Massive Budget Surprises in QLD and WA! What This Means for House Prices [APS087]

In our previous videos, we covered the New South Wales and Victoria budgets—and the feedback was incredible. Many viewers asked me to also break down the Queensland and Western Australia budgets. They said only after understanding those can we figure out where the property investment opportunities lie in the next 12 months—Sydney, Melbourne, Brisbane, or Perth? No problem. Today, I’ll deliver both in one go.

Queensland and WA are quite similar in terms of economic scale. Both rely heavily on resource exports, both have mid-sized capital cities, and both have been magnets for interstate and international migration. Over the past five years, their housing markets have surged. The similarities are striking. So, what do this year’s state budgets reveal about their fiscal health and economic outlook? Where are the major infrastructure investments going? What bold policies have they rolled out to stimulate the housing market? And if you had to choose, based purely on the fundamentals, which state makes more sense for property investors—Queensland or Western Australia? Let me give you a spoiler right now: one state is focused on infrastructure, while the other is sinking into the mounting fiscal deficits.

WA State Budget 2025–26

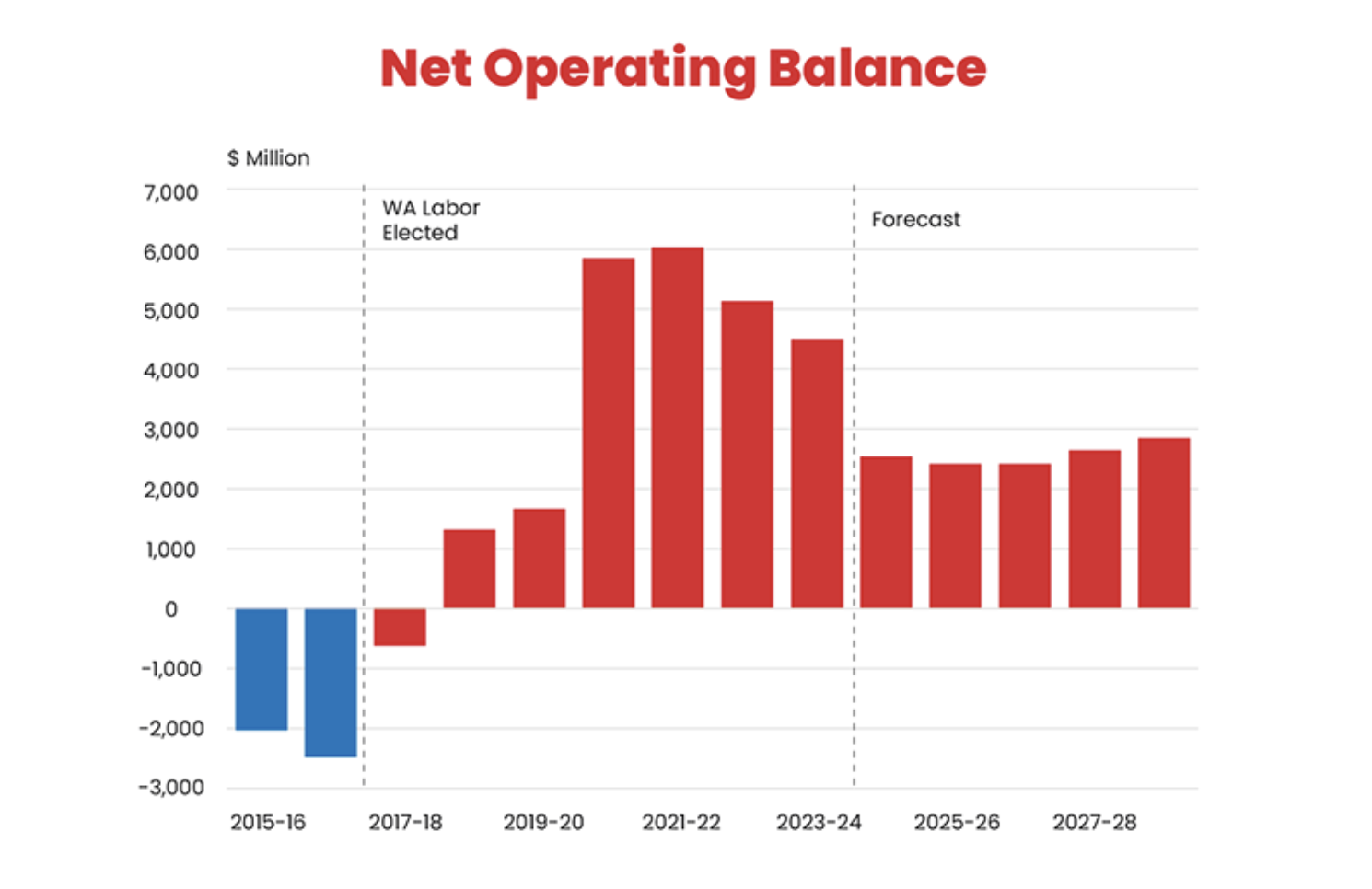

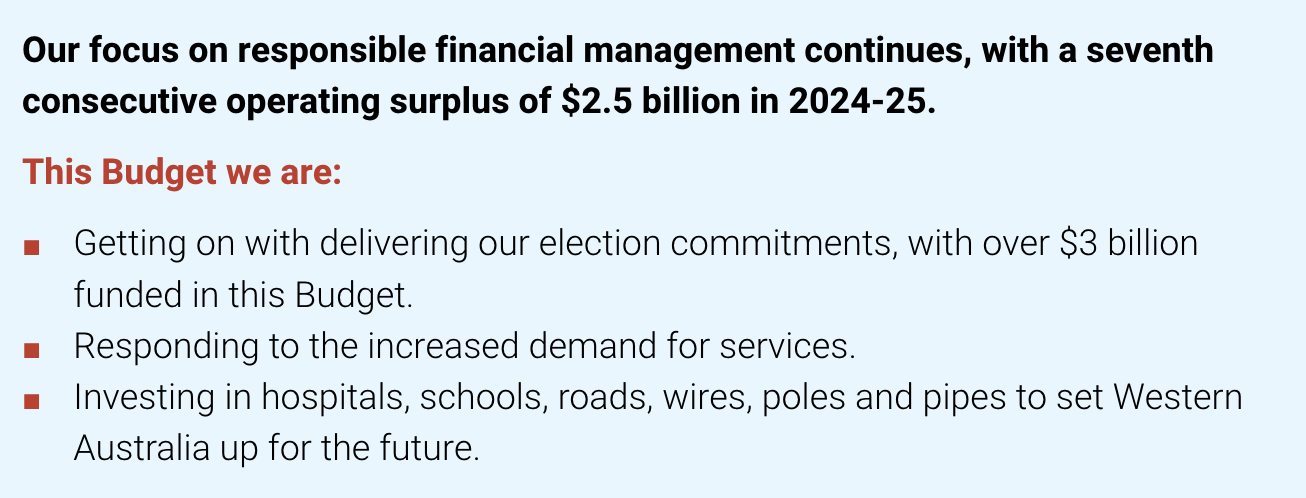

Once again, Western Australia is the best-performing state in Australia when it comes to fiscal health—hands down. Since 2018, including the entire COVID period, WA has delivered seven consecutive years of budget surpluses. The biggest surplus was in the 2021–22 financial year, hitting $6 billion. In 2023–24, it dipped slightly to around $4.5 billion. And for the just-concluded 2024–25 financial year, WA still achieved a $2.5 billion surplus—even though it only received 75% of its GST share. The other 25%? It was redirected to support Victoria.

Looking ahead, for the 2025–26 financial year, WA is forecasting a slight dip in its surplus to $2.4 billion before gradually climbing back up to $2.8 billion over the next four years.

