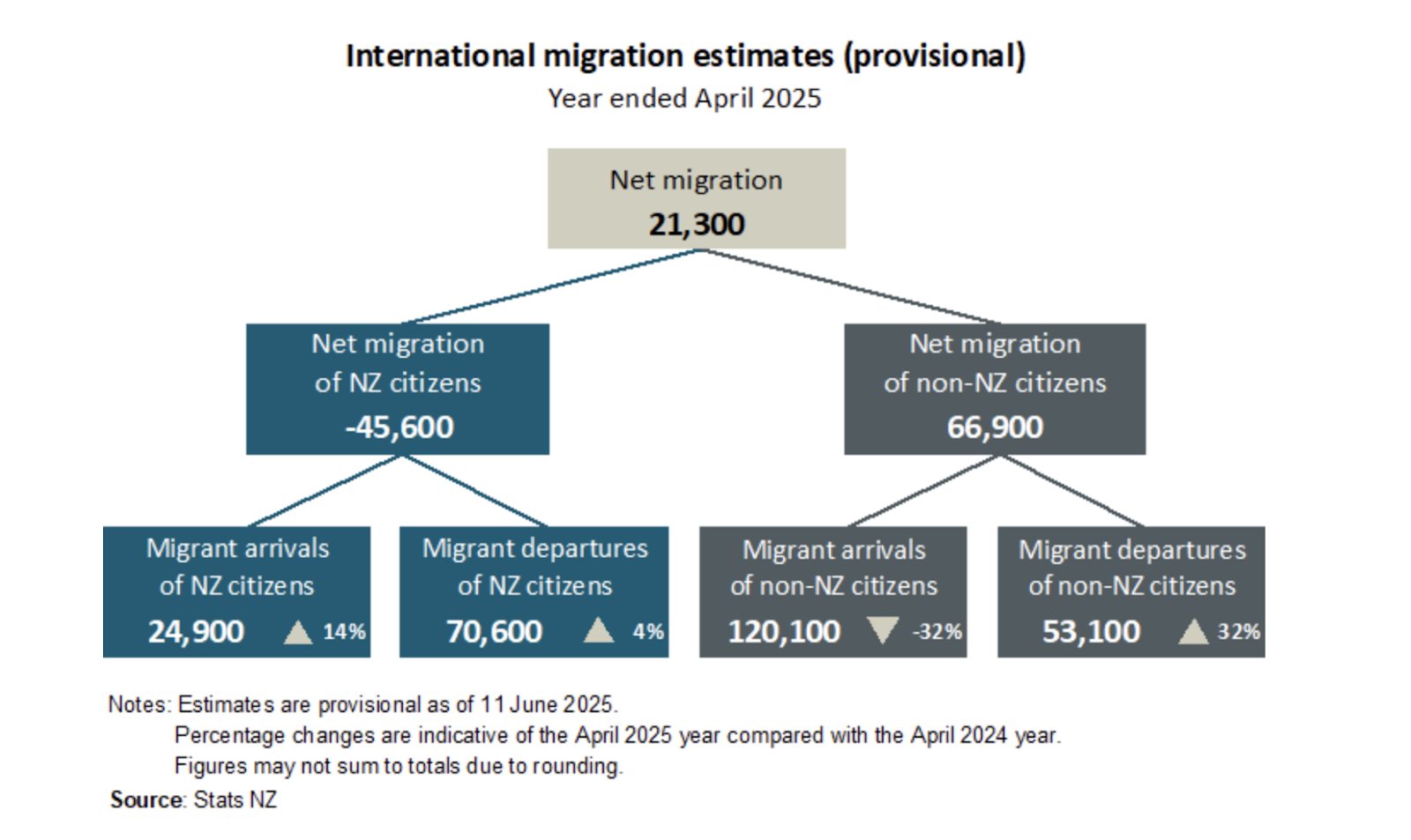

As New Zealand's economy continued to weaken, unemployment rose, and with fewer ways to earn a living, more and more people began leaving the country. In the 12 months leading up to April this year, New Zealand's net migration was just 21,000. If we break it down, Non-New Zealand citizens had a net gain of 67,000 people, made up of 120,000 arrivals and 53,000 departures. That makes sense. But take a look at what New Zealand citizens did: 70,000 citizens left the country, and only 25,000 came back. That's a net loss of 45,000 people — all citizens.

So where did they go? You guessed it — most of them came to Australia. Why? The answer is simple: economic reasons. New Zealand has high housing prices, fewer job opportunities, lower wages, and little economic growth. So, of course, people would want to leave for a better life.

