Boom, Pause, Panic|RBA Shocks the Market|Is This the End of Australia's Housing Boom? [APS088]

Have you noticed what's been happening in the Australian housing market in the first half of 2025? With no warning signs, the market suddenly took off. While many were still waiting for the much-anticipated third rate cut to finally "drop," home prices had already quietly risen for five straight months. And in June, the national property price index continued its upward climb—not only showing no signs of slowing down but accelerating even faster than in April and May. Nothing stops this train. Yet just as the market was gaining full momentum, the Australian Central Bank, RBA, made a surprise move: they paused the rate cuts. This unexpected decision has thrown a curveball into the market. So what exactly does this mean? Is this the end of the housing market's rapid upswing? Or could this be the last chance for property buyers to get on board?

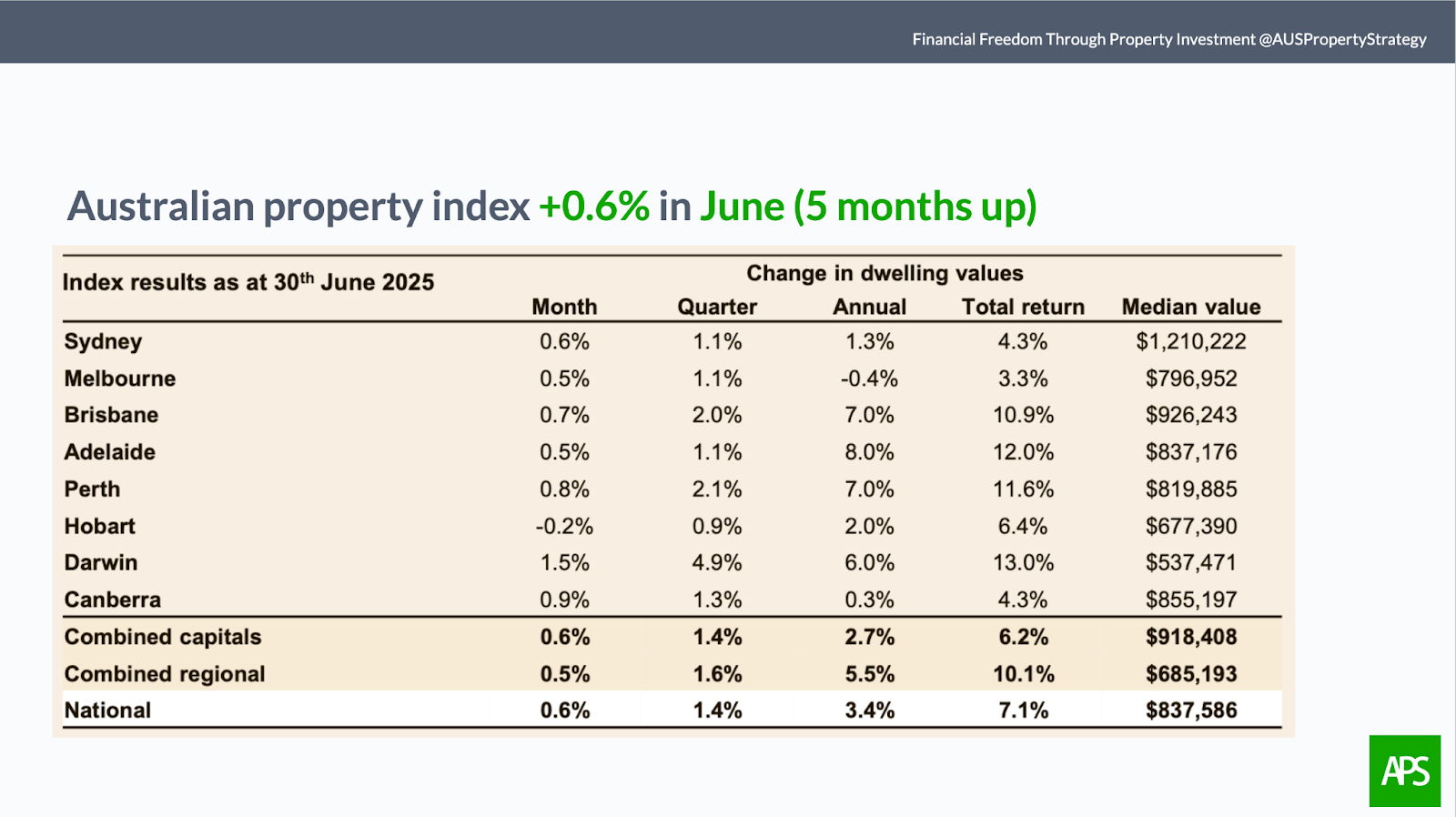

Property Market Accelerates Sharply in June

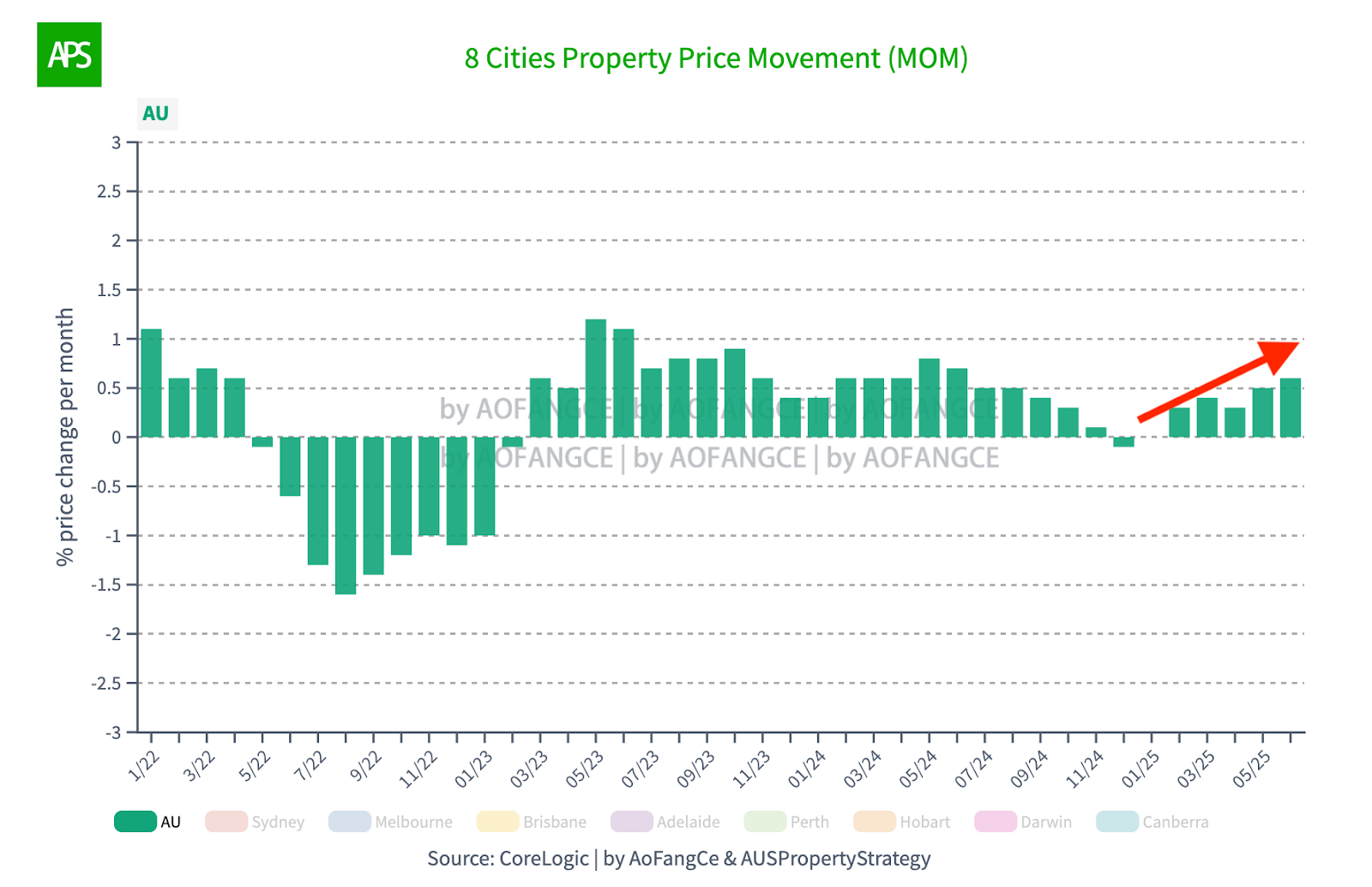

Ever since the Australian housing market hit bottom with a 0.1% drop in December 2024, it has entered a crucial rebound phase. Prices rose steadily in January, February, and March—each month faster than the last. The key turning point came in February. In April, growth slowed slightly. This was due to the uncertainty surrounding the federal election and also because the impact of February's rate cut had begun to fade. But once the election settled and another rate cut followed, June brought a strong rebound: national home prices jumped 0.6% in just one month. If you connect the monthly growth curve for the first half of the year, you'll clearly see a steadily accelerating upward trend.