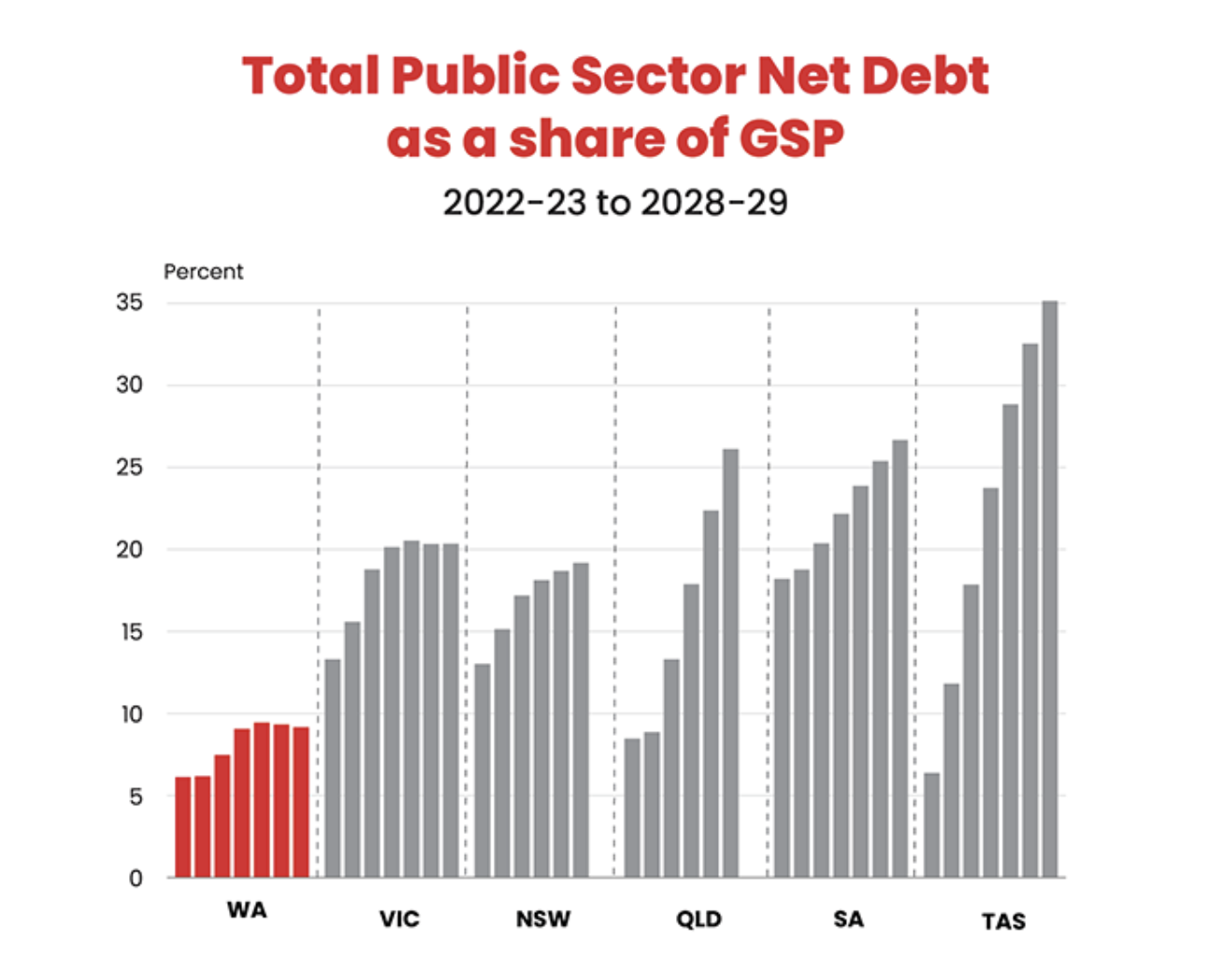

In terms of economic size, WA only ranks fourth in the country. But when measured by state debt as a percentage of economic output, WA comes in at the lowest, with just around 9%. To compare, Victoria is at 20%, and Tasmania is at 35%.

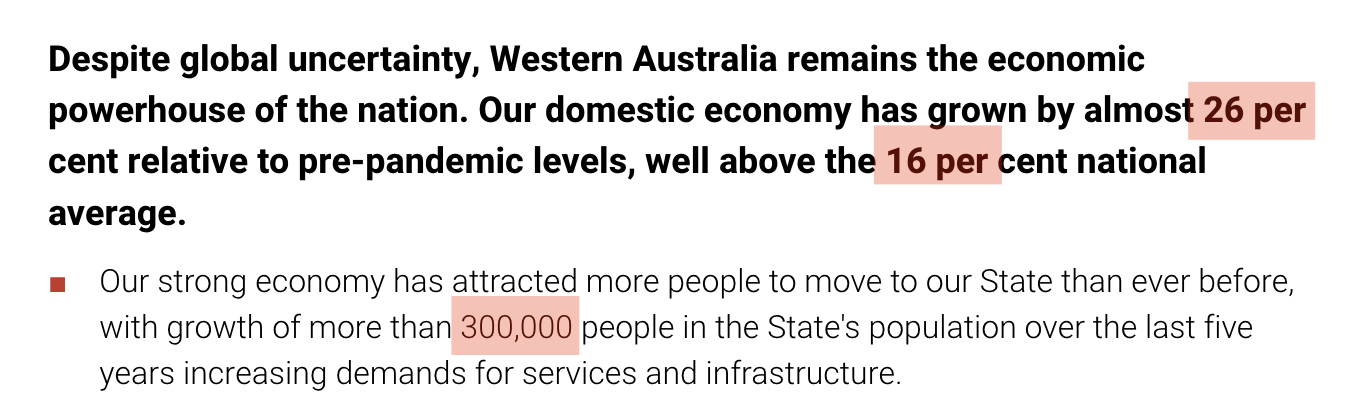

Over the past five years, Victoria added 300,000 people and grew its economy by 26% compared to pre-COVID levels. But Australia’s national average? Only 16%. So, if you’re asking which state is the healthiest economically, there’s no question—WA takes the crown.

So how is Western Australia planning to spend its money in the 2025–26 budget? I’ve picked out the parts most relevant to property investors, and I’ll break them down for you one by one.

Made in WA

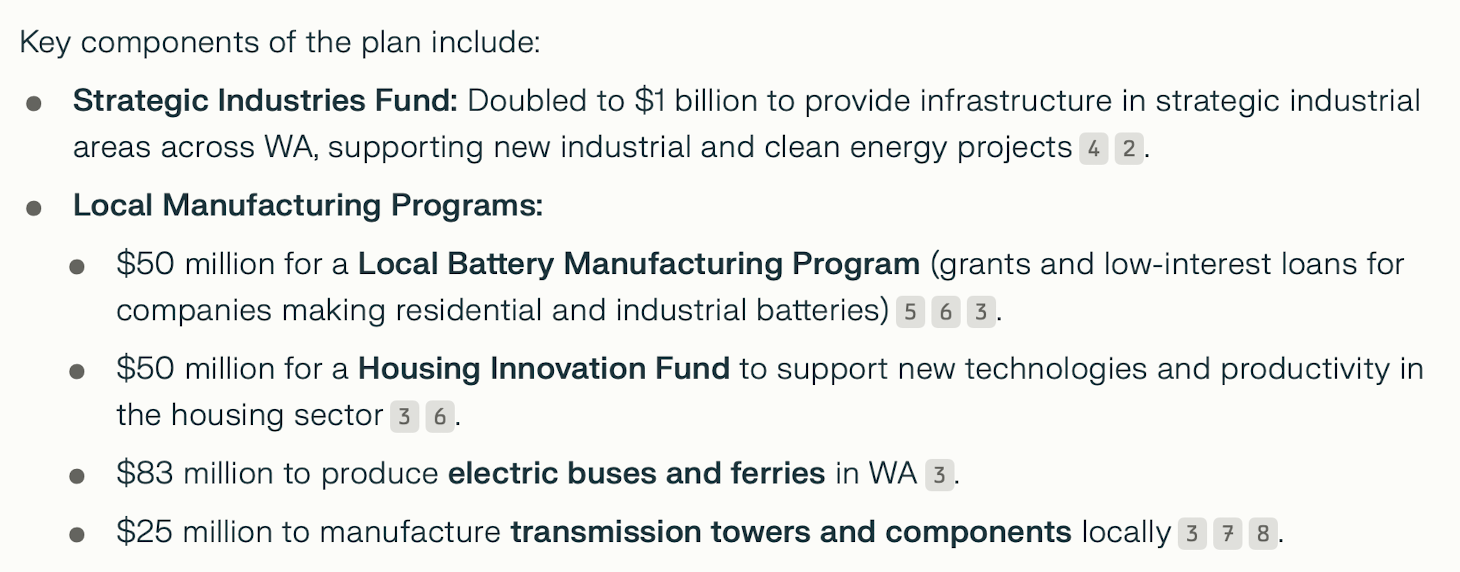

One of the major highlights in this year’s budget is the “Made in WA” initiative. WA is investing $1.4 billion to boost high-end local manufacturing, clean energy, and economic infrastructure. The goal? To diversify WA’s economy and reduce its heavy reliance on resource exports.

What does this include, exactly? A new Strategic Industries Fund, backed with $1 billion, to build infrastructure in industrial zones across the state and support clean energy projects. Additional funding for local manufacturing projects to strengthen WA’s electricity grid and improve productivity and efficiency in industries like construction and housing.

Now, these investments aren’t flashy—they’re not things the average person sees day to day. But over time, they’ll genuinely improve life for people living in WA. This is very different from Victoria, where the government seems obsessed with finding more ways to tax everyday people while half of their infrastructure projects get scrapped, and nobody knows when the airport will even get a train line.

This budget also includes over $300 million in funding for free TAFE courses—specifically to train construction workers and manufacturing workers. In WA, these are high-paying jobs, and now the training is free.

If I were in either of these industries, I’d move to WA without hesitation. Why? Because your standard of living would instantly improve.

Traditionally, about half of WA’s economy has depended on mining exports. Whether the economy—and even property prices—do well has long been directly related to iron ore prices. But since last year, that’s starting to change. WA is now actively pursuing economic diversification. This shift supports stronger job creation and helps stabilise the housing market, reducing its volatility and encouraging sustainable long-term growth.