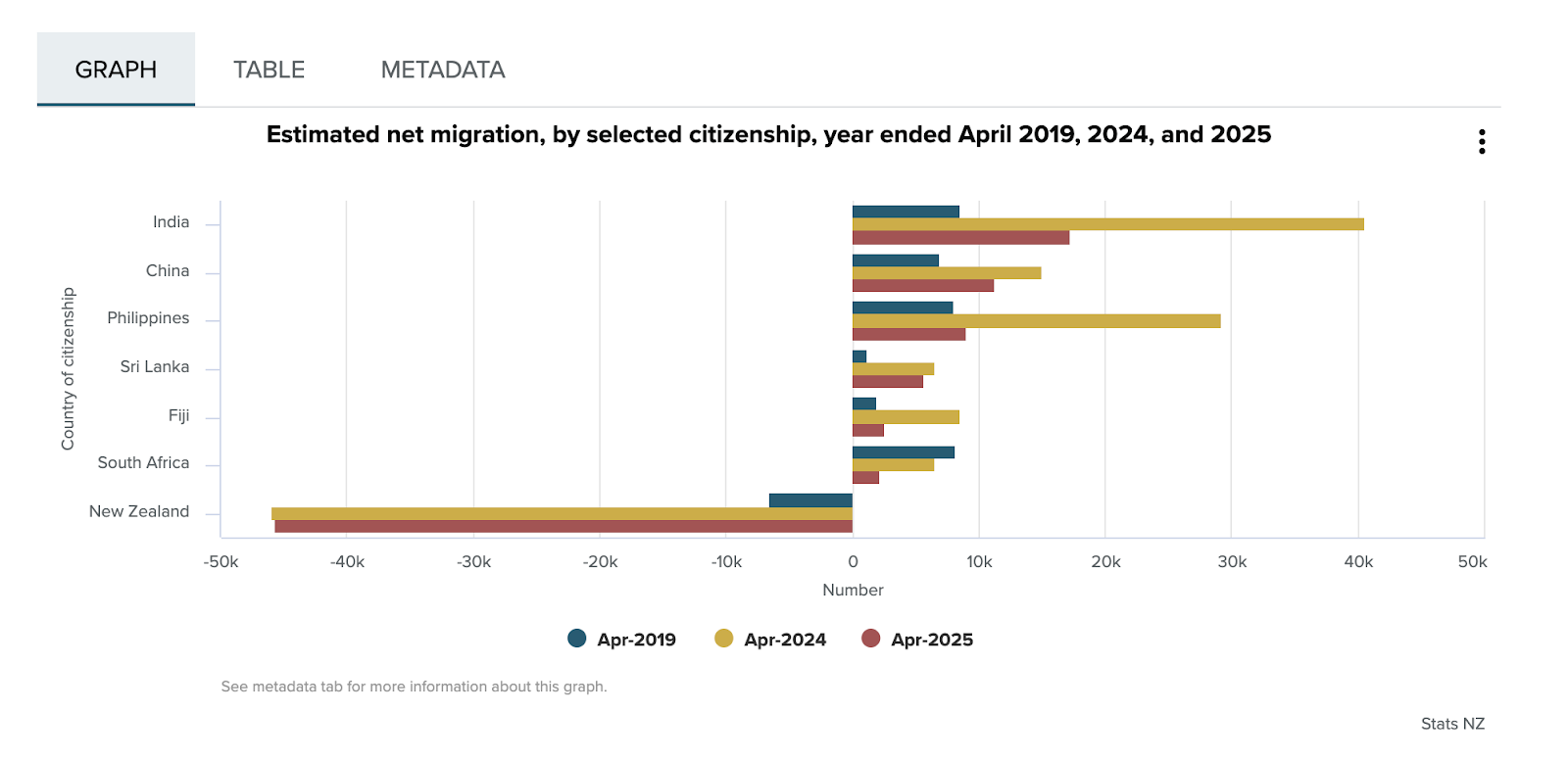

If you break it down by country of origin, the migration patterns become even clearer. In the blue bar representing 2019, India, China, and South Africa were the top sources of immigrants to New Zealand. Some locals left too, but the numbers were pretty balanced.

Fast forward to 2024 (represented by the yellow bar), and everything has changed. Indian immigration surged, Filipino immigration surged, Chinese immigration rose slightly. But look at the New Zealanders: the number leaving was around 60% of the total number arriving from those three countries combined.

By 2025 (the red bar), the picture becomes even more dramatic. Indian immigration fell by 60% compared to 2024, Chinese immigration fell by 20%, Filipino immigration dropped by 70%, and the number of New Zealanders leaving? It didn't change at all.

If this trend continues, we might end up with a strange scenario — people from other countries move to New Zealand, while New Zealanders move to Australia — a complete demographic swap. Think about it: When people leave, how can the economy grow? How can property prices rise? Without people, there's no housing demand — it's that simple.