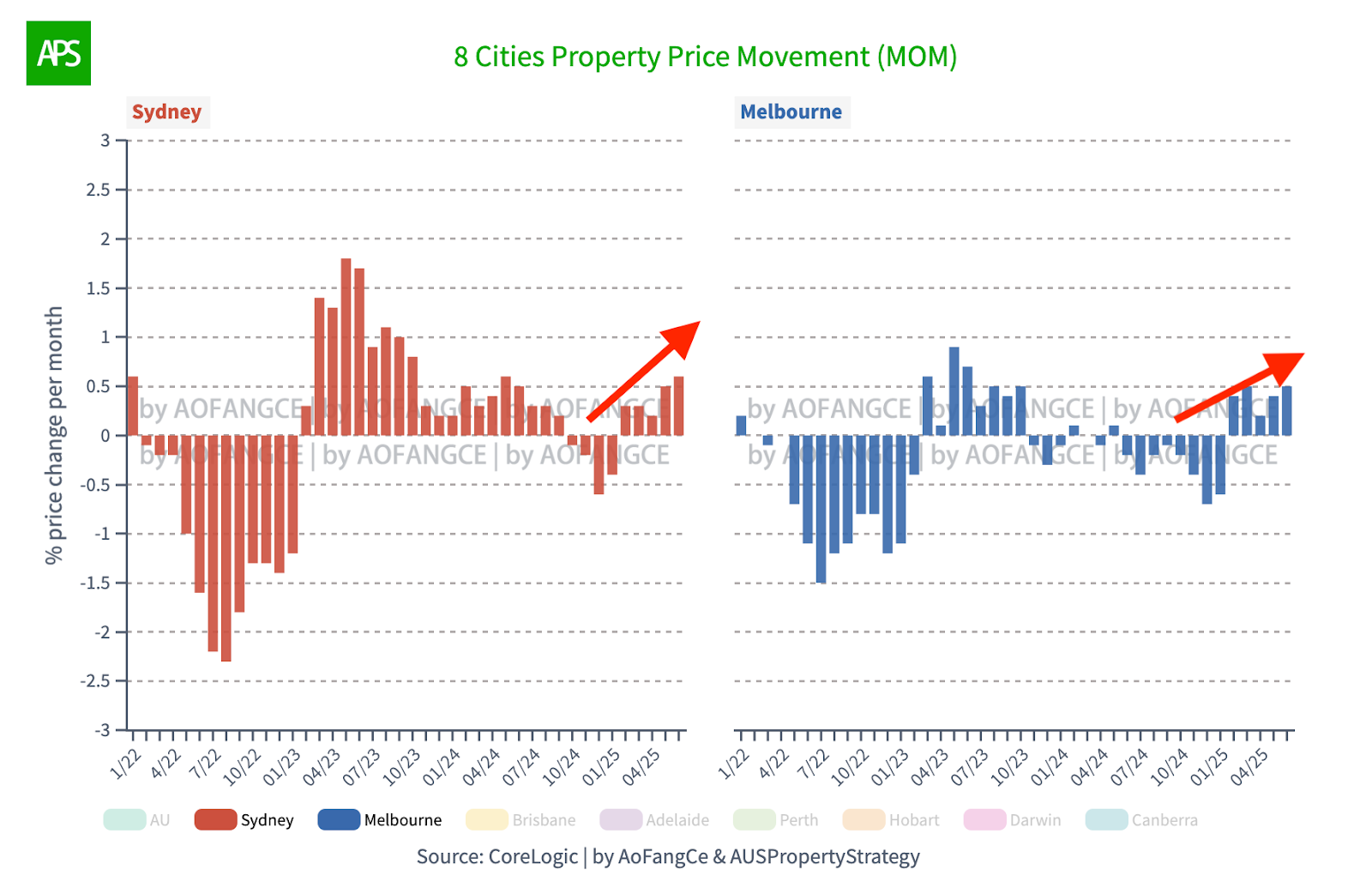

Sydney's housing market rose 0.6% in June alone—an obvious acceleration. Melbourne followed a similar pattern, with a 0.5% monthly increase. While the city hasn't yet broken through our "flat market" threshold of ±0.5%, the trend is crystal clear. It's only a matter of time. If you zoom out over a longer period, the V-shaped recovery becomes even more visible. Sydney saw price growth peak in April 2023, bottom out in January 2025, and is now clearly in an upswing. Melbourne's rebound isn't as sharp as Sydney's, but the trajectory is the same.

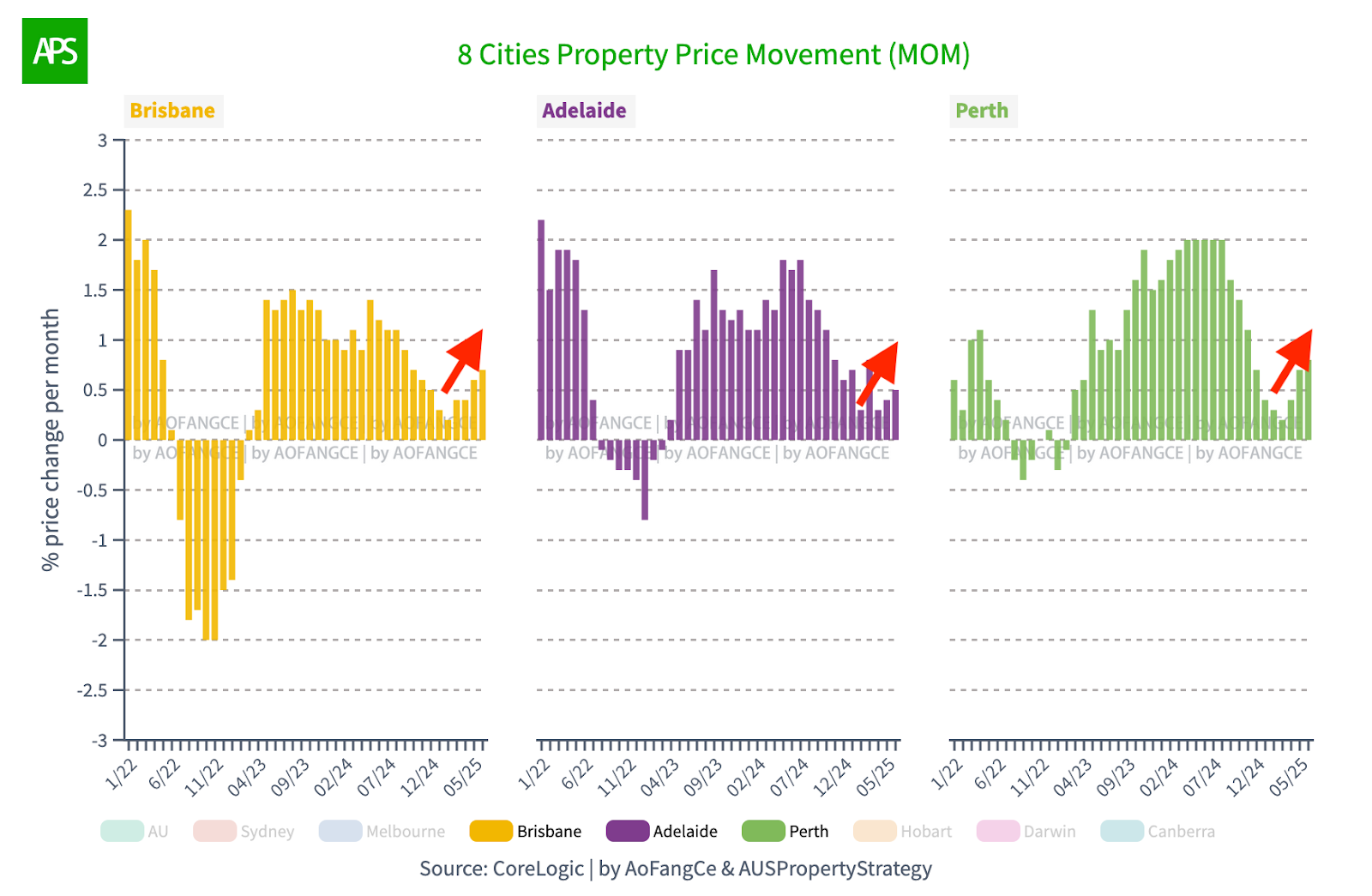

Now let's look at the three mid-sized cities: Brisbane, Adelaide, and Perth. All three have been rising continuously for over two years. Although their pace of growth dipped slightly in February, they still managed to record positive gains that month. Then, from March to June, they entered four consecutive months of accelerating growth. In June, Brisbane's home prices rose by 0.7%, confirming it has now entered a clear upward cycle. Perth jumped 0.8%, picking up pace. Adelaide rose 0.5%, a slightly more modest but still positive increase. It's clear now: Brisbane and Perth have completed a V-shaped recovery without ever entering a period of negative growth, just as we predicted in our year-end live webinar back in November last year. I wonder if those who were worried two years ago that these three mid-sized cities had already peaked actually ended up buying.