First Home Buyers

When it comes to supporting first-home buyers, WA has come up with some new ideas. The first initiative is called a Shared Equity Loan—a government co-buying program designed to help low- to middle-income earners purchase apartments and townhouses, whether they’re off the plan or under construction.

WA has set up a special entity called Keystart, which provides home loans to help buyers get into the market with less upfront cash. So how does the shared equity model work?

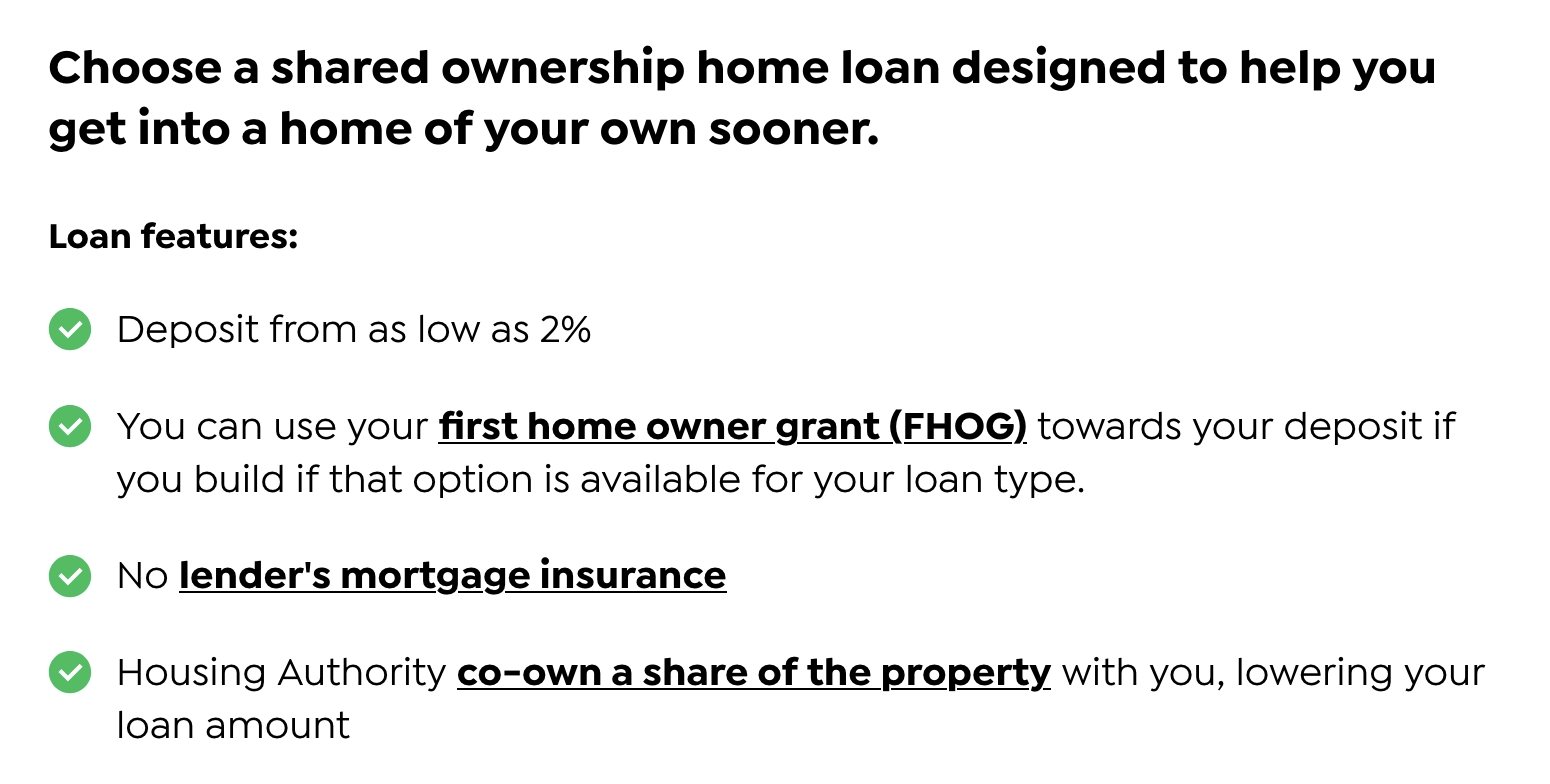

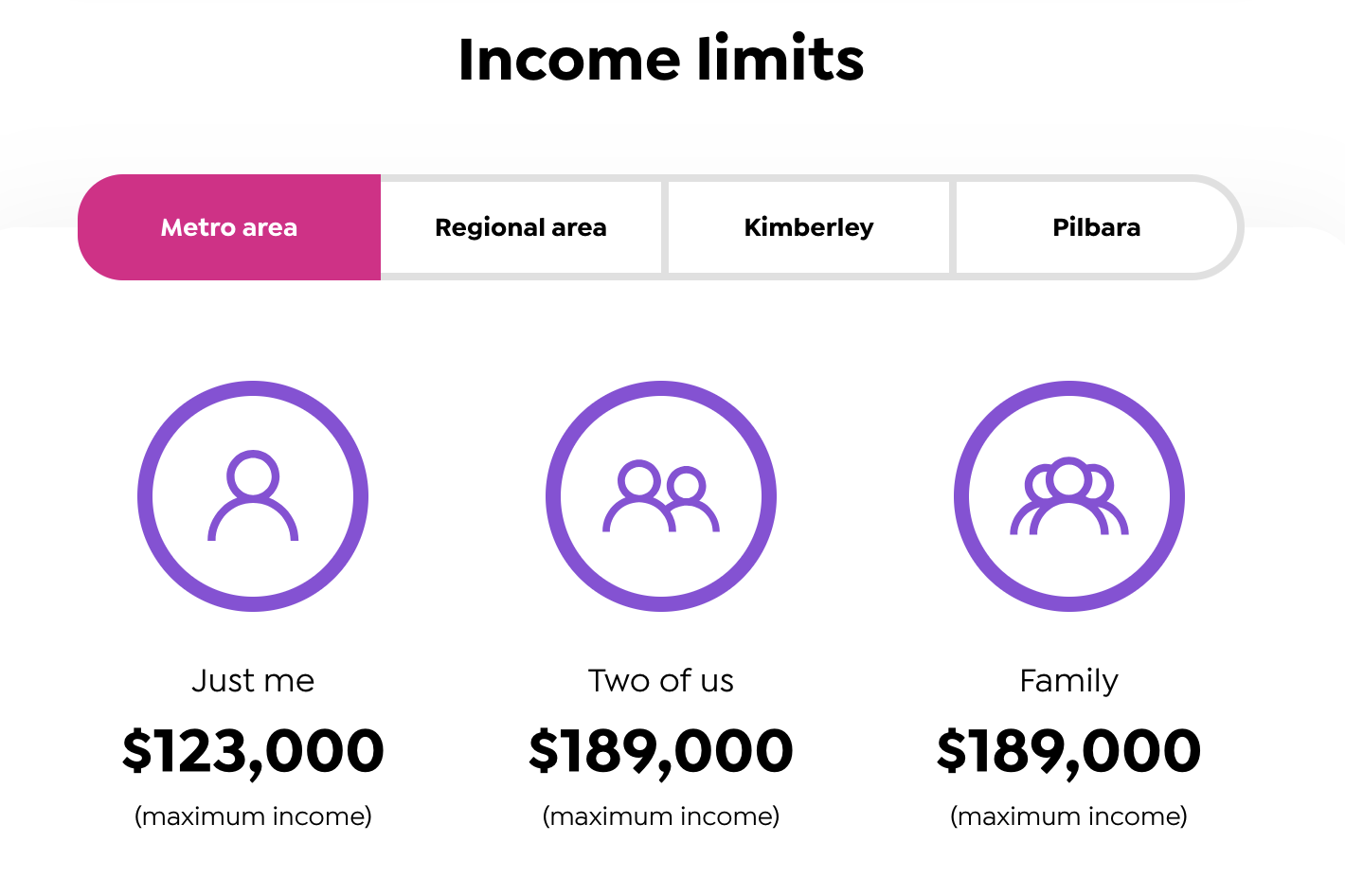

The government can contribute up to 30% of the property value. The buyer only needs to put down as little as 2%. The remaining amount is a loan—also by the government. The best part? There’s no need for lenders mortgage insurance. However, there are income caps: For singles, the annual income limit is $123,000. For couples, it’s $189,000.

But since it’s a government-backed loan, the interest rate is relatively high—currently sitting at 7.35% (variable). There are only 1,000 spots available in the program.

Now, if it were the buyer, I probably wouldn’t make this my first choice. The plan is limited to apartments and townhouses, and the loan interest is steep. Unless I really had no other options, desperately wanted to buy a home to live in, and couldn’t afford a house, then I might consider it.