Over the past few years, New Zealand has tightened its immigration policies, raising requirements for skilled migrants in terms of language, education, and work experience. Applying for permanent residency or family reunion has also become more difficult. This is also one of the reasons why immigration numbers have dropped.

Australia, on the other hand, has never had trouble attracting immigrants. If the government wanted to, it could let in a million people in a year, and there would be no shortage of people eager to come.

At the end of the day, it all depends on whether Australia offers a better life than immigrants' original countries — a more relaxed lifestyle, higher income potential, and more opportunity. And compared to Australia, New Zealand doesn't have the same pull. And sometimes, it's not even up to the New Zealand government — if people don't want to come, there's nothing they can do.

As long as Australia keeps its door open to New Zealanders for work and residency, many will continue to move across the sea — because the income gap is simply too big. If New Zealand can't attract a large number of new immigrants, its property market will struggle to rise. And as long as Australia remains open, New Zealand's housing prices will be under pressure. For New Zealand's housing market to truly rebound, the country needs to become wealthier. New Zealanders need to start earning more than Australians; only then will they have a reason to come home, and only then will they be able to support New Zealand's property prices again.

Will the Australian Property Market Follow?

We've covered a lot so far, so now let's try to answer the question we posed at the beginning of the video: New Zealand's property market isn't doing well—so will Australia be next?

After all the analysis we've just walked through, you probably already have your own answer in mind. In fact, I've talked about this in many previous episodes. I'm bullish on the Australian property market for 20 years—and that view has never changed. If you're interested, feel free to go back and check out my earlier videos.

Here's the over-simplified way to understand the Australian housing market: As long as immigration numbers stay strong, the property market won't see any major problems. If immigration slows down considerably or stops altogether, the market might be okay for a short while, just like during the early days of the pandemic when borders were shut and the government flooded the economy with printed money. But in the long run, the market wouldn't be able to hold up.

As for comparing Australia to New Zealand, I personally don't think the performance of New Zealand's property market will have much effect on Australia. Why? Because the rules that apply to New Zealand simply don't apply to Australia. And that's for one simple reason: Australia is a different country.

You can't really compare property markets across countries—just like you can't compare their political systems, economic structures, natural resources, population sizes, or geography. Even within Australia, each state and territory has its own property cycle and unique market characteristics. Sometimes, two neighbouring suburbs in the same city can be going in completely opposite directions. Comparing national markets is meaningless.

At AusPropertyStrategy, our perspective has always been this: Yes, the mechanism behind property price movements is universal—it's about the balance between supply and demand. But the factors behind supply and demand vary drastically from market to market.

People often carry this mindset with them: "This is how I used to invest in real estate where I lived before," "This is how I used to build relationships," "This is how I used to understand politics and economics." And they assume those lessons can be applied to every corner of the world.

Some even convince themselves they've already mastered it all—when in fact, they're stepping into a completely new environment with zero understanding, and they refuse to admit it. They want to act like an expert without being willing to learn from scratch. That's just wishful thinking.

We've had quite a few VISION members in situations where they bought a few properties, found them to be losing money, realised they had made mistakes, and then came to us. The first thing I always ask them is: Where were you earlier? You've lost time, lost money, gone around in circles—and now you want me to fix the mess. Why not come to me from the very beginning?

And the answer, at the end of the day, is always the same: It's a mindset issue. They don't realise they're investing in a field they completely don't understand. They also don't understand that property investment is a profession—and good service comes with a price.

I've also met another group of people. They have solid jobs in Australia, earning somewhere between $150K to $250K a year. In their career field, no doubt—they're elite, hardworking, and absolutely respectable. They know they should invest in property, but they just never take action. Why? Because they haven't figured out what truly matters.

Here in Australia, if you're only working a job, you will never break out of the middle class. What does "middle class" mean in Australia? It means you work your butt off every day, earn what looks like a good income on paper—but nearly half of it goes to taxes. That's working for the government. If you have a home loan, another big chunk goes to the bank—that's working for the bank. In the end, you're working for your boss, for the government, for the bank…Everyone's making money off of you—and you're left with just a bit for yourself. And yet, you might still feel proud somehow. You're carrying the load, sure—but at what cost?

If you want to escape the rat race, there's only one way: own property. Just one good property can earn more in a year than your salary—and you barely have to lift a finger. That's the truth.

So what's the right approach? Even if you have to take unpaid leave, you should get out there, inspect properties, and make the right investments. That's what someone truly focused on building wealth would do. At AusPropertyStrategy, we help you do exactly that.

Visit our website to learn more about our VIP service: VISION Membership—a one-stop solution for building and managing your entire Australian property portfolio.

Watch the video version of the blog on YouTube.