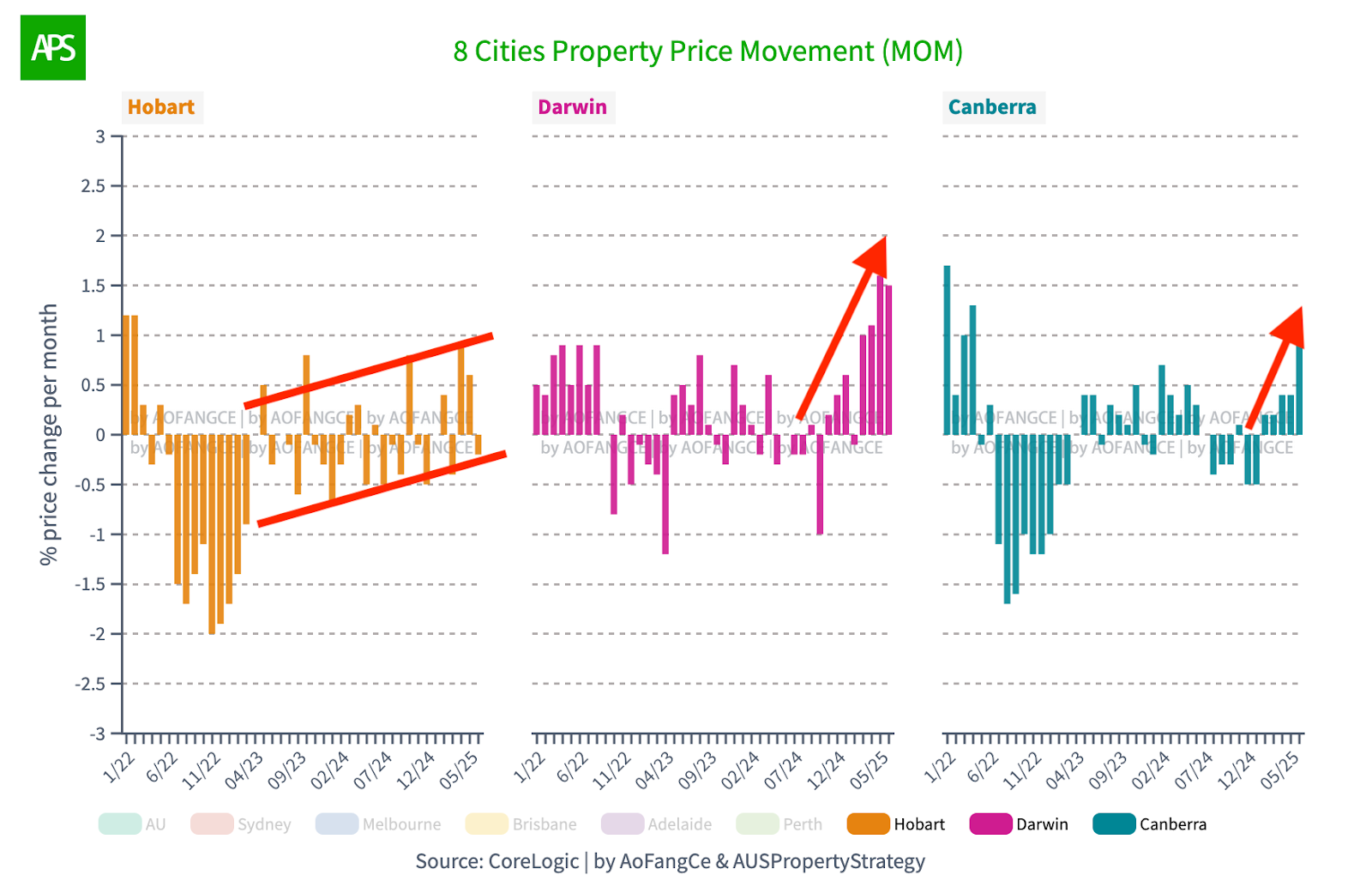

This time, the three smaller capital cities are showing a slightly different pattern. Hobart hasn't developed a clear upward trend yet. Over the past two years, prices have fluctuated up and down. But overall, the market is improving. Darwin, on the other hand, is continuing its explosive upward trajectory. As for the reasons behind this surge, I gave a detailed explanation during last Saturday's mid-year livestream. It's a good time to buy in Darwin, but only for seasoned investors who know what they are doing. The real surprise this time came from Canberra. It posted a sharp 0.9% increase in a month, clearly entering an upward cycle. But the question is whether this momentum can last. And if it can, for how long? After all, in the past two years, Canberra has gone through several mini-cycles where prices rose for a few months, then fell again.

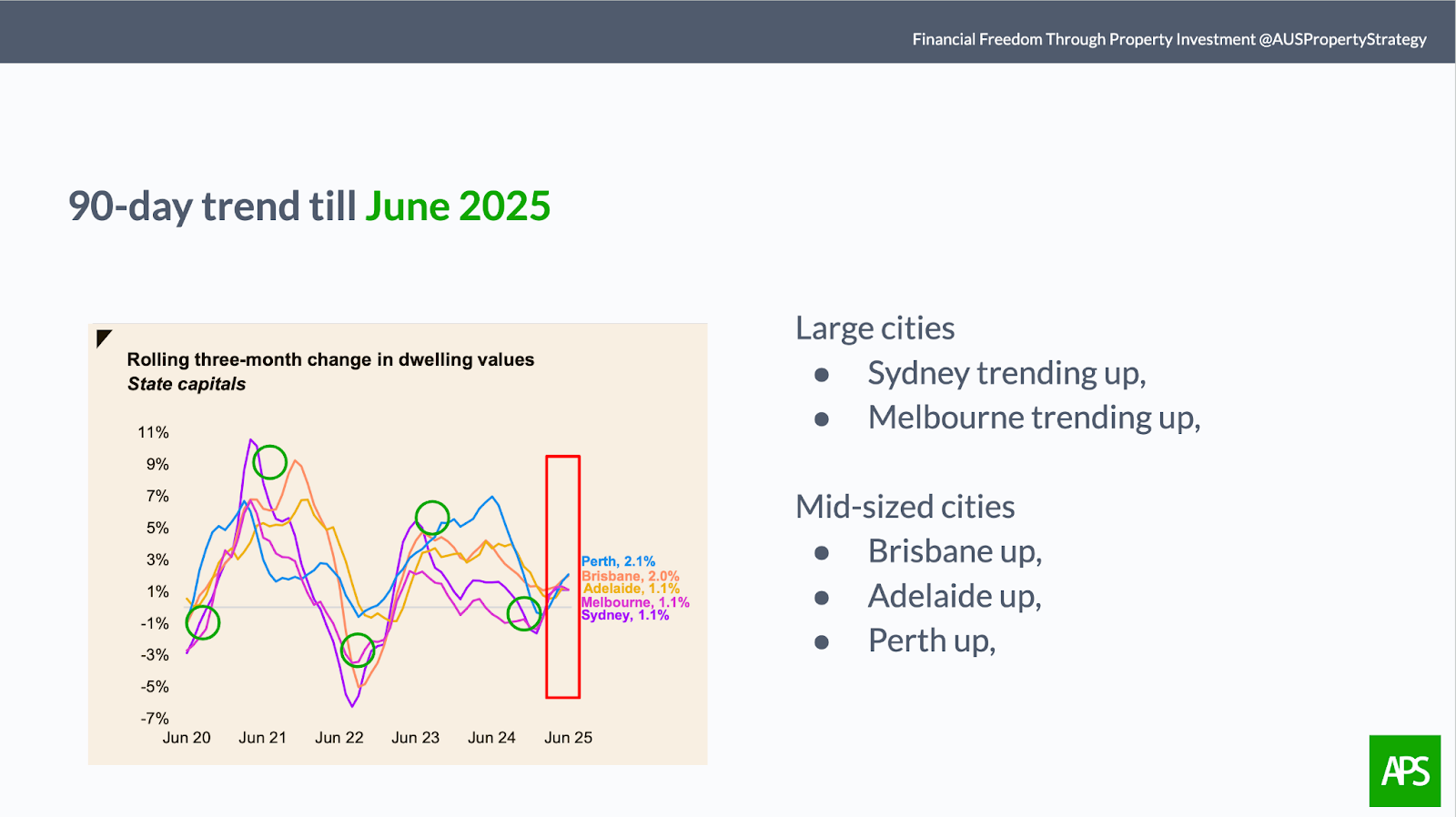

That wraps up the month-on-month movements across all capital cities. But if you want to read the trend more clearly, the best way is to look at the 90-day charts. When you stretch the timeline to a full quarter, it smooths out the volatility and gives a much clearer picture of the overall direction.

From the chart, it's easy to see that all large and mid-sized cities are now firmly in an upward cycle.