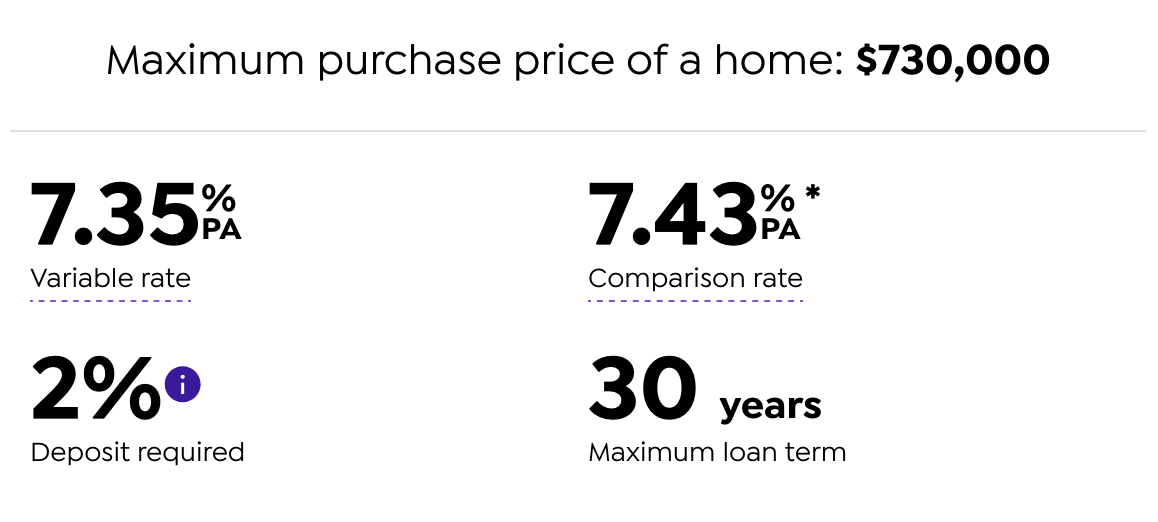

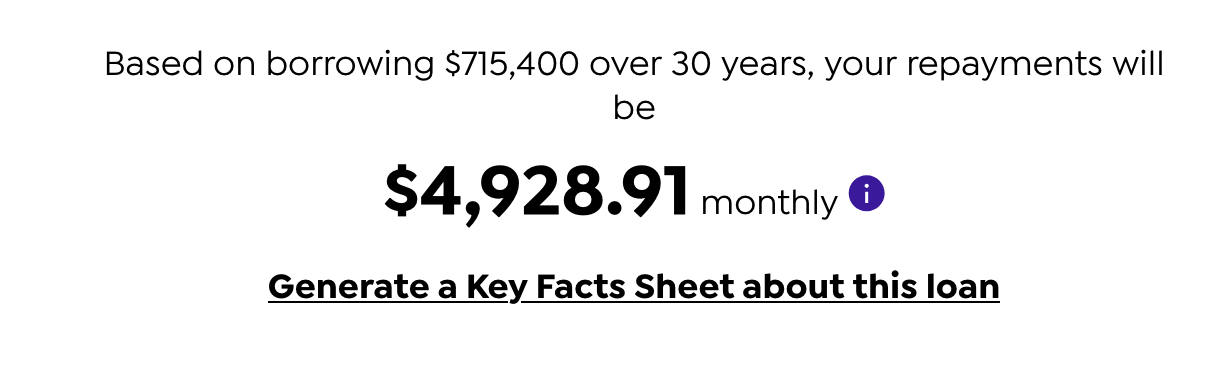

The second support scheme for first-home buyers is much more interesting. Unlike the first one, which is limited to units and townhouses, this one covers houses—including existing homes, new builds, and modular homes (that’s the technical term for prefabricated housing).

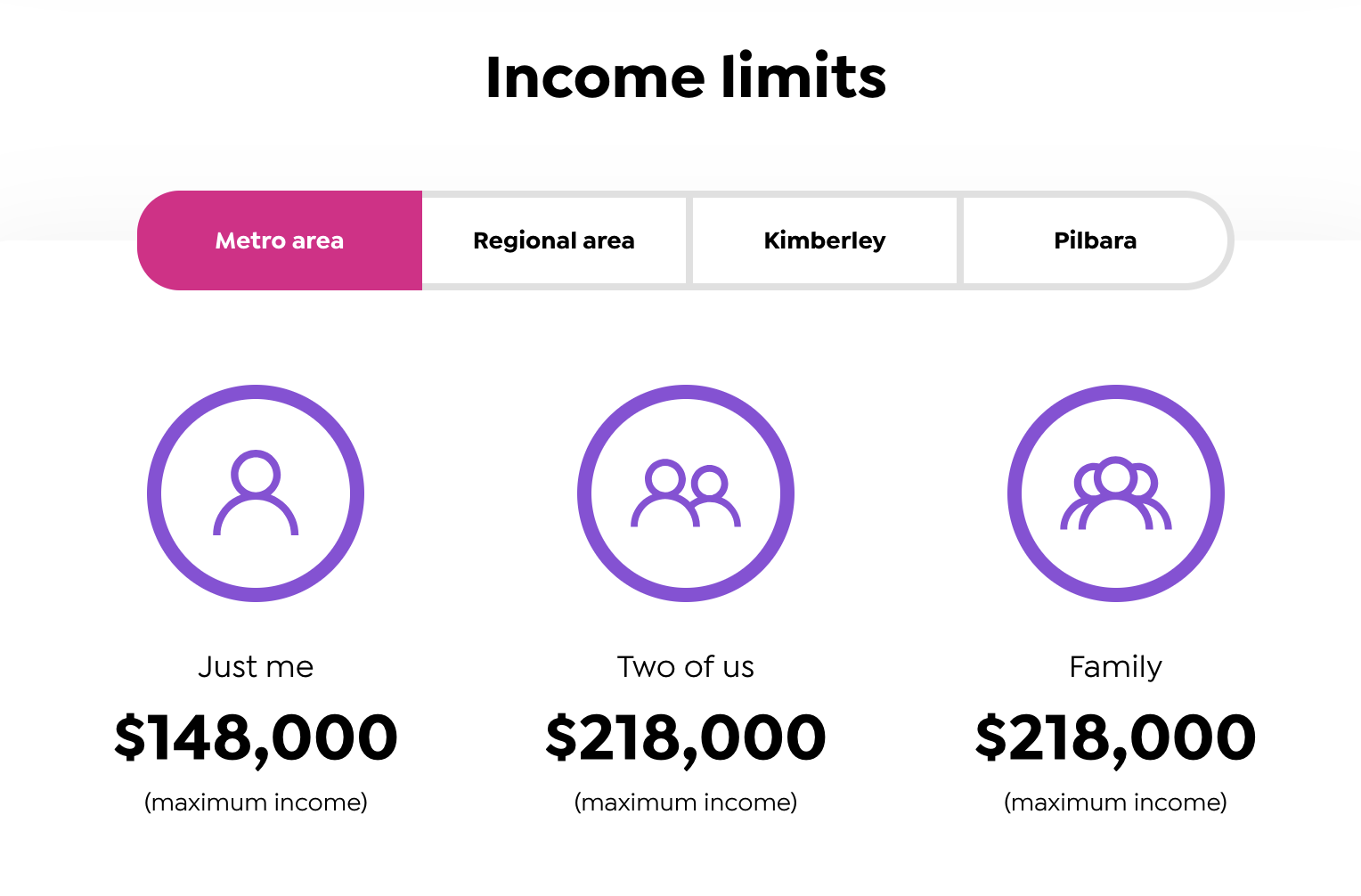

You still only need a minimum 2% deposit; there’s no mortgage insurance, but the property price must be under $730,000. Interest rate? Still at 7.35%. The income limits are higher at $148,000 for singles and $218,000 for couples.

Here’s the key difference: the buyer owns 100% of the property, while the government simply provides the loan. The leverage ratio can go as high as 49:1. That means with just 2% down, you’re borrowing the other 98% at a high interest rate. If you’re buying a $730,000 house, your monthly repayment could hit $5,000. For an average household, that’s a huge cash flow burden.

So here’s my personal view: unless you really have no savings at all, this scheme might not be the best idea. If property prices continue to rise sharply, from an investment perspective, it could pay off. But if the market grows slowly—or worse, drops, you might end up with a negative equity property. It’s a bit of a gamble. Realistically, with $5,000 per month, you could rent a very nice home in WA.