There are five green circles on the graph—those mark the five points in the past five years when I made predictions about the market's direction. And all five turned out to be spot-on. Most recently, my forecast from our year-end livestream last November—about the housing market's performance in the first half of this year—has also been proven correct. You could say I've been incredibly lucky.

As for auction clearance rates, the June numbers were outstanding. The national clearance rate rose to 67%, already surpassing the 10-year average of 65%.

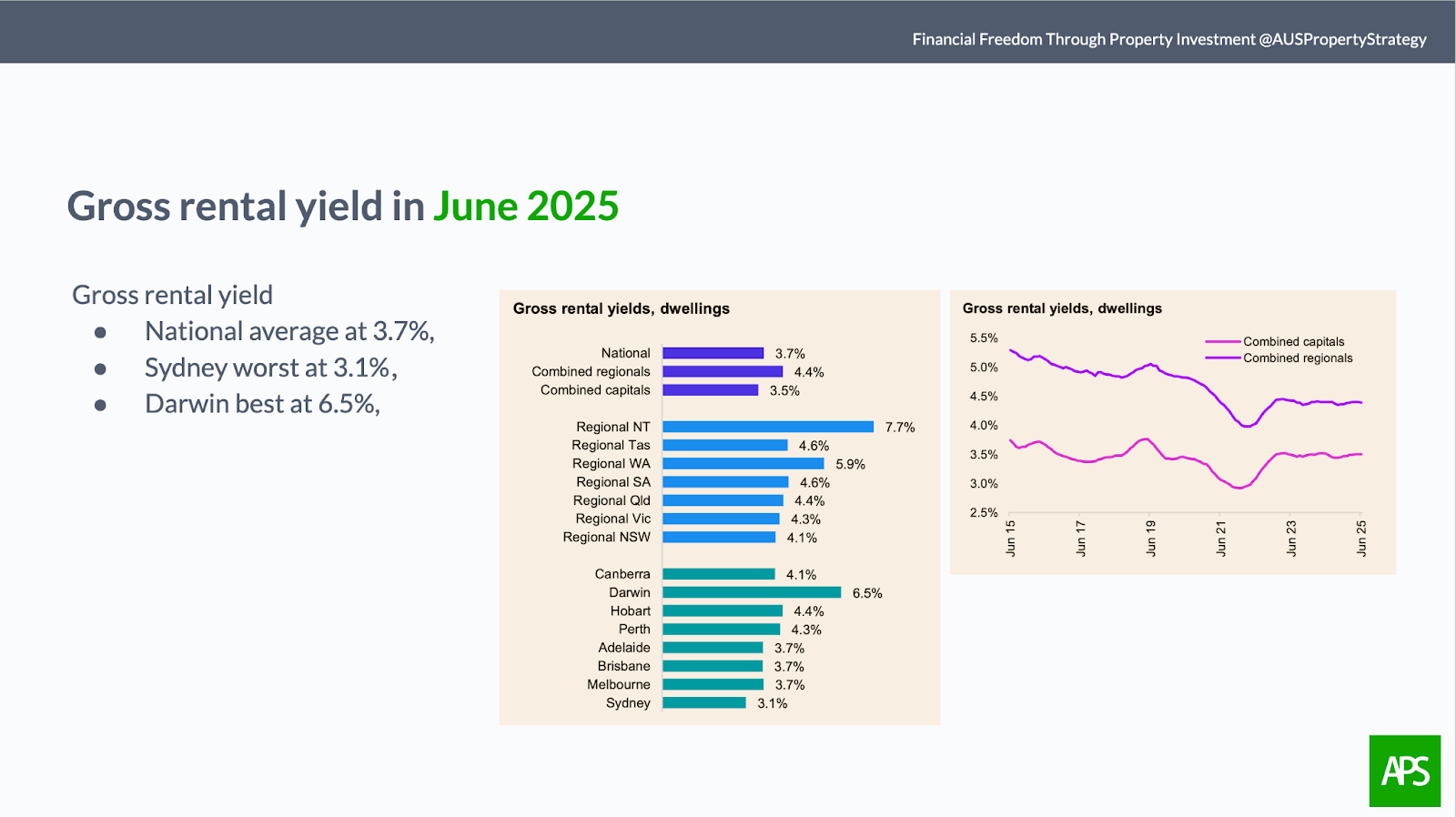

Rental yields didn't change much. The national average yield in June remained at 3.7%. Sydney's yield is the lowest at 3.1%, due to its relatively high property prices. Darwin continues to offer the highest returns, with a yield of 6.5%. Adelaide, Brisbane, and Melbourne all sit around 3.7%. Given current interest rates and an 80% loan-to-value ratio, Darwin is the only market in Australia where a long-term rental property could still deliver a positive cash flow. But I want to be very clear: positive cash flow alone should never be the sole reason for buying an investment property. Capital growth potential, long-term stability, local population quality, economic development, and economic diversity are all critical factors.

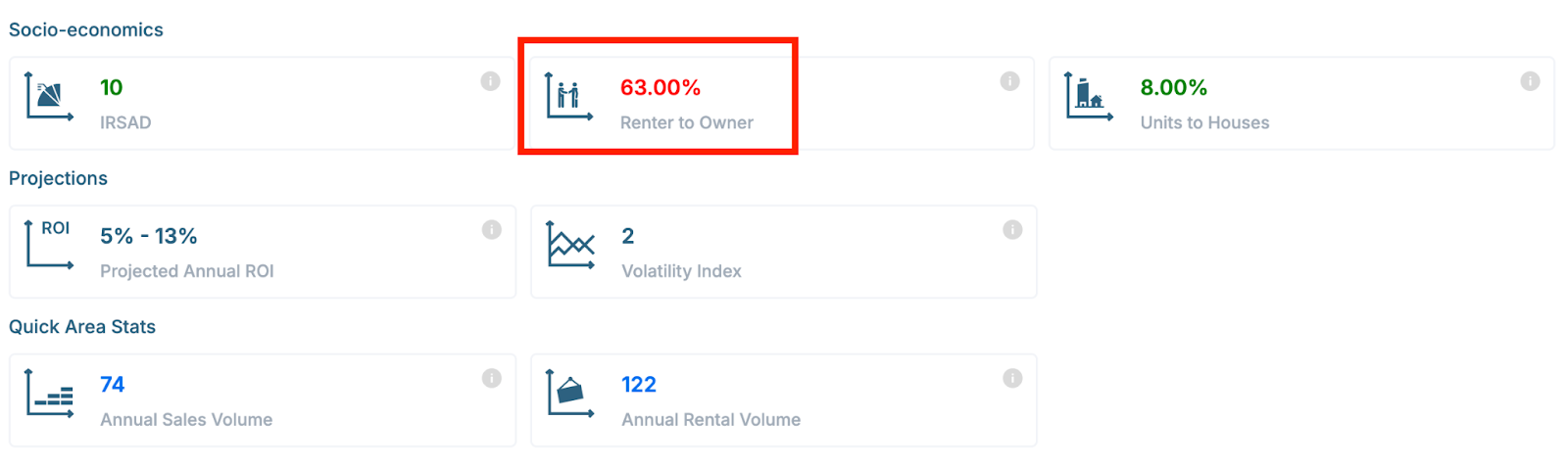

I had a client ask me the other day whether a property in a small town in Western Australia was worth buying. The cash flow looked excellent. On the data platform, it showed a price around $800,000, with weekly rent between $1,200 and $1,400—and that's on a long-term rental. Not bad.

But when I looked closer, I found that property prices in that area had huge swings—classic mining-driven volatility. And the proportion of renters was a staggering 63%. So I told the client: if you want to play a short-term game, maybe. But this is absolutely not suitable for long-term investment. If you're going for a short-term play, why not go all in? Borrow money, buy leveraged ETFs or even crypto—that's the real rollercoaster. You may receive your results in a few days. Of course, I'm joking. To all our AusPropertyStrategy followers: please don't do that.

By the way, I serve as the Head Trainer and Senior Data Analyst at that data platform. I train buyer's agents across Australia on how to conduct proper data analysis.

So, the first half of 2025 saw property prices bottom out in terms of growth rate, followed by a full-on upswing. But the second half of the year? It's not going to be as smooth. While the overall trend still looks positive, there's now a major variable on the demand side—interest rates. And this time, the rate cut everyone had been hoping for… didn't happen. So, what's going to happen in the market over the next few months? And where are interest rates heading from here? Let's take a closer look.

RBA Pauses Rate Cuts

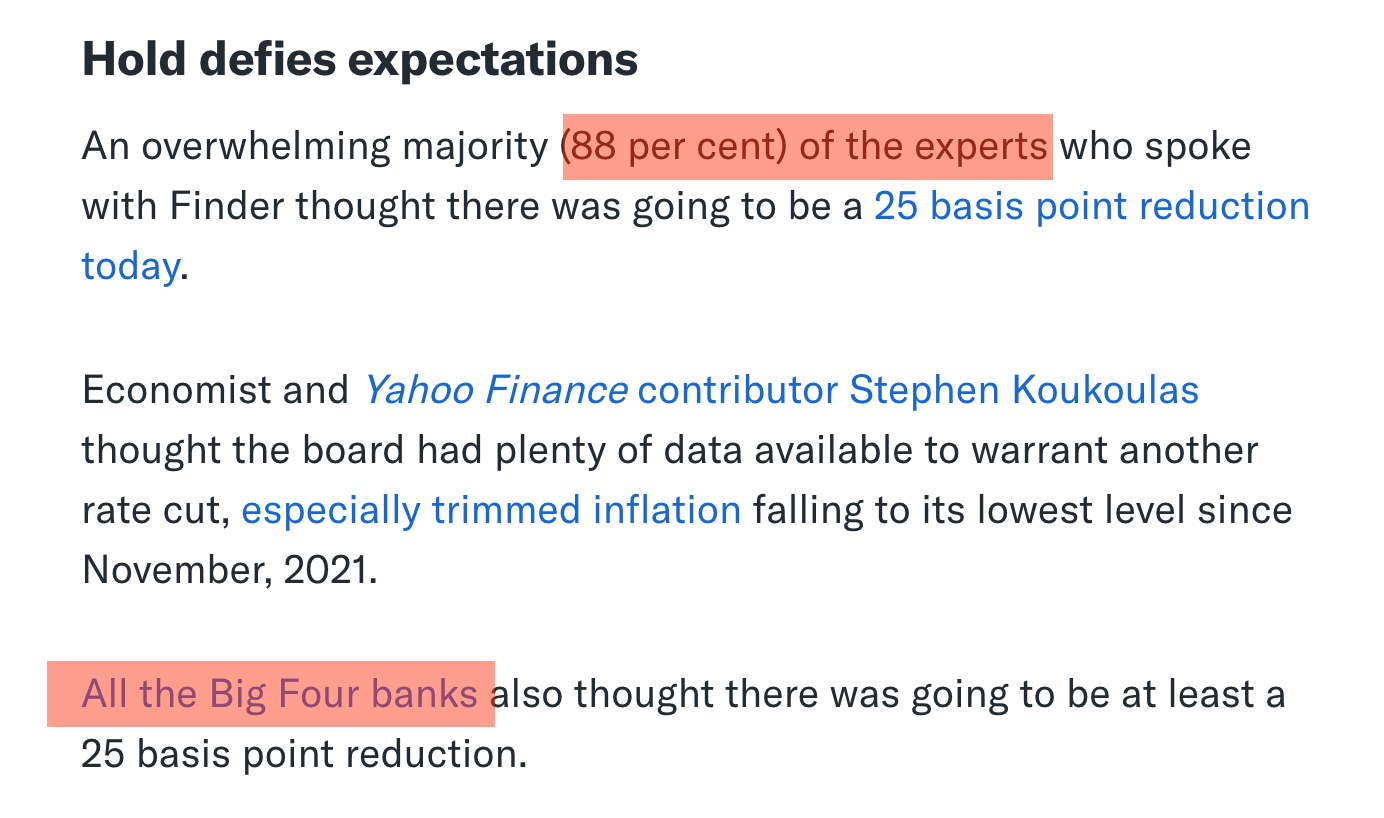

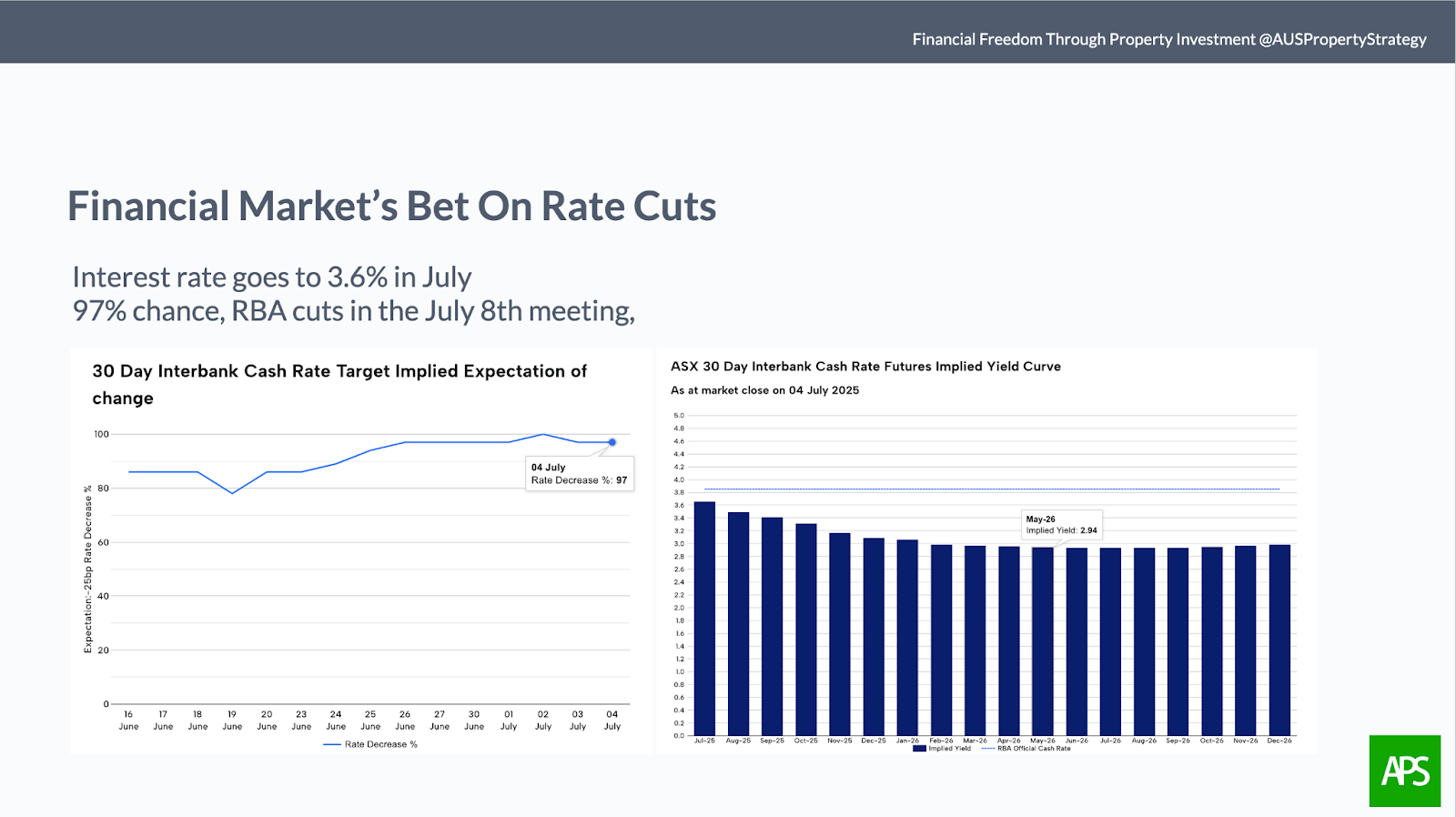

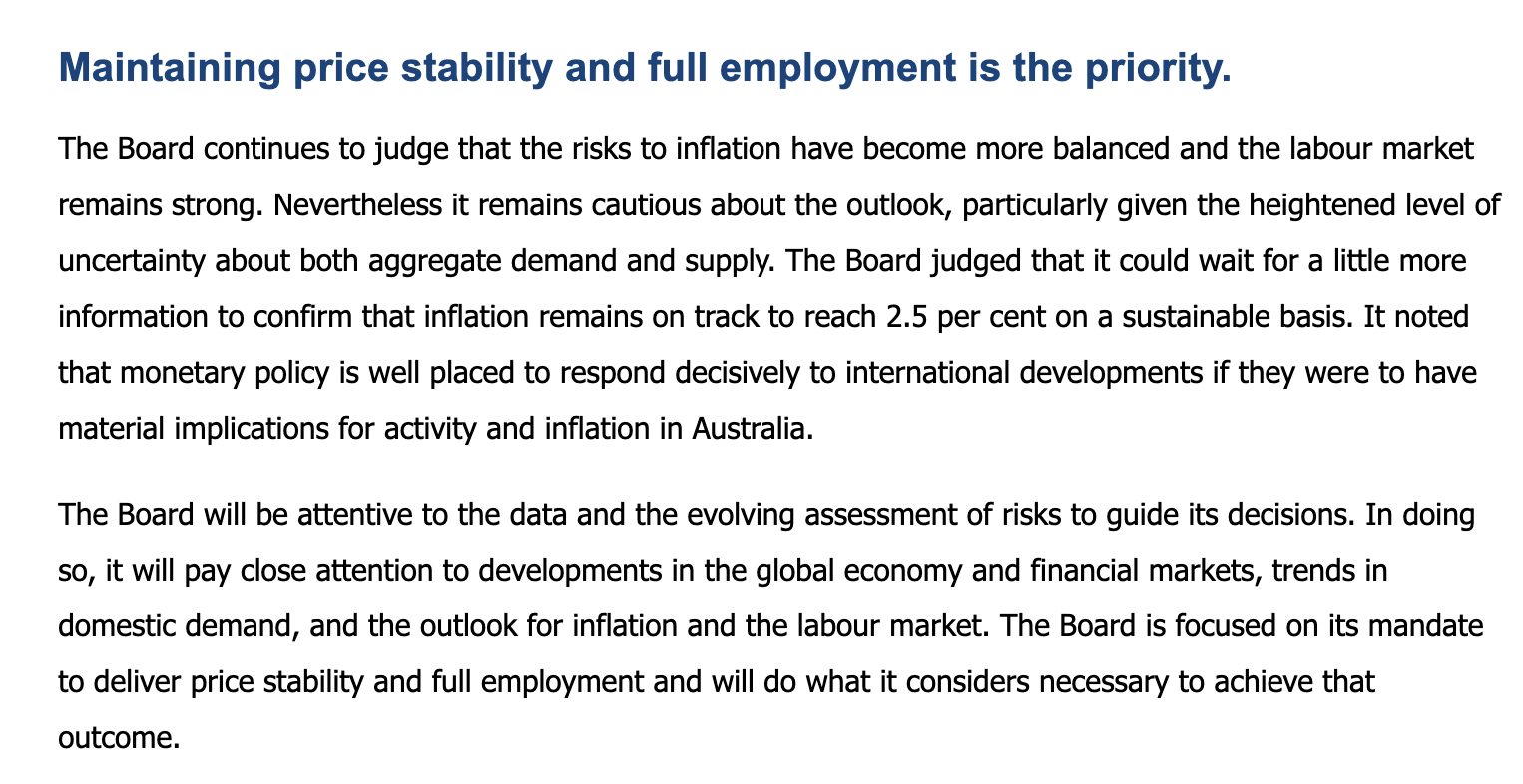

Before the RBA's meeting, the financial markets had basically made up their minds: there was a 97% chance that the Reserve Bank would cut rates by 0.25%. Most forecasts expected the cash rate to drop to around 3% between March and June next year. This wasn't just speculation from traders—economists, major banks, and even myself were convinced that a rate cut was coming. But this time, the RBA caught everyone off guard. They didn't give anyone what they were hoping for. No rate cut. Just like that. Looks like the current RBA governor really doesn't follow the usual playbook. So, I dug into the RBA's statement, and uncovered several key reasons behind this surprising pause.