Supply & Demand Are Rebalancing

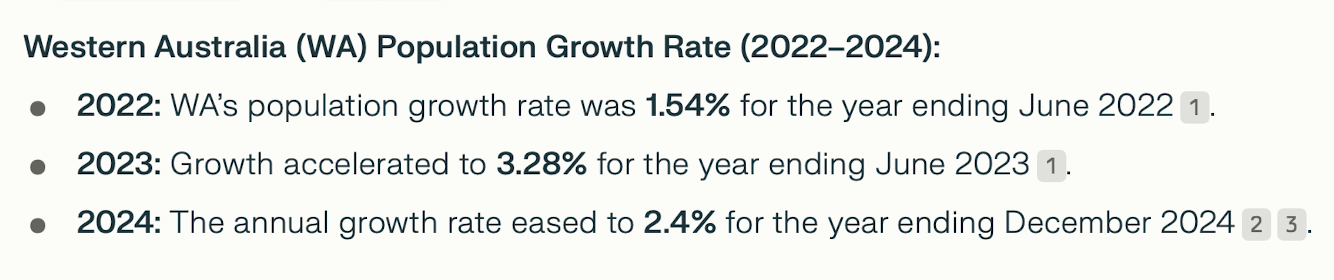

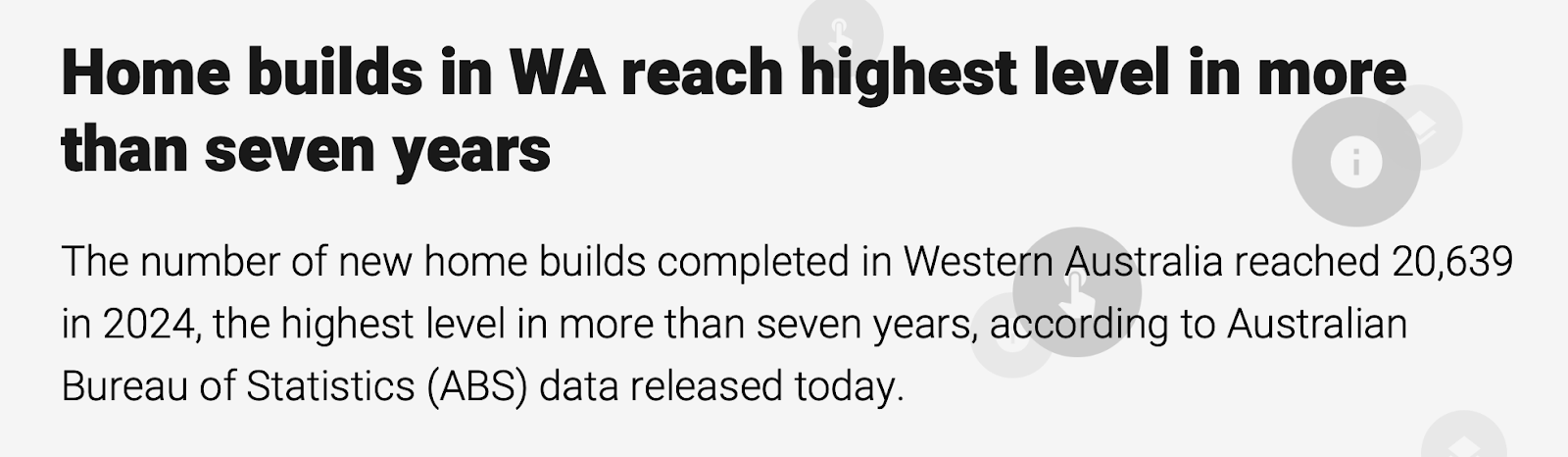

In recent years, WA has had the fastest population growth among all Australian states and territories. And to meet that demand, housing completions have increased rapidly. Today, supply is finally starting to catch up with demand.

The WA government is doing everything it can to encourage property development, attract skilled talent, train construction workers, and draw interstate migration. Overall, while housing supply still lags behind demand, it’s no longer as drastically imbalanced as it was in 2022 or 2023. Which means the explosive growth in Perth house prices we saw back then. That momentum may be fading.

In my opinion, in the short to medium term, unless something unexpected happens, Perth property prices should rise steadily and moderately. With infrastructure improving and public services leading the nation, the quality of life in WA will likely continue rising. That’s why I believe Perth is more suited for long-term investors.

Now that we’ve wrapped up WA, let’s move on to its usual counterpart—Queensland. What’s the economic situation over there? What stands out in their state budget this year? How might their housing market evolve in the coming years? And most importantly, if you’re considering buying an investment property—which state makes more sense: WA or QLD?

Let’s dive into that next.

Queensland Budget 2025–26

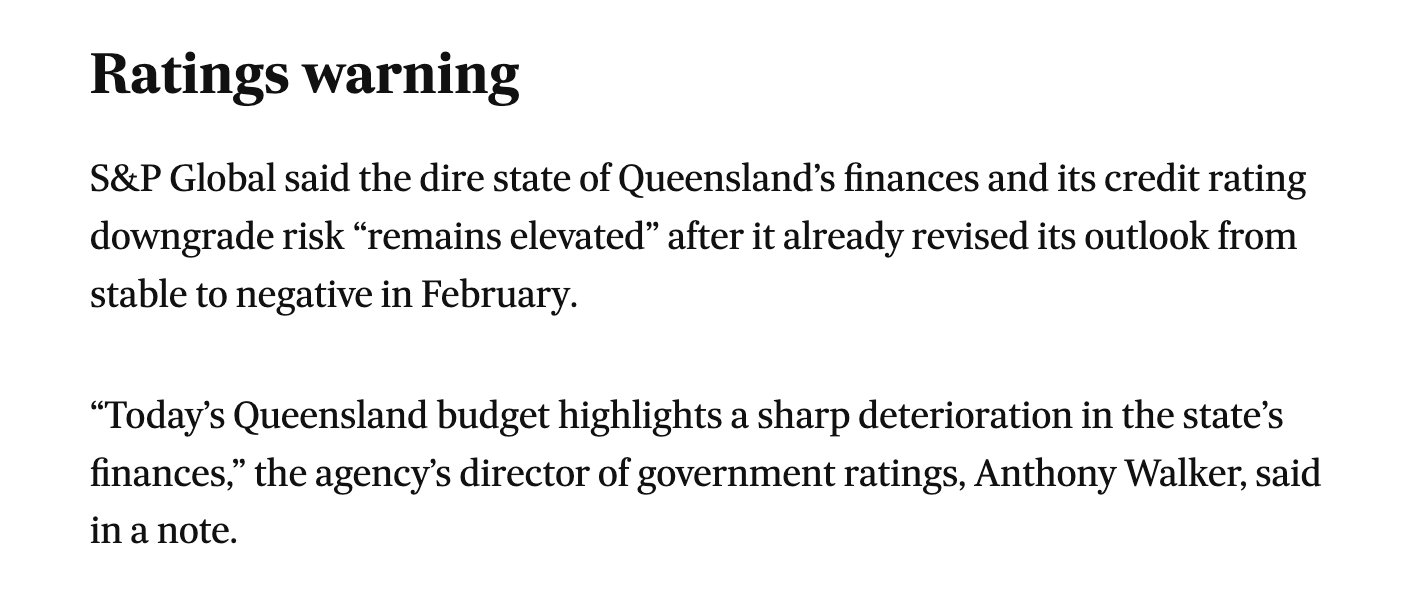

Queensland's finances are undeniably slipping. Last Tuesday, the Queensland Government released its 2025–26 state budget—and the moment the numbers came out, I got a shock. Why? Because the debt projection is now almost $20 billion higher than what was forecasted just last year. Even international ratings agency S&P couldn't ignore it. They issued a formal warning, stating that Queensland's finances had suffered a "sharp deterioration."

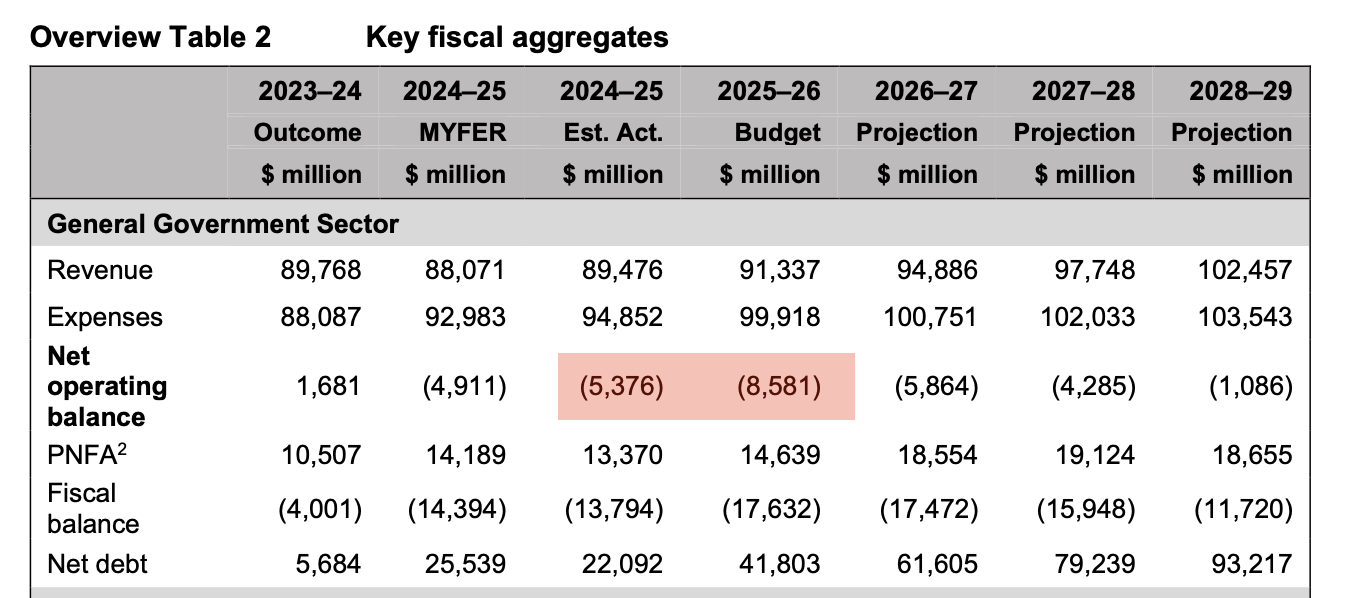

This is the first budget under the Liberal National Party after more than a decade out of power. It was meant to mark a fresh start. But the numbers? Frankly, they're alarming. The budget forecasts a massive $8.6 billion deficit next year, up $1.7 billion from previous estimates—and there's not a single surplus in sight over the next four years.