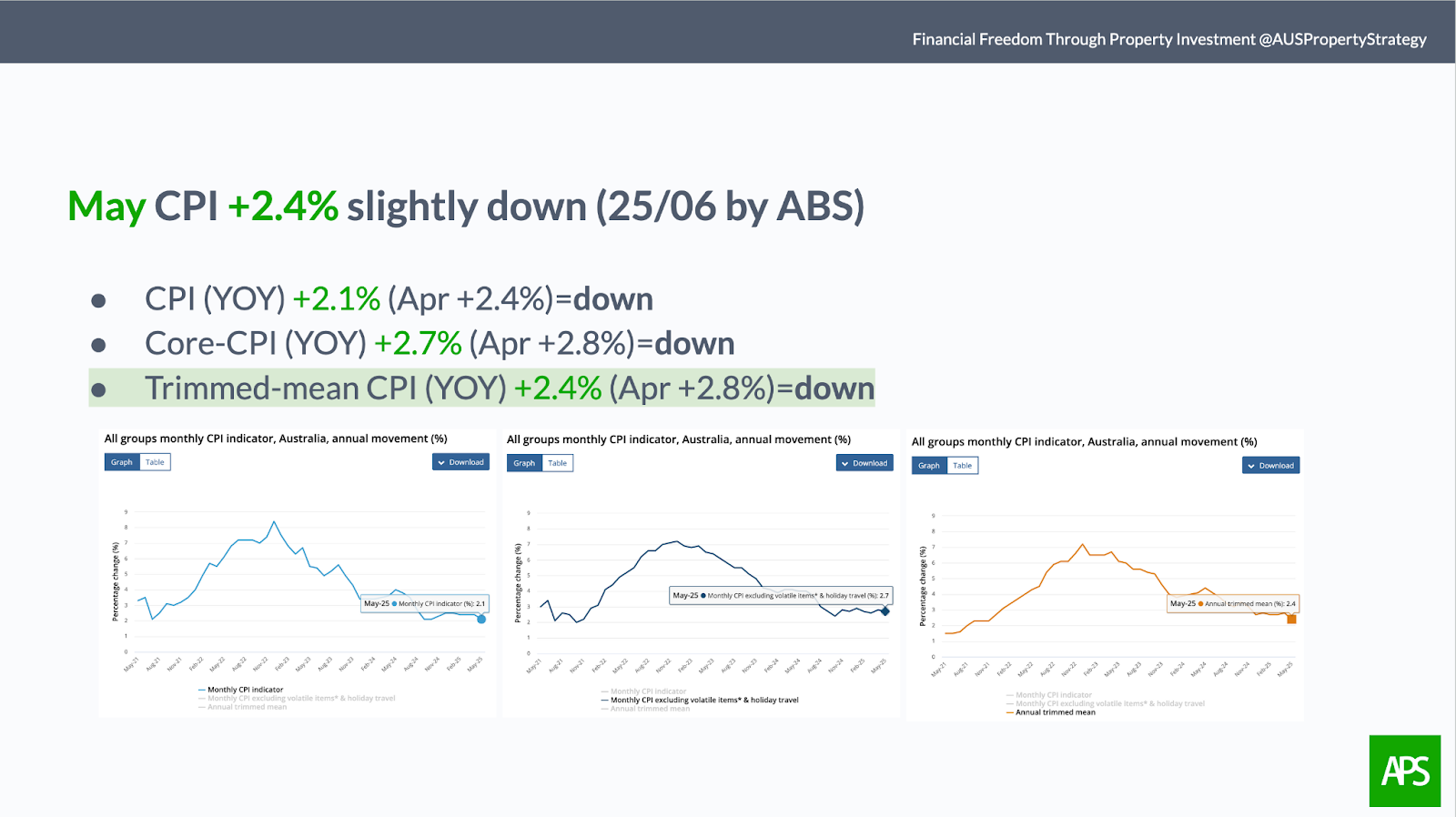

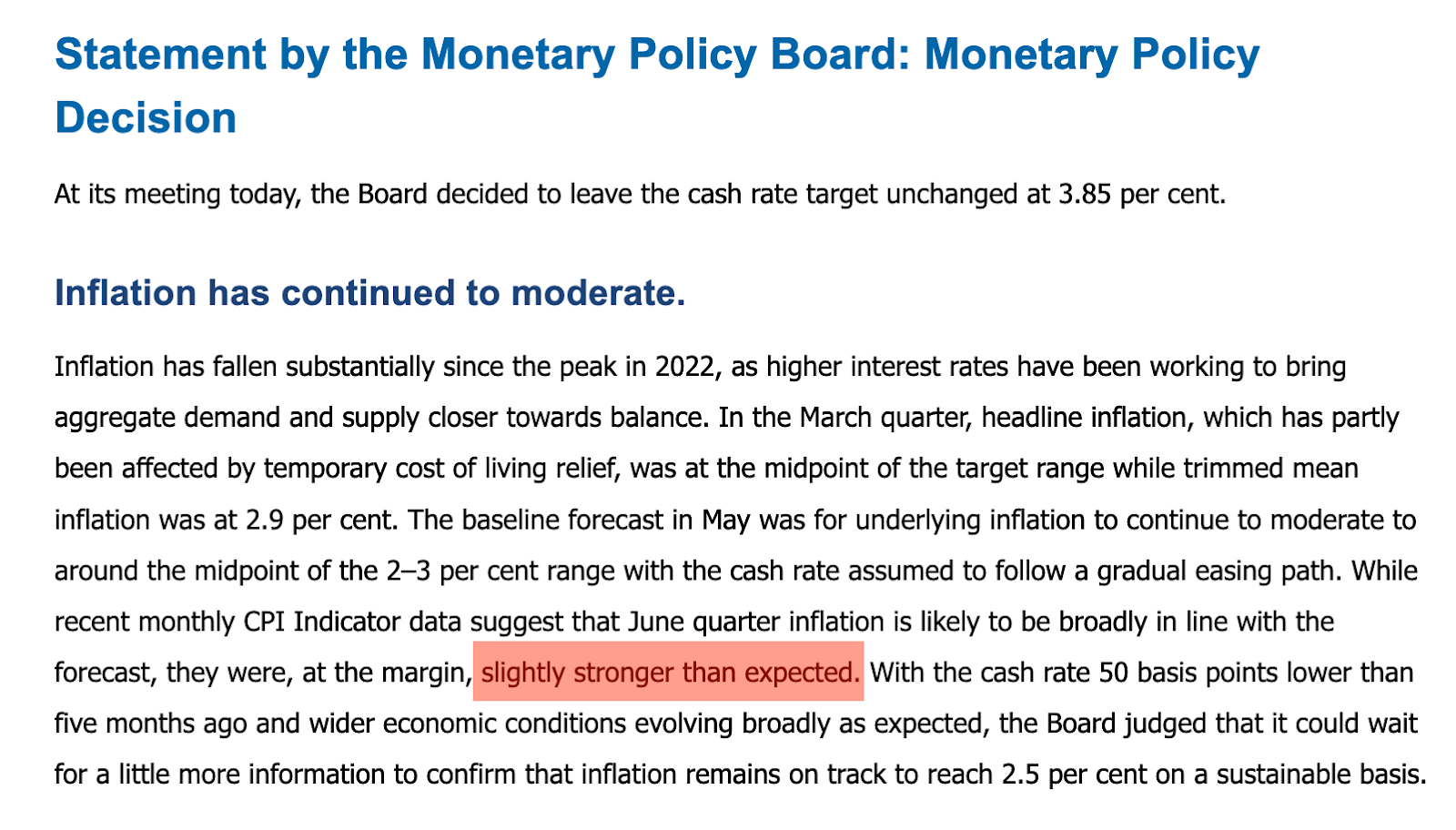

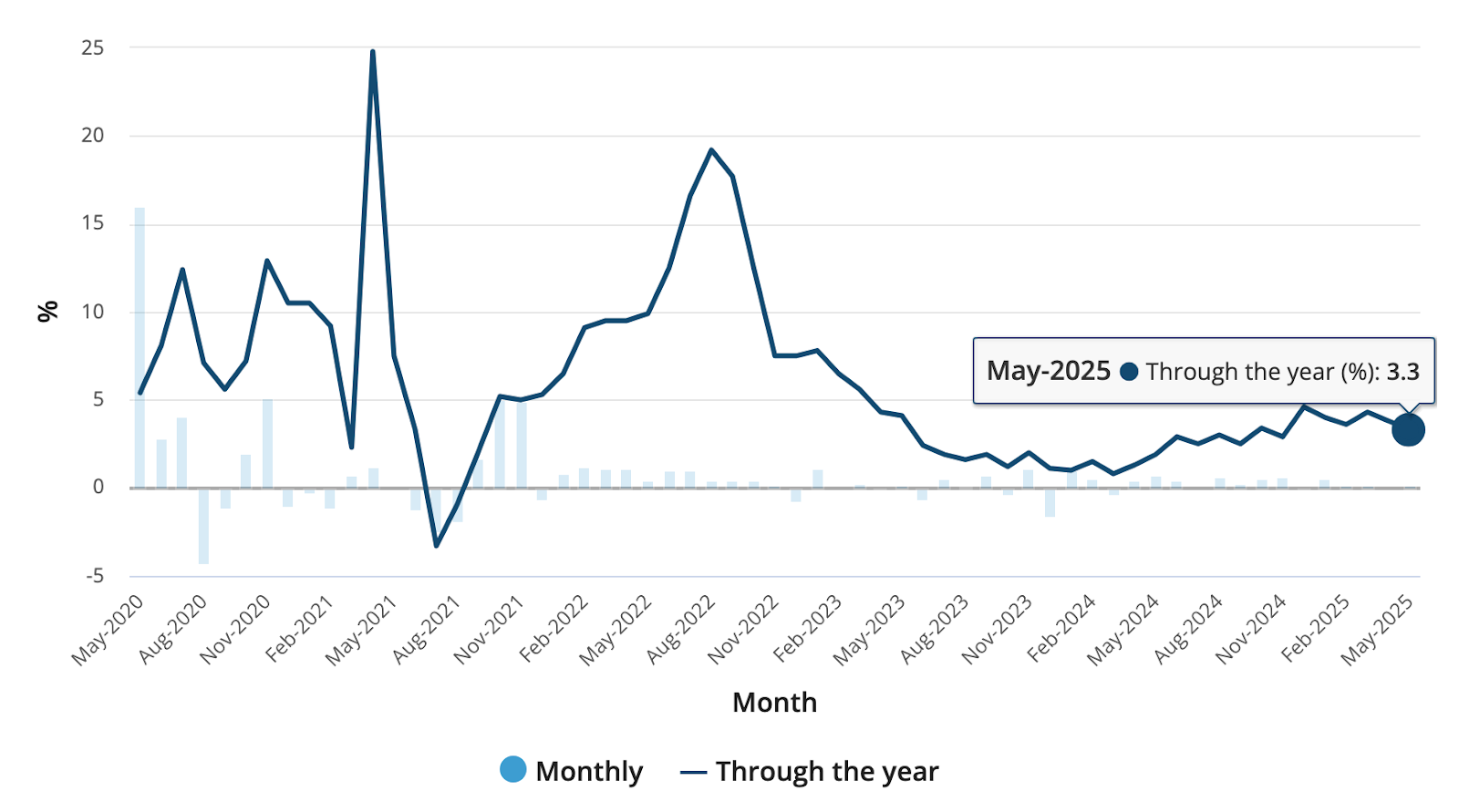

1.— Inflation has droppedbut not in the way the RBA wants. Since the peak in 2022, inflation has fallen sharply. In May, the trimmed mean CPI dropped from 2.8% in April to 2.4%. Technically, this is already within the RBA's 2–3% target range. Even at the midpoint, we're looking at under 2.5%. So logically, a rate cut would make sense. But reading the RBA's Statement, I noticed a different tone.

They said: "Recent data suggests second-quarter inflation may come in slightly higher than expected." Wait—what? Let me explain. Australia's Bureau of Statistics has two kinds of inflation data: Monthly data, released at the end of each month for the previous month. Quarterly data, released 25 to 30 days after each quarter ends.

So officially, second-quarter inflation data won't be available until the end of this month. But the RBA clearly has access to internal forecasts or early indicators—suggesting inflation might be picking up again. That's why they're holding off. They want to wait and see inflation stabilise around 2.5%. My guess? They want to see three months hovering around that mark before making a move.