What's the government's explanation? They're blaming a few things: A collapse in coal royalty revenue; unfair GST distribution, with funds diverted to support Victoria; And of course, they've pinned a big part of the blame on the former Labour government, accusing them of poor fiscal management that left a mess behind.

Honestly, finger-pointing isn't surprising. Anytime a new party takes over, they use the opportunity to trash the previous government—it's politics 101. But to get to the truth, just look at the numbers’

Queensland will run budget deficits every year for the next four years, and even though the size of the deficits may shrink, total debt will keep climbing, reaching $205.7 billion by 2028–29. S&P has made their stance clear: Queensland's credit rating remains at risk. They already downgraded the state's outlook from "stable" to "negative" back in February, and this budget confirms their concerns.

S&P's official statement reads: "This budget shows Queensland's fiscal position has deteriorated significantly." They also emphasised that the new government hasn't introduced any major fiscal reforms. The reality is this: 1.Deficits every year; 2.Soaring infrastructure spending; 3.And most of it being funded through borrowing.

Will Property Investors Be Targeted Next?

Naturally, many people are now asking: If Queensland's finances are deteriorating, will property investors be the next target—like in Victoria? We don't have time here to go into a detailed comparison, so I'll just make two key points,

Queensland is governed by the Liberal National Party. Their focus is typically business, economic growth, and productivity. They prefer to spend money in ways that generate returns and stimulate investment. Victoria, on the other hand, is governed by the Labor Party, which tends to focus on redistribution and supporting lower-income groups, often at the expense of business and investors. So I have more confidence that Queensland will look for fiscal solutions other than punishing property investors.

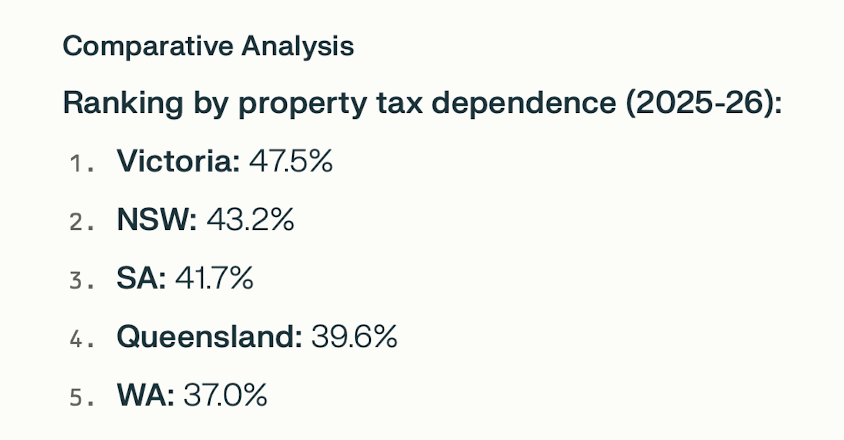

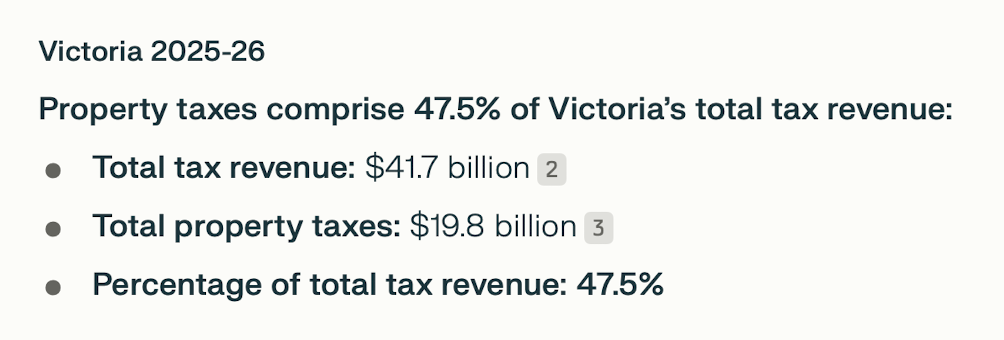

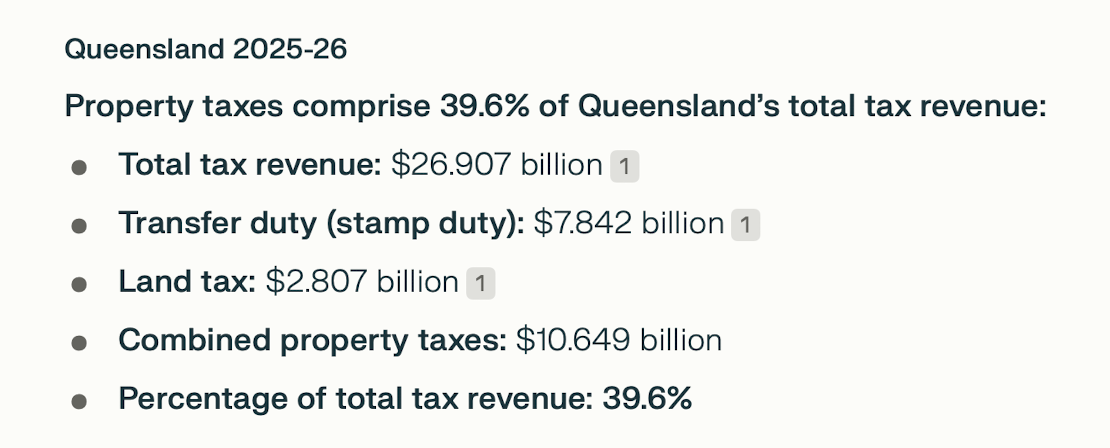

Let's look at how dependent each state is on property taxes. In Victoria, 47.5% of total state tax revenue comes from property-related taxes—the highest in Australia. In Queensland, it's only 39.6%. That means in Victoria, just a small policy change in the property sector has a big impact on the state's budget. In Queensland, however, property tax makes up less of the pie, so any significant increase in revenue would require much more drastic changes, which are harder to implement without triggering a backlash.

So if we ask which state is most likely to "milk" property investors in the future, it's: Victoria, most likely, Then New South Wales, Followed by Western Australia, And Queensland comes in last—for now.

My view is that Queensland won't follow Victoria's lead when it comes to anti-investor tax policies—at least not in the short to medium term.

Now, since the budget predicts ongoing deficits and a growing debt burden, let's ask the real question: Are they wasting the money? Or are they investing it in projects that turn $1 into $2 in return? For us property investors, the most important area to watch is infrastructure.

Queensland's Infrastructure Investment

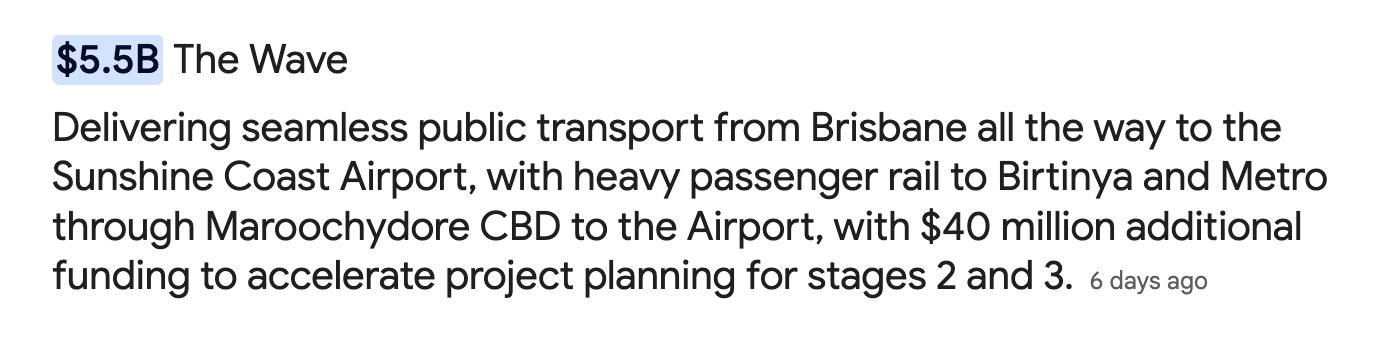

When it comes to infrastructure, Queensland is going all in. Let's start in the north, with the massive "Wave" project—a transport corridor connecting Brisbane to the Sunshine Coast Airport. This includes rail upgrades, light rail extensions, and more. It's expected to significantly improve connectivity, boost tourism, support commuter movement, and drive growth in hospitality, retail, and residential development.