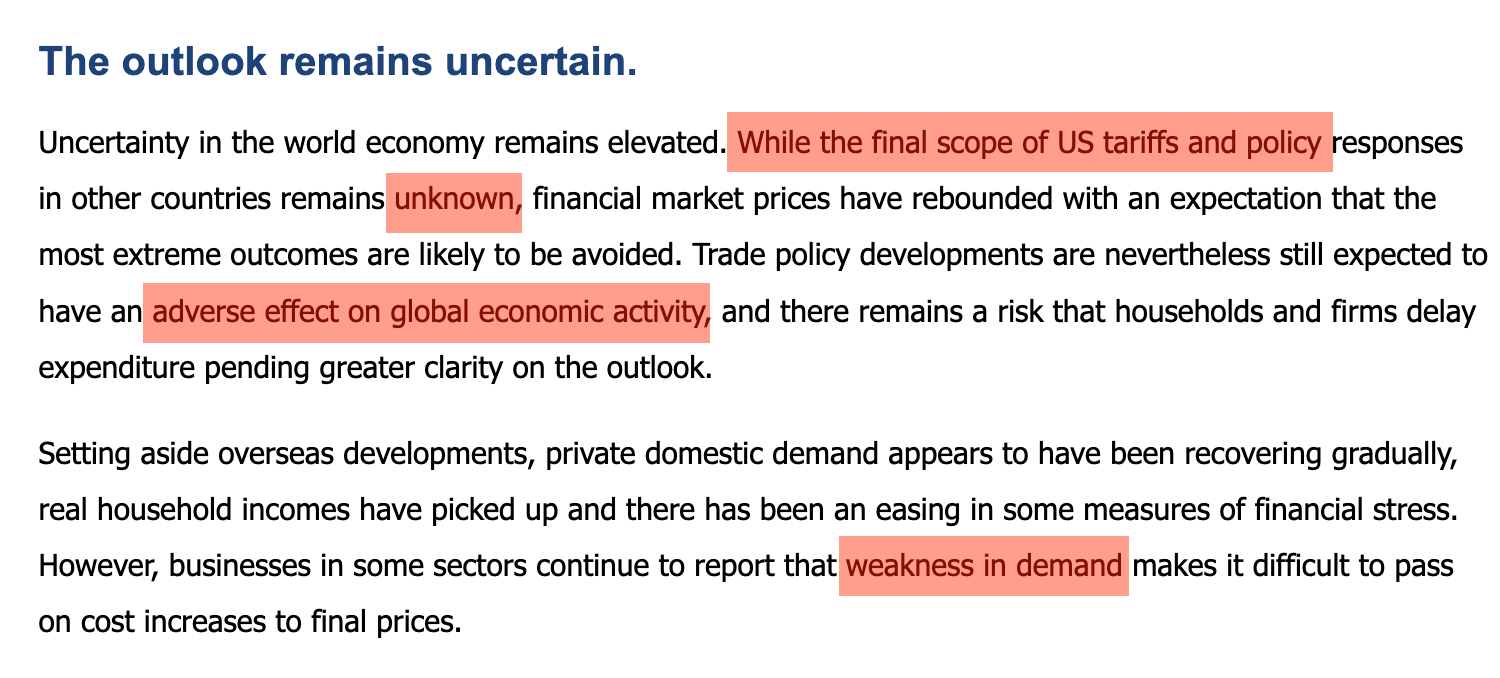

2. Global and domestic uncertainty is rising. On April 9, the U.S. announced a 90-day pause on new tariffs—set to expire on July 9. But then the Treasury Secretary pushed the deadline further to August 1. So now, nobody really knows what the final tariff policy will look like. The RBA flagged this as a key source of global uncertainty in their statement. They also mentioned weakening domestic demand as a reason to hold off. I think they were referring to the soft May retail sales figures, which showed slowing momentum. That means consumer sentiment still isn't strong enough to sustain rapid growth. Now, you'd think weak consumer demand would be a reason to cut rates… right? But the RBA's message is clear: soft consumption alone isn't enough to justify a rate cut. Or maybe they're waiting for things to get worse before acting. In their eyes, the situation isn't serious enough.