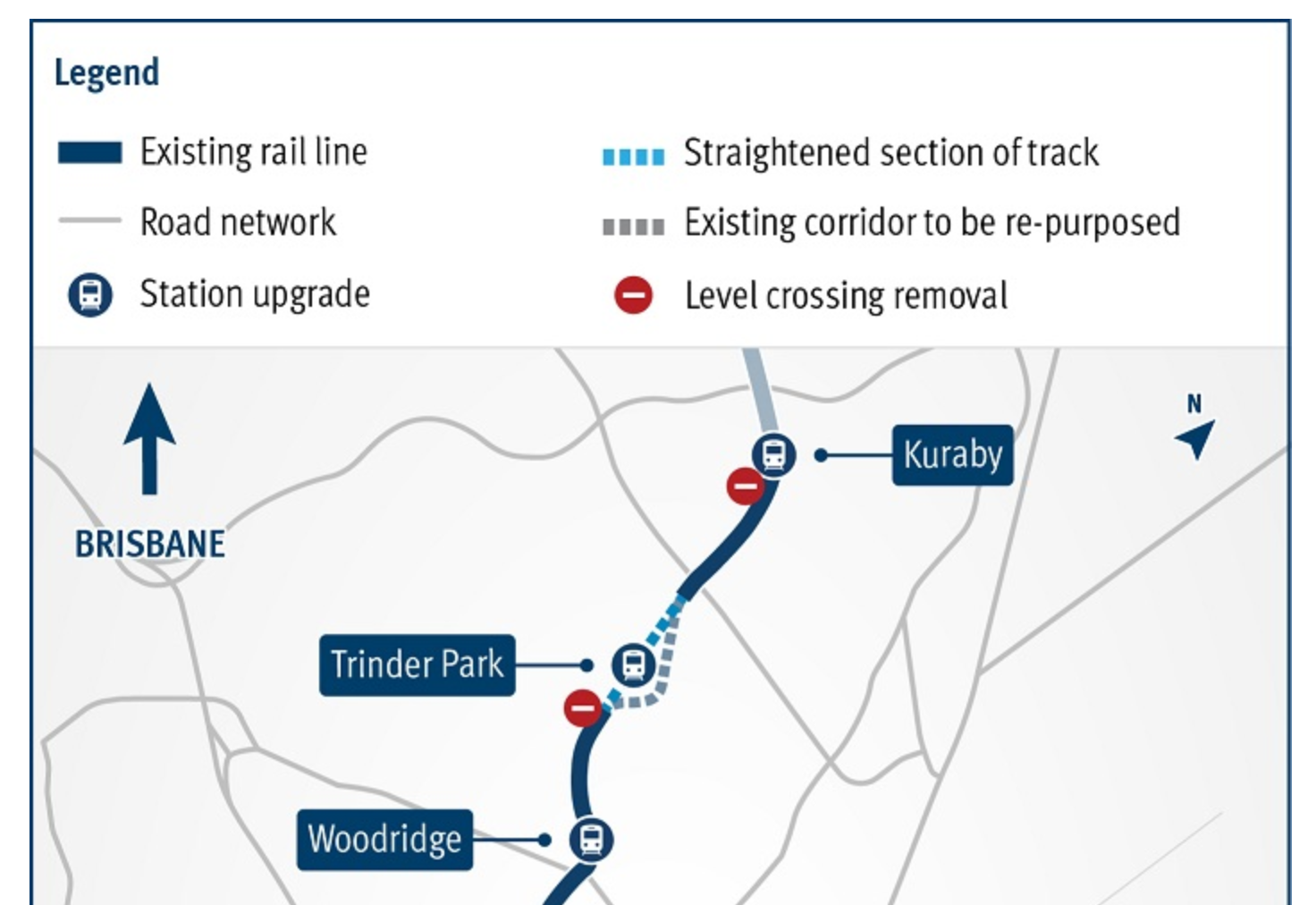

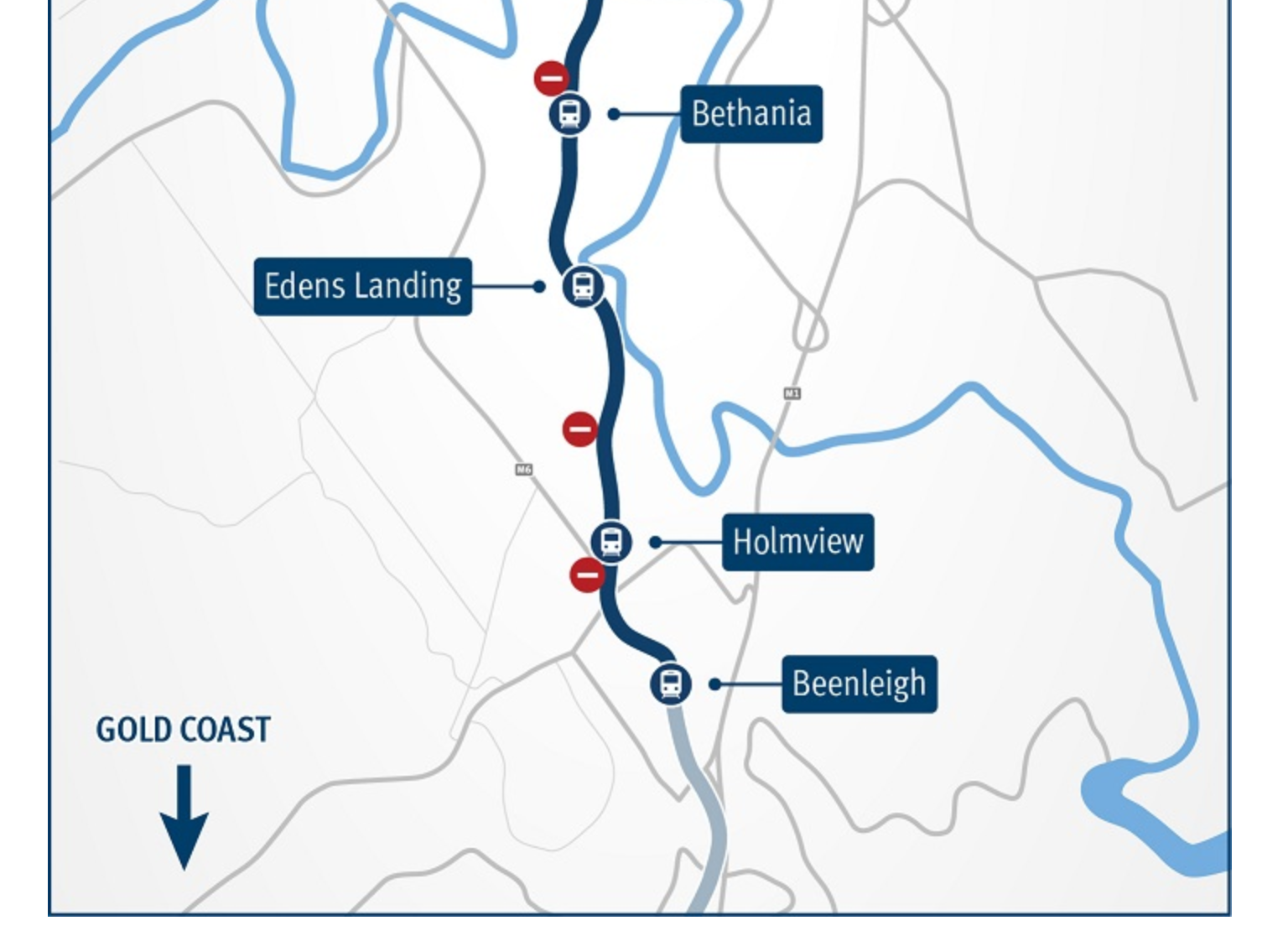

In the south, the government is investing heavily in the Logan and Gold Coast regions—specifically in rail upgrades to increase speed and capacity, making commuting between Brisbane and the Gold Coast faster and easier. This will improve labour mobility, attract business investment, and create strong upward pressure on property prices along the route.

To the west, Ripley Town Centre is getting a complete makeover. Shopping centre expansions will kick off in early 2026. The area already has a growing mix of detached homes and townhouses, and a new train line is under construction. The core area will feature commercial, office, and residential towers, turning it into a fast-growing satellite city.

Ripley is located within Ipswich Council, which is projected to be the fastest-growing LGA in Queensland over the next two years. Many of our VISION members have already invested there, thanks to our exclusive access to both listed and off-market deals.

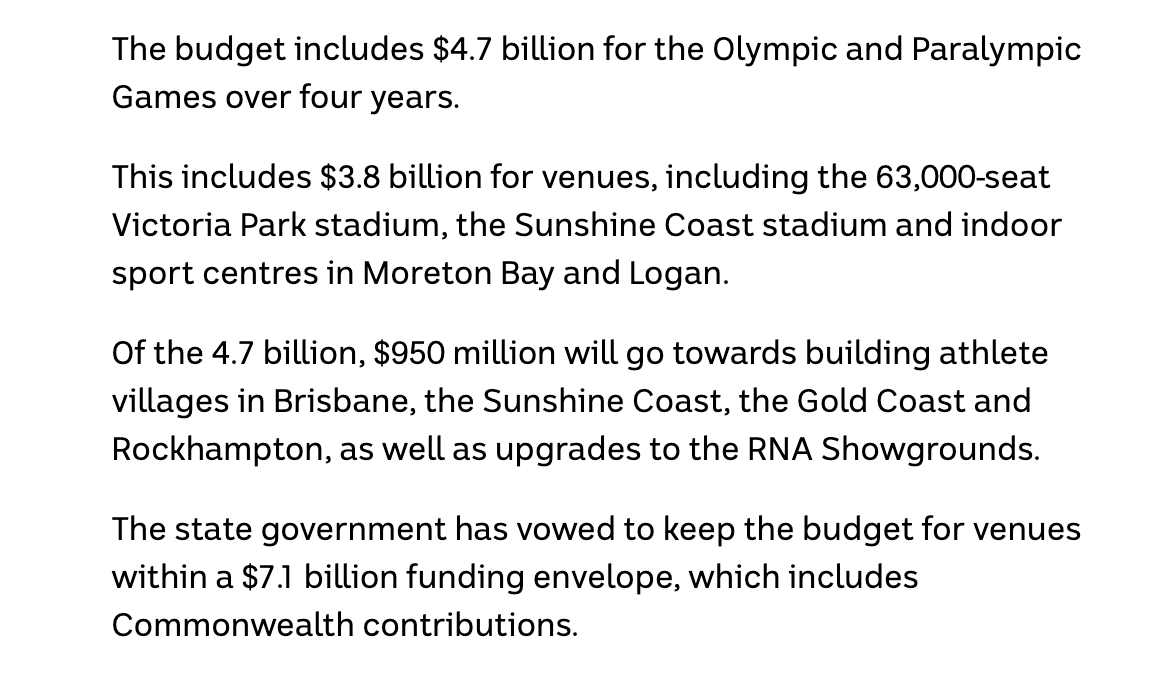

Let's not forget the Olympics—$4.7 billion in funding from the Queensland government, plus $7.1 billion from the federal government. This will support venue construction and upgrades including: Victoria Park Stadium, Gold Coast Stadium, Logan and Moreton Bay indoor centres and new Olympic villages across Brisbane, Gold Coast, and Sunshine Coast. Let's just hope that once the Games are over, these Olympic facilities don't go to waste—and are converted into housing or hotels that can generate ongoing value.

Queensland is spending big on infrastructure. They're opening up north–south connectivity, driving growth in facilities, the economy, and property prices along the way. And most importantly? They're investing in projects that create value. Even if it means borrowing more now, the long-term return will be worth it. This is a completely different approach from Victoria—where every $1 spent on infrastructure seems to return just 60 cents.

So no, I don't believe Queensland's debt levels are a real concern—not with this level of strategic investment. And don't forget—Queensland still has its resources. If commodity prices surge again, and if the federal government improves GST distribution, Queensland could easily return to the massive surpluses we saw just two years ago. Victoria? Not a chance.

First Home Buyer Grant

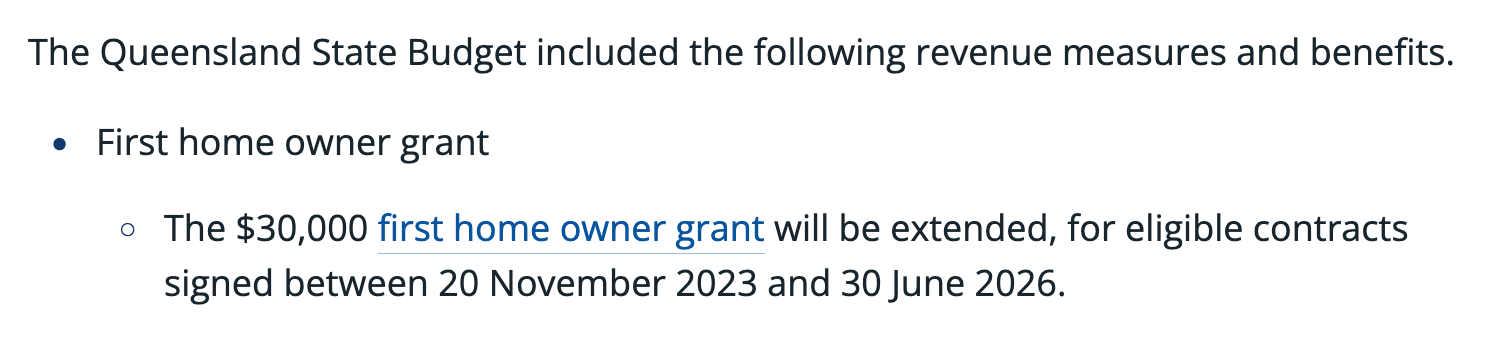

In this year's budget, Queensland has increased its support for first-home buyers once again. The existing First Home Buyers Grant has been extended for another year. As long as you sign a contract between November 20, 2023, and June 30, 2026, and meet the criteria, you can receive a one-time grant of $30,000.

The detailed eligibility rules are on the Queensland Revenue Office website, but to put it simply, You must be an Australian citizen or permanent resident. It must be your first time buying a newly built home to live in. And the property price must be under $750,000. Other existing stamp duty concessions remain unchanged—you can also find the details on the official website.

Boost to Buy

Now, here's the biggest news: Queensland has launched its own version of a shared equity scheme called "Boost to Buy"—and it might just drive price movements in certain market segments. So what's the deal?

The Queensland Government will co-purchase a home with eligible first-home buyers—just like two friends teaming up, each putting in money and sharing ownership. The government's contribution is not a loan, so there's no interest to repay.

However, the buyer must pay for all property-related costs, including utilities, council rates, insurance, and so on. And when the property is sold, the government receives a share of the profits based on their ownership percentage. For new homes, the government can contribute up to 30%. For existing homes, up to 25%. Buyers only need a 2% deposit, meaning you're using 49x leverage. Even more surprising, the income cap is quite high: Up to $150,000 per year for singles; Up to $225,000 for couples. And the maximum property price is $1 million.

So this policy isn't targeting people with no money or earning power—it's clearly aimed at middle-class buyers who earn well but lack cash savings. To me, it feels like the government is saying: "Even if you make $150k a year in Queensland, you still can't save enough to buy a basic house." Applications open at the end of 2025, and the program is expected to offer up to 1,000 spots.

Let's be real: You barely put in any cash and no mortgage insurance; You still get to own about 70% of the property. And if the property goes up in price, you keep most of the profit. Where else can you find a deal like that? The loans come from regular banks, not government lenders—so the interest rate is market-based, about 1% to 1.5% lower than WA's government-backed scheme. There's only one small catch: If property prices fall after you buy, you could easily end up in negative equity because, technically, you only own 2% at the start.

Still, my personal take is that "Boost to Buy" won't move the needle on Queensland's overall housing market since it only affects 1,000 properties. But for well-located homes under $1 million, with good transport access, it could absolutely boost demand and prices. And compared to WA's shared equity model, the terms are much more attractive for buyers.

Quick Summary

Let's wrap this up. The average property prices in QLD and WA are fairly similar, and the economic size of both states is comparable. So where should you buy? If it's for owner-occupancy, the answer is simple: Buy locally. No need to overthink. If your goal is to make money, and you're open to moving but not sure where to go, then Queensland is your best bet—because it offers the most generous first-home buyer support in Australia. They're not just making promises—they're putting real money on the table. If you're buying an investment property and you're already in Melbourne, just buy in Melbourne. Honestly, 90% of Melbourne residents buy only in Melbourne, and no matter what I say, that mindset is not going to change.

But if you're open to other options, here's how I'd rank it: First property in Queensland; Second property in Western Australia. And keep in mind—this is about the long-term view. Right now, there's no evidence of any short-term boom, where prices rise 20% in a single year. That kind of growth just isn't happening. The fundamentals are not there. If you've got a bigger budget, then buying a standalone house in a mainstream Sydney suburb is also a solid choice. Just be prepared to spend at least $3.5 million.

Watch the video version of the blog on YouTube.