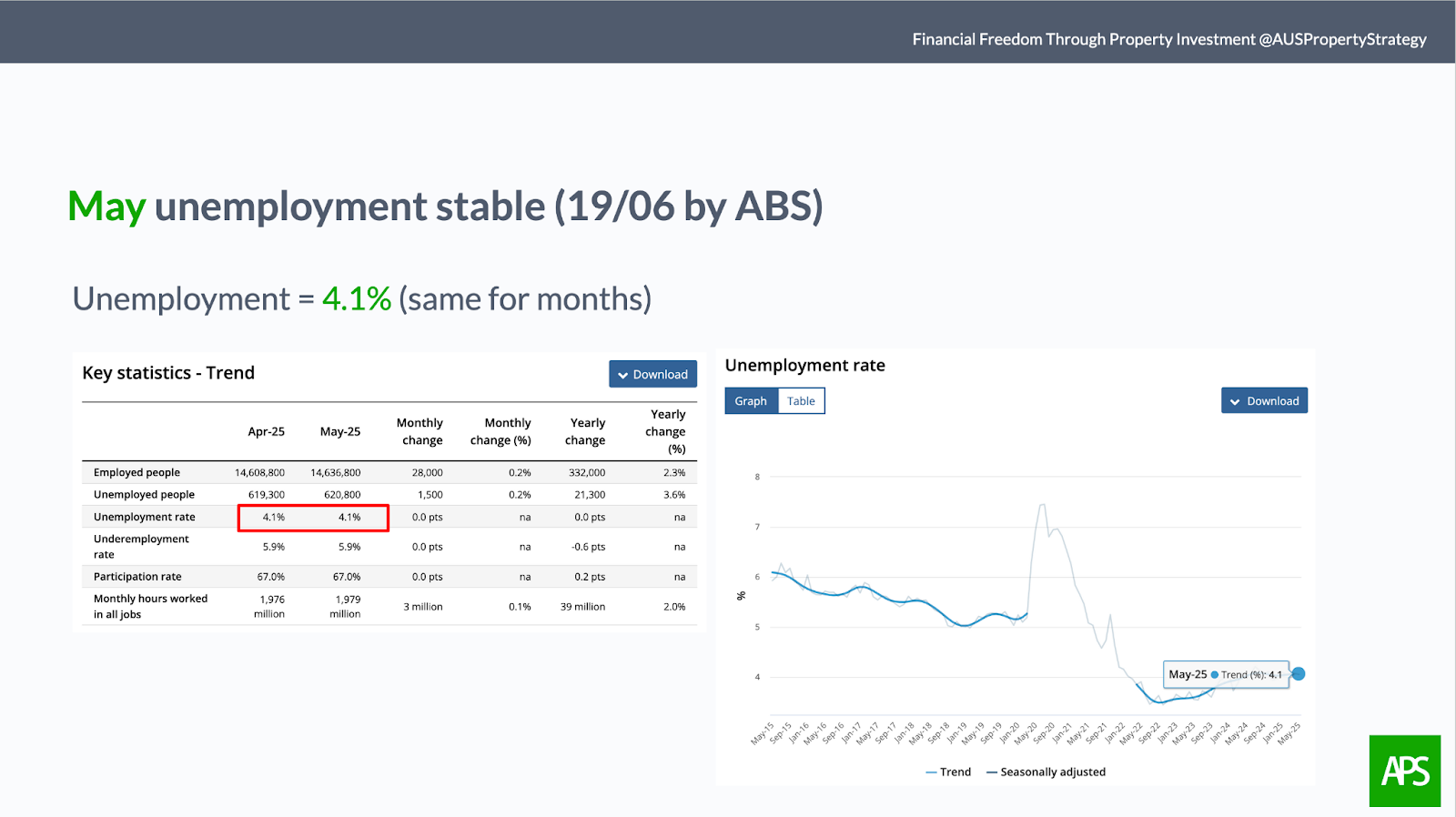

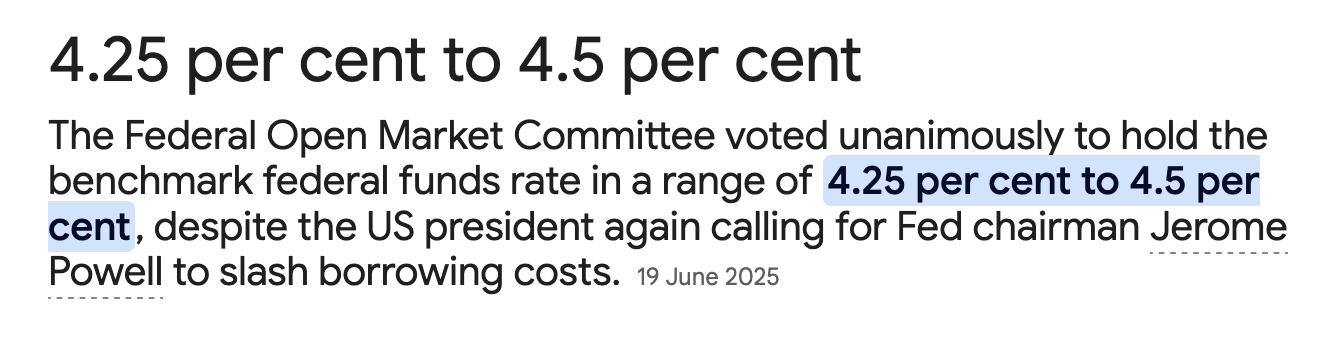

3. The job market remains strong. Unemployment has held steady at 4.1% for about six months now, with no signs of deterioration. The RBA emphasised its dual mandate: keeping inflation stable and supporting full employment. So maybe I'm missing something. Maybe the RBA sees trouble ahead—and wants to hold off while the Economy is still holding up. Or maybe they're just taking their cues from the U.S. Federal Reserve, which also decided not to cut rates in late June. And the RBA wants to wait and see what the Fed does next.

With all these questions, I ran a quick research online. The responses I got show there are a few possible explanations:

1. Rates have already been cut by 50 basis points from their peak. The RBA feels it can wait.

2. The effects of the last two cuts haven't fully played out yet—there's still a time lag.

3. The data simply isn't convincing enough. So, no cut.

The next RBA meeting is set for August 12. And once again, the markets are saying: "This time for sure—rate cut guaranteed." But after this latest surprise, I think more and more people are going to stop taking those forecasts seriously. This uncertainty—combined with the current pause—could have a real impact on the property market. So why did I say at the start of this video that this might be the last window for people who haven't bought a property yet?

To Buy or Not to Buy—That's the Question

Australia's housing market flipped back into growth mode in February this year. By the end of June, we had already seen five straight months of rising prices. And the growth is accelerating across nearly every major city. Buyers were starting to regain confidence. But now, this pause in rate cuts might shake that optimism. In cities where the housing market was rapidly picking up pace, that momentum might now slow down—or at least pause—until the next rate cut is officially locked in. In the meantime, many buyers will adopt a wait-and-see attitude. That fear of missing out could fade. And auction clearance rates could dip as a result.

Of course, I'm talking about the majority of buyers—because, let's face it, most people buy based on emotion. When the emotion kicks in, they buy immediately. But as property investors, we have to go against human nature if we want to succeed. As long as we're confident about the short-term outlook (next 12 months) and the long-term trend (next 10 years), this next month or so could be the best time to get in. In fact, you may even be able to negotiate a better deal—simply because some other buyers are pausing. Those who delay their purchases just because of this rate cut pause… may end up missing a rare opportunity in the market.

I'm hosting a monthly live webinar to provide you with the latest updates on the Australian Property Market, the Australian Economy, and market predictions. You can also ask all the questions you want. There is a poll in the post section regarding the day and time; please let me know your preference.

Watch the video version of the blog on YouTube.